Situation

Net Income

$140.00

Target equity ratio 80%

Total capital budget

$112.50

Number of shares 100

Distribution = Net Income – [(Target equity ratio) * (Total capital budget)]

Net income

$140

Chapter 14. Mini Case

Your new boss at the consulting firm Flick and Associates, which has been retained to help IWT prepare

has asked you to make a presentation to Jackson and Smithfield in which you review the theory of divide

the following issues.

(3.) What do the three theories indicate regarding the actions management should take with respect to div

Answer: See Chapter 14 Mini Case Show

a. (1.) What is meant by the term “distribution policy”? How have dividend payouts versus stock repurchases changed over

time? Answer: See Chapter 14 Mini Case Show

Integrated Waveguide Technologies (IWT) is a 6-year old company founded by Hunt Jackson and David

metamaterial plasmonic technology to develop and manufacture miniature microwave frequency direct

receivers for use in mobile Internet and communications applications. The technology, although highly

inexpensive to implement and their patented manufacturing techniques require little capital in compari

fabrication ventures. Because of the low capital requirement, Jackson and Smithfield have been able to a

stock and thus own all of the shares. Because of the explosion in demand for its mobile Internet applic

access outside equity capital to fund its growth and Jackson and Smithfield have decided to take the c

now, Jackson and Smithfield have paid themselves reasonable salaries but routinely reinvested all afte

firm, so dividend policy has not been an issue. However, before talking with potential outside investors

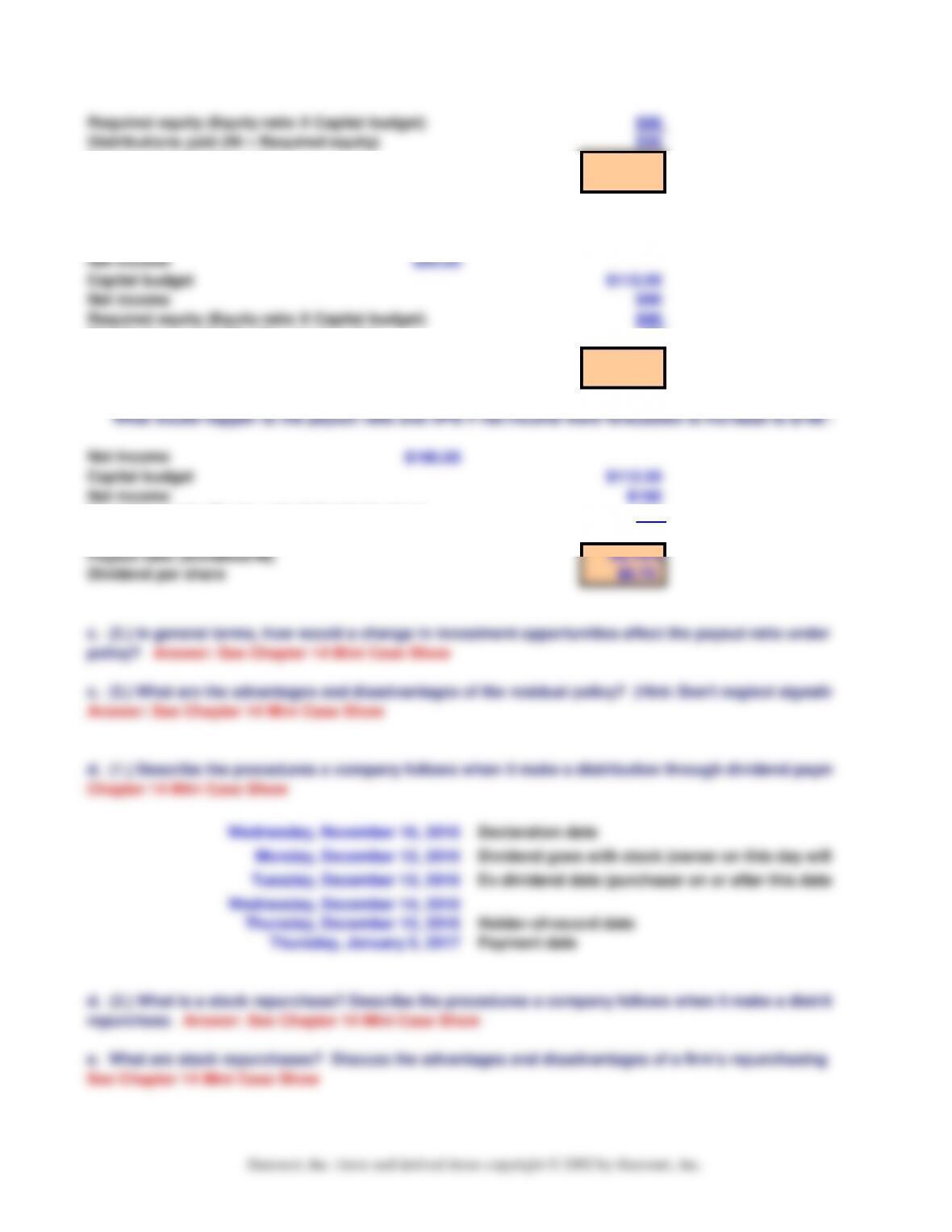

c. (1.) Assume that IWT has a $112.5 million capital budget planned for the coming year. You have dete

capital structure (80% equity and 20% debt) is optimal, and its net income is forecasted at $140 million. Us

distribution model approach to determine IWT’s total dollar distribution. Assume for now that the distribution is in the form of a

dividend. IWT has 100 million shares. What is the forecasted dividend payout ratio? What is the forecas

(2.) The terms “irrelevance,” “dividend prefernce, or bird-in-the-hand,” and “tax effect” have been use

major theories regarding the way dividend payouts affect a firm’s value. Explain what these terms mea

each theory. Answer: See Chapter 14 Mini Case Show

(4.) What results have empirical studies of the dividend theories produced? How does all this affect w

managers about dividend payouts? Answer: See Chapter 14 Mini Case Show

b. Discuss (1) the clientele effect, (2) the information content, or signaling, hypothesis, and (3) their eff

Answer: See Chapter 14 Mini Case Show

Required equity (Equity ratio X Capital budget)

$90

Distributions paid (NI – Required equity) $50

Payout ratio (Dividend/NI)

35.71%

Dividend per share $0.50

What would happen to the payout ratio and DPS if net income were forecasted to decrease to $90 m

Net Income

$90.00

Capital budget

$112.50

Net income

$90

Required equity (Equity ratio X Capital budget)

$90

Distributions paid (NI – Required equity) $0

Payout ratio (Dividend/NI)

0.00%

Dividend per share $0.00

What would happen to the payout ratio and DPS if net income were forecasted to increase to $160 m

Net Income

$160.00

Capital budget

$112.50

Net income

$160

Required equity (Equity ratio X Capital budget)

$90

Distributions paid (NI – Required equity) $70

43.75%

Dividend per share $0.70

Declaration date

Dividend goes with stock (owner on this day will

Ex-dividend date (purchaser on or after this date doe

Holder-of-record date

Payment date

c. (3.) What are the advantages and disadvantages of the residual policy? (Hint: Don’t neglect signaling a

Answer: See Chapter 14 Mini Case Show

Wednesday, November 16, 2016

Monday, December 12, 2016

Tuesday, December 13, 2016

Wednesday, December 14, 2016

Thursday, December 15, 2016

c. (2.) In general terms, how would a change in investment opportunities affect the payout ratio under t

policy? Answer: See Chapter 14 Mini Case Show

e. What are stock repurchases? Discuss the advantages and disadvantages of a firm’s repurchasing i

See Chapter 14 Mini Case Show

d. (1.) Describe the procedures a company follows when it make a distribution through dividend payme

Chapter 14 Mini Case Show

d. (2.) What is a stock repurchase? Describe the procedures a company follows when it make a distribut

Thursday, January 5, 2017

Harcourt, Inc. items and derived items copyright © 2002 by Harcourt, Inc.

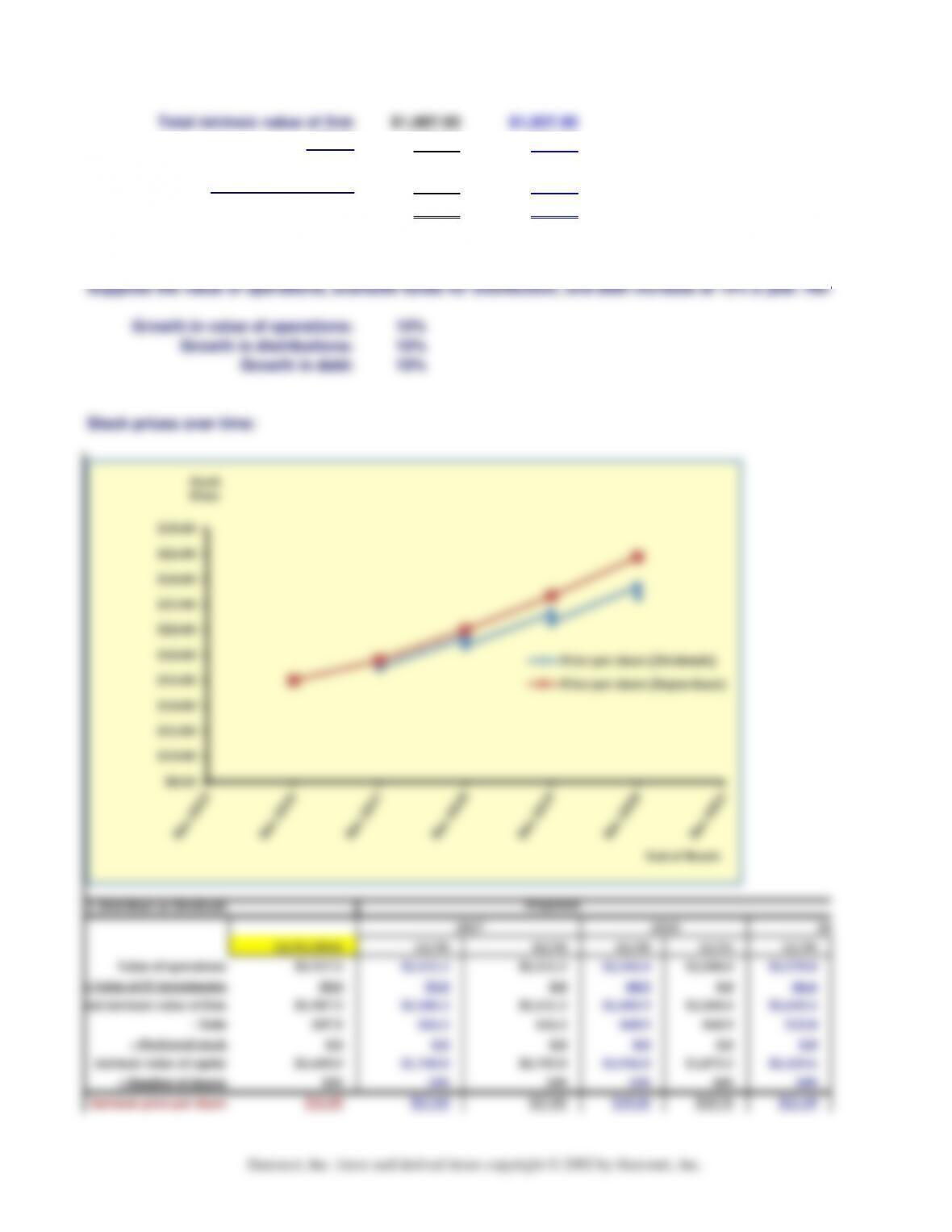

Inputs

Value of operations

$1,937.50

Short-term investments

$50.00

Debt

$387.50

Number of shares

100.00

Value of operations $1,937.50

+ Value of nonoperating assets 50.00

Total intrinsic value of firm $1,987.50

− Debt 387.50

Intrinsic value of equity $1,600.00

÷ Number of shares 100.00

Intrinsic price per share $16.00

+ Value of nonoperating assets 50.00 0.00

− Debt 387.50 387.50

÷ Number of shares 100.00 100.00

Prior to

IWT’s intrinsic value of equity? How many shares did IWT repurchase? How many shares remained outstanding after the

repurchase? What is its intrinsic per share stock price after the repurchase?

Prior to

f. Suppose IWT has decided to distribute $50 million, which it presently is holding in very liquid short-term investments. IWT’s

value of operations is estimated to be about $1,937.5 million. IWT has $387.5 million in debt (it has no pre

mentioned previously, IWT has 100 million shares of stock outstanding.

f. (1.) Assume that IWT has not yet made the distribution. What is IWT’s intrinsic value of equity? What is its intrinsic per share

stock price?

Prior to

f. (2.) Now suppose that IWT has just made the $50 million distribution in the form of dividends. What is IWT’s intrinsic value

Total intrinsic value of firm $1,987.50 $1,937.50

− Debt 387.50 387.50

Intrinsic value of equity $1,600.00 $1,550.00

÷ Number of shares 100.00 96.875

Intrinsic price per share $16.00 $16.00

Number of shares repurchased 3.125

Suppose the value of operations, available funds for distribution, and debt increase at 10% a year. Here

Growth in value of operations: 10%

Growth in distributions: 10%

Growth in debt: 10%

Dividend per share $0.55 $0.61

Section 2. Distribute as Repurchase

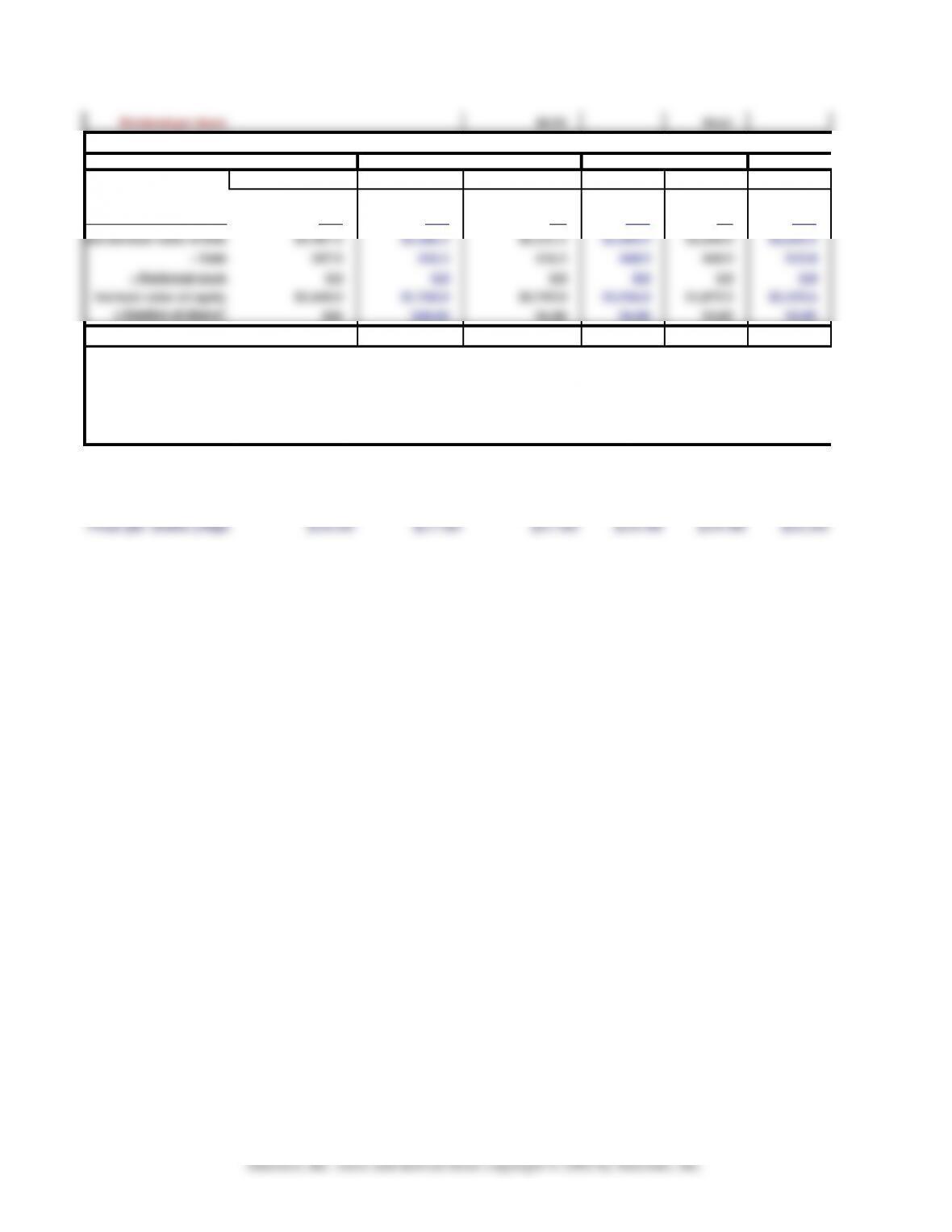

12/31/16 12/30 12/31 12/30 12/31 12/30

Value of operations $1,937.5 $2,131.3 $2,131.3 $2,344.4 $2,344.4 $2,578.8

+ Value of ST investments

50.0 55.0 0.0 60.5 0.0 66.6

− Debt 387.5 426.3 426.3 468.9 468.9 515.8

− Preferred stock 0.0 0.0 0.0 0.0 0.0 0.0

Intrinsic value of equity $1,600.0 $1,760.0 $1,705.0 $1,936.0 $1,875.5 $2,129.6

÷ Number of sharesa100 100.00 96.88 96.88 93.85 93.85

Intrinsic price per share $16.00 $17.60 $17.60 $19.98 $19.98 $22.69

Notes:

End of Month Dec-2016 Dec-2017 Dec-2017 Dec-2018 Dec-2018 Dec-2019

Price per share (Dividends)

$16.00 $17.60 $17.05 $19.36 $18.76 $21.30

Price per share (Repurch

$16.00 $17.60 $17.60 $19.98 $19.98 $22.69

aThe number of shares after the repurchase is: nPost = nPrior − (CashRep/PPrior). In this example, the entire amount of ST investments (i.e.,

the balance of nonoperating assets) is used to repurchase stock.

2017

2018

2019

i. What is a dividend reinvestment plan (DRIP), and how does it work? Answer: See Chapter 14 Mini Ca

g. Describe the series of steps that most firms take in setting dividend policy in practice. Answer: See

Show

h. What are stock dividends and stock splits? What are the advantages and disadvantages of stock di

splits? Answer: See Chapter 14 Mini Case Show