Mini Case: 15 – 19

i. Describe the recapitalization process and apply it to PizzaPalace. Calculate the

resulting the value of the debt that will be issued, the resulting market value of

equity, the price per share, the number of shares repurchased, and the

remaining shares. Considering only the capital structures under analysis, what is

PizzaPalace’s optimal capital structure?

Answer:

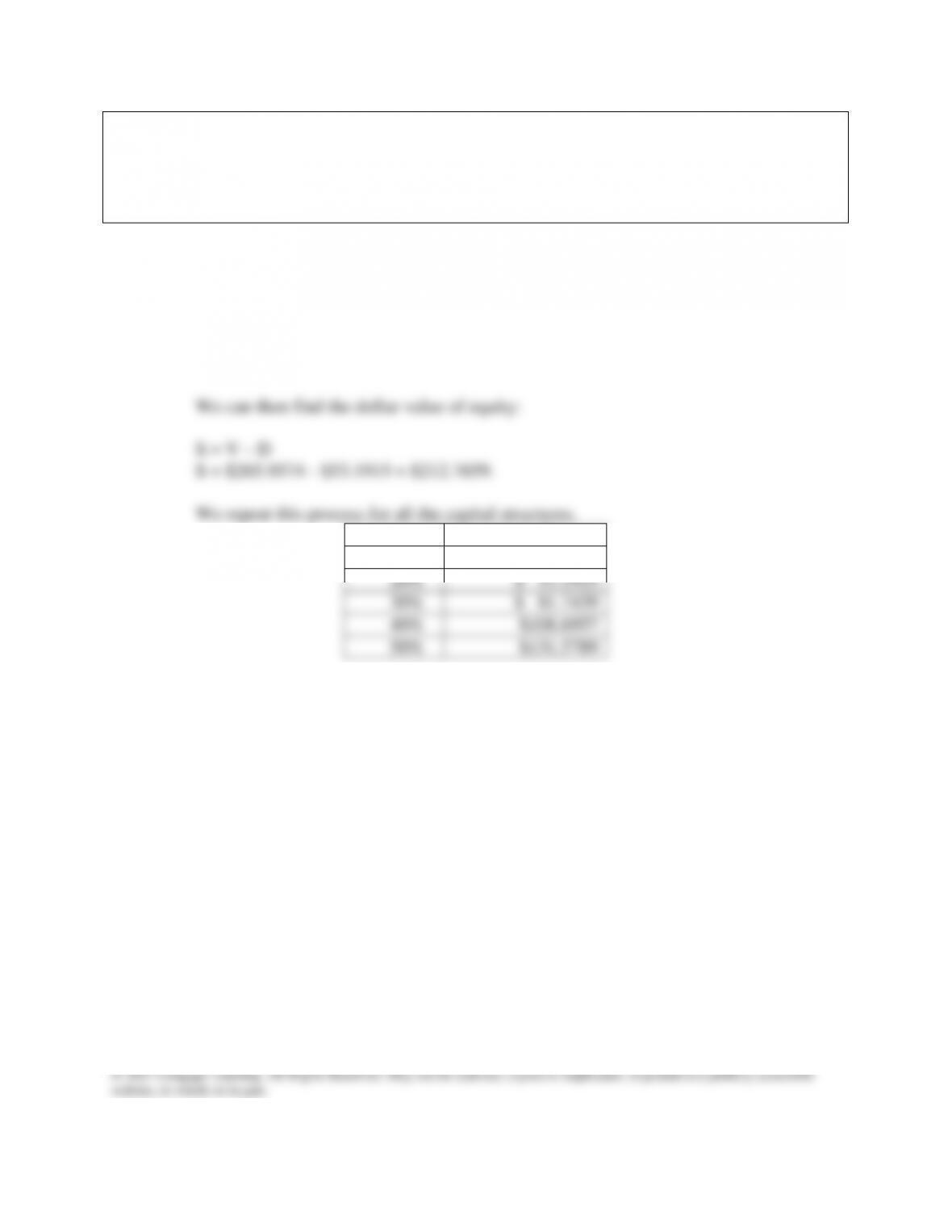

First, find the dollar value of debt. For example, for wd = 20%, the dollar value of

debt is:

d = wd V = 0.2 ($2,659,574) = $53.19.

wd

Debt, D

0%

$ 0

20%

$ 53.1915

30%

$ 81.7439

40%

$108.6957

50%

$131.5789

Note: these are rounded; see Ch15 Mini Case.xls for full calculations.

The situation before the recap is:

Before

Debt

Vop

$250

+ ST Inv.

0

VTotal

$250

− Debt

0

S

$250

n

10

P

$25.00

S

$250

Cash distr.

0

Wealth

$250

The stock price is $25 and the total wealth of shareholders is $2,500,000.

+ ST Inv.

10

10

website, in whole or in part.

The repurchase itself will not change the stock price. If investors thought that the

repurchase would increase the stock price, they would all purchase stock the day

before, which would drive up its price. If investors thought that the repurchase would

decrease the stock price, they would all sell short the stock the day before, which

would drive down the stock price.

n = 10 – 2

= 8.

Before

Debt

After

Debt,

Before

Rep.

After Rep.

Vop

$250

$265.9574

$265.9574

+ ST Inv.

0

53.1915

0

VTotal

$250

$319.1489

$265.9574

− Debt

0

53.1915

53.1915

S

$250

$265.9574

$212.7660

n

10

10

8

P

$25.00

$26.60

$26.60

S

$250

$265.9574

$212.7660

Cash distr.

0

0

53.1915

Wealth

$250

$265.9574

$265.9574

Notice that the value of the equity declines as more debt is issued, because debt is

used to repurchase stock. But the total wealth of shareholders is the value of stock

after the recap plus the cash received in repurchase, and this total is not changed by

the repurchase.

There are some shortcuts we can take to find the values of S, P, and n after the

repurchase:

S = (1 – wd) Vop

nPost = nPrior

OldopNew

NewopNew

DV

DV

PPost =

iorPr

OldopNew

n

DV

Mini Case: 15 – 23

© 2017 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible

website, in whole or in part.

required payment on the debt, and the firm will be bankrupt. The debtholders will

take over the firm and the equity holders will receive nothing. If L’s value is greater

than $2 million in one year, then management will repay the debt and the

stockholders will keep the company.

This option can be valued with the Black-Scholes Option Pricing Model:

V = PN(D1) – Xe–RTN(D2)

And n() is the cumulative normal distribution function, from either appendix a in the

R = 0.06

and calculating,

D1 = 1.552

D2 = 0.9552

The yield on this debt is calculated as

Price = (Face Value)/(1+Yield)N

so that

Yield = [Face Value/Price]1/N – 1.0

Mini Case: 15 – 24

k. What is the value of L’s stock for volatilities between 0.20 and 0.95? What

incentives might the manager of L have if she understands this relationship?

What might debtholders do in response?

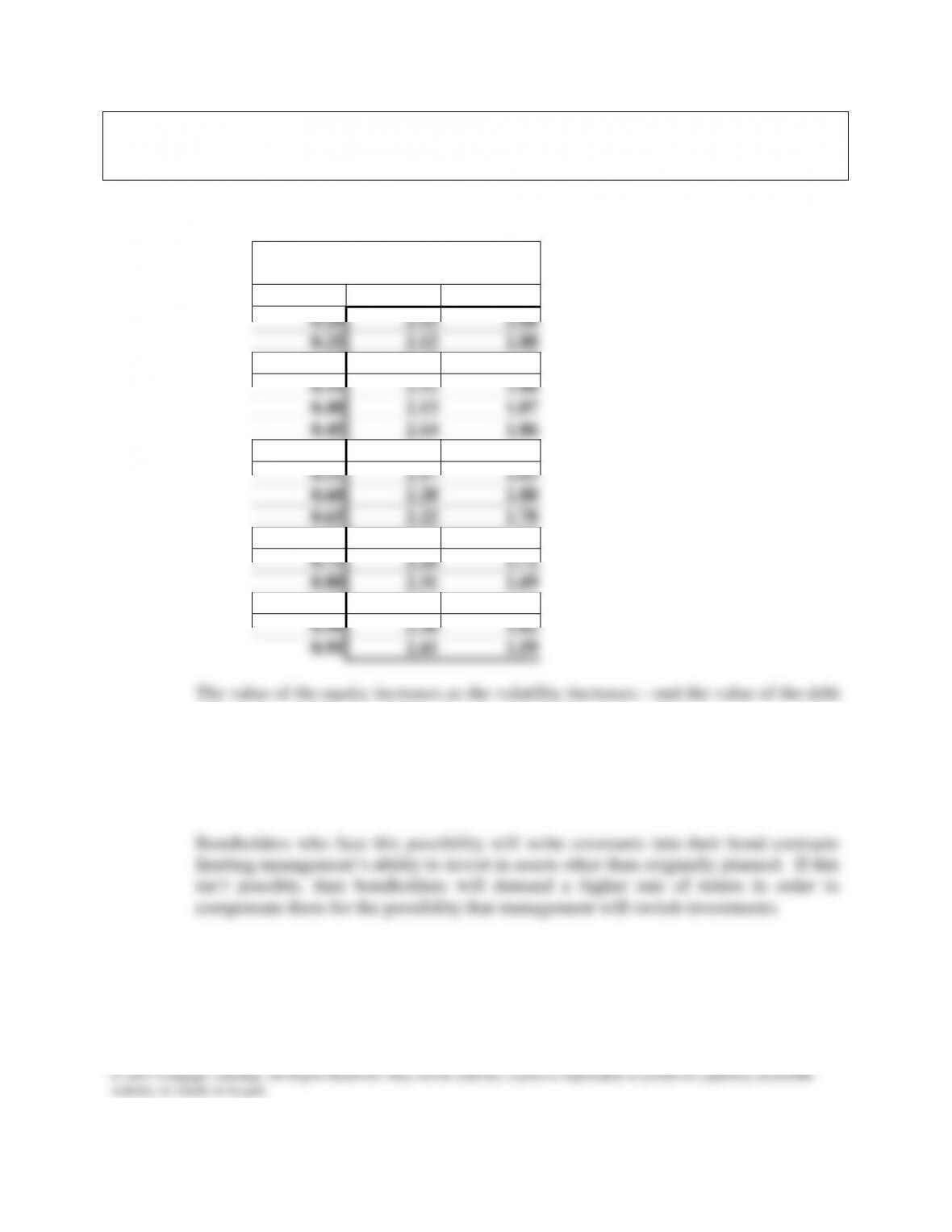

Answer: The mini case model shows the calculations for the table below.

Value of Stock and Debt

for Different Volatilities

Volatility

Equity

Debt

0.20

2.12

1.88

0.25

2.12

1.88

0.30

2.12

1.88

0.35

2.12

1.88

0.40

2.13

1.87

0.45

2.14

1.86

0.50

2.16

1.84

0.55

2.17

1.83

0.60

2.20

1.80

0.65

2.22

1.78

0.70

2.25

1.75

0.75

2.28

1.72

0.80

2.31

1.69

0.85

2.34

1.66

0.90

2.38

1.62

0.95

2.41

1.59

decreases as well. A manager who knows this may choose to invest the proceeds

from borrowing in assets that are riskier than usual. This is called “bait and switch.”

This action decreases the value of the debt, because now its claim is riskier. It

increases the value of equity because the worse the stockholders can do is default on

the bonds, but the best they can do is potentially unlimited.

Mini Case: 15 – 25

l. How do companies manage the maturity structure of their debt?

Answer: Factors that influence the decision to issue long-term bonds rather than short-term

debt:

Maturity matching:

Finance long-term assets with long-term debt

Finance short-term assets with short-term debt.

Information asymmetries: