1

2

3

4

5

6

7

8

9

10

11

12

13

19

20

21

22

23

1. The weighted average cost of capital is independent of the firm’s capital structure.

2. The WACC of a firm with debt is equal to the unlevered cost of equity.

42

43

44

45

51

52

53

54

55

56

A B C D E F G H I

10/28/2015

Situation

Proposition I.

rsL = rsU + (rsU-rd)x (D/S)

WACC =

wd*rd + wce*rs = (D/V)*rd + (S/V)*rs

WACC = 2.24% + 11.8%

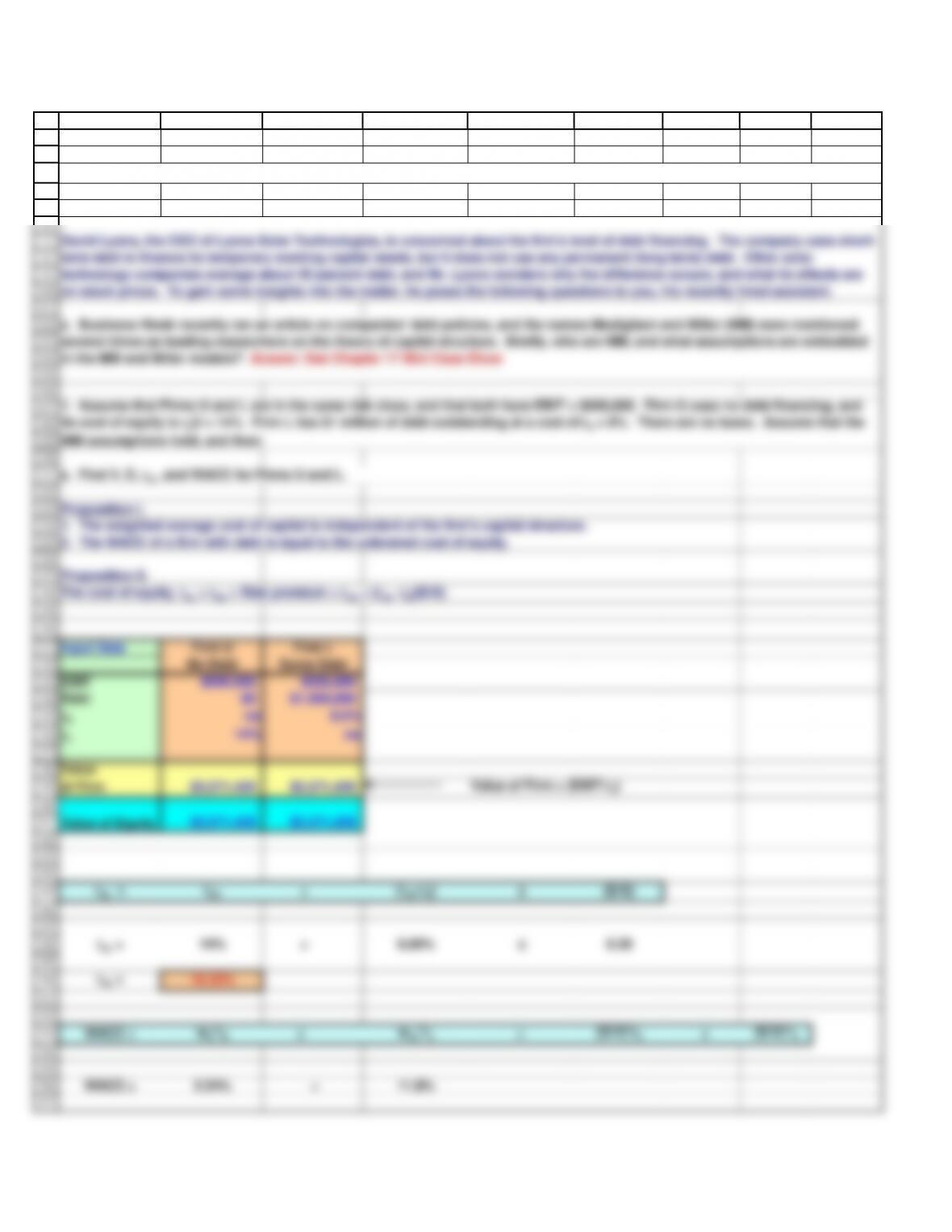

Chapter 21. Mini Case

David Lyons, the CEO of Lyons Solar Technologies, is concerned about his firm’s level of debt financing. The company uses short-

term debt to finance its temporary working capital needs, but it does not use any permanent (long-term) debt. Other solar

technology companies average about 30 percent debt, and Mr. Lyons wonders why the difference occurs, and what its effects are

on stock prices. To gain some insights into the matter, he poses the following questions to you, his recently hired assistant.

a. Business Week recently ran an article on companies’ debt policies, and the names Modigliani and Miller (MM) were mentioned

several times as leading researchers on the theory of capital structure. Briefly, who are MM, and what assumptions are embedded

MM assumptions hold, and then:

a. Find V, S, rsL, and WACC for Firms U and L.

58

59

60

61

62

63

64

70

103

104

105

106

107

rs14.00% 16.33% 14.00% 16.33%

Tax Rate 0% 0% 40% 40%

115

A B C D E F G H I

WACC = 14.00%

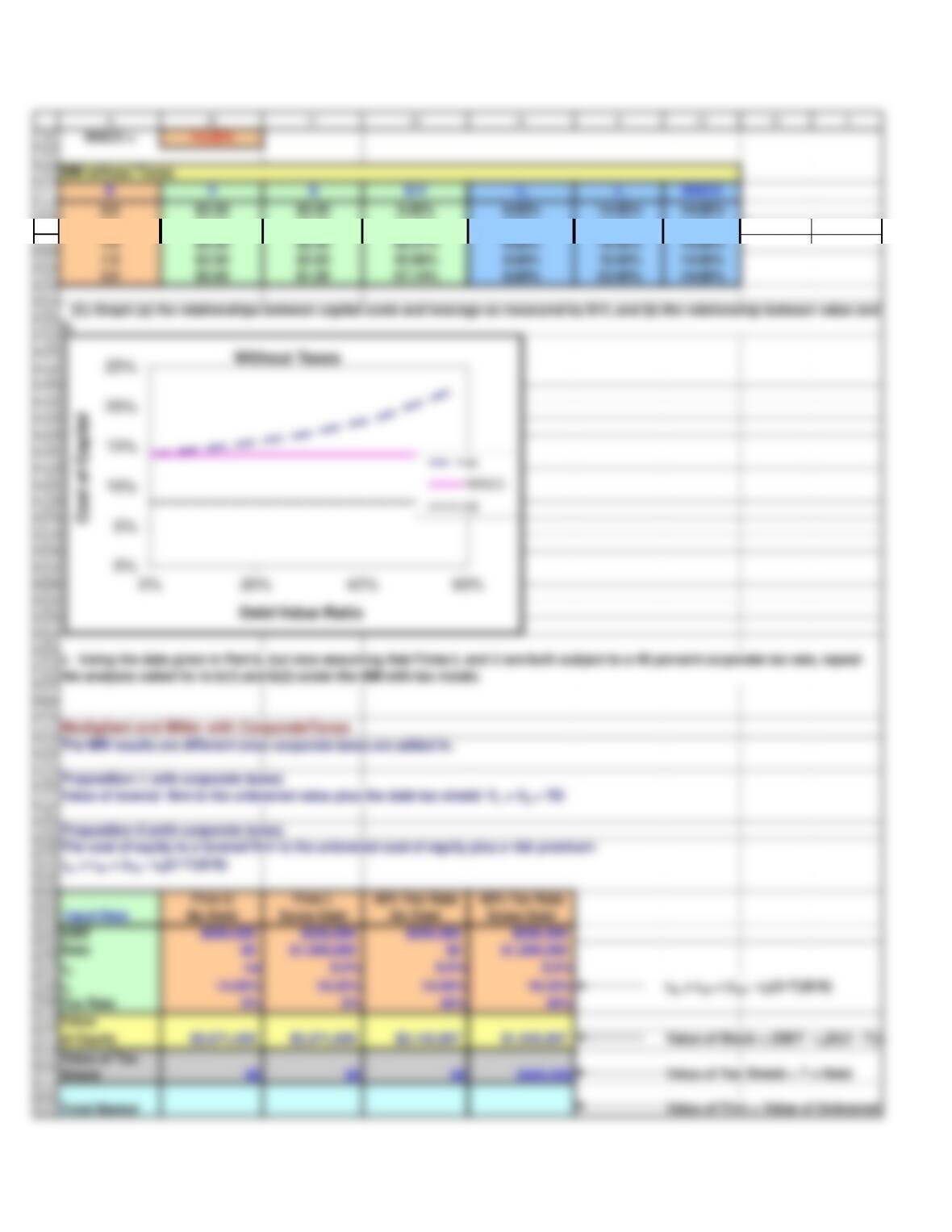

MM without Taxes

D V S D/V

rdrsWACC

0.0 $3.50 $3.50 0.00% 8.00% 14.00% 14.00%

0.5 $3.50 $3.00 14.29% 8.00% 15.00% 14.00%

1.0 $3.50 $2.50 28.57% 8.00% 16.40% 14.00%

Firm U Firm L 40% Tax Rate 40% Tax Rate

Input Data No Debt Some Debt No Debt Some Debt

EBIT $500,000 $500,000 $500,000 $500,000

Debt $0 $1,000,000 $0 $1,000,000

rdna 8.0% 8.0% 8.0%

Value of Firm = Value of Unlevered F

Total Market

116

117

118

119

120

121

122

126

127

128

129

130

137

138

139

140

141

142

148

149

150

151

152

153

159

160

161

A B C D E F G H I

WACC 14.00% 14.00% 14.00% 11.80%

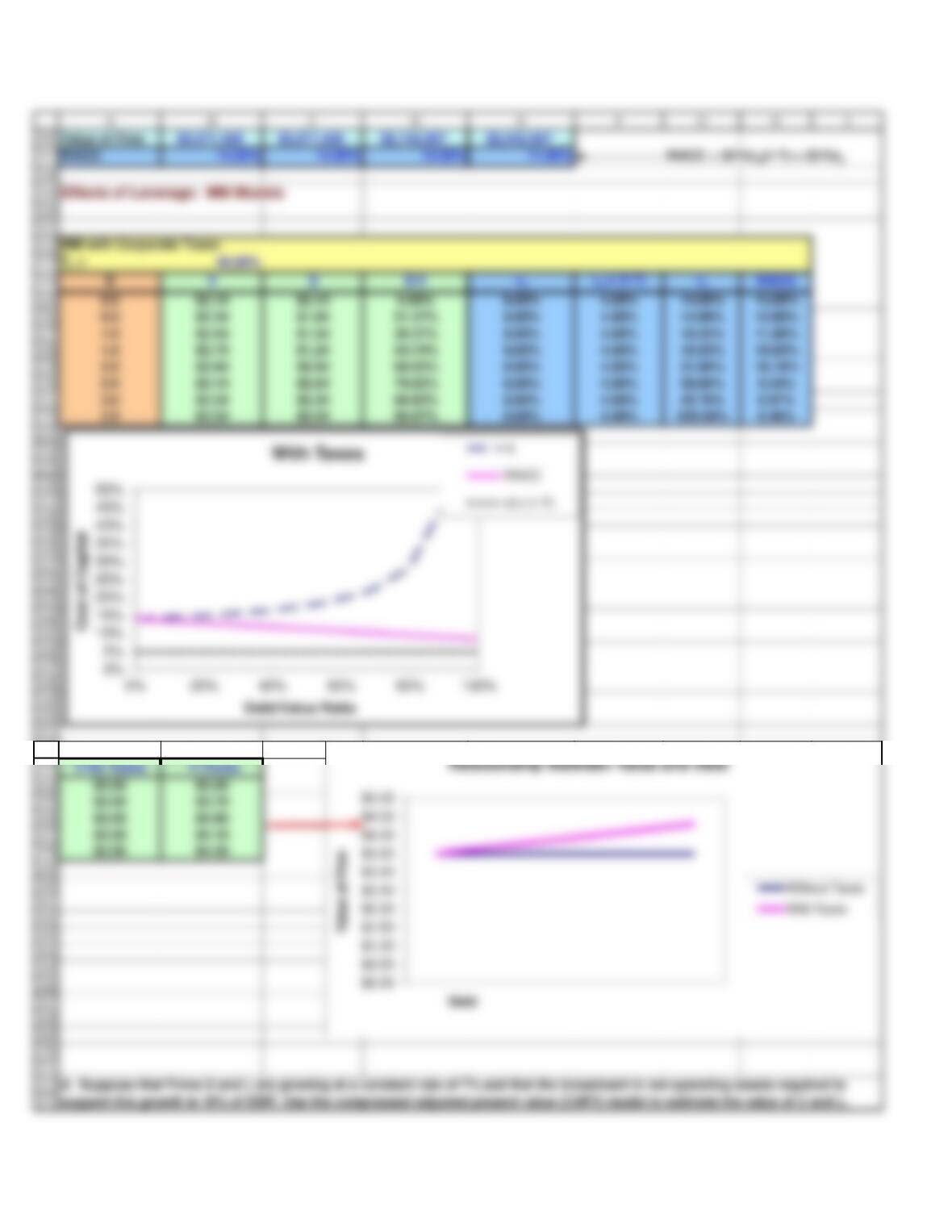

Effects of Leverage: MM Models

MM with Corporate Taxes

0.5 $2.34 $1.84 21.37% 8.00% 4.80% 14.98% 12.80%

1.0 $2.54 $1.54 39.37% 8.00% 4.80% 16.34% 11.80%

1.5 $2.74 $1.24 54.74% 8.00% 4.80% 18.35% 10.93%

2.0 $2.94 $0.94 68.03% 8.00% 4.80% 21.66% 10.19%

2.5 $3.14 $0.64 79.62% 8.00% 4.80% 28.06% 9.54%

V-No Taxes V-Taxes

WACC = (D/V)rd(1-T) + (S/V)rs

$3,571,429

$2,142,857

$2,542,857

Total Market

Value of Firm

$3,571,429

25%

30%

35%

40%

45%

0% 20% 40% 60% 80% 100%

Debt/Value Ratio

rd x (1-T)

$2.50

$3.00

Relationship Between Value and Debt

Without Taxes

174

175

176

177

178

179

180

181

184

185

186

188

189

= NOPAT

195

196

197

198

199

200

208

209

210

211

Value of Tax Shield = (rd T D)/( rU – g

Of Firm $2,142,857 $3,571,429 $2,371,429 $4,028,571 Value of Firm = Value of Unlevered F

217

218

219

220

221

222

from part c.

228

229

230

A B C D E F G H I

50,000

7%

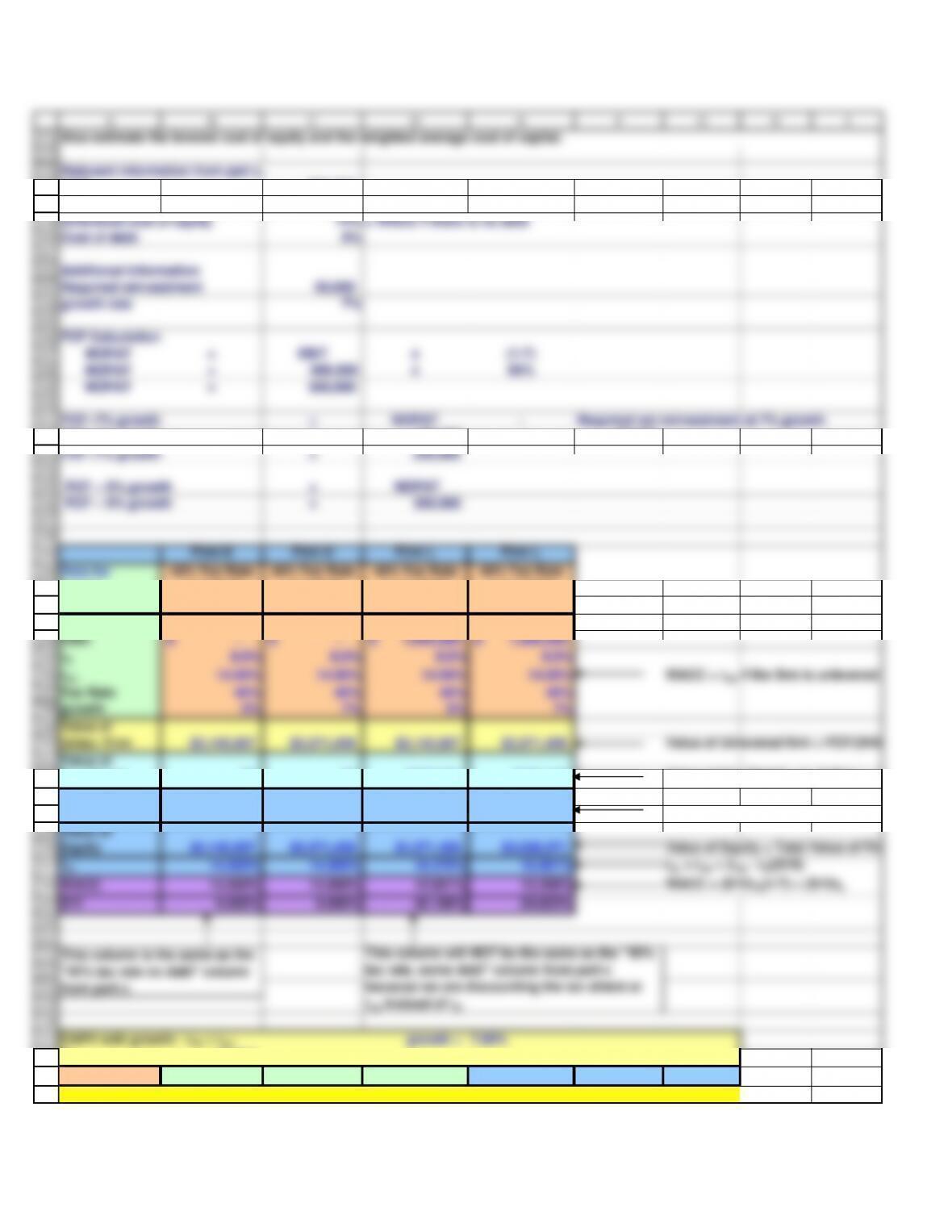

Relevant information from part c.

EBIT

500,000

Tax rate

40%

Unlevered cost of equity

14% = WACC if there is no debt

Cost of debt

8%

growth rate

FCF Calculation

NOPAT

NOPAT

=300,000

FCF — 0% growth

FCF — 0% growth

= 300,000

Firm U Firm U Firm L Firm L

Data for 40% Tax Rate 40% Tax Rate 40% Tax Rate 40% Tax Rate

growth 0% 7% 0% 7%

Value of

Unlev. Firm $2,142,857 $3,571,429 $2,142,857 $3,571,429 Value of Unlevered firm = FCF/(WAC

Value of

rsL 14.000% 14.000% 18.375% 15.981% rsL = rsU + (rsU – rd)(D/S)

WACC 14.000% 14.000% 12.651% 13.206%

WACC = (D/V)rd(1-T) + (S/V)rs

D/V 0.000% 0.000% 42.169% 24.823%

T = 40.00%

DV S D/V Tax shield

rsL WACC

$4,028,571 $3,028,571 24.823% $457,143 15.981% 13.206%

This column will NOT be the same as the “40%

This column is the same as the

Also estimate the levered cost of equity and the weighted average cost of capital.

231

232

233

234

235

236

237

238

239

240

241

242

248

249

250

251

252

253

259

260

261

262

263

264

270

271

272

273

274

11.20%

281

282

283

284

285

14.40% 13.44% 14.67% 13.68%

A B C D E F G H I

– 3,571,429 3,571,429 0.00% – 14.00% 14.00%

500,000 3,800,000 3,300,000 13.16% 228,571 14.91% 13.58%

1,000,000 4,028,571 3,028,571 24.82% 457,143 15.98% 13.21%

1,500,000 4,257,143 2,757,143 35.23% 685,714 17.26% 12.87%

2,000,000 4,485,714 2,485,714 44.59% 914,286 18.83% 12.57%

2,500,000 4,714,286 2,214,286 53.03% 1,142,857 20.77% 12.30%

3,000,000 4,942,857 1,942,857 60.69% 1,371,429 23.26% 12.06%

3,500,000 5,171,429 1,671,429 67.68% 1,600,000 26.56% 11.83%

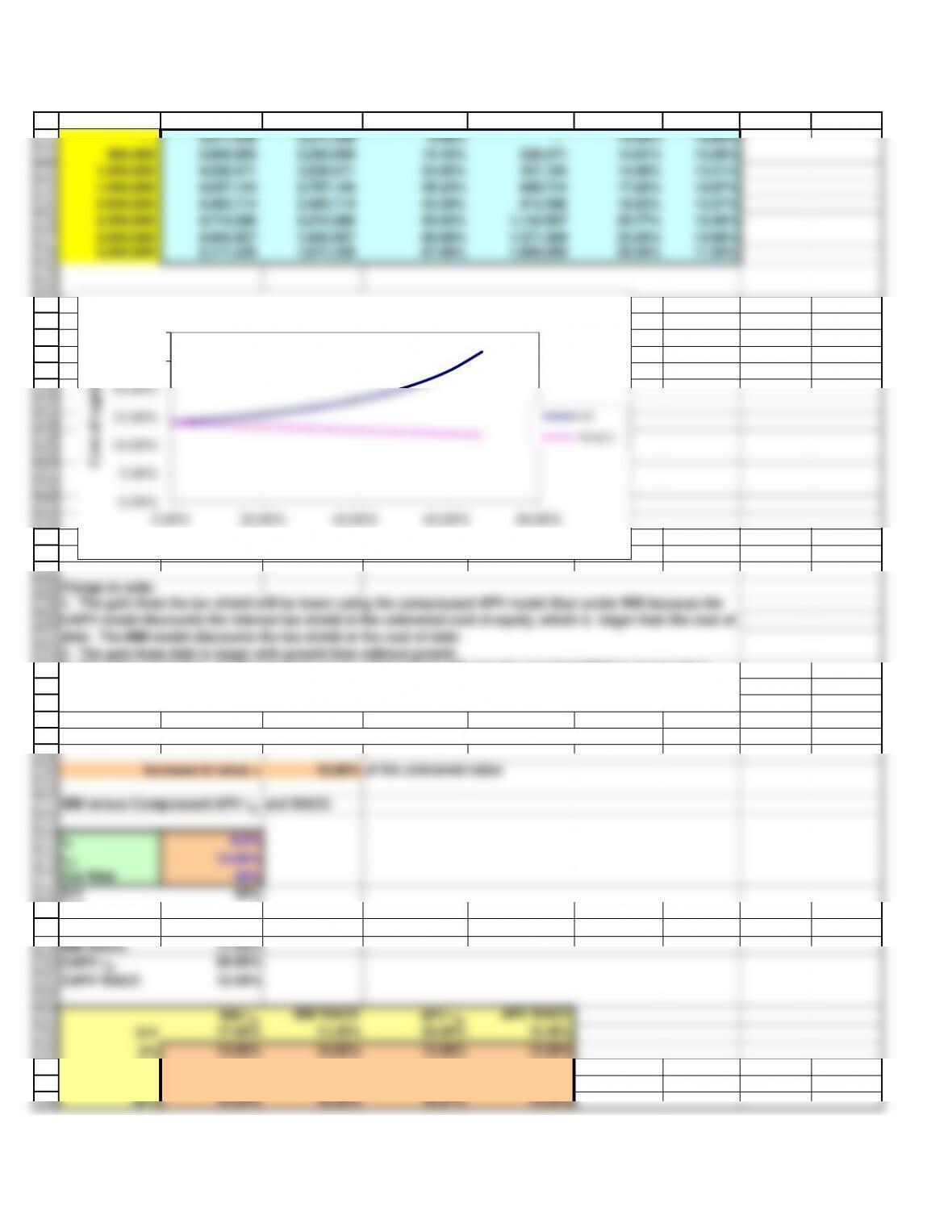

2. The gain from debt is larger with growth than without growth.

MM versus Compressed APV rsL and WACC

rd8.0%

rsU 14.00%

CAPV WACC

12.40%

MM rsL MM WACC APV rsL APV WACC

D/V 17.60% 11.20% 20.00% 12.40%

0%

14.00% 14.00% 14.00% 14.00%

1. The gain from the tax shield will be lower using the compressed APV model than under MM because the

CAPV model discounts the interest tax shield at the unlevered cost of equity, which is larger than the cost of

debt. The MM model discounts the tax shield at the cost of debt.

3. The value of the firm, whether levered or not, will be larger with growth, provided ROIC is greater than

WACC. Although we don’t show it here, ROIC is greater than WACC, so the value of the firm increases with

0.00%

5.00%

10.00%

15.00%

Cost of capital

Cost of Capital with growth

WACC

289

290

291

292

293

294

295

296

302

303

304

305

306

307

313

314

315

316

317

323

324

325

326

327

A B C D E F G H I

40%

16.40% 11.76% 18.00% 12.72%

50%

17.60% 11.20% 20.00% 12.40%

60%

19.40% 10.64% 23.00% 12.08%

70%

22.40% 10.08% 28.00% 11.76%

80% 28.40% 9.52% 38.00% 11.44%

Tax Rate = 40%

Free Cash Flow

$250.00 $290.00 $320.00

rsU = 14.00%

Interest expense

$80.00 $95.00 $120.00

gL = 7%

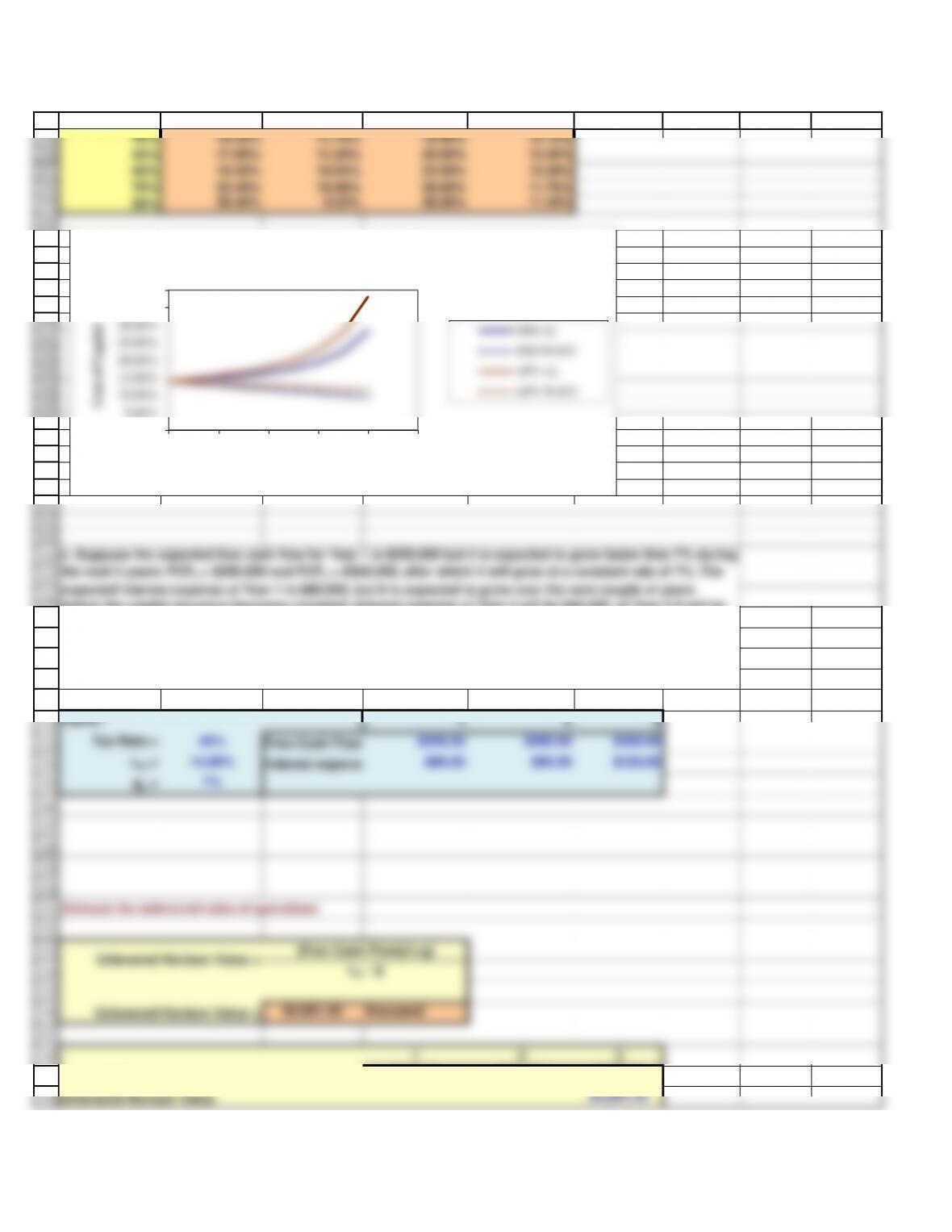

e. Suppose the expected free cash flow for Year 1 is $250,000 but it is expected to grow faster than 7% during

the next 3 years: FCF2 = $290,000 and FCF3 = $320,000, after which it will grow at a constant rate of 7%. The

expected interest expense at Year 1 is $80,000, but it is expected to grow over the next couple of years

before the capital structure becomes constant: Interest expense at Year 2 will be $95,000, at Year 3 it will be

$120,000 and it will grow at 7% thereafter. What is the estimated horizon unlevered value of operations (i.e.,

0.00%

5.00%

10.00%

15.00%

20.00%

Cost of Capital

Costs of capital for MM and APV

APV rsL

APV WACC