Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Ch25 Mini Case.xlsx Mini Case

10/28/2015

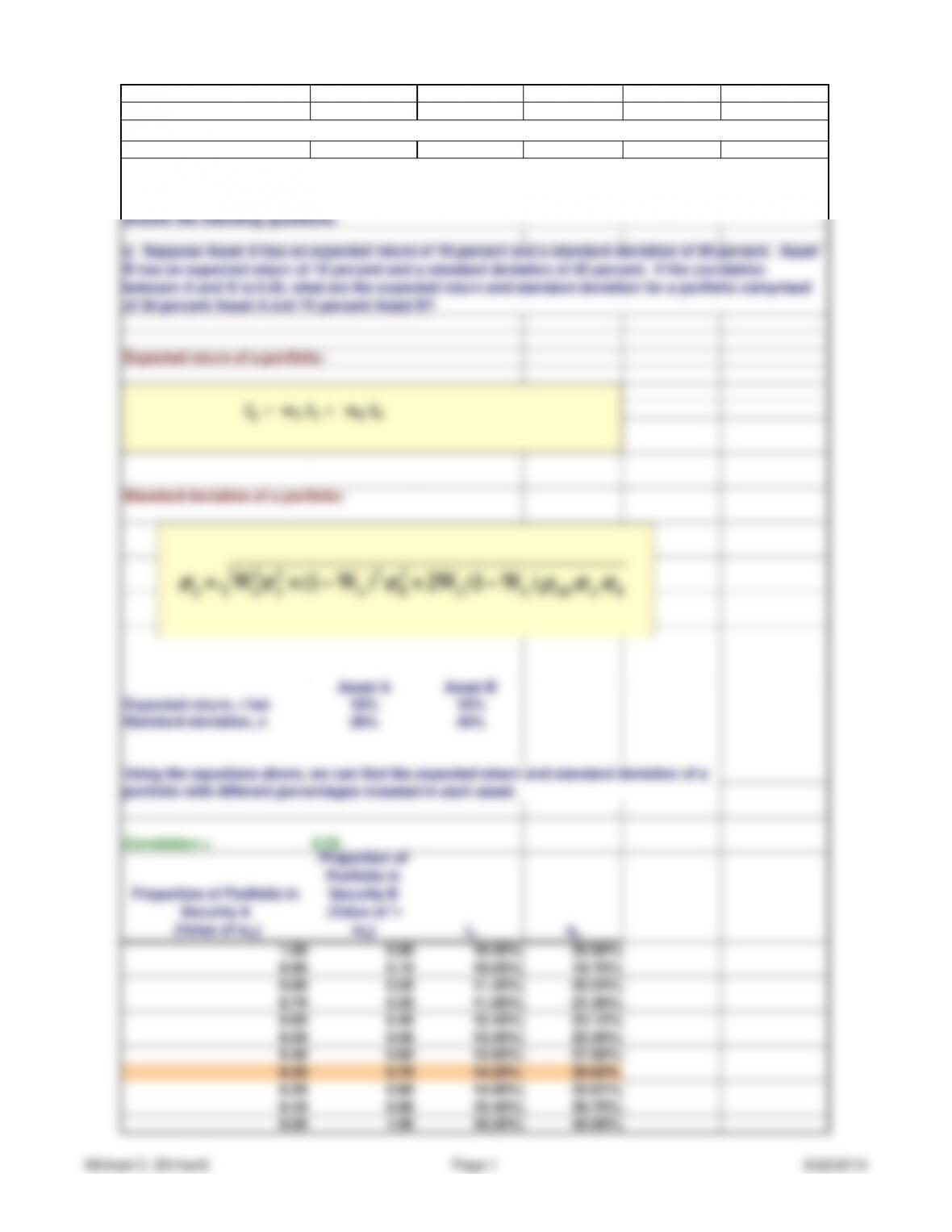

Expected return of a portfolio:

Standard deviation of a portfolio:

Asset A Asset B

Expected return, r hat 10% 16%

Standard deviation, s20% 40%

Correlation = 0.35

Proportion of Portfolio in

Security A

(Value of wA)

Proportion of

Portfolio in

Security B

(Value of 1-

wA)

rpsp

1.00 0.00 10.00% 20.00%

0.90 0.10 10.60% 19.76%

0.80 0.20 11.20% 20.24%

0.70 0.30 11.80% 21.39%

0.60 0.40 12.40% 23.12%

0.50 0.50 13.00% 25.30%

0.40 0.60 13.60% 27.83%

0.30 0.70 14.20% 30.62%

0.20 0.80 14.80% 33.61%

0.10 0.90 15.40% 36.75%

0.00 1.00 16.00% 40.00%

Chapter 25. Mini Case

a. Suppose Asset A has an expected return of 10 percent and a standard deviation of 20 percent. Asset

B has an expected return of 16 percent and a standard deviation of 40 percent. If the correlation

between A and B is 0.35, what are the expected return and standard deviation for a portfolio comprised

of 30 percent Asset A and 70 percent Asset B?

Using the equations above, we can find the expected return and standard deviation of a

portfolio with different percentages invested in each asset.

You have been hired at the investment firm of Bowers & Noon. One of its clients doesn’t understand the

value of diversification or why stocks with the biggest standard deviations don’t always have the highest

expected returns. Your assignment is to address the client’s concerns by showing the client how to

answer the following questions.

BAABAA

2

B

2

A

2

A

2

Ap )W1(W2)W1(W

sssss

��= �

�+ �

�

Michael C. Ehrhardt Page 1 9/22/2019

Ch25 Mini Case.xlsx Mini Case

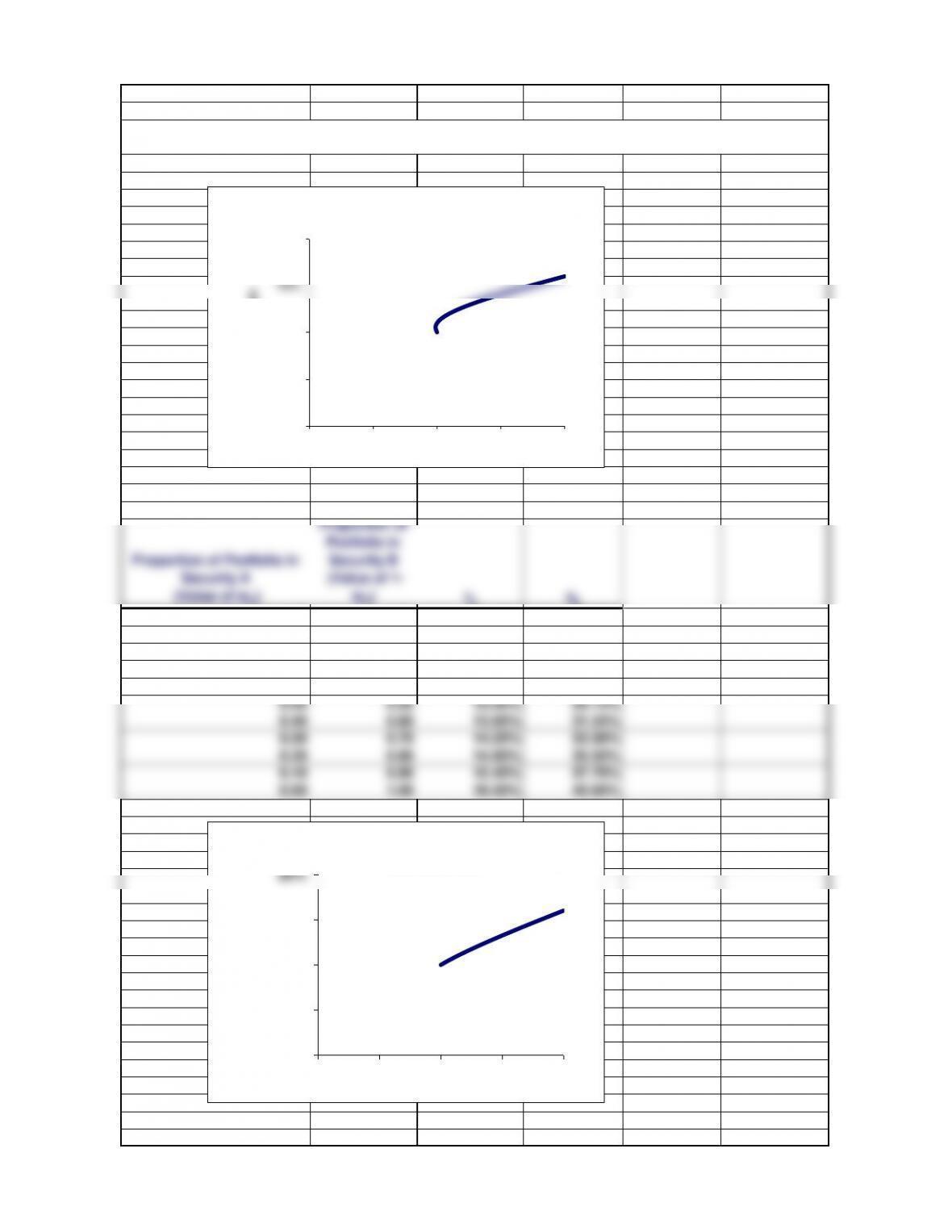

Correlation = 1

Proportion of Portfolio in

Security A

(Value of wA)

Proportion of

Portfolio in

Security B

(Value of 1-

wA)

rpsp

1.00 0.00 10.00% 20.00%

0.90 0.10 10.60% 21.59%

0.80 0.20 11.20% 23.32%

0.70 0.30 11.80% 25.18%

0.60 0.40 12.40% 27.13%

0.50 0.50 13.00% 29.15%

0.40 0.60 13.60% 31.24%

0.30 0.70 14.20% 33.38%

0.20 0.80 14.80% 35.55%

0.10 0.90 15.40% 37.76%

0.00 1.00 16.00% 40.00%

b. Plot the attainable portfolios for a correlation of 0.35. Now plot the attainable portfolios for

correlations of +1.0 and -1.0.

0%

5%

10%

15%

20%

0% 10% 20% 30% 40%

Expected return

Risk, sp

AB = +0.35: Attainable Set of Risk/Return

Combinations

0%

5%

10%

15%

20%

0% 10% 20% 30% 40%

Expected return

Risk, sp

AB = +1.0: Attainable Set of Risk/Return

Combinations

Ch25 Mini Case.xlsx Mini Case

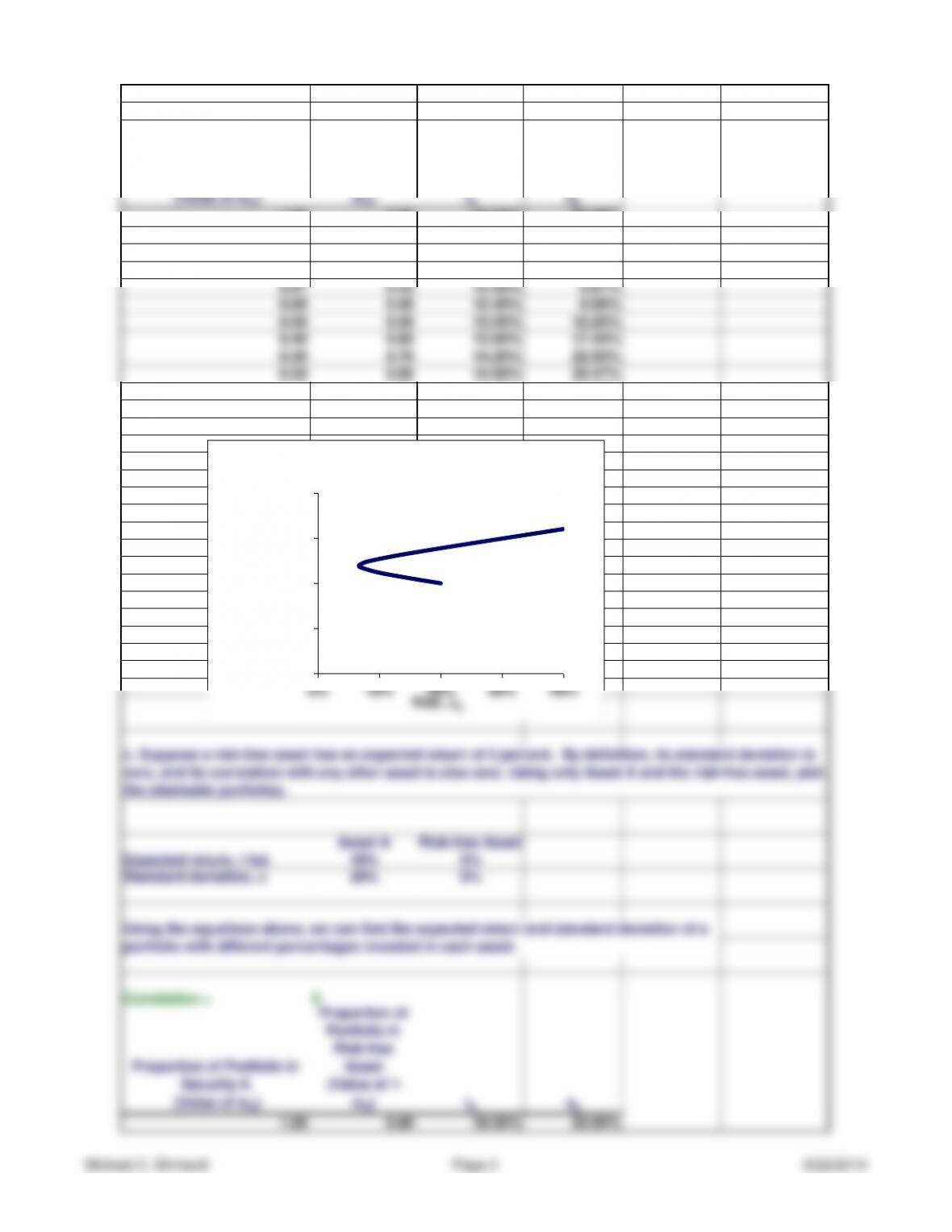

Correlation = -1

Proportion of Portfolio in

Security A

(Value of wA)

Proportion of

Portfolio in

Security B

(Value of 1-

wA)

rpsp

1.00 0.00 10.00% 20.00%

0.90 0.10 10.60% 14.63%

0.80 0.20 11.20% 9.80%

0.70 0.30 11.80% 6.78%

0.67 0.33 12.00% 6.67%

0.60 0.40 12.40% 8.00%

0.50 0.50 13.00% 12.25%

0.40 0.60 13.60% 17.44%

0.30 0.70 14.20% 22.93%

0.20 0.80 14.80% 28.57%

0.10 0.90 15.40% 34.26%

0.00 1.00 16.00% 40.00%

Asset A Risk-free Asset

Expected return, r hat 10% 5%

Standard deviation, s20% 0%

Correlation = 0

Proportion of Portfolio in

Security A

(Value of wA)

Proportion of

Portfolio in

Risk-free

Asset

(Value of 1-

wA)

rpsp

1.00 0.00 10.00% 20.00%

Using the equations above, we can find the expected return and standard deviation of a

portfolio with different percentages invested in each asset.

c. Suppose a risk-free asset has an expected return of 5 percent. By definition, its standard deviation is

zero, and its correlation with any other asset is also zero. Using only Asset A and the risk-free asset, plot

the attainable portfolios.

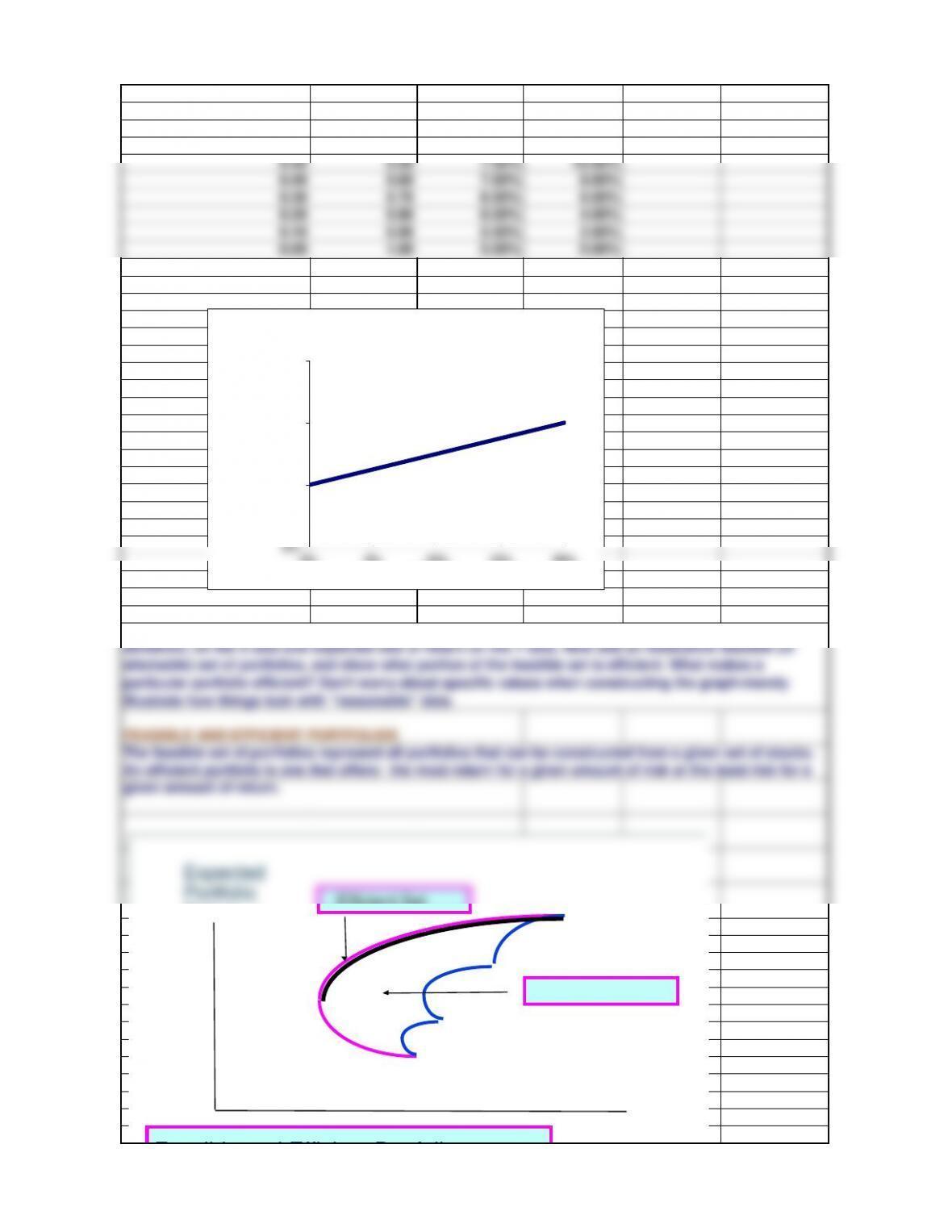

0%

5%

10%

15%

20%

0% 10% 20% 30% 40%

Expected return

Risk, sp

AB = -1.0: Attainable Set of Risk/Return

Combinations

Michael C. Ehrhardt Page 3 9/22/2019

Ch25 Mini Case.xlsx Mini Case

0.90 0.10 9.50% 18.00%

0.80 0.20 9.00% 16.00%

0.70 0.30 8.50% 14.00%

0.60 0.40 8.00% 12.00%

0.50 0.50 7.50% 10.00%

0.40 0.60 7.00% 8.00%

0.30 0.70 6.50% 6.00%

0.20 0.80 6.00% 4.00%

0.10 0.90 5.50% 2.00%

0.00 1.00 5.00% 0.00%

FEASIBLE AND EFFICIENT PORTFOLIOS

The feasible set of portfolios represent all portfolios that can be constructed from a given set of stocks.

An efficient portfolio is one that offers: the most return for a given amount of risk or the least risk for a

given amount of return.

d. Construct a reasonable, but hypothetical, graph that shows risk, as measured by portfolio standard

deviation, on the X axis and expected rate of return on the Y axis. Now add an illustrative feasible (or

attainable) set of portfolios, and show what portion of the feasible set is efficient. What makes a

particular portfolio efficient? Don't worry about specific values when constructing the graph-merely

illustrate how things look with "reasonable" data.

Expected

Portfolio

Return, r p

Risk, sp

Efficient Set

Feasible Set

Feasible and Efficient Portfolios

0%

5%

10%

15%

0% 5% 10% 15% 20%

Expected return

Risk, sp

Attainable Set of Risk/Return Combinations

with Risk-Free Asset

Michael C. Ehrhardt Page 4 9/22/2019

Ch25 Mini Case.xlsx Mini Case

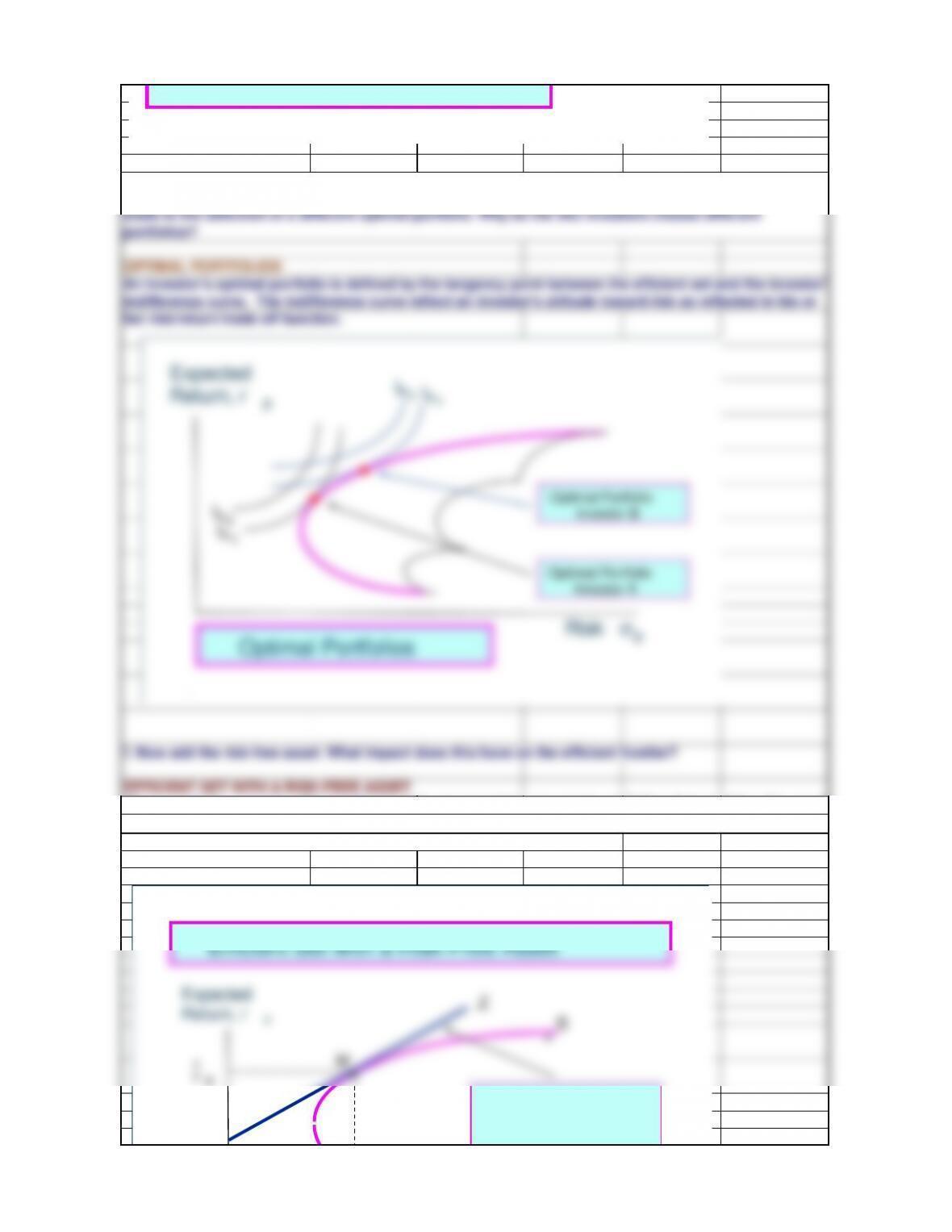

OPTIMAL PORTFOLIOS

An investor's optimal portfolio is defined by the tangency point between the efficient set and the investor's

indifference curve. The indifference curve reflect an investor's attitude toward risk as reflected in his or

her risk/return trade off function.

f. Now add the risk-free asset. What impact does this have on the efficient frontier?

EFFICIENT SET WITH A RISK-FREE ASSET

When a risk free asset is added to the feasible set, investors can create portfolios that combine this asset

with a portfolio of risky asset. The straight line connecting rrf with M, the tangency point between the line

and the old efficiency set, becomes the new efficient frontier.

e. Now add a set of indifference curves to the graph created for part b. What do these curves represent?

What is the optimal portfolio for this investor? Finally, add a second set of indifference curves which

leads to the selection of a different optimal portfolio. Why do the two investors choose different

portfolios?

.

s

Feasible and Efficient Portfolios

IB2IB1

IA2

IA1

Optimal Portfolio

Optimal Portfolio

Investor B

Expected

Return, r p

Z

Efficient Set with a Risk-Free Asset

Expected

Return, r p

Ch25 Mini Case.xlsx Mini Case

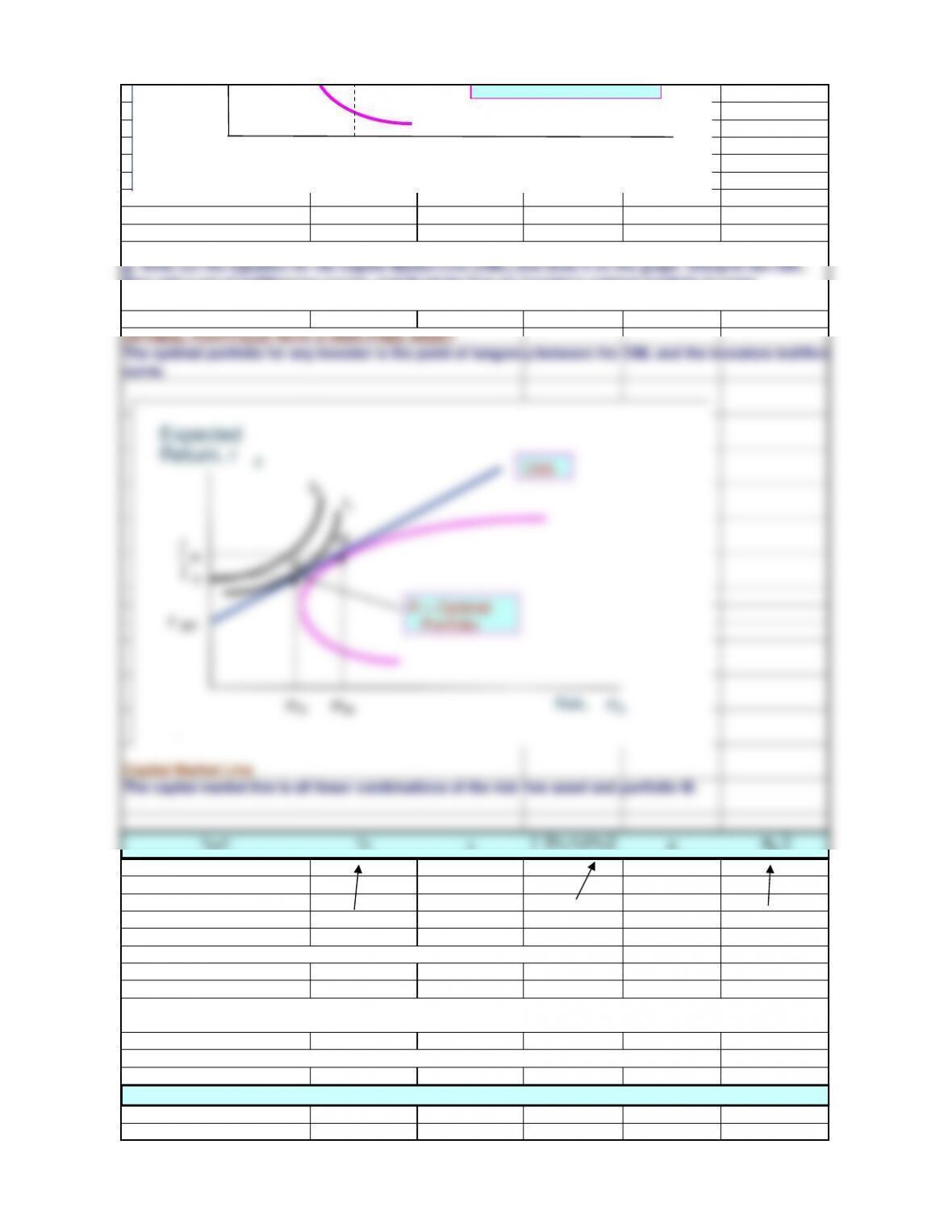

OPTIMAL PORTFOLIO WITH A RISK-FREE ASSET

The optimal portfolio for any investor is the point of tangency between the CML and the investors indifferen

curve.

Capital Market Line

The capital market line is all linear combinations of the risk free asset and portfolio M.

rhat= rrf + { [(rm-rrf)/sm]xσp }

Intercept Slope Risk Measure

The CML gives the risk and return relationship for efficient portfolios

The SML , also part of CAPM, gives the risk and return relationship for individual stocks.

SML =

ri + [ (RPM)xb ]

g. Write out the equation for the Capital Market Line (CML) and draw it on the graph. Interpret the CML.

Now add a set of indifference curves, and illustrate how an investor's optimal portfolio is some

combination of the risky portfolio and the risk-free asset. What is the composition of the risky portfolio?

h. What is the Capital Asset Pricing Model (CAPM)? What are the assumptions that underlie the model?

What is the Security Market Line? See PowerPoint Show.

.

.

rRF

sMRisk, sp

New Efficient Set

.

rRF

sMRisk, sp

I1

I2

CML

R = Optimal

Portfolio

.

R.

M

r

R

rM

sR

^

^

Expected

Return, r p

Michael C. Ehrhardt Page 6 9/22/2019

Ch25 Mini Case.xlsx Mini Case

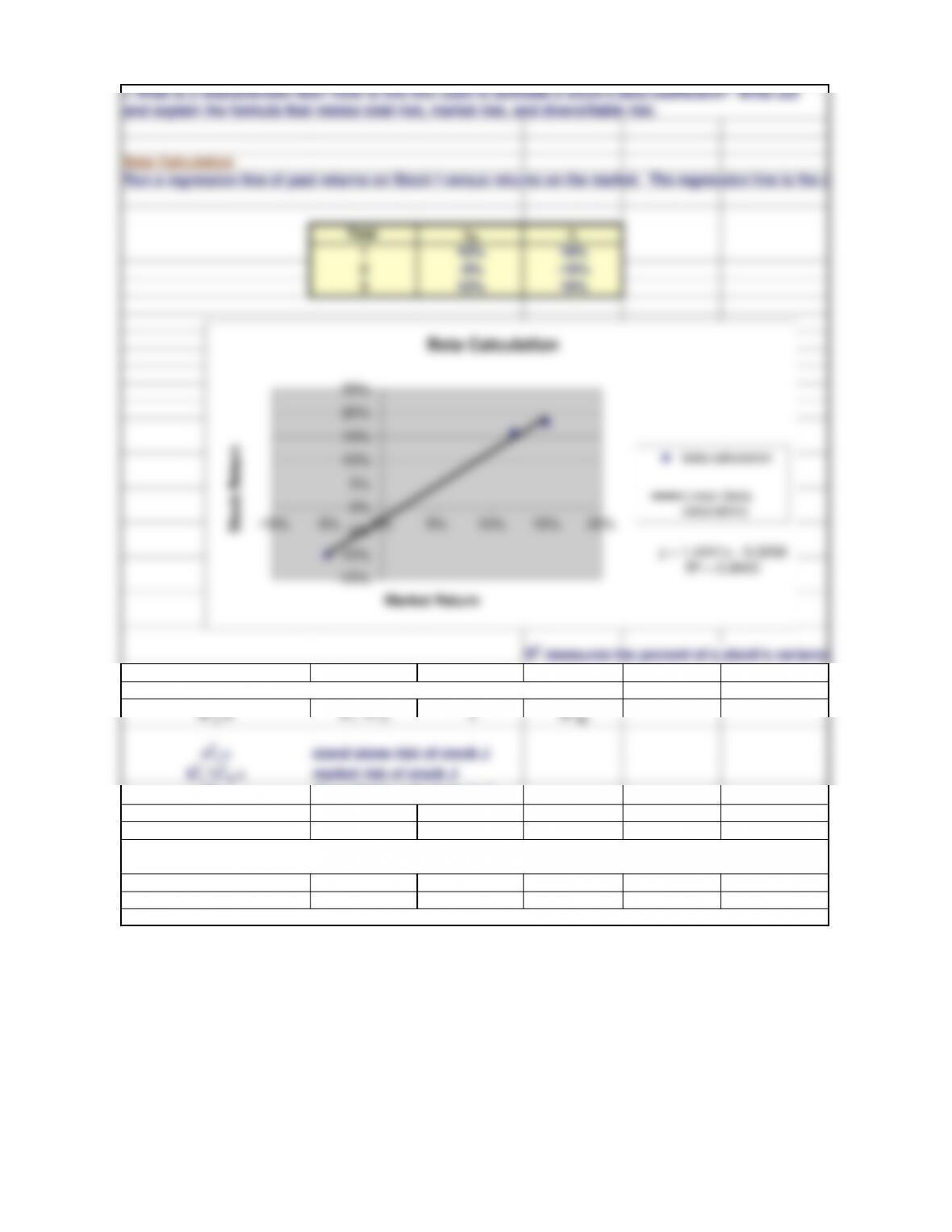

Beta Calculation

Run a regression line of past returns on Stock I versus returns on the market. The regression line is the cha

Year

rMri

115% 18%

2-5% -10%

312% 16%

i. What is a characteristic line? How is this line used to estimate a stock's beta coefficient? Write out

and explain the formula that relates total risk, market risk, and diversifiable risk.

-5%

0%

5%

10%

15%

20%

25%

-10% -5% 0% 5% 10% 15% 20%

Stock Return

Beta Calculation

beta calculation

Linear (beta

calculation)