10/28/2015

2016 2017 2018 2019 2020 2021

Net sales 60.00 90.00 112.50 127.50 139.70

Cost of goods sold (60%) 36.00 54.00 67.50 76.50 83.80

Selling/administrative expense 4.50 6.00 7.50 9.00 11.00

Interest expense

5.00 6.50 6.50 7.00 8.16

Total Net Operating Capital 150.00 150.00 157.50 163.50 168.00 173.00

Investment in net operating capital 0.00 7.50 6.00 4.50 5.00

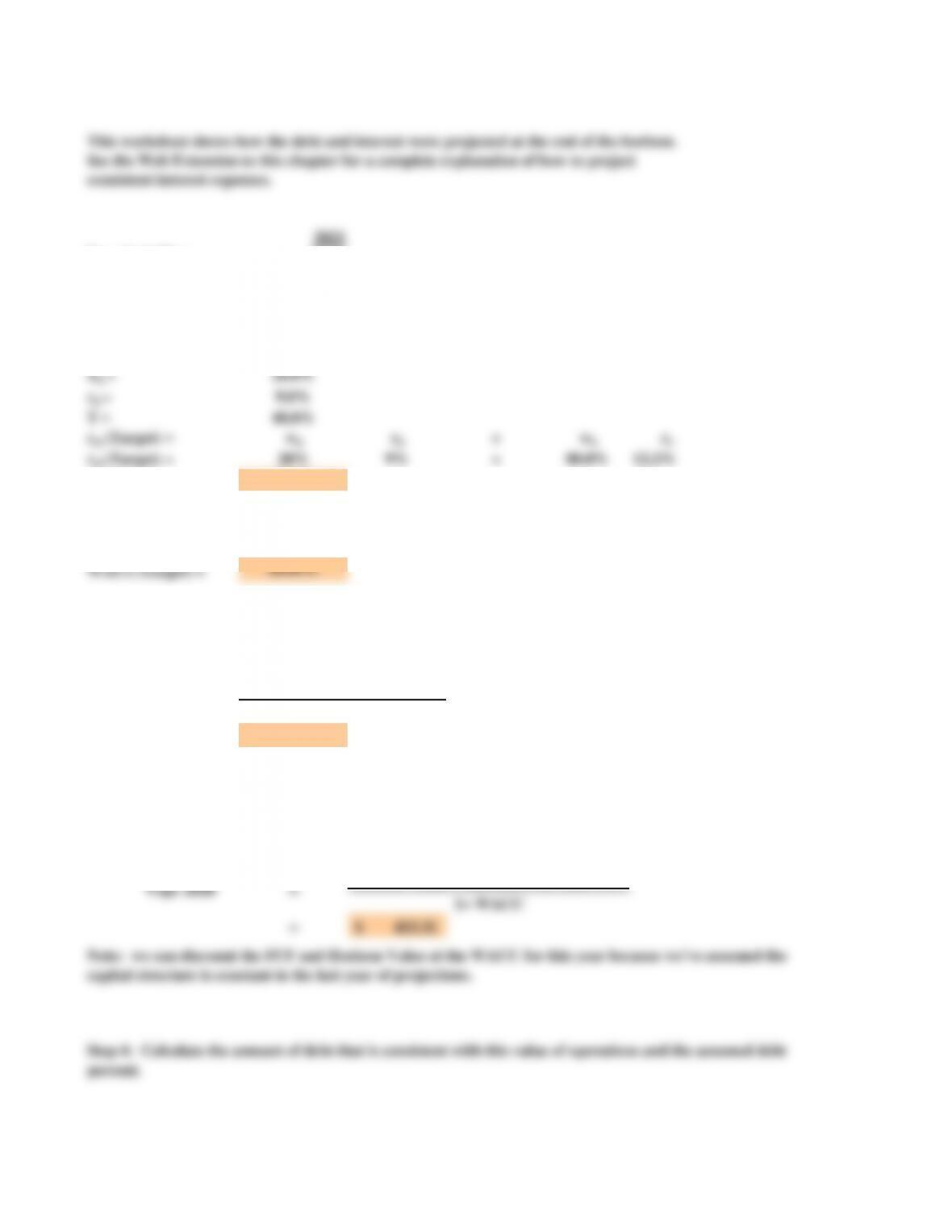

risk free rate 7%

market risk premium 4%

pre-merger beta 1.3

pre-merger % debt 20%

pre-merger debt 55.00$ million

pre-merger debt rd9%

Tax rate 40%

a.

Economically justifiable reasons:

Synergy: Value of the whole exceeds sum of the parts. Could arise from:

Operating economies

Financial economies

Differential management efficiency

Taxes (use accumulated losses)

Break-up value: Assets would be more valuable if broken up and sold to other companies.

Questionable reasons for mergers:

Diversification

Purchase of assets at below replacement cost

Acquire other firms to increase size, thus making it more difficult to be acquired

b.

Friendly merger:

The merger is supported by the managements of both firms.

Hostile merger:

Target firm’s management resists the merger.

Acquirer must go directly to the target firm’s stockholders, try to get 51% to tender their shares.

Often, mergers that start out hostile end up as friendly, when offer price is raised.

Chapter 22. Mini Case for Mergers and Corporate Control

Hager’s management is new to the merger game, so Zona has been asked to answer some basic

questions about mergers as well as to perform the merger analysis. To structure the task, Zona has

developed the following questions, which you must answer and then defend to Hager’s board.

Several reasons have been proposed to justify mergers. Among the more prominent are (1) tax

considerations, (2) risk reduction, (3) control, (4) purchase of assets at below-replacement cost, (5)

synergy, and (6) globalization. In general, which of the reasons are economically justifiable?

Which are not? Which fit the situation at hand? Explain.

Briefly describe the differences between a hostile merger and a friendly merger.

The table below indicates Zona’s estimates of LL’s earnings potential if it came under Hager’s

management (in millions of dollars). The interest expense listed here includes the interest (1) on LL’s

existing debt, which is $55 million at a rate of 9 percent, and (2) on new debt expected to be issued

over time to help finance expansion within the new “L division,” the code name given to the target

firm. If acquired, LL will face a 40 percent tax rate.

Security analysts estimate LL’s beta to be 1.3. The acquisition would not change Lyons’ capital

structure, which is 20 percent debt. Zona realizes that Lyons’ Lighting’s business plan also requires

certain levels of operating capital and that the annual investment could be significant. The required

levels of total net operating capital are listed below.

Hager’s Home Repair Company, a regional hardware chain, which specializes in “do-it-yourself”

materials and equipment rentals, is cash rich because of several consecutive good years. One of the

alternative uses for the excess funds is an acquisition. Doug Zona, Hager’s treasurer and your boss,

has been asked to place a value on a potential target, Lyons’ Lighting, a chain which operates in

several adjacent states, and he has enlisted your help.

Zona estimates the risk-free rate to be 9 percent and the market risk premium to be 4 percent. He also

estimates that free cash flows after 2021 will grow at a constant rate of 6 percent. Following are

projections for sales and other items.

c.

d.

2016 2017 2018 2019 2020 2021

Net sales 60.0$ 90.0$ 112.5$ 127.5$ 139.7$

Cost of goods sold (60%) 36.0 54.0 67.5 76.5 83.8

Selling/administrative expense 4.5 6.0 7.5 9.0 11.0

EBIT 19.5 30.0 37.5 42.0 44.9

Taxes on EBIT (40%) 7.8 12.0 15.0 16.8 18.0

NOPAT 11.7 18.0 22.5 25.2 26.9

Total net operating capital 150.0 150.0 157.5 163.5 168.0 173.0

Investment in operating capital 0.0 7.5 6.0 4.5 5.0

Free Cash Flow 11.70 10.50 16.50 20.70 21.94

Interest expense

5.00 6.50 6.50 7.00 8.16

Tax savings from interest 2.000$ 2.600$ 2.600$ 2.800$ 3.264$

e.

rs(Target) = rRF + (rM – rRF) bTarget

rsL(Target) = 7% +4% X 1.3

rsL(Target) = 12.2%

rsU(Target) = wdrd+ wSrL

rsU(Target) = 20% 9% 80.0% 12.2%

rsU(Target) = 11.560%

f.

Beta = 1.3

(2021 Free Cash Flow)(1+g)

Tax Rate

40%

rsU = 11.56%

g = 6%

Unlevered Horizon Value = $ 418.3 million

Use the data developed in the table to construct the L division’s free cash flows for 2017 through

2021. Why are we identifying interest expense separately since it is not normally included in

calculating free cash flows or in a capital budgeting cash flow analysis? Why is the investment in

net operating capital deducted in calculating the free cash flow?

Unlevered

Horizon Value =

What are the steps in valuing a merger?

When the capital structure is changing rapidly, as in many mergers, the WACC

changes from year-to-year and it is difficult to apply the corporate valuation model in

these cases. The APV model works better when the capital structure is changing. The

steps are:

When debt levels are changing rapidly, as they do with many mergers, it is difficult to apply the

corporate value model or standard capital budgeting techniques to merger valuation because the

discount rate changes as the debt level changes. Instead, the APV method is easier to apply.

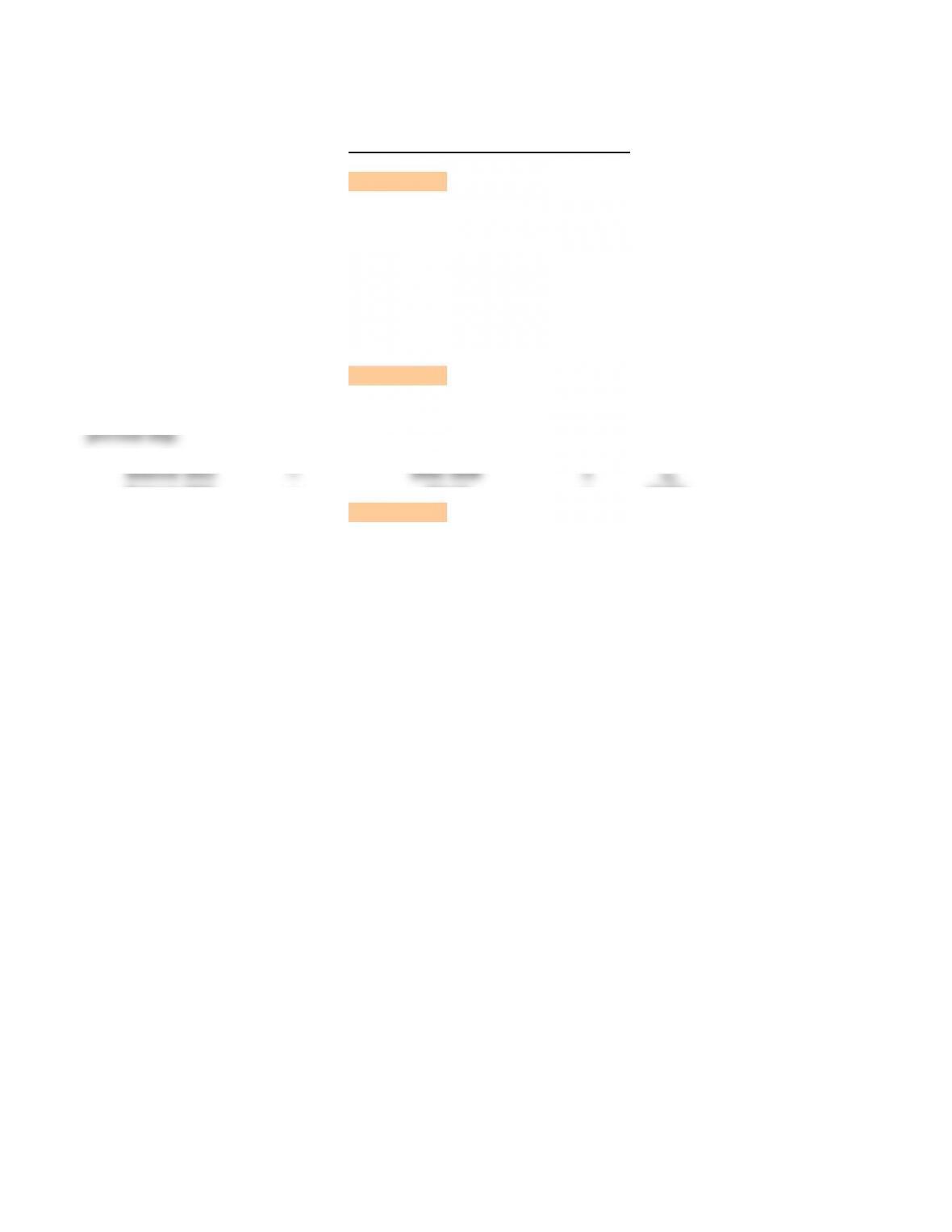

rsU – g

8. Calculate Vops as the sum of the unlevered value and the tax shield value.

Conceptually, what is the appropriate discount rate to apply to the cash flows developed in Part c?

What is your actual estimate of this discount rate?

What is the estimated horizon, or continuing, value of the acquisition; that is, what is the estimated

value of the L division’s unlevered cash flows and tax shields beyond 2021? What is Lyons’ value

to Hager’s shareholders? Suppose another firm were evaluating Lyons‘ as an acquisition

candidate. Would they obtain the same value? Explain.

These estimated cash flows are unlevered flows plus the tax shelter from interest payments. Because

the free cash flows are unlevered equity flows, they should be discounted at the unlevered cost of

equity. Similarly, the tax savings (also called tax shields) should be discounted at the unlevered cost

of equity. Note that the cash flows reflect the target’s business risk, not the acquiring company’s.

However, if the merger will affect the target’s leverage and tax rate, then it will affect its financial risk.

The horizon value should be calculated once the capital structure is stable at its post-merger target

level of debt.

5. Calculate the horizon value of the unlevered firm using the constant growth formula and

FCFN-.

6. Calculate the unlevered firm value as the present value of the unlevered horizon value and

the FCFs at the unlevered cost of equity.

7. Calculate the value of the tax shields as the present value of the tax shield horizon value and

the individual tax shields.

1. Project FCFt ,TSt until the target is at its target capital structure for one year and and is

expected to grow thereafter at a constant growth rate.

2. Project the horizon growth rate.

3. Calculate the unlevered cost of equity, rsu.

4. Calculate horizon value of tax shields using the constant growth formula and TSN-.

2017 2018 2019 2020 2021

Free Cash Flow $ 11.7 $ 10.5 $ 16.5 $ 20.7 $ 21.94

Unlevered Horizon Value $ 418.3

Total $ 11.7 $ 10.5 $ 16.5 $ 20.7 $ 440.2

Unlevered Value = PV at rsU = $ 298.9 million

(2021 Tax Shield)(1+g)

TS. Horizon Value = $ 62.2 million

Interest tax shield 2.0$ 2.6$ 2.6$ 2.8$ 3.264$

Tax shield horizon value 62.23$

Total $ 2.0 $ 2.6 $ 2.6 $ 2.8 $ 65.49

Tax Shield Value = PV at rsU = $ 45.462 million

Vops = Tax shield value + Unlevered value = $ 344.4 million

– Debt $ 55.00

= Equity $ 289.4 million

Would another potential acquirer obtain the same value?

No. The cash flow estimates would be different, both due to forecasting inaccuracies and to differential

synergies. Further, a different beta estimate, financing mix, or tax rate would change the discount rate.

Note: Change the shaded cells above ( beta or tax rate ) to see the change in value

g.

Estimated Value of Target = $ 289.4

Target’s Current Value = $ 220.0 20 million shares x $11/share

Merger Premium = $ 69.4

Presumably, the target’s value is increased by $69.4 million due to merger synergies, although realizing

such synergies has been problematic in many mergers.

new level of debt at end of 2020 $221.60 million

new % debt 40%

new rd 10%

Unlevered value (From before. This doesn‘t change) $ 298.9 million

New tax shield in 2021 = Debt in 2021 x new interest rate x T

Interest in 2021 $ 22.16

Tax shield in 2021 $ 8.864 million

(2021 Tax Shield)(1+g)

Tax shield horizon value = $ 169.0 million

2017 2018 2019 2020 2021

Interest tax shield 2.0$ 2.6$ 2.6$ 2.8$ 8.864$

Tax shield horizon value 169.0$

Total tax shield cash flows $ 2.0 $ 2.6 $ 2.6 $ 2.8 $ 177.9

Tax Shield Value = PV at rsU = $ 110.5 million

Vops = Tax shield value + Unlevered value = $ 409.4 million

– Debt 55.0

Tax Shield

Horizon Value =

The offer could range from $11 to $289.4/20 = $14.47 per share. At $11, all merger benefits would go to

the acquiring firm’s shareholders. At $14.47, all value added would go to the target firm’s

rsU – g

Assume that Lyons’ has 20 million shares outstanding. These shares are traded relatively

infrequently, but the last trade, made several weeks ago, was at a price of $11 per share. Should

Hager’s make an offer for Lyons’? If so, how much should it offer per share?

rsU – g

The free cash flows and the unlevered cost of equity would be unchanged. If we assume that the

interest payments in the first 4 years are unchanged, and the intention is to use $221.6 million in debt

from year 5 on, then the horizon value of the tax shield would increase.

h. How would the analysis be different if Hager‘s intended to recapitalize Lyons’ with 40 percent debt

costing 10% at the end of 4 years? This amounts to $221.6 million of debt at the year prior to the

horizon.

Tax Shield

Horizon Value =

= Equity $ 354.4 million

Old equity value under the 20% debt capital structure $ 289.4

New equity value under the 40% debt capital structure $ 354.4

Increase in value due to increased tax shields 65.02

Lyons’ Lighting is worth $ 65.02 million more to Hager’s at 40% debt

than at 20% debt. The difference is the added benefit of a larger tax shield.

This amounts to

$ 3.25 per share difference in maximum purchase price.

i.

Shareholders of target firms reap most of the benefits, that is, the final price is close to full value.

Target management can always say no.

Competing bidders often push up prices.

j.

Pooling of interests has been eliminated. Only purchase accounting may be used.

Purchase:

Goodwill is often created, which appears as an asset on the balance sheet.

Common equity account is increased to balance assets and claims.

k.

Identifying targets

Arranging mergers

Developing defensive tactics

Establishing a fair value

Financing mergers

Arbitrage operations

l.

Sale of an entire subsidiary to another firm.

Spinning off a corporate subsidiary by giving the stock to existing shareholders.

Carving out a corporate subsidiary by selling a minority interest.

Outright liquidation of assets.

A firm divests assets:

Because the subsidiary worth more to buyer than when operated by current owner.

To settle antitrust issues.

Because subsidiary’s value increased if it operates independently.

To change strategic direction.

To shed money losers.

To get needed cash when distressed.

m.

Advantages:

Control with fractional ownership.

Isolation of risks.

Disadvantages:

Partial multiple taxation.

Ease of enforced dissolution.

A holding company is a corporation formed for the sole purpose of owning the stocks of other

companies. In a typical holding company, the subsidiary companies issue their own debt, but their

equity is held by the holding company, which, in turn, sells stock to individual investors.

What are the major types of divestitures? What motivates firms to divest assets?

What are holding companies? What are their advantages and disadvantages?

The assets of the acquired firm are “written up” to reflect purchase price if it is greater than the net

asset value.

What merger-related activities are undertaken by investment bankers?

Hopefully: not paying kickbacks to CEOs for business, and not providing fraudulent

analyst reports to pump up stock prices.

Goodwill is not amortized or expensed over time. Instead, it is subject to an “impairment” test. If

goodwill drops in market value, then a charge for this reduction must be taken. Otherwise, no

expense for goodwill is recorded. Note: goodwill is still amortized for Federal income tax

What method is used to account for mergers?

There has been considerable research undertaken to determine whether mergers really create

value, and, if so, how this value is shared between the parties involved. What are the results of

this research?

According to empirical evidence, acquisitions do create value as a result of economies of scale, other

synergies, and/or better management.

See the Web Extension to this chapter for a complete explanation of how to project

consistent interest expenses.

2021

Free Cash Flow 21.94

growth rate at horizon

6.0%

rsL(Target) = 12.2%

wd =20.0%

rd =9.0%

T =

40.0%

rsU(Target) = wdrd + wSrL

rsU(Target) = 20% 9% +80.0% 12.2%

rsU(Target) = 11.56%

WACC(Target) =

wd(rd)(1 – T) + ws(rs)

structure is constant once the horizon is reached.

capital structure is constant in the last year of projections.

of projections.

This worksheet shows how the debt and interest were projected at the end of the horizon.

Debt 2020 = Vops 2020 xwd

Debt 2020 = x 20.0%

Debt 2020 = $ 90.66

Interest 2021 = Debt 2020 xrd

Interest 2021 = x 9.0%

Interest 2021 = $ 8.16

Calculations with a change in capital structure

Step 1: Calculate the new WACC at the horizon:

Calculate a new levered cost of equity:

New wd =40%

New rd =10%

New rsL = rU+ ( rU– rD) D/S

New rsL =11.56% +11.56% –10% 0.666666667

New rsL =12.60%

Calculate a new WACC:

New WACC(Target) =

wd(rd)(1 – T) + ws(rs)

New WACC(Target) =

2.40% +7.56%

New WACC(Target) =

9.96%

Calculate a new Horizon Value of Operations

Horizon Free Cash Flow)(1+g)

$ 587.28

Step 3: Calculate the value of operations as of the year before the horizon. We need this because we need

to set the debt level in the next to last year of projections so we can set the interest expense in the last year

of projections.

Horizon Value =

New WACC – g

Step 2: Calculate the horizon value using the Corporate Valuation Model. This is ok since the capital

structure is constant once the horizon is reached.

This is the amount of interest expense we projected for the last year of projections.

Horizon Value =

This is exactly the same as above, but we use the new capital structure and new cost of debt to calculate a

new WACC, which is used in Steps 2 and 3 above. The new cost of debt is used in Step 4.

453.31

Step 5: Calculate the interest expense in the last year that corresponds to the debt calculated in the

previous step.

90.66

Vops 2020 = $ 554.04

Debt 2020 = Vops 2020 xwd

Debt 2020 = x 40.0%

Debt 2020 = $ 221.62

Interest 2021 = Debt 2020 xrd

Interest 2021 = x 10.0%

Interest 2021 = $ 22.16

221.62

This is the amount of interest expense we projected for the last year of projections.

Note: we can discount the FCF and Horizon Value at the WACC for this year because we’ve assumed the

capital structure is constant in the last year of projections.

Step 4: Calculate the amount of debt that is consistent with this value of operations and the assumed debt

percent.

554.04

Step 5: Calculate the interest expense in the last year that corresponds to the debt calculated in the

previous step.

Vops

2020

=

Horizon Value + free cash flow2011

1+ New WACC