1

2

3

4

5

6

7

8

9

10

11

12

13

19

20

21

22

23

24

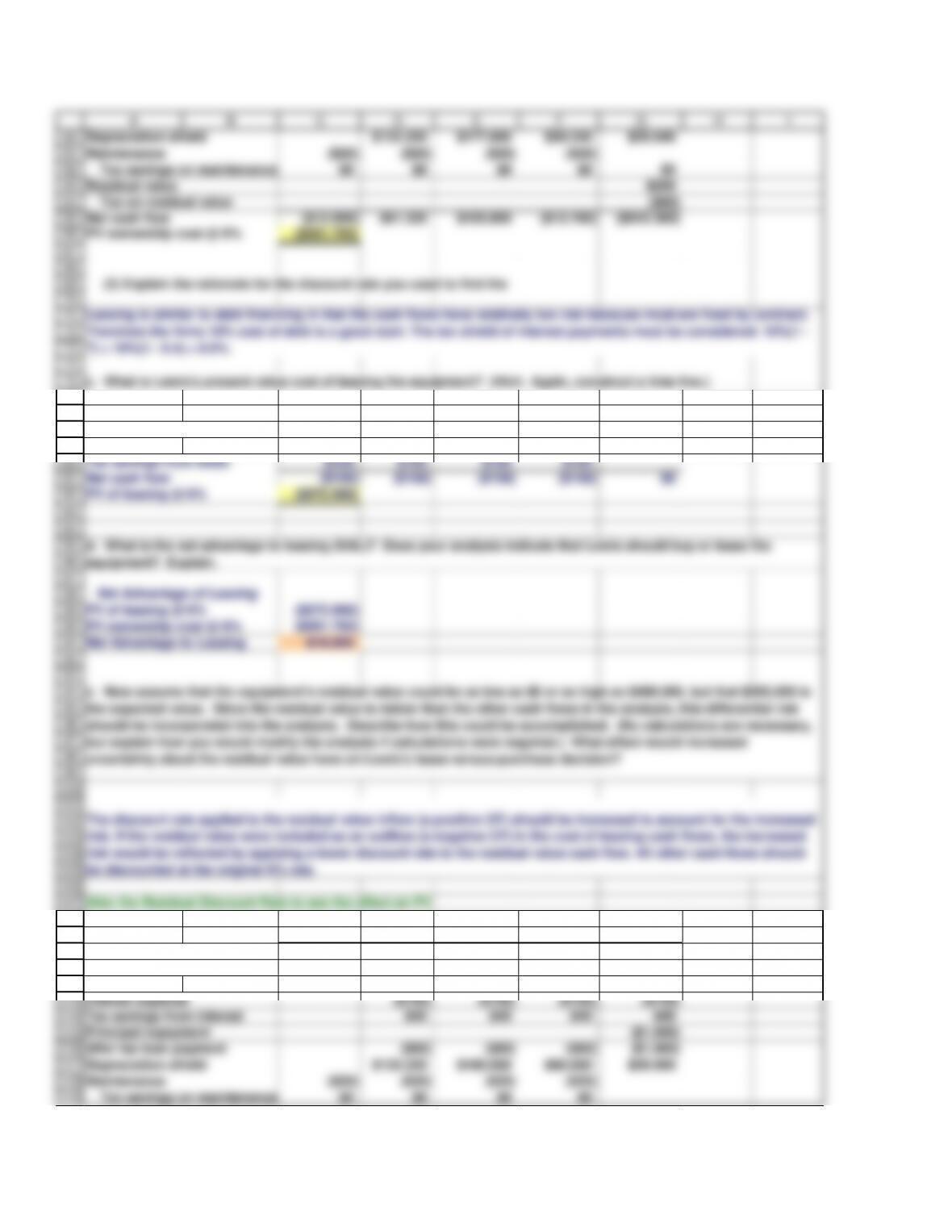

(4) What effect does leasing have on a firm’s balance sheet? Answer: See Chapter 19 Mini Case Show

(3) How are leases classified for tax purposes? Answer: See Chapter 19 Mini Case Show

(5) What effect does leasing have on a firm’s capital structure? Answer: See Chapter 19 Mini Case

29

30

31

32

33

34

35

New Equipment cost $1,000 KEY OUTPUT

New Equipment life 4

Equip. Residual Value $200 LEASE

Tax Rate 40% because the net advantage of leasing is $18.80

41

42

43

44

45

46

Depreciation Rate 33.33% 44.45% 14.81% 7.41%

Depreciation Expense 333.30 444.50 148.10 74.10

BV at end of year 666.70 222.20 74.10 –

52

53

54

55

56

57

Principal repayment ($1,000)

After tax loan payment ($60) ($60) ($60) ($1,060)

A B C D E F G H I

10/28/2015

Input Data

(all dollar figures in thousands)

Loan interest rate 10%

Annual rental charge $260

After-tax cost of debt 6%

Maintenance if not leased $20

Year = 0 1 2 3 4

Present Value of Owning

Equipment cost ($1,000)

Loan amount $1,000

Interest expense ($100) ($100) ($100) ($100)

Tax savings from interest 40 40 40 40

b. (1) What is the present value cost of owning the equipment? (Hint: Set up a time line which shows the net cash

flows over the period t = 0 to t = 4, and then find the PV of these net cash flows, or the PV cost of owning.)

Chapter 19. Mini Case for Lease Financing

Lewis Securities Inc. has decided to acquire a new market data and quotation system for its Richmond home office.

The system receives current market prices and other information from several on-line data services, then either

displays the information on a screen or stores it for later retrieval by the firm’s brokers. The system also permits

customers to call up current quotes on terminals in the lobby.

The equipment costs $1,000,000, and, if it were purchased, Lewis could obtain a term loan for the full purchase price

at a 10 percent interest rate. Although the equipment has a six-year useful life, it is classified as a special-purpose

computer, so it falls into the MACRS 3-year class. If the system were purchased, a 4-year maintenance contract could

be obtained at a cost of $20,000 per year, payable at the beginning of each year. The equipment would be sold after 4

As an alternative to the borrow-and-buy plan, the equipment manufacturer informed Lewis that Consolidated Leasing

would be willing to write a 4-year guideline lease on the equipment, including maintenance, for payments of $260,000

at the beginning of each year. Lewis’s marginal federal-plus-state tax rate is 40 percent. You have been asked to

analyze the lease-versus-purchase decision, and in the process to answer the following questions:

a. (1) Who are the two parties to a lease transaction? Answer: See Chapter 19 Mini Case Show

60

61

62

63

64

65

66

67

72

73

74

75

76

82

Lease payment ($260) ($260) ($260) ($260)

Tax savings from lease $104 $104 $104 $104

Net cash flow ($156) ($156) ($156) ($156) $0

(2) Explain the rationale for the discount rate you used to find the

83

84

85

86

87

89

90

Net Advantage to Leasing $18.803

94

95

96

97

98

risk would be reflected by applying a lower discount rate to the residual value cash flow. All other cash flows should

105

106

107

108

109

Present Value of Owning

Equipment cost ($1,000)

Loan amount $1,000

Interest expense ($100) ($100) ($100) ($100)

Tax savings from interest $40 $40 $40 $40

Principal repayment ($1,000)

116

117

118

119

A B C D E F G H I

Depreciation shield $133.320 $177.800 $59.240 $29.640

Maintenance ($20) ($20) ($20) ($20)

Tax savings on maintenance

$8 $8 $8 $8 $0

Residual value $200

Tax on residual value ($80)

Net cash flow ($12.000) $61.320 $105.800 ($12.760) ($910.360)

PV ownership cost @ 6% ($591.793)

c. What is Lewis’s present value cost of leasing the equipment? (Hint: Again, construct a time line.)

PV of leasing @ 6% ($572.990)

PV ownership cost @ 6% ($591.793)

Alter the Residual Discount Rate to see the effect on PV

Year = 0 1 2 3 4

After tax loan payment ($60) ($60) ($60) ($1,060)

Depreciation shield $133.320 $180.000 $60.000 $28.000

Maintenance ($20) ($20) ($20) ($20)

Tax savings on maintenance

$8 $8 $8 $8

d. What is the net advantage to leasing (NAL)? Does your analysis indicate that Lewis should buy or lease the

equipment? Explain.

be discounted at the original 6% rate.

e. Now assume that the equipment’s residual value could be as low as $0 or as high as $400,000, but that $200,000 is

the expected value. Since the residual value is riskier than the other cash flows in the analysis, this differential risk

should be incorporated into the analysis. Describe how this could be accomplished. (No calculations are necessary,

but explain how you would modify the analysis if calculations were required.) What effect would increased

uncertainty about the residual value have on Lewis’s lease-versus-purchase decision?

Therefore the firms 10% cost of debt is a good start. The tax shield of interest payments must be considered. 10%(1 –

T) = 10%(1 – 0.4) = 6.0%.

120

121

122

123

124

125

126

127

To the lessor, writing the lease is an investment. Therefore, the lessor must compare the return on the lease

A B C D E F G H I

Tax on residual value ($80)

Cash flow without residual $ (12) $ 61 $ 108 $ (12) $ (1,112)

Residual cash flow $ – $ – $ – $200

PV minus residual @ 6% (748.91)$

PV of residual @

6% $158.42

PV of ownership

$ (590.50) Residual Discount Rate 6.00%

The lessor owns the equipment when the lease expires. Therefore, residual value risk is passed from the lessee to the

179

180

181

A B C D E F G H I

A cancellation clause would lower the risk of the lease to the lessee but raise the lessor’s risk. To account for this, the

lessor would increase the annual lease payment or else impose a penalty for early cancellation.