11-13 a. Old depreciation = $5,500 per year.

Book value = $55,000 – 5($5,500) = $27,500.

Gain = $35,000 – $27,500 = $7,500.

Tax on book gain = $7,500(0.35) = $2,625.

Price ($55,000)

b.

1

2

3

4

5

Old depreciation

5,500

5,500

5,500

5,500

5,500

Old tax shield

1,925

1,925

1,925

1,925

1,925

Basis

120,000

New depreciation

39,996

53,340

17,772

8,892

–

New tax shield

13,999

18,669

6,220

3,112

–

0

1

2

3

4

5

After tax savings

19,500

19,500

19,500

19,500

19,500

Depreciation tax shield new

13,999

18,669

6,220

3,112

–

Depreciation tax shield old

(1,925)

(1,925)

(1,925)

(1,925)

(1,925)

Opportunity cost of not selling old machine (after-tax)*

(13,000)

Total CF

(87,625)

31,574

36,244

23,795

20,687

4,575

c. NPV

(4,623)

The NPV is negative therefore, the firm should not replace the old machine.

*After-tax opportunity cost of not being able to sell old machine at end of its useful life.

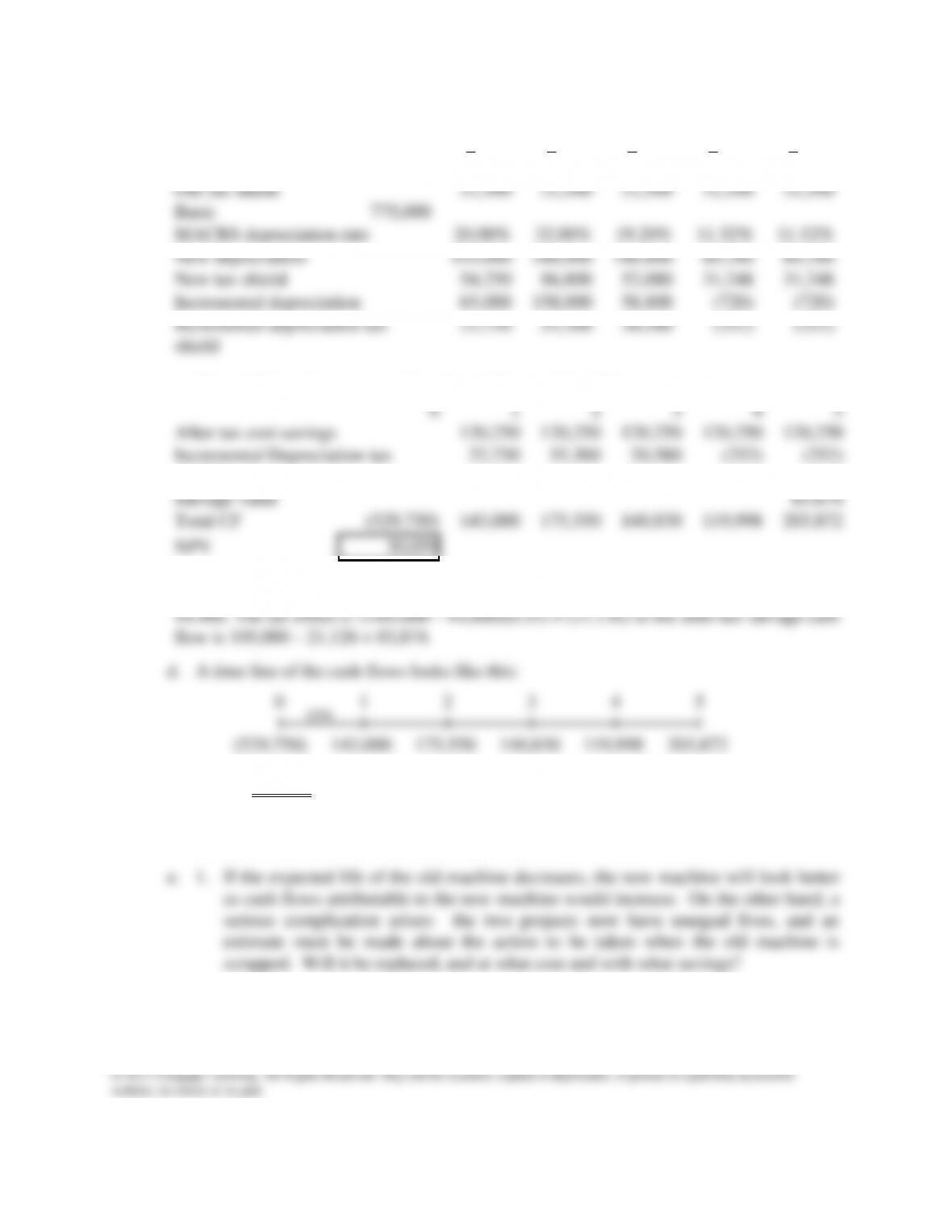

11-14 a. Cost of new machine ($775,000)

Salvage value, old 135,000

Savings due to loss on sale ($450,000 – $135,000) 0.35 110,250

Cash outlay for new machine ($ 529,750)

MACRS Rate

33.33%

44.45%

14.81%

7.41%

0.00%

Answers and Solutions: 11 – 22

b. Recovery Depreciable Depreciation Depreciation Change in

1

2

3

4

5

Old depreciation

90,000

90,000

90,000

90,000

90,000

Old tax shield

31,500

31,500

31,500

31,500

31,500

Basis

775,000

MACRS depreciation rate

20.00%

32.00%

19.20%

11.52%

11.52%

New depreciation

155,000

248,000

148,800

89,280

89,280

New tax shield

54,250

86,800

52,080

31,248

31,248

Incremental depreciation

65,000

158,000

58,800

(720)

(720)

Incremental depreciation tax

shield

22,750

55,300

20,580

(252)

(252)

c. CFt = (Operating expenses)(1 – T) + (Depreciation)(T).

0

1

2

3

4

5

After tax cost savings

120,250

120,250

120,250

120,250

120,250

Incremental Depreciation tax

shield

22,750

55,300

20,580

(252)

(252)

Salvage value

83,874

Total CF

(529,750)

143,000

175,550

140,830

119,998

203,872

NPV

30,059

*The salvage value of the new machine is calculated as: Book value = 7.41%(775,000) =

NPV = $30,059

Since the NPV is positive, the project should be accepted. To buy the new machine

would increase the value of the firm by $30,059.

2. The higher capital cost should be used in the analysis.

Answers and Solutions: 11 – 23

© 2017 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible

website, in whole or in part.

11-15 a. Expected annual cash flows:

Project A: Probable

Probability Cash Flow = Cash Flow

Project B: Probable

Probability Cash Flow = Cash Flow

Coefficient of variation:

CV =

CVB = $5,797.84/$7,650 = 0.7579.

NPV Expected

=

valueExpected

deviation Standard NPV

b. Project B is the riskier project because it has the greater variability in its probable

cash flows, whether measured by the standard deviation or the coefficient of

variation. Hence, Project B is evaluated at the 12 percent cost of capital, while

Project A requires only a 10 percent cost of capital.

Project A: With a financial calculator, input the appropriate cash flows into the cash

flow register, input I/YR = 10, and then solve for NPV = $10,036.25.

Project B: With a financial calculator, input the appropriate cash flows into the cash

11-16 a. First, note that with symmetric probability distributions, the middle value of each

distribution is the expected value. Therefore,

Expected Values

Sales (units) 200

Sales price $13,500

Answers and Solutions: 11 – 25

c. (1) a. Calculate developmental costs. The 44 random number value, coming

between 30 and 70, indicates that the costs for this run should be taken to be

$4 million.

b. Calculate the project life. The 17, being less than 20, indicates that a 3–year

(3) Repeat the process for Year 2. Sales will be 200 with a random number of 79;

the price will be $13,500 with a random number of 83; and the cost will be

$7,000 with a random number of 86:

[200($13,500) – 200($7,000)](0.6) = $780,000 = CF2.

(5) a. 0 = – $4,000,000

IRR = -31.55%.

321 )IRR1(

000,510$

)IRR1(

000,780$

)IRR1(

000,510$

website, in whole or in part.

4000000, CF1 = 510000, CF2 = 780000, CF3 = 510000, and solve for IRR =

-31.55%.

b. NPV = – $4,000,000.

have been about $1 million.

321 )15.1(

000,510$

)15.1(

000,780$

)15.1(

000,510$

(6) & (7) The computer would store NPVs and IRRs for the different trials, then

of occurrence

X

XX

XXXX

X

XX

XXXX

the input and output distributions are badly skewed. The frequency

values would also be used to calculate σNPV and IRR; these values would

be printed out and available for analysis.

website, in whole or in part.

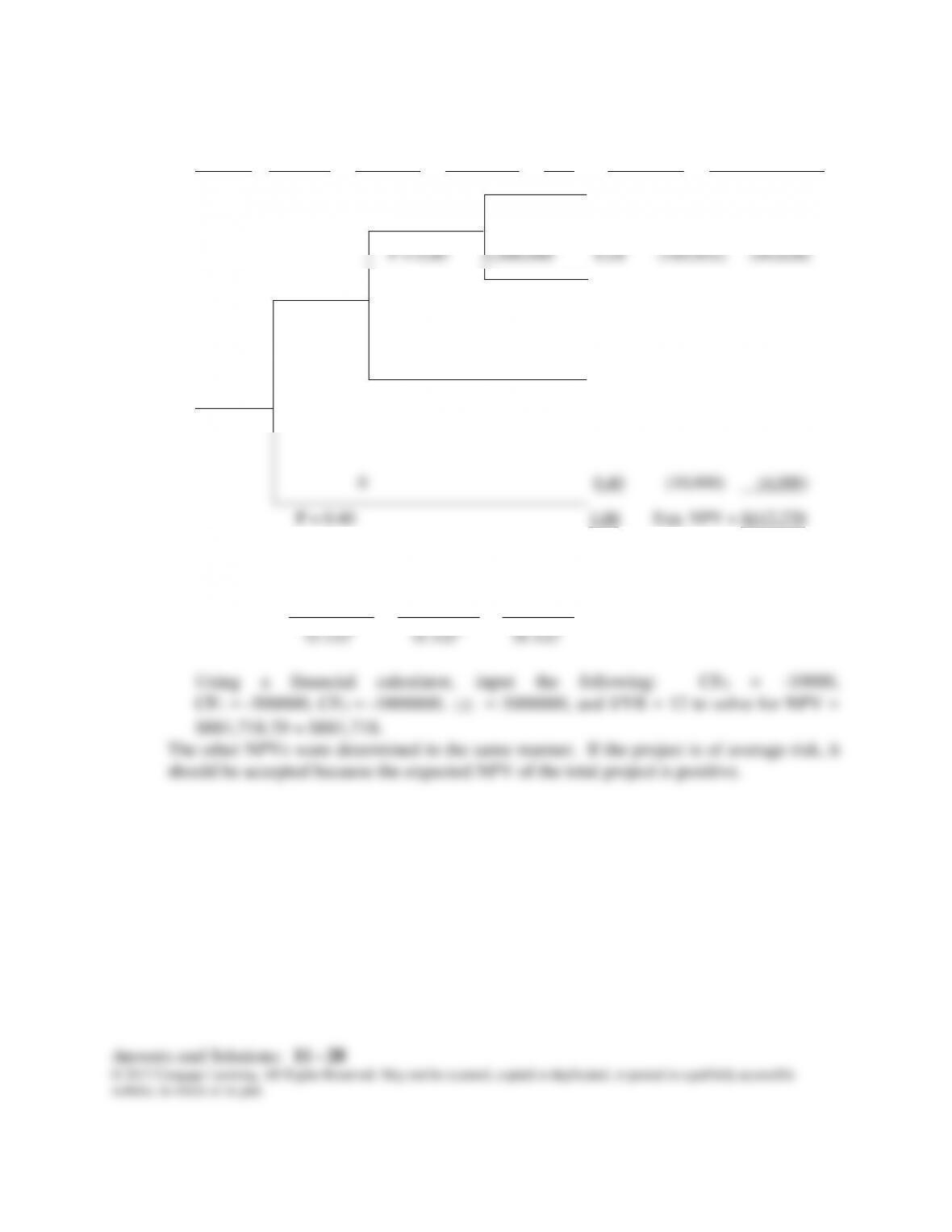

11-17 a. The resulting decision tree is:

NPV

t = 0 t = 1 t = 2 t = 3 P NPV Product

$3,000,000 0.24 $881,718 $211,612

($1,000,000) P = 0.5

($500,000) P = 0.5

P = 0.60

100,000 0.12 (376,709) (45,205)

($10,000) P = 0.20

The NPV of the top path is:

– – – $10,000 = $881,718.

3

)12.1(

000,000,3$

2

)12.1(

000,000,1$

1

)12.1(

000,500$

b. σ2NPV = 0.24($881,718 – $117,779)2 + 0.24(-$185,952 – $117,779)2

+ 0.12(-$376,709 – $117,779)2 + 0.4(-$10,000 – $117,779)2

= 198,078,470,853.

σNPV = $445,060.

CVNPV = = 3.78.

Since the CV is 3.78 for this project, while the firm’s average project has a CV of 1.0 to

779,117$

060,445$

website, in whole or in part.

SOLUTION TO SPREADSHEET PROBLEM

11-18 The detailed solution for the problem is available in the file Ch 11 P18 Build a Model