420

421

422

423

424

425

426

427

428

429

430

431

432

433

434

435

438

439

440

441

442

443

449

450

451

452

453

454

455

456

460

461

462

463

464

469

476

477

478

A B C D E F G H I J K

N3

I0.1

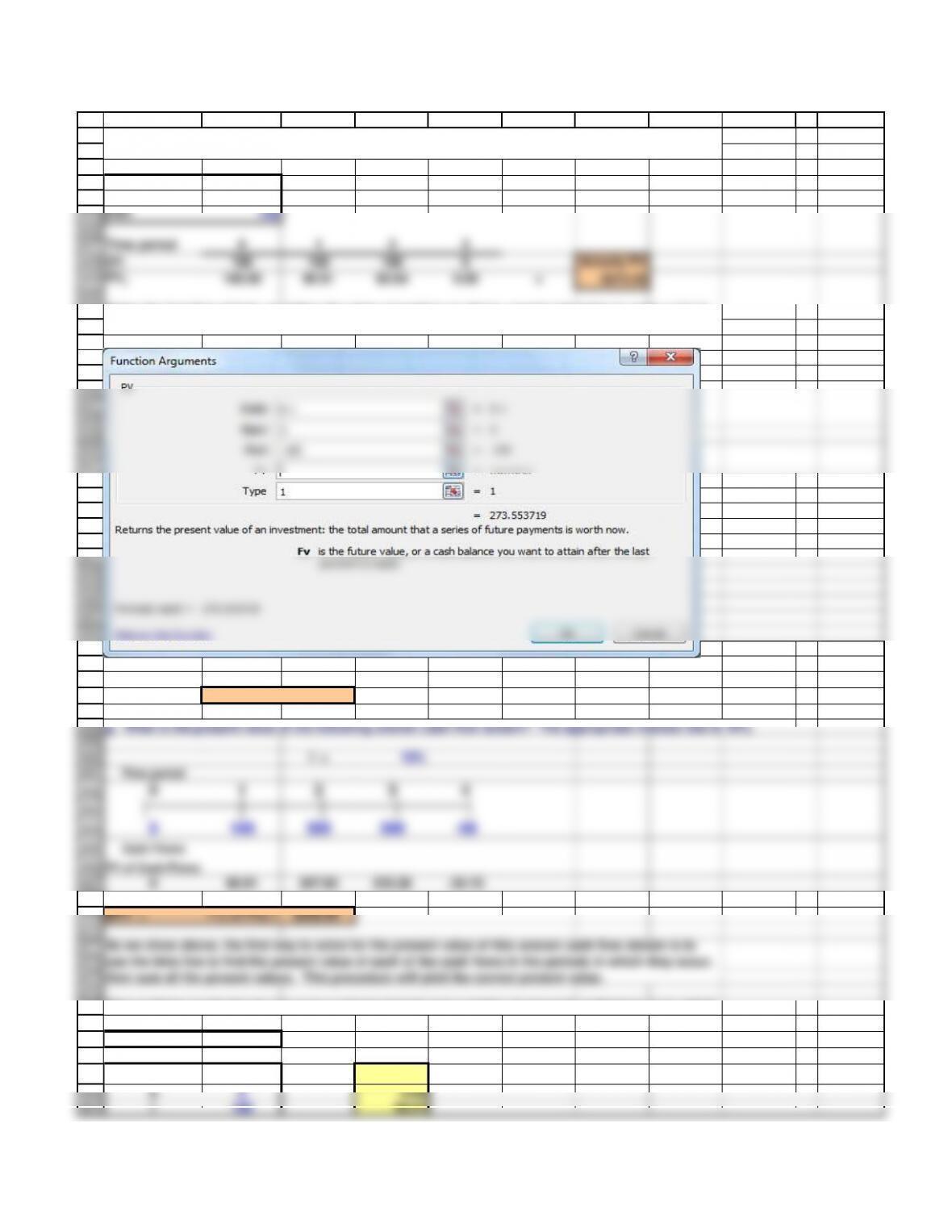

PMT 100

Time period 0 1 2 3

CFt100 100 100 0 Annuity PV

PV3100.00 90.91 82.64 0.00 = $273.55

I = 10%

Time period

0 1 2 3 4

0100 300 300 -50

Using the function wizard, we follow the same procedure as above, except remember to enter a “1” to

tell Excel that in this problem the payments occur at the beginning of the periods.

To find the present value of the annuity due, this problem is solved just like the previous problem,

except that the payments occur in periods 0 through 2.

482

483

484

485

486

487

488

489

492

493

494

496

497

498

499

500

507

508

509

510

511

516

517

518

519

520

521

522

523

524

525

360 or 365 for annual compounding.

528

529

530

531

532

533

538

540

541

542

543

544

A B C D E F G H I J K

2300 247.93

3300 225.39

4-50 -34.15

$530.09

Or

Inputs

m=periods/yr 2This is the number of periods per year, m.

IPER = inom/m

IPER = 10% / 2

IPER = 5%

EFF% = (1+ INOM/M)M

EFF% = (1 + (10%/2))^2 – 1

h. (1.) Identify (a) the stated, or quoted, or nominal rate (iNom) and (b) the periodic rate (iPER).

With, the financial calculator, we could enter each of these cash flows and the discount rate, and

simply press NPV for the present value of the cash flow stream. In Excel, we can perform a similar

time period zero. However, the “NPV” function interprets the first data entry as being the cash flow in

time period one. Therefore, the initial cash flow must be added seperately. In this particular example,

the initial cash flow is zero.

Larger, because interest is earned on interest.

PV of CF stream =

compounding periods.

546

547

548

549

550

551

552

553

554

555

556

557

559

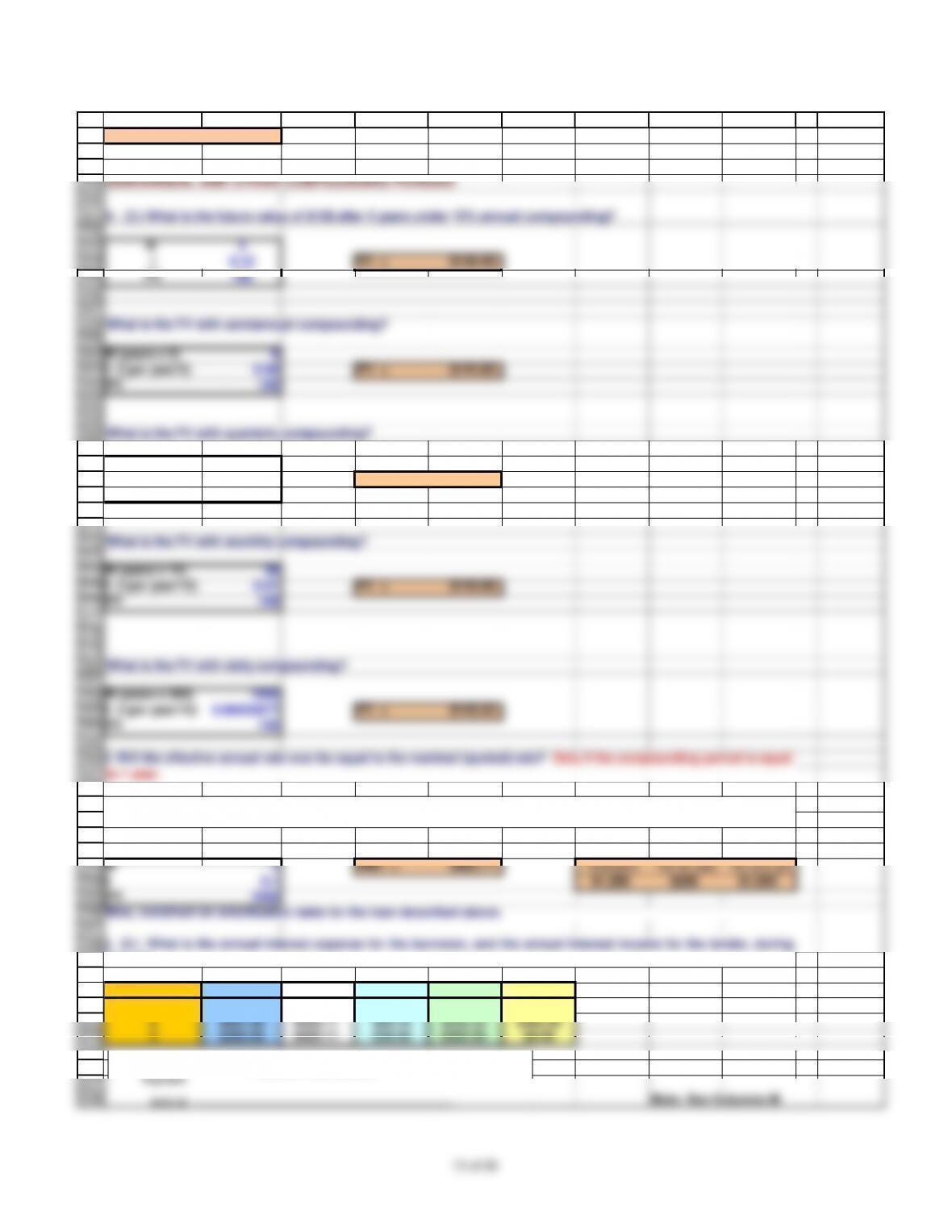

What is the FV with semiannual compounding?

560

561

562

563

564

565

566

567

568

569

570

573

What is the FV with monthly compounding?

574

575

576

577

578

579

What is the FV with daily compounding?

581

582

583

584

585

586

587

588

589

590

591

592

593

594

596

597

598

599

600

601

602

603

604

605

607

608

A B C D E F G H I J K

EFF% = 10.25%

SEMIANNUAL AND OTHER COMPOUNDING PERIODS

h. (3.) What is the future value of $100 after 5 years under 12% annual compounding?

N 3

I0.12 FV = $140.49

PV 100

N (years x 2) 6

I (I per year/2) 0.06 FV = $141.85

PV 100

What is the FV with quarterly compounding?

N (years x 4) 12

I (I per year/4) 0.03 FV = $142.58

PV 100

N (years x 12) 36

I (I per year/12) 0.01 FV = $143.08

PV 100

N (years x 365) 1095

I (I per year/12) 0.00032877 FV = $143.32

PV 100

NBeg. Amt. Payment Interest Principal End. Amt.

1 $1,000.00 $402.11 $100.00 $302.11 $697.89

2 $697.89 $402.11 $69.79 $332.33 $365.56

3 $365.56 $402.11 $36.56 $365.56 $0.00

Note: See Columns M

Now, construct an amortization table for the loan described above.

j. (1.) What would the required payment be on a $1,000 loan that is to be repaid in three equal installments at the

end of each of the next three years if the interest rate is 10%?

I. Will the effective annual rate ever be equal to the nominal (quoted) rate? Only if the compounding period is equal

to 1 year.

j. (2.) What is the annual interest expense for the borrower, and the annual interest income for the lender, during

Year 2?

$450.00

Payment

13 of 30

609

610

611

612

613

614

615

616

617

618

619

620

624

625

626

627

628

634

635

636

637

638

639

640

646

647

648

649

650

655

Periods 0 1.0 2 3.0 4 5.0 6

FV of CF $121.55 $110.25 $100.00

657

658

659

660

663

664

Annual effective rate = 10.25%

FV = $331.80

A B C D E F G H I J K

through R for a 30 year

mortgage example.

I0.00031054

N273

FV $108.85

Years 0 0.5 1 1.5 2 2.5 3

Periods 0 1.0 2 3.0 4 5.0 6

Cash Flow 0 100 0100 0100

Total FV = Σ = $331.80

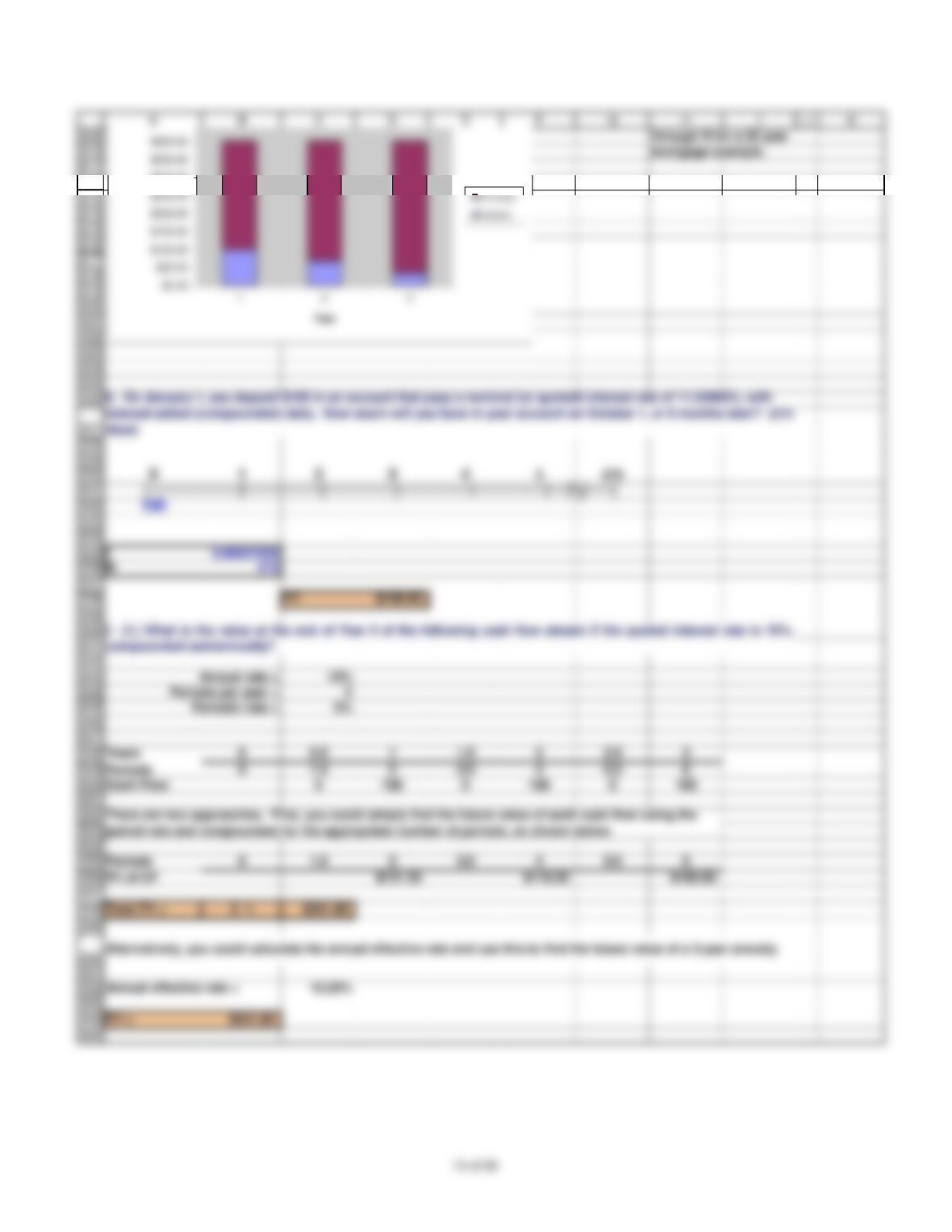

k. On January 1, you deposit $100 in an account that pays a nominal (or quoted) interest rate of 11.33463%, with

interest added (compounded) daily. How much will you have in your account on October 1, or 9 months later? (273

days)

l. (1.) What is the value at the end of Year 3 of the following cash flow stream if the quoted interest rate is 10%,

Alternatively, you could calculate the annual effective rate and use this to find the future value of a 3-year annuity.

$0.00

$50.00

$100.00

$150.00

$200.00

$250.00

$300.00

$350.00

$400.00

$450.00

1 2 3

Year

Principal

Interest

666

667

668

669

670

671

672

673

674

676

677

678

679

680

681

682

684

685

686

687

688

689

690

691

See which provides the greater future wealth

698

699

700

701

702

703

704

705

708

709

710

711

712

713

715

716

717

See which has the higher effective rate of return, EFF%

720

721

722

723

724

A B C D E F G H I J K

Periods 0 1 2 3.0 4 5.0 6

PV of CF $90.70 $82.27 $74.62

In the second approach, we use the annual effective rate to find the present value of a 3-year annuity.

PV = $247.59

0 1 2 3 4 5456

850

I0.00018538

0 1 2 3 4 5456

1000

0 1 2 3 4 5456

850 1000

what condition holds? (Hint: Think of annual compounding, when iNOM = EAR = iPER.) What would be wrong with

your answer to questions l(1) and l(2) if you used the nominal rate (10%) rather than the periodic rate (iNOM/2 = 10%/2

l. (2.) What is the PV of the same stream?

See which has the greater present value

m. Suppose someone offered to sell you a note calling for the payment of $1,000 in 15 months (or 456 days). They

offer to sell it to you for $850. You have $850 in a bank time deposit that pays a 6.76649% nominal rate with daily

compounding, which is a 7% effective annual interest rate, and you plan to leave the money in the bank unless you

buy the note. The note is not risky–you are sure it will be paid on schedule. Should you buy the note? Check the

l. (3.) Is the stream an annuity? No, because we don’t have a payment for each compounding period.

Using the first approach, we find the present value of each individual cash flow using the periodic rate

and the number of periods.

727

728

729

A B C D E F G H I J K

I 0.035646% per day

EAR 13.89% > 7% so buy the note.

16 of 30

1

2

3

4

5

6

7

8

9

10

11

12

13

14

L M N O P Q R S

57

58

59

60

61

62

63

64

69

70

71

72

73

80

81

82

83

84

91

92

93

94

101

102

103

104

105

106

113

114

115

116

117

L M N O P Q R S

119

120

121

122

123

124

125

126

127

128

129

130

131

132

133

134

135

136

137

138

139

L M N O P Q R S

140

141

142

143

144

145

146

147

152

153

154

155

156

157

163

164

165

166

167

168

174

175

176

177

178

179

185

186

187

188

189

190

196

197

198

199

200

201

L M N O P Q R S