1

2

3

4

5

6

7

8

9

10

11

12

19

20

21

22

23

and the market risk premium is 6 percent.

structure can affect the weighted average cost of capital and free cash flows. Answer: See Chapter 15 Mini

Case Show

30

31

32

33

34

Mini Case Show

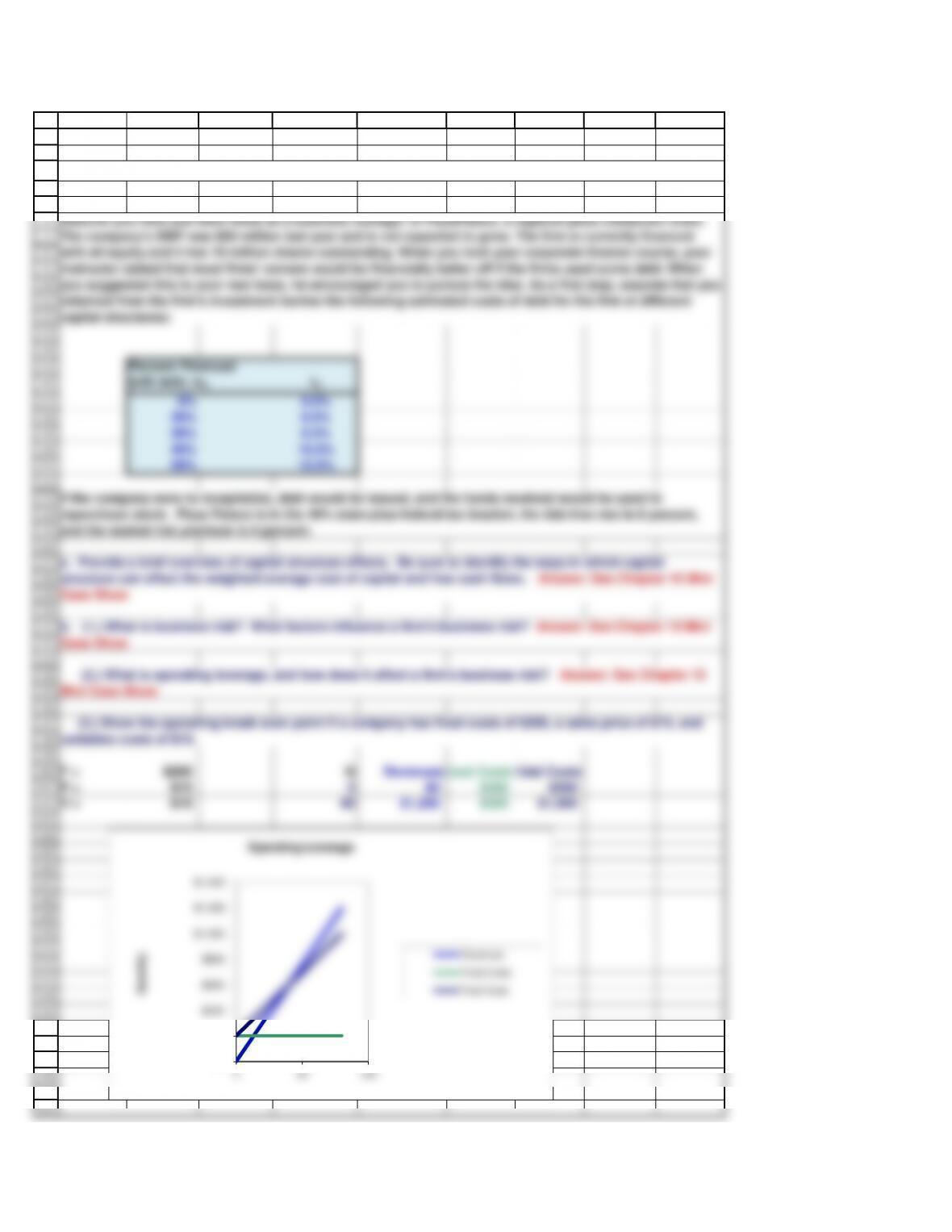

(3.) Show the operating break even point if a company has fixed costs of $200, a sales price of $15, and

41

42

43

44

45

A B C D E F G H I

10/28/2015

Situation

30% 8.5%

40% 10.0%

50% 12.0%

P = $15 0$0 $200 $200

V = $10 80 $1,200 $200 $1,000

Chapter 15. Mini Case

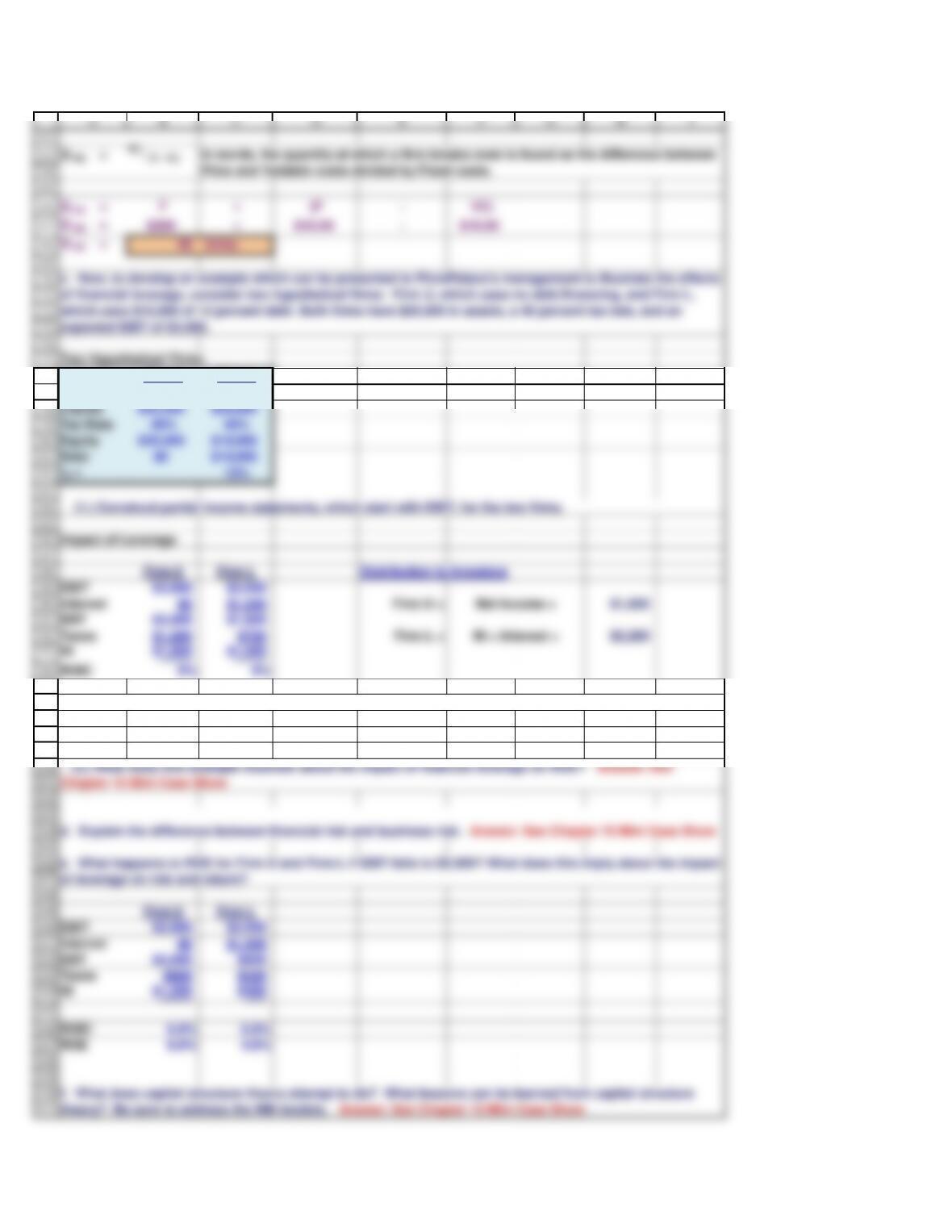

If the company were to recapitalize, debt would be issued, and the funds received would be used to

b. (1.) What is business risk? What factors influence a firm’s business risk? Answer: See Chapter 15 Mini

Case Show

(2.) What is operating leverage, and how does it affect a firm’s business risk? Answer: See Chapter 15

Assume you have just been hired as a business manager of PizzaPalace, a regional pizza restaurant chain.

The company’s EBIT was $50 million last year and is not expected to grow. The firm is currently financed

with all equity and it has 10 million shares outstanding. When you took your corporate finance course, your

instructor stated that most firms’ owners would be financially better off if the firms used some debt. When

you suggested this to your new boss, he encouraged you to pursue the idea. As a first step, assume that you

obtained from the firm’s investment banker the following estimated costs of debt for the firm at different

capital structures:

Operating Leverage

62

63

64

65

66

67

Q BE = 40 Units.

A B C D E F G H I

Q BE = FC / (P – VC)

Q BE = F÷(P – VC)

Q BE = $200 ÷$15.00 – $10.00

In words, the quantity at which a firm breaks even is found as the difference between

Price and Variable costs divided by Fixed costs.

122

123

124

125

126

127

128

129

133

134

135

136

137

138

142

143

144

145

146

Vop = [FCF(1+g)]/(WACC-g)

Vop = $250

155

156

157

158

159

A B C D E F G H I

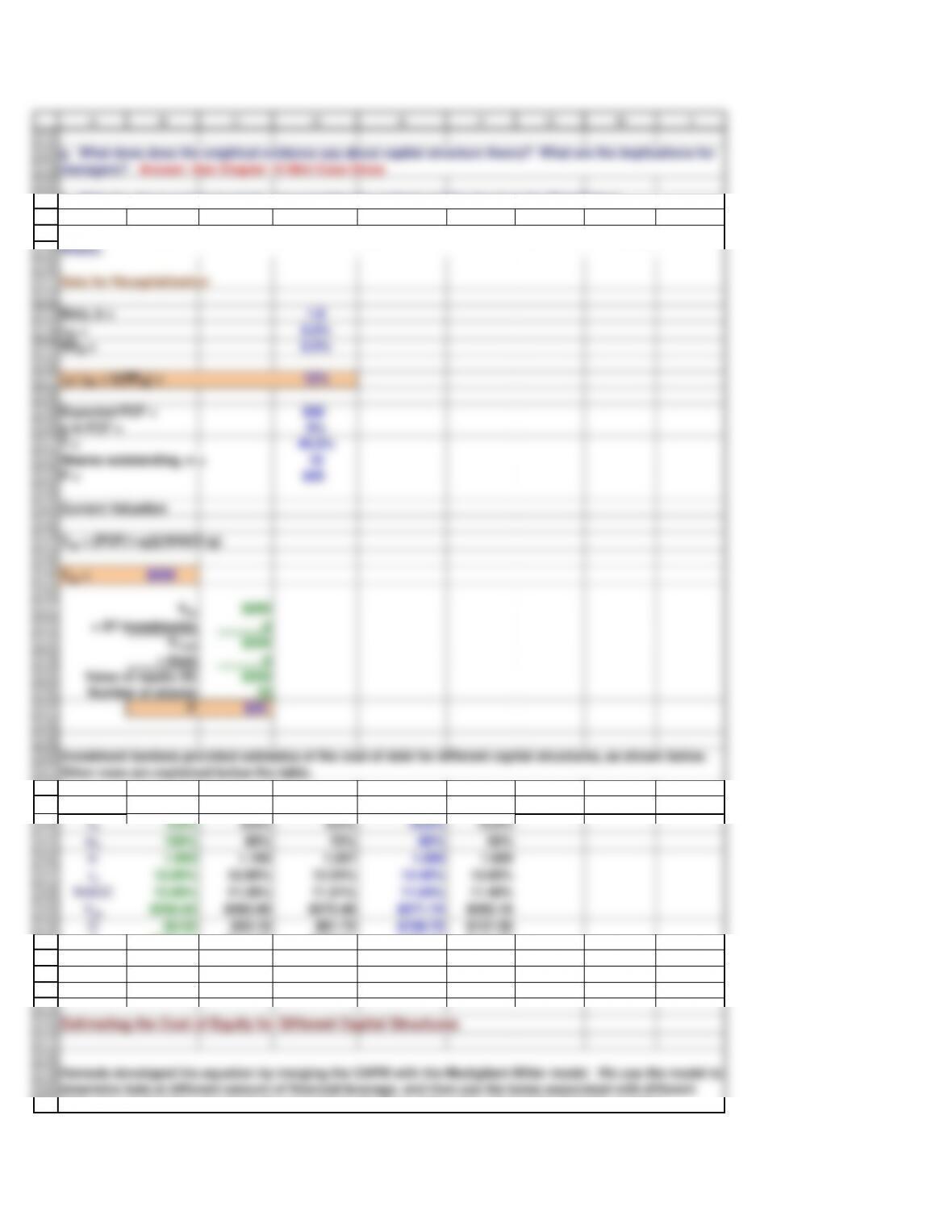

Beta, b = 1.0

rRF = 6.0%

RPM = 6.0%

rs= rRF + b(RPM) = 12%

Shares outstanding, n = 10

P = $25

Current Valuation

Value of equity (S)

$250

Number of shares

10

P $25

(1.) For each capital structure under consideration, calculate the levered beta, the cost of equity, and the

WACC.

h. With the above points in mind, now consider the optimal capital structure for PizzaPalace.

g. What does does the empirical evidence say about capital structure theory? What are the implications for

managers? Answer: See Chapter 15 Mini Case Show

182

183

184

185

186

187

188

189

190

197

198

199

200

201

Vop = [FCF(1+g)]/(WACC-g)

208

209

210

211

212

Equity = S = ws Vop = $212.77

219

220

221

230

231

232

233

234

A B C D E F G H I

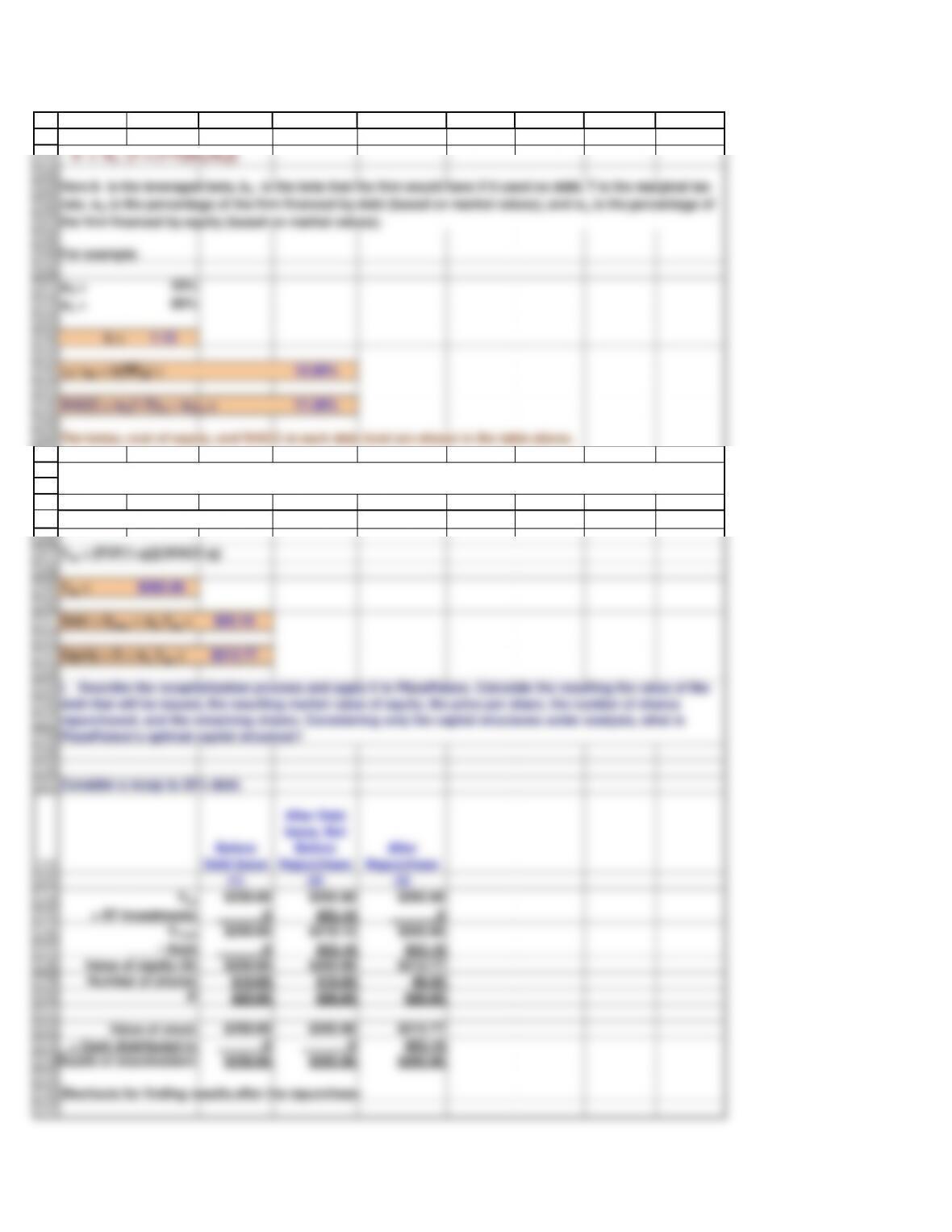

rs= rRF + b(RPM) = 12.90%

b = bU [1 + (1-T)(wd/ws)]

For example:

WACC = wd(1-T)rd + wsrs = 11.28%

The betas, cost of equity, and WACC at each debt level are shown in the table above.

Vop = $265.96

Debt = DNew = wd Vop = $53.19

Consider a recap to 20% debt.

After Debt

P $25.00 $26.60 $26.60

Value of stock

$250.00 $265.96 $212.77

0 0 $53.19

Wealth of shareholders

$250.00 $265.96 $265.96

+ Cash distributed in

Here b is the leveraged beta, bU is the beta that the firm would have if it used no debt, T is the marginal tax

rate, wd is the percentage of the firm financed by debt (based on market values), and ws is the percentage of

the firm financed by equity (based on market values).

238

239

240

241

242

243

244

245

246

247

248

249

250

251

252

253

254

255

256

257

258

259

260

261

262

265

266

267

268

269

275

276

A B C D E F G H I

S =(1- wd) (VopNew)

For wd = 20%: S = $212.77

nPost = nPrior ´ [(VopNew – DNew)/(VopNew-DOld)

For wd = 20%: nPost = 8.00

PPost = (VopNew − DOld)/nPrior

For wd = 20%: PPost = $26.60

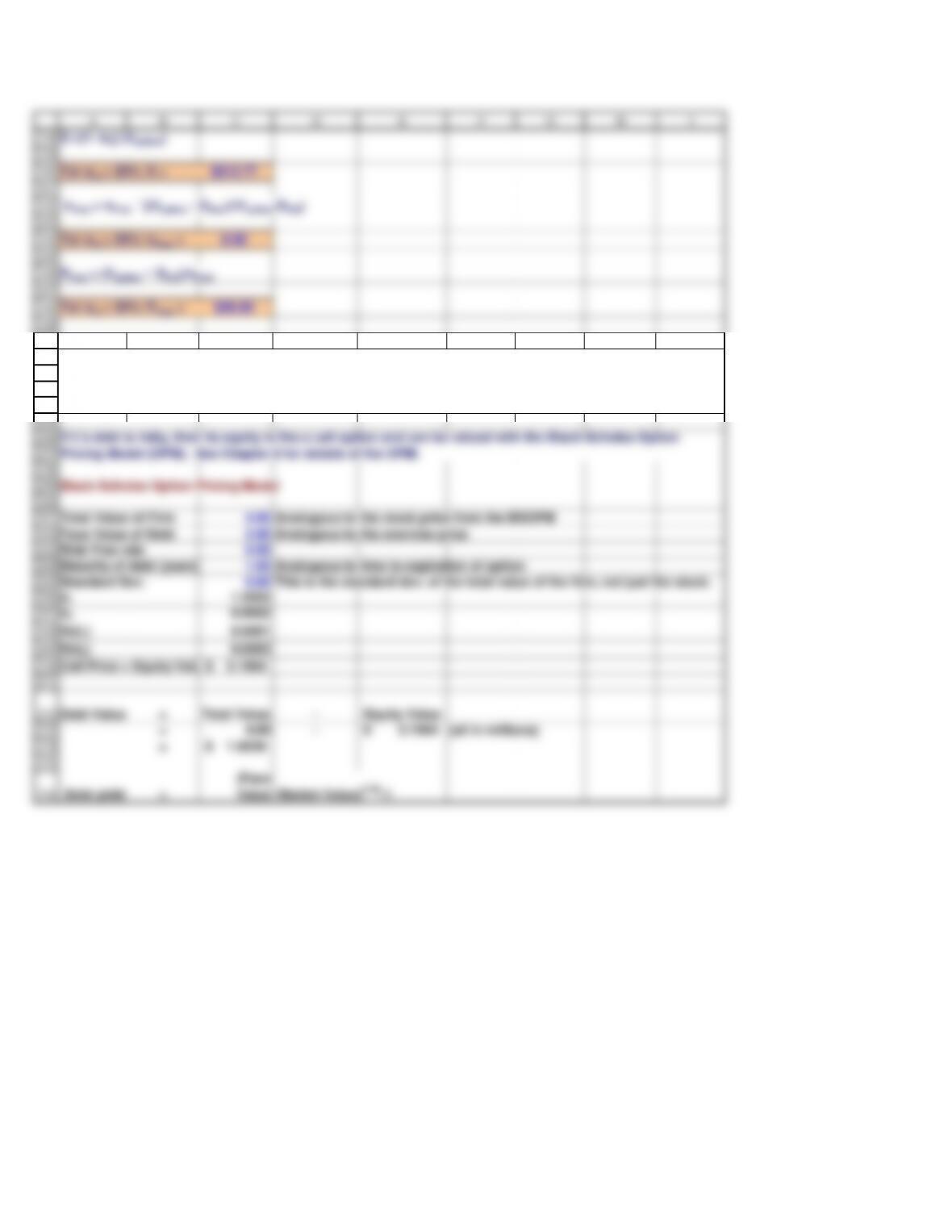

Black-Scholes Option Pricing Model

Total Value of Firm 4.00 Analogous to the stock price from the BSOPM

Face Value of Debt 2.00 Analogous to the exercise price

Standard Dev. 0.60 This is the standard dev. of the total value of the firm, not just the stock.

d11.5552

d20.9552

N(d1) 0.9401

N(d2) 0.8303

Debt yield

=

(Face

Value

/Market Value)(1/N)-1

j. Suppose there is a large probability that L will default on its debt. For the purpose of this example, assume

that the value of L’s operations is $4 million (the value of its debt plus equity). Assume also that its debt

consists of 1-year, zero coupon bonds with a face value of $2 million. Finally, assume that L’s volatility, σ is

0.60 and that the risk-free rate rRF is 6%.

If L’s debt is risky, then its equity is like a call option and can be valued with the Black-Scholes Option

Pricing Model (OPM). See Chapter 8 for details of the OPM.

277

278

279

280

281

282

283

284

285

286

287

288

289

290

291

292

293

294

295

300

301

302

303

304

311

312

313

322

323

324

325

A B C D E F G H I

Debt yield

= 10.888%

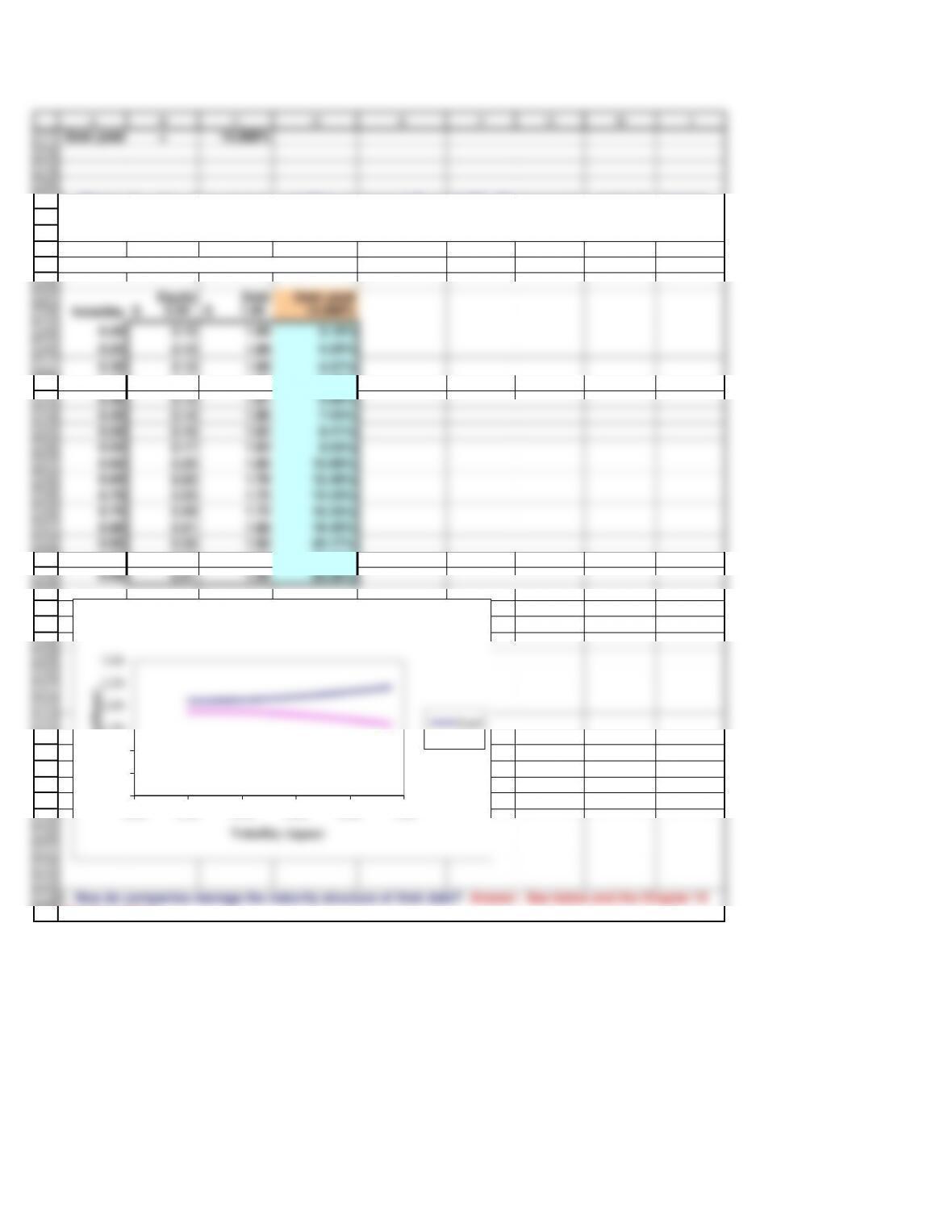

Value of Stock and Debt for Different Volatilities

Equity Debt Debt yield

Volatility $ 2.20 $ 1.80 10.888%

0.20

2.12 1.88 6.18%

0.25

2.12 1.88 6.20%

0.30

2.12 1.88 6.27%

0.35

2.12 1.88 6.48%

0.40

2.13 1.87 6.89%

0.45 2.14 1.86 7.53%

0.50 2.16 1.84 8.41%

0.75 2.28 1.72 16.23%

0.80 2.31 1.69 18.40%

0.85 2.34 1.66 20.77%

0.90 2.38 1.62 23.33%

0.95 2.41 1.59 26.08%

l. How do companies manage the maturity structure of their debt? Answer: See below and the Chapter 15

Mini Case Show.

k. What is the value of L‘s stock for volatilities between 0.20 and 0.95? What incentives might the manager

of L have if she understands this relationship? What might debtholders do in response? Answer: See

below and the Chapter 15 Mini Case Show.

2.00

2.50

1

2

3

4

5

6

7

8

9

10

17

18

19

20

21

28

29

30

31

32

39

40

41

42

43

50

51

52

53

54

61

J K

62

63

64

65

66

67

68

70

71

72

73

74

75

82

83

84

85

86

93

94

95

96

97

104

105

106

107

108

114

115

116

117

118

119

J K

122

123

124

125

126

127

128

129

130

135

136

137

138

139

140

141

147

148

149

150

151

158

159

160

161

162

163

169

170

171

172

173

180

181

J K

182

183

184

185

186

187

188

190

191

192

193

194

201

202

203

204

205

212

213

214

215

216

222

223

234

235

236

237

J K