Mini Case: 12 – 21

e. 1. For each of the next four years, forecast the following items: sales, cash, accounts

receivable, inventories, net fixed assets, accounts payable & accruals, operating

costs (excluding depreciation), depreciation, and earnings before interest and taxes

(EBIT).

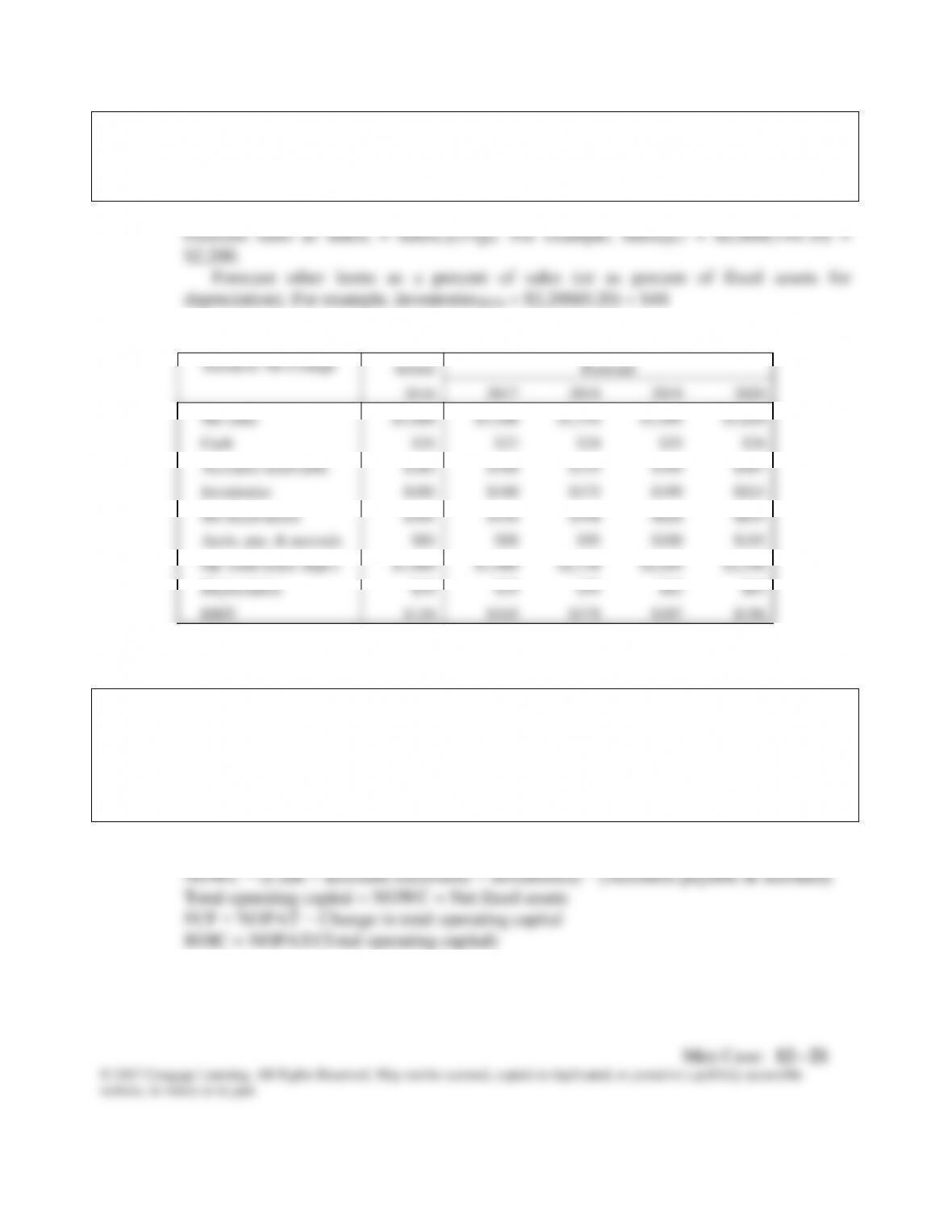

Scenario: No Change

Actual

Forecast

2016

2017

2018

2019

2020

Net sales

$2,000

$2,200

$2,376

$2,495

$2,620

Cash

$20

$22

$24

$25

$26

Accounts receivable

$280

$308

$333

$349

$367

Inventories

$400

$440

$475

$499

$524

Net fixed assets

$500

$550

$594

$624

$655

Accts. pay. & accruals

$80

$88

$95

$100

$105

Op. costs (excl. depr.)

$1,800

$1,980

$2,138

$2,245

$2,358

Depreciation

$50

$55

$59

$62

$65

EBIT

$150

$165

$178

$187

$196

e. 2. Using the previously forecasted items, calculate for each of the next four years the

net operating profit after taxes (NOPAT), net operating working capital, total

operating capital, free cash flow, (FCF), annual growth rate in FCF, and return on

invested capital. What does the forecasted free cash flow in the first year imply

about the need for external financing? Compare the forecasted ROIC compare

with the WACC. What does this imply about how well the company is performing?

NOPAT = EBIT(1-T)

website, in whole or in part.

Scenario:

Actual

Forecast

No Change

2016

2017

2018

2019

2020

NOPAT

$90

$99

$107

$112

$118

NOWC

$620

$682

$737

$773

$812

Total op. capital

$1,120

$1,232

$1,331

$1,397

$1,467

FCF

−$13

$8

$46

$48

Growth in FCF

–164%

447.1%

5.0%

ROIC

8.0%

8.0%

8.0%

8.0%

8.0%

e. 3. Assume that FCF will continue to grow at the growth rate for the last year in the

forecast horizon (Hint: 5%). What is the horizon value at 2020? What is the present

value of the horizon value? What is the present value of the forecasted FCF? (Hint:

use the free cash flows for 2017 through 2020). What is the current value of

operations? Using information from the 2016 financial statements, what is the

current estimated intrinsic stock price?

Scenario:

No Change

Horizon Value:

Value of operations

$958

+ ST investments

$0

=

$1,261

Estimated total intrinsic value

$958

− All debt

$500

Value of Operations:

− Preferred stock

$0

Present value of HV

$893

Estimated intrinsic value of equity

$458

+ Present value of FCF

$64

÷ Number of shares

10

Value of operations =

$958

Estimated intrinsic stock price =

$45.75

HV9 = 9+gL

WACC − gL

Mini Case: 12 – 23

© 2017 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible

website, in whole or in part.

The estimated intrinsic stock value of $45.75 is less than the actual market price of

$52.80. The market price indicates that the market expected the operating performance

to improve; if operating performance doesn’t improve, the market price is likely to drop.

But keep in mind that stocks prices are very volatile, so a difference of −13% =

$45.75/$52.80 – 1 is not very big.

f. Continue with the same assumptions for the No Change scenario from the previous

question, but now forecast the balance sheet and income statements for 2017 (but

not for the following three years) using the following preliminary financial policy.

(1) Regular dividends will grow by 10%. (2) No additional long-term debt or

common stock will be issued. (3) The interest rate on all debt is 8%. (4) Interest

expense for long-term debt is based on the average balance during the year. (5) If

the operating results and the preliminary financing plan cause a financing deficit,

eliminate the deficit by drawing on a line of credit. The line of credit would be

tapped on the last day of the year, so it would create no additional interest expenses

for that year. (6) If there is a financing surplus, eliminate it by paying a special

dividend. After forecasting the 2017 financial statements, answer the following

questions.

f. 1. How much will Hatfield need to draw on the line of credit?

Mini Case: 12 – 24

Assets

2016

Input

Basis for 2017 Forecast

2017

Cash

$20

1%

× 2017 Sales

$22

Accts. rec.

$280

14%

× 2017 Sales

$308

Inventories

$400

20%

× 2017 Sales

$440

Total CA

$700

$770

Net fixed assets

$500

25%

× 2017 Sales

$550

Total assets

$1,200

$1,320

Liabilities and equity

Accts. pay. & accruals

$80

4%

× 2017 Sales

$88

Line of credit

$0

Add LOC if fin. deficit

Total CL

$80

$88

Long-term debt

$500

No Change

$500

Total liabilities

$580

$588

Common stock

$420

No Change

$420

Retained earnings

$200

Old RE + Add. to RE

$253

Total common equity

$620

$673

Total liabs. & equity

$1,200

$1,261

Check: TA − TL & Equ.

$59

percent of Net PP&E. Forecast interest expense on the long-term debt as the product of

the interest rate and the average balance on the long-term debt (i.e., the average of the

beginning value and the ending value). Pay a regular dividend. Leave the special

dividend blank for now.

2016

Input

Basis for 2017 Forecast

2017

Sales

$2,000

110%

× 2016 Sales

$2,20

0

Op. costs (excl. depr.)

$1,800

90%

× 2017 Sales

$1,98

0

Depreciation

$50

10%

× 2017 Net fixed assets

$55

EBIT

$150

$165

Less: Interest on LTD

$40

8%

× Avg bonds

$40

Interest on LOC

$0

8%

× Beginning LOC

$0

Pretax earnings

$110

$125

Taxes (40%)

$44

40%

× Pretax earnings

$50

Net income

$66

$75

Regular common dividends

$20

110%

× 2016 Dividend

$22

Special dividends

$0

Pay if financing surplus

Addition to RE

$46

Net income – Dividends

$53

The next step is to identify the financing surplus or deficit. Start with the additions to

operating assets, subtract the increase in spontaneous liabilities (accounts payable and

accruals), subtract any new external financing from long-term debt or common stock,

subtract the previous LOC (because the preliminary financial plan does not call for any

Increase in spontaneous liabilities (accounts payable and accruals)

$8

+ Increase in long-term debt and common stock

$0

− Previous LOC

$0

+ Net income minus regular common dividends

$53

Increase in financing

$61

− Increase in total assets

$120

Amount of deficit or surplus financing:

−$59

If deficit in financing (negative), draw on line of credit

$59

If surplus in financing (positive), pay special dividend

$0

would cause a lower addition to retained earnings, which would cause a bigger financial

deficit. This is called financing feedback. See Ch12 Tool Kit.xls and look at the

worksheet CFO Model for a simple way to resolve financing feedback and for an

extension of the 1-year forecasted financial statements to multiple years.

website, in whole or in part.

Assets

2016

Input

Basis for 2017 Forecast

2016

Cash

$20

1%

× 2017 Sales

$22

Accts. rec.

$280

14%

× 2017 Sales

$308

Inventories

$400

20%

× 2017 Sales

$440

Total CA

$700

$770

Net fixed assets

$500

25%

× 2017 Sales

$550

Total assets

$1,200

$1,320

Liabilities and equity

Accts. pay. & accruals

$80

4%

× 2017 Sales

$88

Line of credit

$0

Add LOC if fin. deficit

$59

Total CL

$80

$147

Long-term debt

$500

No Change

$500

Total liabilities

$580

$647

Common stock

$420

No Change

$420

Retained earnings

$200

Old RE + Add. to RE

$253

Total common equity

$620

$673

Total liabs. & equity

$1,200

$1,320

Check: TA − TL & Equ.

$0

f. 2. What are some alternative ways than those in the preliminary financial policy that

Hatfield might choose to eliminate the financing deficit?

Answer: Here are some alternative ways to eliminate the deficit:

Cut dividends.

g. Repeat the analysis performed the previous question but now assume that Hatfield

is able to improve the following inputs: (1) reduce operating costs (excluding

depreciation)/sales to 89.5% at a cost of $40 million; and (2) reduce

inventories/sales to 16% at a cost of $10 million. This is the Improve scenario.

Answer: The impact on the operating plan is shown below:

Scenario:

Actual

Forecast

Improve

2016

2017

2018

2019

2020

NOPAT

$90

$106

$114

$120

$126

NOWC

$620

$594

$642

$674

$707

Total op. capital

$1,120

$1,144

$1,236

$1,297

$1,362

FCF

$82

$23

$58

$61

Growth in FCF

–72%

157.3%

5.0%

ROIC

8.0%

9.2%

9.2%

9.2%

9.2%

Scenario:

Improve

Horizon Value:

Value of operations

$1,314

+ ST investments

$0

=

$1,598

Estimated total intrinsic value

$1,314

− All debt

$500

Value of Operations:

− Preferred stock

$0

Present value of HV

$1,132

Estimated intrinsic value of equity

$814

+ Present value of FCF

$182

÷ Number of shares

10

Value of operations =

$1,314

Estimated intrinsic stock price =

$81.37

HV = 9+gL

WACC − gL

website, in whole or in part.

The impact on the financial statements is shown below.

Scenario:

Improve

Assets

2016

Input

Basis for 2017 Forecast

2016

Cash

$20

1%

× 2017 Sales

$22

Accts. rec.

$280

14%

× 2017 Sales

$308

Inventories

$400

16%

× 2017 Sales

$352

Total CA

$700

$682

Net fixed assets

$500

25%

× 2017 Sales

$550

Total assets

$1,200

$1,232

Liabilities and equity

Accts. pay. & accruals

$80

4%

× 2017 Sales

$88

Line of credit

$0

Add LOC if fin. deficit

$0

Total CL

$80

$88

Long-term debt

$500

No Change

$500

Total liabilities

$580

$588

Common stock

$420

No Change

$420

Retained earnings

$200

Old RE + Add. to RE

$224

Total common equity

$620

$644

Total liabs. & equity

$1,200

$1,232

Check: TA − TL & Equ.

$0

Improve

2016

Input

Basis for 2017 Forecast

2016

Sales

$2,000

110%

× 2016 Sales

$2,200

Op. costs (excl. depr.)

$1,800

89.5%

× 2017 Sales

$1,969

Depreciation

$50

10%

× 2017 Net fixed assets

$55

EBIT

$150

$176

Less: Interest on LTD

$40

8%

× Avg bonds

$40

Interest on LOC

$0

8%

× Beginning LOC

$0

Pretax earnings

$110

$136

Taxes (40%)

$44

40%

× Pretax earnings

$54

Net income

$66

$82

Regular common dividends

$20

110%

× 2016 Dividend

$22

Special dividends

$0

Pay if financing surplus

$36

Addition to RE

$46

Net income – Dividends

$24

Increase in spontaneous liabilities (accounts payable and accruals)

$8

+ Increase in long-term debt and common stock

$8

+ Net income minus regular common dividends

$0

Increase in financing

$60

− Increase in total assets

$68

Amount of deficit or surplus financing:

$32

If deficit in financing (negative), draw on line of credit

$36

If surplus in financing (positive), pay special dividend

$0

g. 1. Should Hatfield implement the plans? How much value would they add to the

company?

g. 2. How much can Hatfield pay as a special dividend in the Improve Scenario? What

else might Hatfield do with the financing surplus?