1

2

3

4

5

6

7

A B C D E F G H I

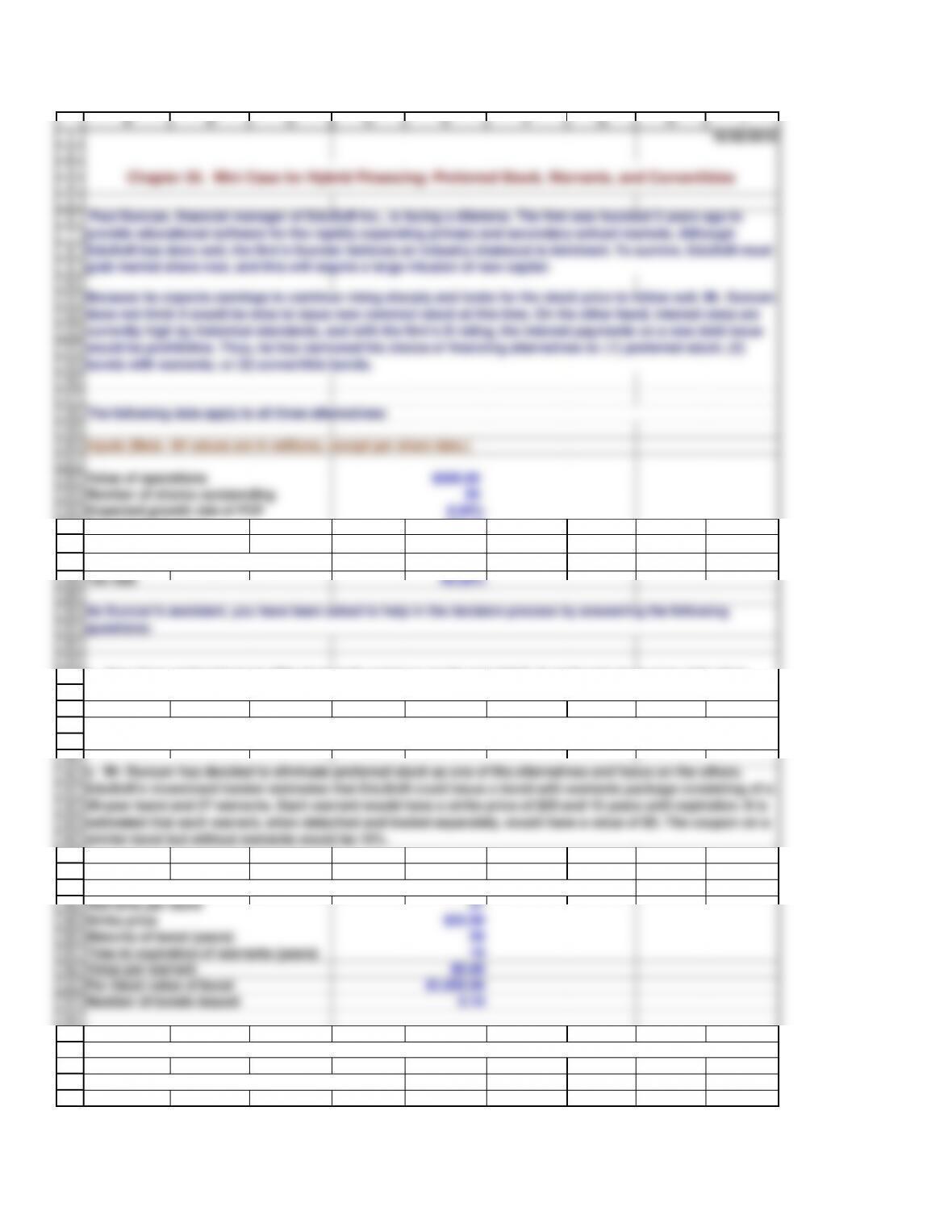

does not think it would be wise to issue new common stock at this time. On the other hand, interest rates are

10/28/2015

Paul Duncan, financial manager of EduSoft Inc., is facing a dilemma. The firm was founded 5 years ago to

provide educational software for the rapidly expanding primary and secondary school markets. Although

Chapter 20. Mini Case for Hybrid Financing: Preferred Stock, Warrants, and Convertibles

61

62

63

64

Bonds

66

67

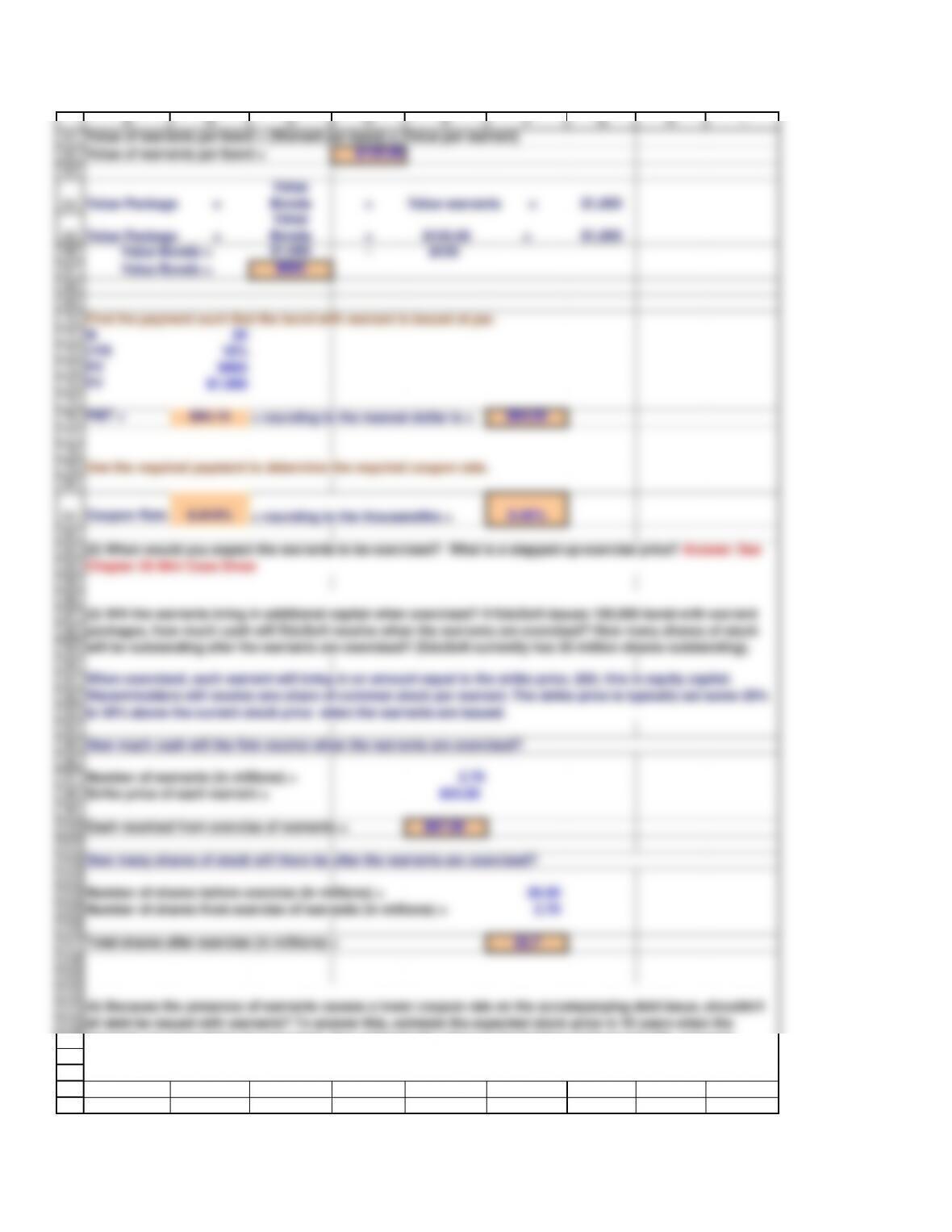

Find the payment such that the bond with warrant is issued at par.

73

74

75

76

77

78

79

80

81

82

86

87

88

89

90

91

92

to 30% above the current stock price when the warrants are issued.

How much cash will the firm receive when the warrants are exercised?

98

99

100

101

102

Number of shares before exercise (in millions) = 20.00

Number of shares from exercise of warrants (in millions) = 2.70

106

107

109

110

111

112

113

114

115

A B C D E F G H I

Value of warrants per bond = (Warrant per bond) x (Value per warrant)

Value of warrants per bond = $135.00

Value Package =

Value

Bonds

+Value warrants = $1,000

Value

$1,000 – $135

$865

PV $865

FV $1,000

PMT = $84.14 = rounding to the nearest dollar is = $84.00

Coupon Rate 8.414% = rounding to the thousandths = 8.40%

Strike price of each warrant = $25.00

Cash received from exercise of warrants = $67.50

Total shares after exercise (in millions) = 22.7

Use the required payment to determine the required coupon rate.

When exercised, each warrant will bring in an amount equal to the strike price, $25; this is equity capital.

Warant-holders will receive one share of common stock per warrant. The strike price is typically set some 20%

Value Bonds =

Value Bonds =

(3) Will the warrants bring in additional capital when exercised? If EduSoft issues 100,000 bond-with-warrant

packages, how much cash will EduSoft receive when the warrants are exercised? How many shares of stock

will be outstanding after the warrants are exercised? (EduSoft currently has 20 million shares outstanding).

(4) Because the presence of warrants causes a lower coupon rate on the accompanying debt issue, shouldn’t

all debt be issued with warrants? To answer this, estimate the expected stock price in 10 years when the

warrants are expected to be exercised, then estimate the return to the holders of the bond-with- warrants

packages. Use the corporate valuation model to estimate the expected stock price in 10 years. Assume that

EduSoft’s current value of operations is $500 million and it is expected to grow at 8% per year.

How many shares of stock will there be after the warrants are exercised?

118

119

120

121

122

123

124

125

128

129

Current valuation analysis

131

132

133

134

135

136

Value of operations $500

Total intrinsic value of firm $500

142

143

144

145

146

147

Required inputs:

Number of years until expiration = 10

153

154

155

156

157

163

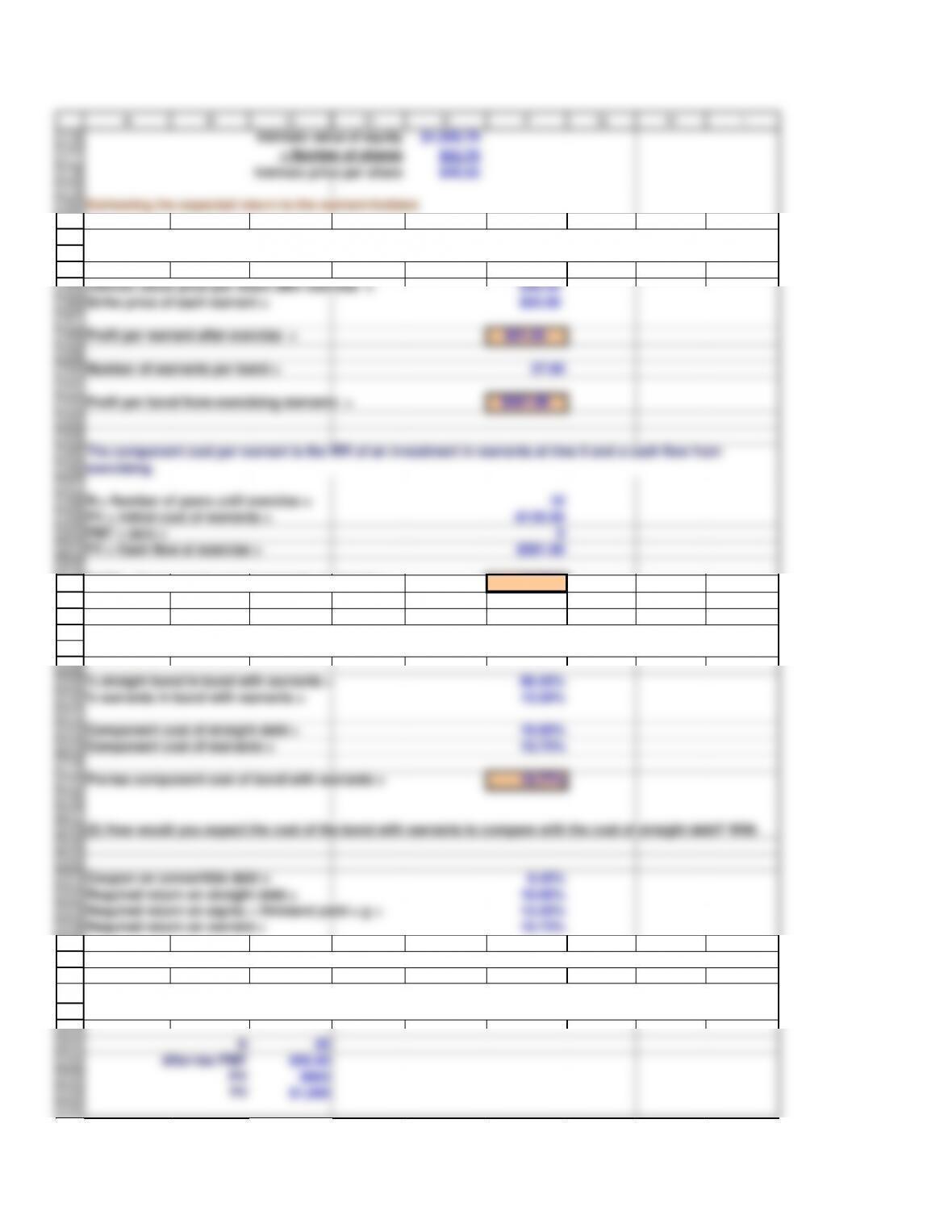

Coupon rate 8.40%

PMT $84

164

165

166

167

168

169

170

171

172

174

175

A B C D E F G H I

The cost of debt debt is the cost of straight debt = rd = 10%

Required inputs:

Initial Vop $500

Initial value of debt = Number of bonds x Iissue price $100

Number of shares outstanding 20

Intrinsic value of equity $400

÷ Number of shares 20

Intrinsic price per share $20.00

Valuation analysis in 10 years when warrants expire

Expected V10 =$500 * 2.159

Expected V10 =$1,079.46

Price = $901.69

Number of bonds (in millions) 0.10

Total bond value (in millions) = $90.169

Intrinsic stock price in at expiration

Value of operations $1,079.46

Total intrinsic value of firm $1,146.96

− Debt $90.17

How much will the bonds be worth in 10 years? (There will be 10 years remaining to maturity.)

Begin by estimating the required return on the debt, rd, and the required return on the warrants, rw. To find the

overall cost of capital for the convertible bond, rc, comine the cost of straight debt with the cost of the warrant,

weighting them by the percentages they comprise of the bond-with-warrants package.

To find the cost of warrants, we will find the expected profit of the warrant holders and the expected return. If

the warrants are very likely to be in the money at expiration, then we can approximate the expected profit by

expected growth rate.

176

177

178

179

180

181

182

187

Intrinsic stock price per share after exercise = $46.55

Strike price of each warrant = $25.00

188

189

190

191

192

194

195

198

199

200

201

202

203

209

210

211

212

213

214

215

Pre-tax component cost of bond with warrants = 10.77%

221

222

223

224

225

232

233

234

235

A B C D E F G H I

Intrinsic value of equity $1,056.79

÷ Number of shares $22.70

Intrinsic price per share $46.55

Estimating the expected return to the warrant-holders

Profit per warrant after exercise = $21.55

Number of warrants per bond = 27.00

Profit per bond from exercising warrants = $581.98

N = Number of years until exercise = 10

PV = Intitial cost of warrants = -$135.00

PMT = zero = 0

FV = Cash flow at exercise = $581.98

RATE = Component cost of warrants per bond = 15.73%

% straight bond in bond with warrants = 86.50%

% warrants in bond with warrants = 13.50%

Component cost of straight debt = 10.00%

Component cost of warrants = 15.73%

Coupon on convertible debt = 8.40%

Required return on straight debt = 10.00%

Required return on equity = Dividend yield + g = 13.40%

Required return on warrant = 15.73%

After-tax PMT $50.40

PV $865

FV $1,000

The per warrant profit to the warrant-holder is equal to the stock price minus the strike price. The total profit

The component cost per warrant is the IRR of an investment in warrants at time 0 and a cash flow from

236

237

238

239

240

241

242

243

244

245

246

250

251

252

253

254

Conversion ratio = 40

Maturity (in years) of convertible bond = 20

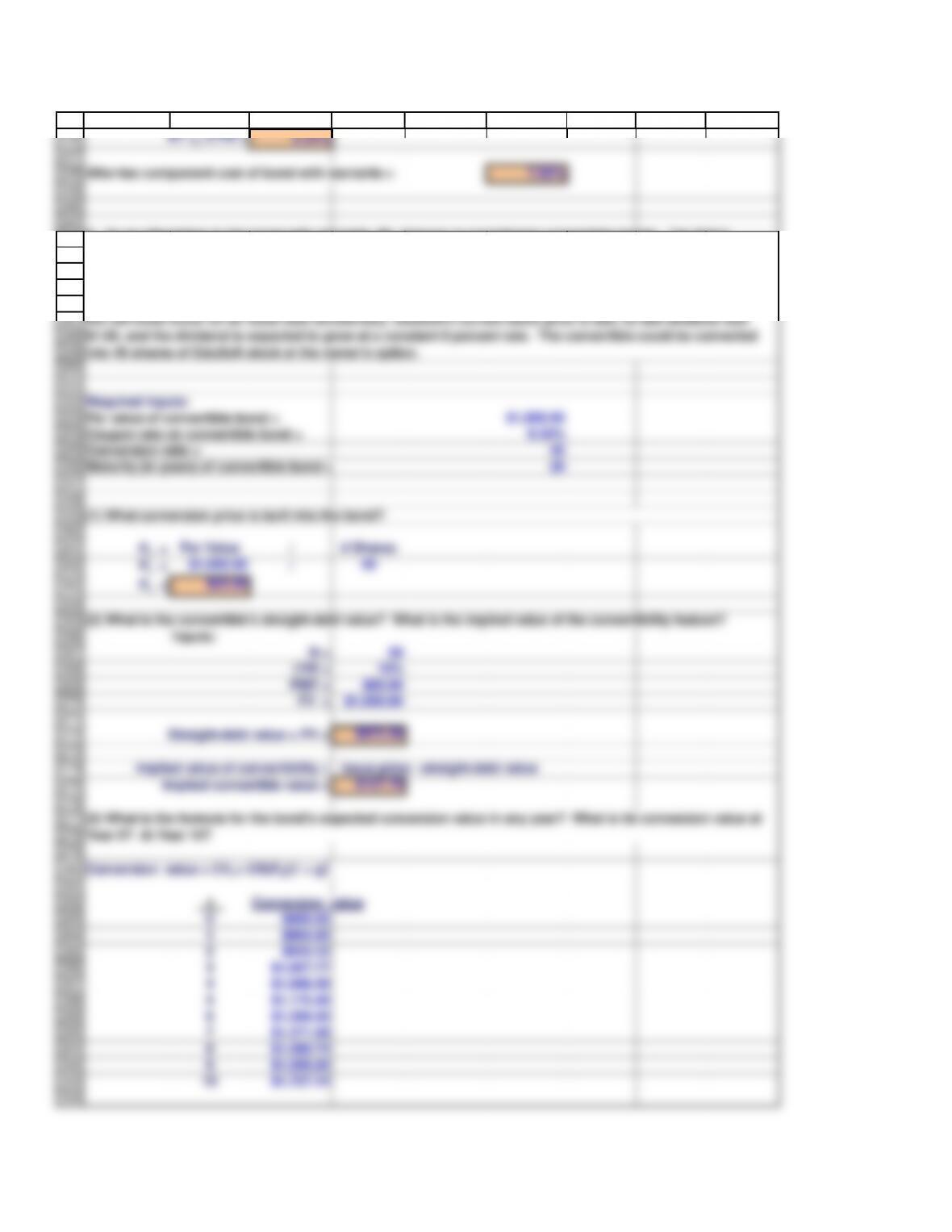

(1) What conversion price is built into the bond?

261

262

263

264

265

into 40 shares of EduSoft stock at the owner’s option.

271

272

273

274

275

276

278

279

280

281

282

283

284

285

286

287

5$1,175.46

6$1,269.50

7$1,371.06

8$1,480.74

9$1,599.20

294

A B C D E F G H I

AT rd =I/YR = 6.24%

After-tax component cost of bond with warrants = 7.52%

Required inputs:

Par value of convertible bond = $1,000.00

Coupon rate on convertible bond = 8.50%

Pc = Par Value /# Shares

Pc = $1,000.00 /40

Pc = $25.00

Straight-debt value = PV = $872.30

Implied value of convertibility = Issue price – straight-debt value

Implied convertible value = $127.70

Conversion value = CVt = CR(P0)(1 + g)t.

t Conversion value

0$800.00

1$864.00

2$933.12

3$1,007.77

4$1,088.39

Year 0? At Year 10?

d. As an alternative to the bond with warrants, Mr. Duncan is considering convertible bonds. The firm’s

investment bankers estimate that EduSoft could sell a 20-year, 8.5 percent annual coupon, callable convertible

bond for its $1,000 par value, whereas a straight-debt issue would require a 12 percent coupon. The

convertibles would be call protected for 5 years, the call price would be $1,100, and the company would

probably call the bonds as soon as possible after their conversion value exceeds $1,200. Note, though, that

(2) What is the convertible’s straight-debt value? What is the implied value of the convertibility feature?

295

296

297

298

299

300

301

302

304

305

306

307

308

309

7$1,371.06 $603.79 $1,371.06

8$1,480.74 $579.16 $1,480.74

9$1,599.20 $552.08 $1,599.20

315

316

317

318

319

320

to be called? (Hint: Recall that the call must be made on an anniversary date of the issue.)

Notice that the conversion value grows at the same rate as the stock. So the first step is to find the number of

years until the initial conversion value grows to the value at which it will be called.

326

327

328

329

330

331

just found up to the next integer. Also, we must verify that the year is at least as great as the number of years

the bond is protected from calls.

337

338

339

340

341

342

conversion, the bondholder will also receive the conversion value. We can find the return using the RATE

348

349

350

351

0$800.00 $723.65 $800.00

352

353

A B C D E F G H I

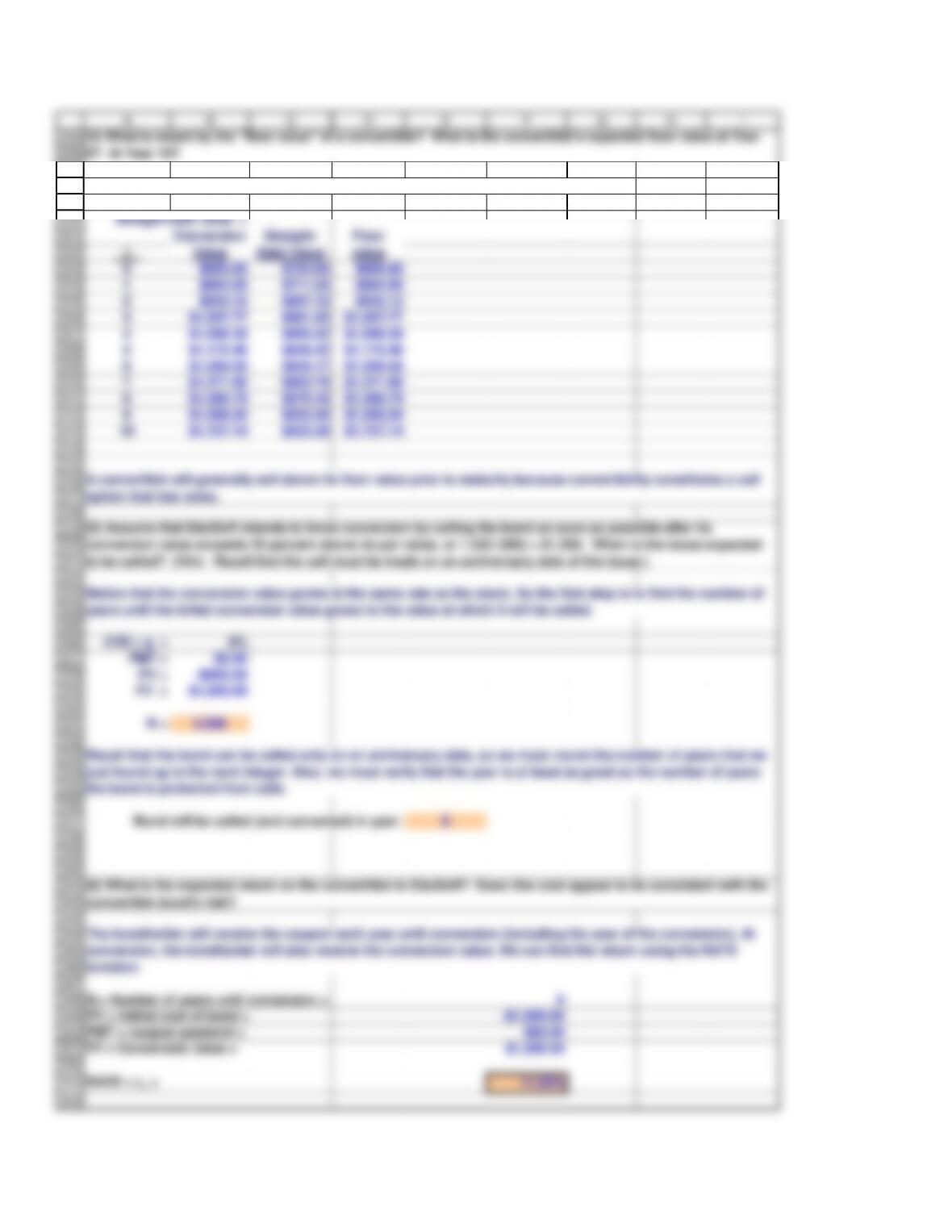

The floor value is the higher of the straight debt value and the conversion value.

Straight-debt value =

t

1$864.00 $711.02 $864.00

2$933.12 $697.12 $933.12

3$1,007.77 $681.83 $1,007.77

4$1,088.39 $665.02 $1,088.39

5$1,175.46 $646.52 $1,175.46

6$1,269.50 $626.17 $1,269.50

I/YR = g = 8%

PMT = $0.00

PV = -$800.00

FV = $1,200.00

N = 5.268

Bond will be called (and converted) in year: 6

N = Number of years until conversion = 6

PV = Intitial cost of bond = -$1,000.00

PMT = coupon payment = $85.00

FV = Conversion value = $1,269.50

RATE = rc = 11.83%

(4) What is meant by the “floor value” of a convertible? What is the convertible’s expected floor value at Year

0? At Year 10?

(5) Assume that EduSoft intends to force conversion by calling the bond as soon as possible after its

conversion value exceeds 20 percent above its par value, or 1.2($1,000) = $1,200. When is the issue expected

A convertible will generally sell above its floor value prior to maturity because convertibility constitutes a call

option that has value.

(6) What is the expected return on the convertible to EduSoft? Does this cost appear to be consistent with the

convertible bond’s risk?

Conversion

Value

Straight-

Debt Value

Floor

value

355

356

357

358

359

360

361

362

363

364

365

366

367

368

369

370

371

372

373

374

378

379

380

381

382

383

389

390

391

392

393

394

400

A B C D E F G H I

decision based on other factors. What are some of the factors which he should consider?

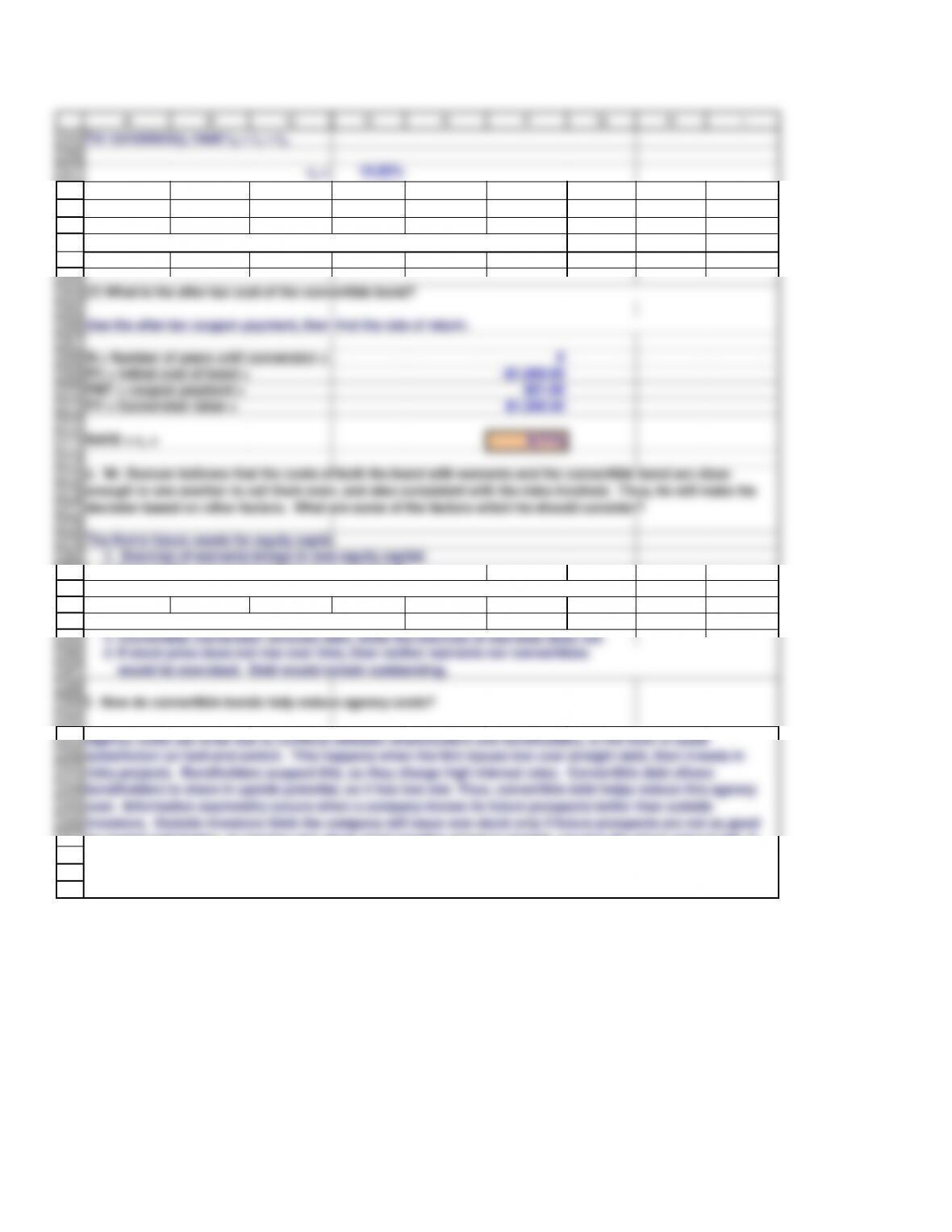

For consistency, need rd < rc < rs.

10.00%

rc = 11.83%

rs = 13.40%

Since rc is between rd and rs, the costs are consistent with the risks.

N = Number of years until conversion = 6

PV = Intitial cost of bond = -$1,000.00

PMT = coupon payment = $51.00

FV = Conversion value = $1,269.50

RATE = rc = 8.71%

1. Exercise of warrants brings in new equity capital.

2. Convertible conversion brings in no new funds.

3. In either case, new lower debt ratio can support more financial leverage.

f. How do convertible bonds help reduce agency costs?

Agency costs can arise due to conflicts between shareholders and bondholders, in the form of asset

substitution (or bait-and-switch. This happens when the firm issues low cost straight debt, then invests in

risky projects. Bondholders suspect this, so they charge high interest rates. Convertible debt allows

converted into equity, which is what the company wants to issue.

(7) What is the after-tax cost of the convertible bond?

Use the after-tax coupon payment, then find the rate of return.

The firm’s future needs for equity capital:

rd =