1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

36

37

A B C D E F G H I J

Days sales outstanding (365-day basis) 45.63 32.00

Inventory turnover 10.80 20.00

Fixed assets turnover 7.75 13.22

Total assets turnover 2.60 3.00

Profit margin on sales 2.07% 3.50%

Return on equity (ROE) 10.45% 21.00%

10/28/2015

RR Industry

Current 1.75 2.25

Quick 0.92 1.16

TL/assets 58.76% 50.00%

Turnover of cash 16.67 22.22

Payables deferral period 30.00 33.00

Karen Johnson, CFO for Raucous Roasters (RR), a specialty coffee manufacturer, is rethinking her company’s working capital

policy in light of a recent scare she faced when RR’s corporate banker, citing a nationwide credit crunch, balked at renewing

RR’s line of credit. Had the line of credit not been renewed, RR would not have been able to make payroll, potentially forcing the

company out of business. Although the line of credit was ultimately renewed, the scare has forced Johnson to examine carefully

each component of RR’s working capital to make sure it is needed, with the goal of determining whether the line of credit can be

eliminated entirely. In addition to (possibly) freeing RR from the need for a line of credit, Johnson is well aware that reducing

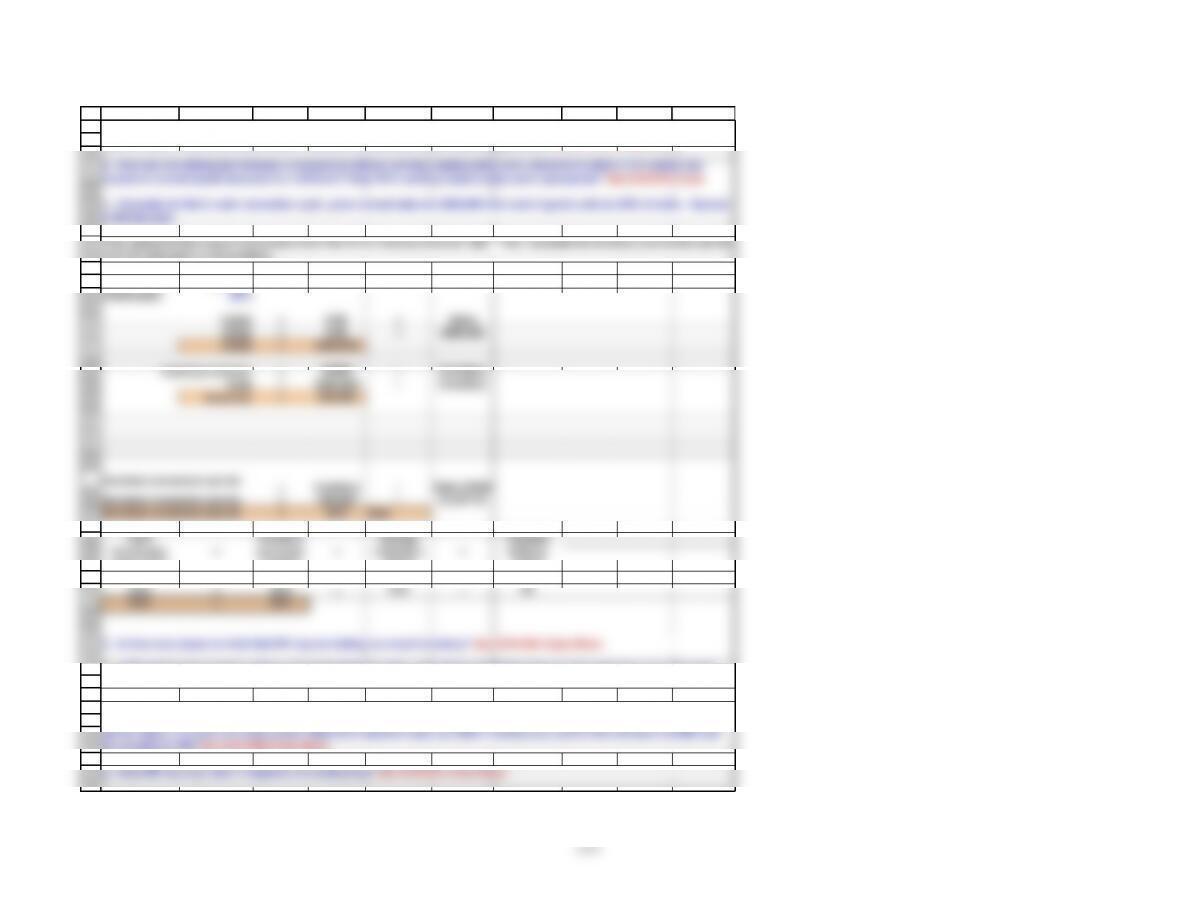

Historically, RR has done little to examine working capital, mainly because of poor communication among business functions. In

the past, the production manager resisted Johnson’s efforts to question his holdings of raw materials, the marketing manager

resisted questions about finished goods, the sales staff resisted questions about credit policy (which affects accounts

receivable), and the treasurer did not want to talk about the cash and securities balances. However, with the recent credit scare,

this resistance became unacceptable and Johnson has undertaken a company-wide examination of cash, marketable securities,

Chapter 16. Mini Case for Supply Chains and Working Capital Management

Johnson also knows that decisions about working capital cannot be made in a vacuum. For example, if inventories could be

lowered without adversely affecting operations, then less capital would be required, and free cash flow would increase. However,

lower raw materials inventories might lead to production slowdowns and higher costs, and lower finished goods inventories

might lead to stock-outs and loss of sales. So, before inventories are changed, it will be necessary to study operating as well as

financial effects. The situation is the same with regard to cash and receivables. Johnson has begun her investigation by

38

39

40

41

42

43

44

45

46

47

48

55

56

57

58

59

65

66

67

68

69

77

78

79

80

81

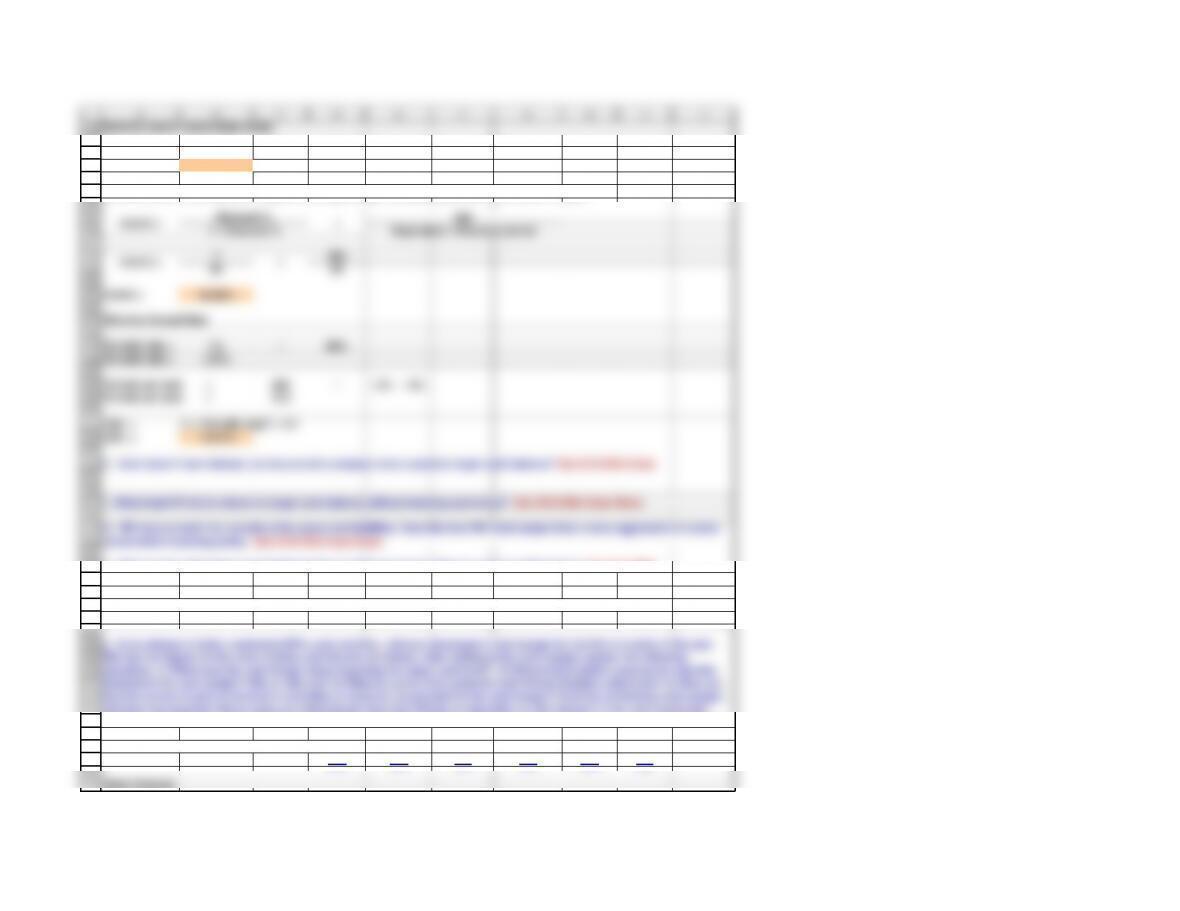

g. Does RR face any risks if it tightens its credit policy? See Ch16 Mini Case Show.

should tighten or loosen its credit policy? What four variables make up a firm’s credit policy, and in what direction should each

be changed by RR? See Ch16 Mini Case Show.

88

A B C D E F G H I J

COGS =0.90 × Sales

COGS =0.90 × $660,000

COGS =$594,000

=COGS / Inventory

10.80 =$594,000 / Inventory

Inventory =$55,000

=

Inventory / Daily COGS

=$55,000 / $1,627.40

=33.8 days

c. Calculate the firm’s cash conversion cycle given annual sales are $660,000 and cost of goods sold are 90% of sales. Assume

a 365-day year.

First, determine the amount of inventory from the firm’s inventory turnover ratio. Then, calculate the inventory conversion period

from the data given in the problem.

b. How can one distinguish between a relaxed but rational working capital policy and a situation in which a firm simply has

excessive current assets because it is inefficient? Does RR’s working capital policy seem appropriate? See Ch16 Mini Case

a. Johnson plans to use the preceding ratios as the starting point for discussions with RR’s operating team. Based on the data,

does RR seem to be following a relaxed, moderate, or restricted current asset usage policy? See Ch16 Mini Case Show.

Inventory turnover

d. Is there any reason to think that RR may be holding too much inventory? See Ch16 Mini Case Show.

Inventory conversion period

Inventory conversion period

e. If RR reduces its inventory without adversely affecting sales, what effect should this have on free cash flow: (1) in the short

run and (2) in the long run? See Ch16 Mini Case Show.

Payables

Cash

Inventory

Average

89

90

91

92

93

94

95

96

97

98

99

100

101

102

103

104

105

106

107

108

109

110

111

116

117

118

119

120

121

Credit Breakdown

127

A B C D E F G H I J

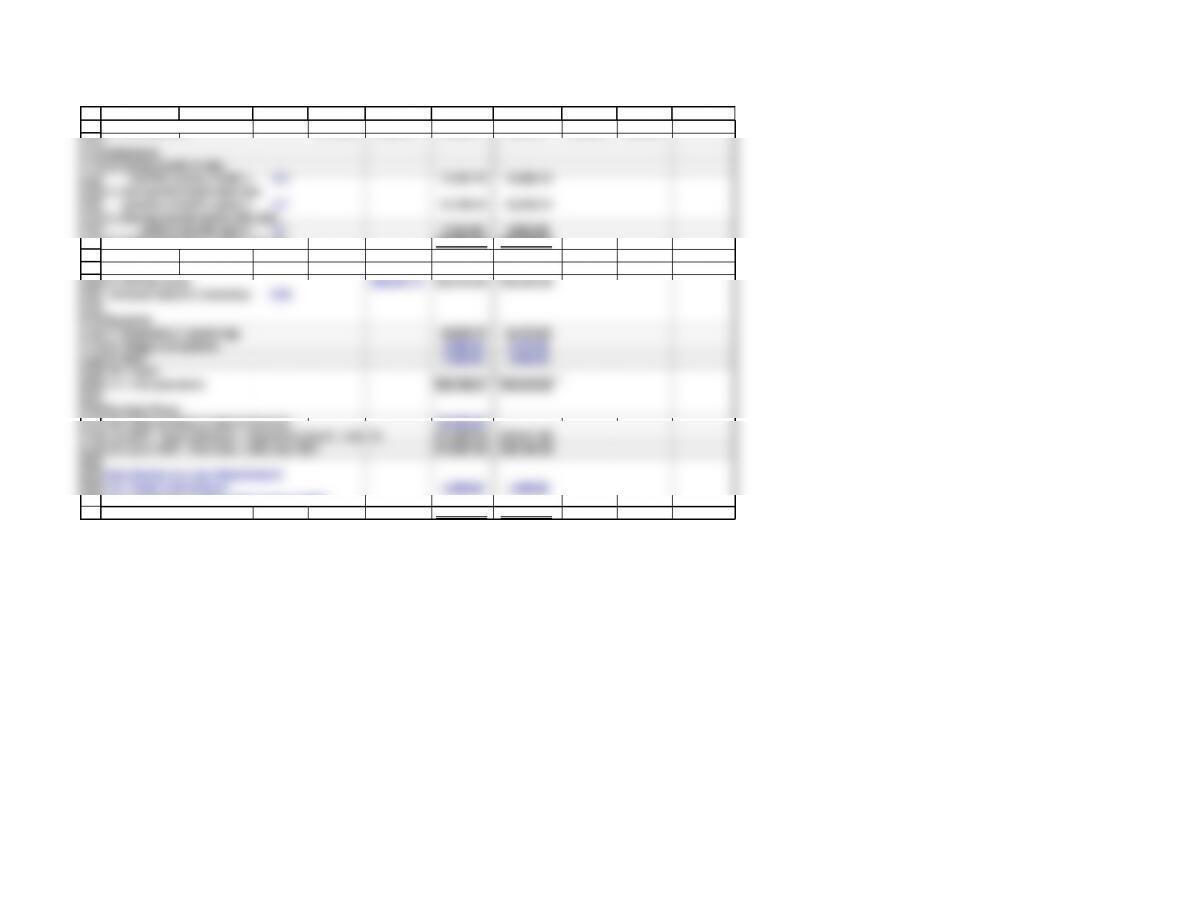

Payables level if discount is taken:

Terms: free credit period = 10 days.

“Official” credit period = 30 days.

Credit period taken = 40

Discount = 1%

Annual net purchases = $200,000

Annual gross purchases = $202,020

Gross – net purchase = $2,020

Company buys goods worth $200,000. That’s the cash price.

They must pay $2,020 more over the year if they forego the discount.

Think of the extra $2,020 as a financing cost similar to the interest on a loan.

Payables = $548 ×10

Payables = $5,479

Payables level if don’t take discount:

Payables = $548 ×40

Payables = $21,918

j. Assume that RR purchases $200,000 (net of discounts) of materials on terms of 1/10, net 30, but that it can get

away with paying on the 40th day if it chooses not to take discounts. How much free trade credit can the company

get from its equipment supplier, how much costly trade credit can it get, and what is the percentage cost of the

costly credit? Should RR take discounts?

h. If the company reduces its DSO without seriously affecting sales, what effect would this have on its free cash flows: (1) in the

short run and (2) in the long run? See Ch16 Mini Case Show.

i. What is the impact of higher levels of accruals, such as accrued wages or accrued taxes? Is it likely that RR could

make changes to accruals? See Ch16 Mini Case Show.

128

129

130

131

132

133

134

135

136

138

139

140

141

142

Effective Annual Rate

Periodic rate = 1% /99%

Periodic rate = 1.01%

Periods per year = 365 /( 40 – 10 )

149

150

151

152

153

A B C D E F G H I J

Nominal cost of costly trade credit:

r(nom) = $2,020 / $16,438

r(nom) = 12.29%

But the $2,020 in lost discounts is paid all during the year, not just at year-end, so the EAR is higher.

1365

99 30

r(nom) = 12.29%

Periods per year = 12.2

EAR =

(1 + Periodic rate)n – 1.0

EAR = 13.01%

r(nom) =

×

Discount %

r(nom) =

1 – Discount %

Days taken – Discount period

×

365

180

181

182

183

184

185

186

187

188

189

190

191

192

193

194

195

196

197

198

199

200

201

202

203

204

205

206

207

208

209

210

A B C D E F G H I J

( 1 ) Sales (gross) $71,218 $68,212 $65,213 $52,475 $42,909 $30,524

Collections

( 2) During month of sale

(month’s sales) x (0.98) x 0.2 12,781.75 10,285.10

( 3 ) During first month after sale

(previous month’s sales) x 0.7 47,748.40 45,649.10

( 4 ) During second month after sale

(sales 2 months ago) x 0.1 7,121.80 6,821.20

( 5 ) Total collections (Lines 2 + 3 + 4) $67,651.95 $62,755.40

Purchases

( 6 ) During month $44,603.75 $36,472.65 $25,945.40

(forecast sales in 2 months)x 0.85

Payments

( 7 ) Payments (1-month lag) 44,603.75 36,472.65

( 8 ) Wages and salaries 6,690.56 5,470.90

( 9 ) Rent 2,500.00 2,500.00

( 10 ) Taxes

( 11 ) Total payments $53,794.31 $44,443.55

Net Cash Flows

( 12 ) Cash on hand at start of forecast $3,000.00

( 13 ) NCF: Total Collection – Payments (Line 5 – Line 11) $13,857.64 $18,311.85

( 14 ) Cum. NCF: Prior mos. + this mos. NCF $16,857.64 $35,169.49

Cash Surplus (or Loan Requirement)

( 15 ) Target cash balance 1,500.00 1,500.00

( 16 ) Cumulative surplus cash or loan needed

(Line 16 – Line 17) $15,357.64 $33,669.49