b. 2. Graph (a) the relationships between capital costs and leverage as measured by

D/V, and (b) the relationship between value and D.

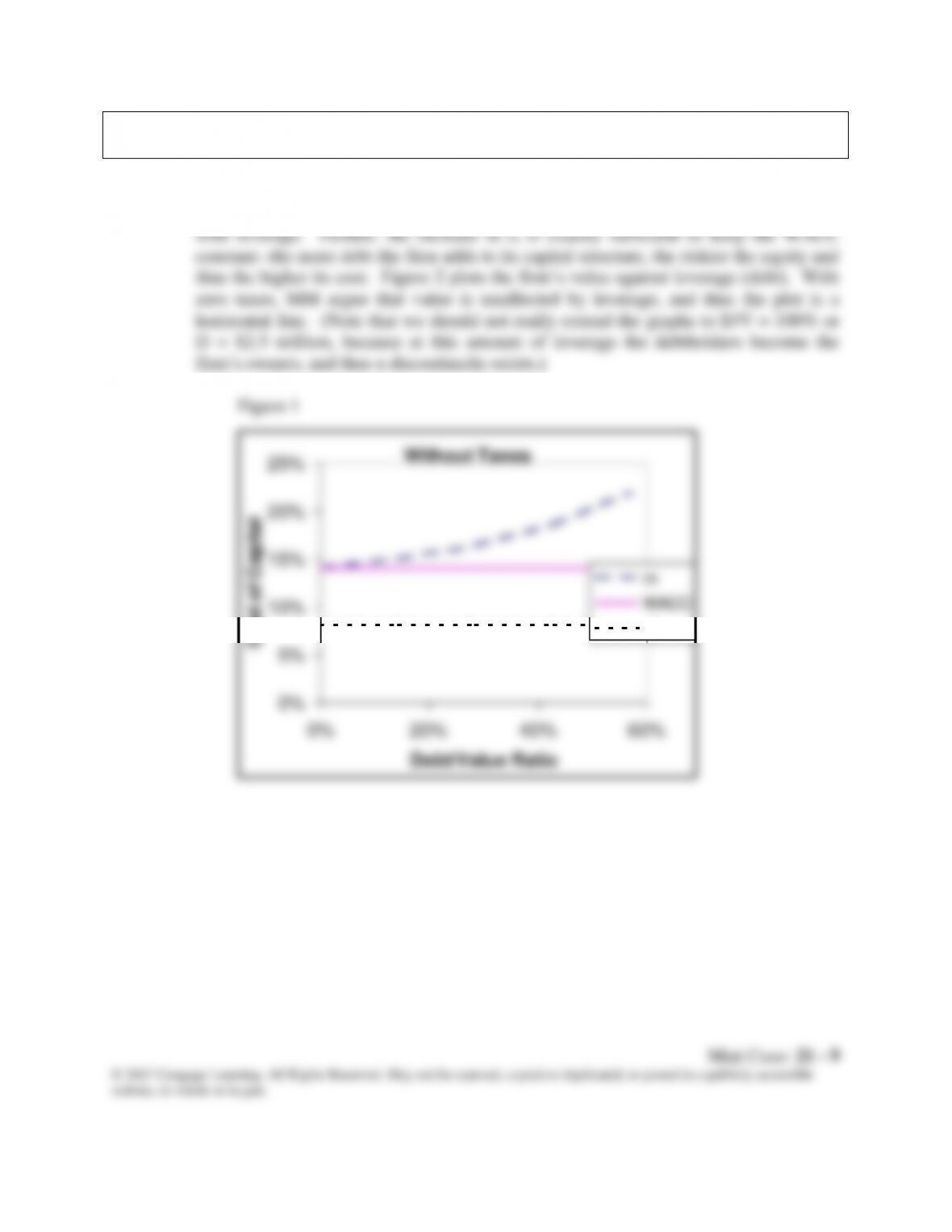

Answer: Figure 1 plots capital costs against leverage as measured by the debt/value ratio.

Note that, under the MM no-tax assumption, rd is a constant 8 percent, but rs increases

c. Using the data given in part B, but now assuming that firms L and U are both

subject to a 40 percent corporate tax rate, repeat the analysis called for in B(1)

and B(2) under the MM with-tax model.

Answer: With corporate taxes added, the MM propositions become:

Proposition I: VL = VU + TD.

There are two very important differences between these propositions and the zero-tax

propositions: (1) when corporate taxes are added, VL does not equal VU; rather, VL

increases as debt is added to the capital structure, and the greater the debt usage, the

higher the value of the firm. (2) rsL increases less rapidly when corporate taxes are

4

3

2

1

0 0.5 1.0 1.5 2.0 2.5

Firm Value ($3.6 Million)

Value of Firm, V

(Millions of $)

VUVL

($)

Debt ($)

Figure 2

website, in whole or in part.

This represents a 40% decline in value, and it is logical, because the 40% tax rate

takes away 40% of the income and hence 40% of the firm’s value.

Looking at VL, we see that:

D + SL = VL

$1,000,000 + SL = $2,542,857

SL = $1,542,857.

now,

= ($1,000/$2,543)(8%)(0.6) + (1,543/$2,543)(16.33%)

= 1.89% + 9.91% = 11.8%.

The WACC is lower for the levered firm than for the unlevered firm when corporate

taxes are considered.

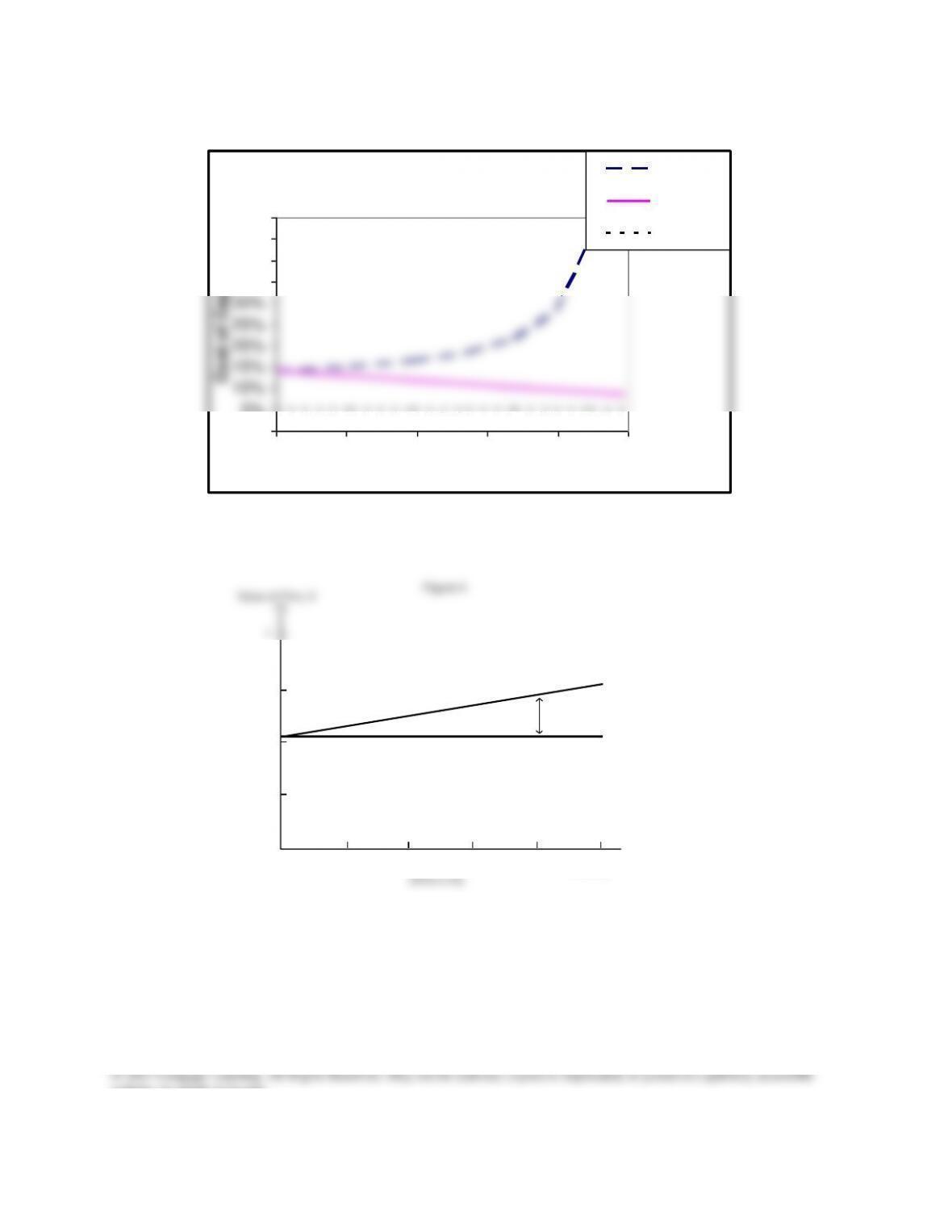

Figure 3 below plots capital costs at different D/V ratios under the MM model

downward-sloping WACC curve.

Figure 4 shows that, when corporate taxes are considered, the firm’s value

increases continuously as more and more debt is used.

Mini Case: 21 – 12

© 2017 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible

website, in whole or in part.

Figure 3

With Taxes

0%

5%

35%

40%

45%

50%

0% 20% 40% 60% 80% 100%

Debt/Value Ratio

rs

WACC

rd x (1-T)

Mini Case: 21 – 13

website, in whole or in part.

d. Suppose that Firms U and L are growing at a constant rate of 7% and that the

investment in net operating assets required to support this growth is 10% of

EBIT. Use the compressed adjusted present value (APV) model to estimate the

value of U and L. Also estimate the levered cost of equity and the weighted

average cost of capital.

Answer: If a firm is growing, the assumptions that MM made are violated. The extension to

shield.

First, calculate expected free cash flow:

Next, note that WACC = unlevered cost of equity if there is no debt so

WACC = rsU = 14%

Therefore, the value of the firm = $3,571,429 + $457,143 = $4,028,571.

The value of the equity is the value of the firm less the value of the

This is less than the increase in the non-growing firm’s value as calculated using the

And the new levered WACC:

WACCL = (D/V)rd(1 – T) + (S/V)rs

= (1,000,000/4,028,571)8%(1-.40)

+ ($3,028,571/4,028,571)15.98%

= 13.2%.

e. Suppose the expected free cash flow for Year 1 is $250,000 but it is expected to

grow unevenly over the next 3 years: FCF2 = $290,000 and FCF3 = $320,000,

after which it will grow at a constant rate of 7%. The expected interest expense

at Year 1 is $80,000, but it is expected to grow over the next couple of years

before the capital structure becomes constant: Interest expense at Year 2 will be

$95,000, at Year 3 it will be $120,000 and it will grow at 7% thereafter. What is

the estimated horizon unlevered value of operations (i.e., the value at Year 3

immediately after the FCF at Year 3)? What is the current unlevered value of

operations? What is the horizon value of the tax shield at Year 3? What is the

current value of the tax shield? What is the current total value? The tax rate and

The unlevered value of operations is the present value of the free cash flows and the

horizon value. In Excel, the formula is:

=NPV(Rate,value1,value2….) = NPV(0.14,250,290,320+4891.43) = $3,960.01.

website, in whole or in part.

The horizon value of the tax shield can be found by applying the constant growth

=NPV(Rate,value1,value2….) = NPV(0.14,32,38,48+733.71) = $584.94.

The value of operations is the sum of the unlevered value of operations and the value

of the tax shield:

Vop = VU + VTS = $3,960.01 + $584.94 = $4,544.95.