Mini Case: 11 – 31

MINI CASE

Shrieves Casting Company is considering adding a new line to its product mix, and the

capital budgeting analysis is being conducted by Sidney Johnson, a recently graduated MBA.

The production line would be set up in unused space in Shrieves’ main plant. The

machinery’s invoice price would be approximately $200,000, another $10,000 in shipping

charges would be required, and it would cost an additional $30,000 to install the equipment.

The machinery has an economic life of 4 years, and Shrieves has obtained a special tax ruling

that places the equipment in the MACRS 3-year class. The machinery is expected to have a

salvage value of $25,000 after 4 years of use.

The new line would generate incremental sales of 1,250 units per year for 4 years at an

incremental cost of $100 per unit in the first year, excluding depreciation. Each unit can be

sold for $200 in the first year. The sales price and cost are both expected to increase by 3%

per year due to inflation. Further, to handle the new line, the firm’s net working capital

would have to increase by an amount equal to 12% of sales revenues. The firm’s tax rate is

40%, and its overall weighted average cost of capital, which is the risk-adjusted cost of

capital for an average project (r), is 10%.

a. Define “incremental cash flow.”

a. 1. Should you subtract interest expense or dividends when calculating project cash

flow?

a. 2. Suppose the firm had spent $100,000 last year to rehabilitate the production line

site. Should this cost be included in the analysis? Explain.

Mini Case: 11 – 32

a. 3. Now assume that the plant space could be leased out to another firm at $25,000

per year. Should this be included in the analysis? If so, how?

a. 4. Finally, assume that the new product line is expected to decrease sales of the

firm’s other lines by $50,000 per year. Should this be considered in the analysis?

If so, how?

b. Disregard the assumptions in part a. What is Shrieves’ depreciable basis? What

are the annual depreciation expenses?

Answer: The asset’s depreciable basis includes shipping and installation costs. Thus, the asset’s

3 0.1481 240 35

website, in whole or in part.

c. Calculate the annual sales revenues and costs (other than depreciation). Why is it

important to include inflation when estimating cash flows?

Sales $250,000 $257,500 $265,225 $273,188

Costs $125,000 $128,750 $132,613 $136,588

The cost of capital is a nominal cost; i.e., it includes a premium for inflation. In other

words, it is larger than the real cost of capital. Similarly, nominal cash flows (those that

are inflated) are larger than real cash flows. If you discount the low, real cash flows

d. Construct annual incremental operating cash flow statements.

Answer:

Year 1

Year 2

Year 3

Year 4

Sales

$250,000

$257,500

$265,225

$273,188

Costs

125,000

128,750

132,613

136,588

Depreciation

79,992

106,680

35,544

17,784

Op. EBIT

$45,008

$22,070

$97,069

$118,807

Taxes (40%)

18,003

8,828

38,827

47,523

EBIT(1 – T)

$27,005

$13,242

$58,241

$71,284

Depreciation

79,992

106,680

35,544

17,784

Net Operating CF

$106,997

$119,922

$93,785

$89,068

website, in whole or in part.

e. Estimate the required net working capital for each year, and the cash flow due to

investments in net working capital.

Answer: The project requires a level of net working capital in the amount equal to 12% of the

next year’s sales. Any increase in NWC is a negative cash flow, and any decrease is a

Year 0

Year 1

Year 2

Year 3

Year 4

Sales

$250,000

$257,500

$265,225

$273,188

NWC (12% of sales)

$30,000

$30,900

$31,827

$32,783

$0

CF due to NWC

($30,000)

($900)

($927)

($956)

$32,783

f. Calculate the after-tax salvage cash flow.

Answer: When the project is terminated at the end of Year 4, the equipment can be sold for

Mini Case: 11 – 35

g. Calculate the net cash flows for each year. Based on these cash flows and the

average project cost of capital, what are the project’s NPV, IRR, MIRR, PI,

payback, and discounted payback? Do these indicators suggest that the project

should be undertaken?

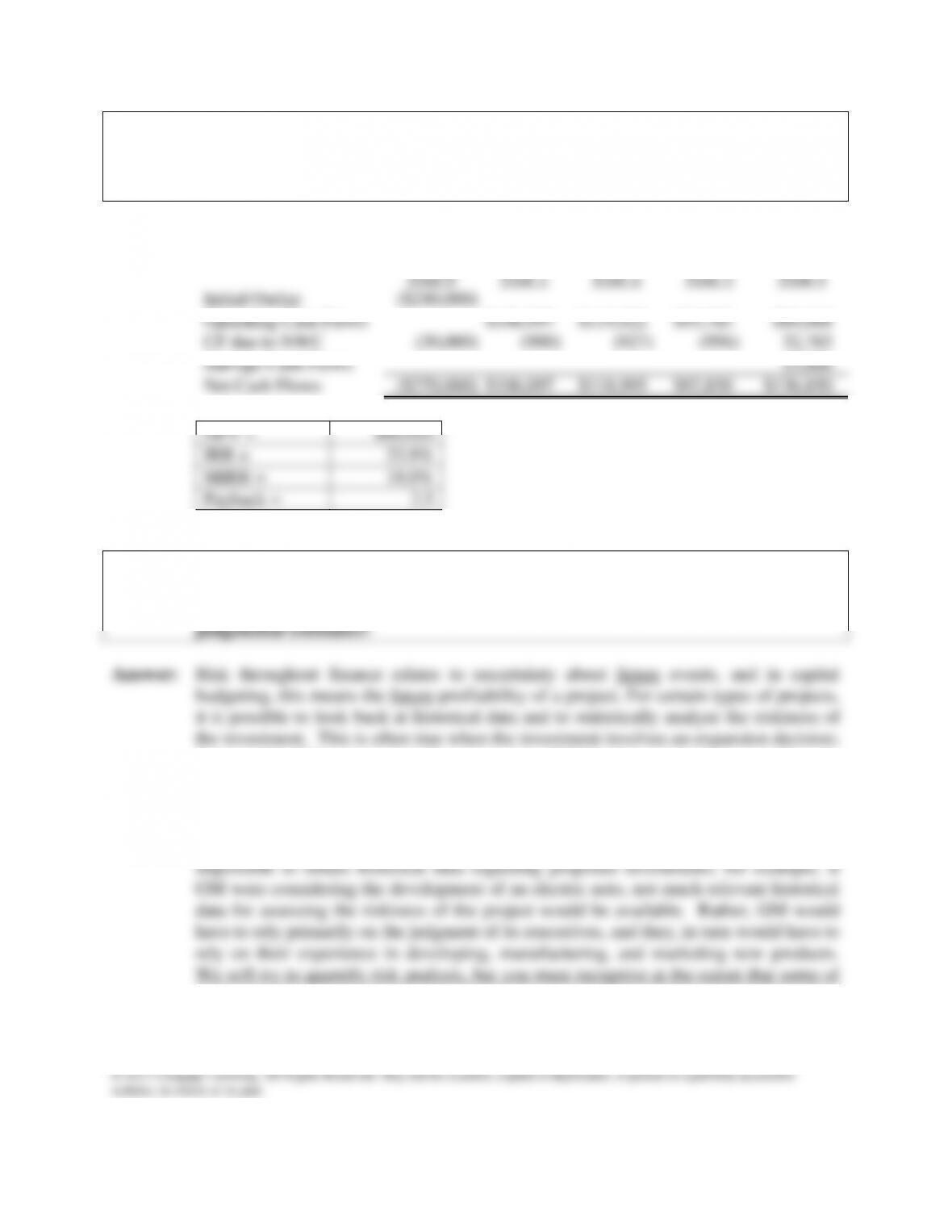

Answer: The net cash flows are:

Year 0

Year 1

Year 2

Year 3

Year 4

Initial Outlay

($240,000)

Operating Cash Flows

$106,997

$119,922

$93,785

$89,068

CF due to NWC

(30,000)

(900)

(927)

(956)

32,783

Salvage Cash Flows

15,000

Net Cash Flows

($270,000)

$106,097

$118,995

$92,830

$136,850

NPV =

$88,010

IRR =

23.9%

MIRR =

18.0%

Payback =

2.5

h. What does the term “risk” mean in the context of capital budgeting; to what

extent can risk be quantified; and when risk is quantified, is the quantification

based primarily on statistical analysis of historical data or on subjective,

for example, if Sears were opening a new store, if Citibank were opening a new branch,

or if GM were expanding its Chevrolet plant, then past experience could be a useful

guide to future risk. Similarly, a company that is considering going into a new business

might be able to look at historical data on existing firms in that industry to get an idea

about the riskiness of its proposed investment. However, there are times when it is

Mini Case: 11 – 36

the data used in the analysis will necessarily be based on subjective judgments rather

than on hard statistical observations.

i. 1. What are the three types of risk that are relevant in capital budgeting?

2. How is each of these risk types measured, and how do they relate to one another?

Answer: Here are the three types of project risk:

Stand-alone risk is the project’s total risk if it were operated independently. Stand–

alone risk ignores both the firm’s diversification among projects and investors’

other projects, that is, to diversification within the firm. It is the contribution of the

project to the firm’s total risk, and it is a function of (a) the project’s standard deviation

of NPV and (b) the correlation of the projects’ returns with those of the rest of the firm.

Within-firm risk is often called corporate risk, and it is measured by the project’s

corporate beta, which is the slope of the regression line formed by plotting returns on

i. 3. How is each type of risk used in the capital budgeting process?

Answer: Because management’s primary goal is shareholder wealth maximization, the most

relevant risk for capital projects is market risk. However, creditors, customers,

suppliers, and employees are all affected by a firm’s total risk. Since these parties

project’s stand-alone risk is likely to be highly correlated with its within-firm risk,