Mini Case: 4 -37

or in part.

l. 2. What is the PV of the same stream?

Answer: 0 1 2 3

| | | | | | |

100 100 100

l. 3. Is the stream an annuity?

l. 4. An important rule is that you should never show a nominal rate on a time line or

use it in calculations unless what condition holds? (Hint: Think of annual

compounding, when INOM = EFF% = IPER.) What would be wrong with your

answer to questions l(1) and l(2) if you used the nominal rate (10%) rather than

the periodic rate (INOM /2 = 10%/2 = 5%)?

5%

Mini Case: 4 – 38

or in part.

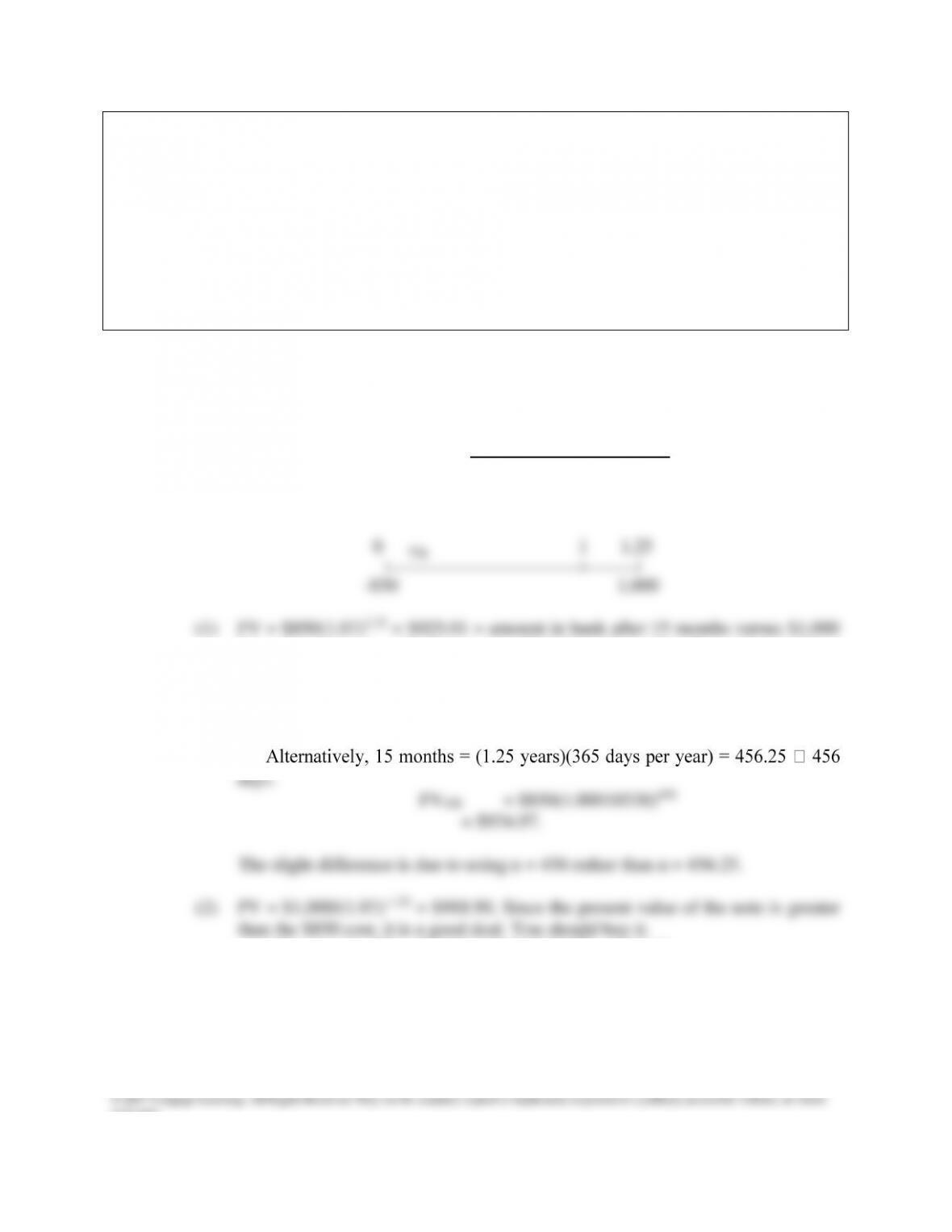

m. Suppose someone offered to sell you a note calling for the payment of $1,000 15

months from today. They offer to sell it to you for $850. You have $850 in a

bank time deposit which pays a 6.76649% nominal rate with daily compounding,

which is a 7% effective annual interest rate, and you plan to leave the money in

the bank unless you buy the note. The note is not risky—you are sure it will be

paid on schedule. Should you buy the note? Check the decision in three ways:

(1) by comparing your future value if you buy the note versus leaving your

money in the bank, (2) by comparing the PV of the note with your current bank

account, and (3) by comparing the EFF% on the note versus that of the bank

account.

Answer: You can solve this problem in three ways—(1) by compounding the $850 now in the

bank for 15 months and comparing that FV with the $1,000 the note will pay, (2) by

finding the PV of the note and then comparing it with the $850 cost, and (3) finding

the effective annual rate of return on the note and comparing that rate with the 7%

you are now earning, which is your opportunity cost of capital. All three procedures

lead to the same conclusion. Here is the time line:

if you buy the note. (Again, you can find this value with a financial calculator.

Note that certain calculators like the hp 12c perform a straight-line interpolation

for values in a fractional time period analysis rather than an effective interest

rate interpolation. The value that the hp 12c calculates is $925.42.) This

procedure indicates that you should buy the note.

Alternatively, PV = $1000/(1.00018538)456 = $918.95.

Mini Case: 4 -39

© 2017 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole

or in part.

(3) FVN = PV(1 + I)N, So $1,000 = $850(1 + i)1.25 = $1,000. Since we have an

equation with one unknown, we can solve it for i. You will get a value of i =

13.88%. The easy way is to plug values into your calculator. Since this return

is greater than your 7% opportunity cost, you should buy the note. This action

will raise the rate of return on your asset portfolio.

Alternatively, we could solve the following equation:

Web Extension 4C Continuous Compounding and Discounting

Solutions to Problems

4C-1 FV15 = $15,000e0.06(15) = $36,894.05.

Continuous compounding:

4C-4 Calculate the growth factor using PV and FV which are given:

Inputs: 2.0. Press LN key. Output: LN = 0.6931.

I(6)ln e = ln 2.0

I(6) = 0.6931

I = 0.1155 = 11.55%.

Web Extension 4C: 4 –41

or in part.

4C-7 e(0.03)(10) =

20

NOM

2

I

1

e0.3 =

20

NOM

2

I

1

INOM

2

2

INOM = 0.0302 = 3.02%.

Step 2: Calculate the PV or initial deposit: