Mini Case: 14 – 18

d. (2) What is a stock repurchase? Describe the procedures a company follows when it

make a distribution through a stock repurchase.

Answer: A firm may distribute cash to stockholders by repurchasing its own stock rather than

A company announces intent to purchase a dollar amount of its own stock during a

specific period. The announcement is not binding; in fact, companies often don’t

e. Discuss the advantages and disadvantages of a firm’s repurchasing its own

shares.

Advantages of repurchases:

1. A repurchase announcement may be viewed as a positive signal that management

believes the shares are undervalued.

2. Stockholders have a choice—if they want cash, they can tender their shares,

receive the cash, and pay the taxes, or they can keep their shares and avoid taxes.

4. Repurchased stock, called treasury stock, can be used later in mergers, when

employees exercise stock options, when convertible bonds are converted, and

Disadvantages of repurchases:

building,” where they invest funds in low-return projects.

firms generally announce repurchase programs in advance.

4. The firm may bid the stock price up and end up paying too high a price for the

f. 1. Suppose IWT has decided to distribute $50 million, which it presently is holding

in very liquid short-term investments. IWT’s value of operations is estimated to

be about $1,937.5 million. IWT has $387.5 million in debt (it has no preferred

stock). As mentioned previously, IWT has 100 million shares of stock

outstanding. Assume that IWT has not yet made the distribution. What is IWT’s

intrinsic value of equity? What is its intrinsic per share stock price?.

Answer:

Value of operations

$1,937.50

+ Value of nonoperating assets

50.00

Total intrinsic value of firm

$1,987.50

− Debt

387.50

Intrinsic value of equity

$1,600.00

÷ Number of shares

100.00

Intrinsic price per share

$16.00

f. (2) Now suppose that IWT has just made the $50 million distribution in the form of

dividends. What is IWT’s intrinsic value of equity? What is its intrinsic per

share stock price?

Answer:

Before

After Dividend

Value of operations

$1,937.50

$1,937.50

+ Value of nonoperating assets

50.00

0.00

Total intrinsic value of firm

$1,987.50

$1,937.50

− Debt

387.50

387.50

Intrinsic value of equity

$1,600.00

$1,550.00

÷ Number of shares

100.00

100.00

Intrinsic price per share

$16.00

$15.50

Dividend per share

$0.50

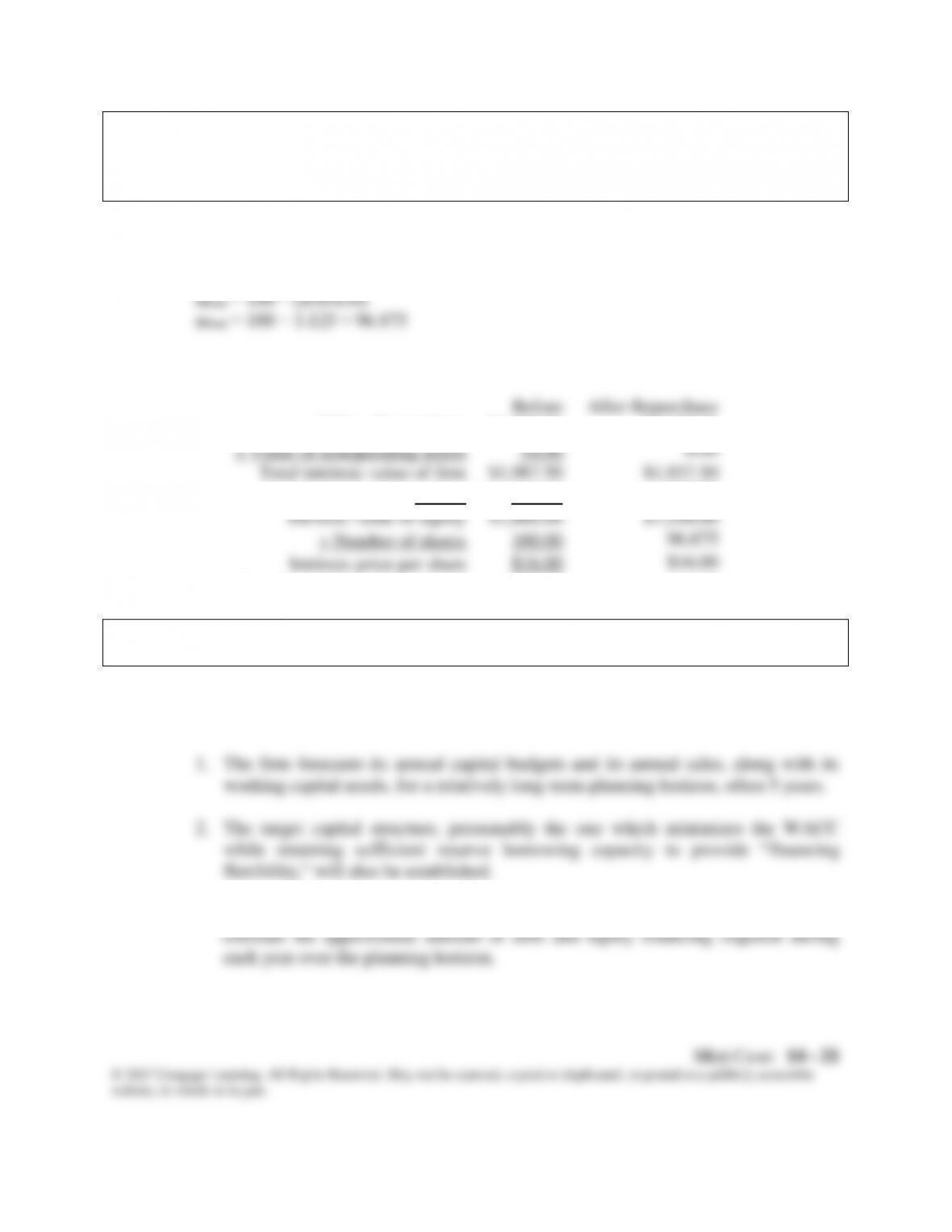

f. (3) Suppose instead that IWT has just made the $50 million distribution in the form

of a stock repurchase. Now what is IWT’s intrinsic value of equity? How many

shares did IWT repurchase? How many shares remained outstanding after the

repurchase? What is its intrinsic per share stock price after the repurchase?

Answer:

nPost = nPrior − (CashRep/PPrior)

website, in whole or in part.

4. A long-term target payout ratio is then determined, based on the residual model

concept. Because of flotation costs and potential negative signaling, the firm will

not want to issue common stock unless this is absolutely necessary. At the same

there is a great deal of uncertainty about cash flows and capital needs, then a

relatively low initial dollar dividend will be set, for this will minimize the

probability that the firm will have to either reduce the dividend or sell new

common stock. The firm will run its corporate planning model so that

management can see what is likely to happen with different initial dividends and

projected growth rates under different economic scenarios.

h. What are stock dividends and stock splits? What are the advantages and

disadvantages of stock dividends and stock splits?

Answer: When it uses a stock dividend, a firm issues new shares in lieu of paying a cash

doubled. A 100% stock dividend and a 2-for-1 stock split would produce the same

unchanged. For example, a 2-for-1 split of a stock selling for $50 would result in the

stock price being cut in half, to $25.

It is hard to come up with a convincing rationale for small stock dividends, like 5

percent or 10 percent. No economic value is being created or distributed, yet

stockholders have to bear the administrative costs of the distribution. Further, it is

Mini Case: 14 – 23

purchased in round lots, hence at reduced commissions, by most investors. A higher

within it.

Another factor that may influence stock splits and dividends is the belief that they

signal management’s belief that the future is bright. If a firm’s management would be

inclined to split the stock or pay a stock dividend only if it anticipated improvements

in earnings and dividends, then a split/dividend action could provide a positive signal

years has been absolutely spectacular. It may be that Berkshire’s market value would

be higher if it had a 425:1 stock split, or it may be that the conventional wisdom is

wrong.

i. What is a dividend reinvestment plan (drip), and how does it work?

to invest excess funds, and (3) the company generally pays all administrative costs

associated with the operation.

In a new stock plan, the firm issues new stock to the DRIP members in lieu of

cash dividends. No fees are charged, and many companies even offer the stock at a 5

percent discount from the market price on the dividend date on the grounds that the

firm avoids flotation costs that would otherwise be incurred. Only firms that need

new equity capital use new stock plans, while firms with no need for new stock use

an open market purchase plan.