Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Chapter 11 Mini Case

Situation

Part I: Input Data

Equipment cost $200,000 Key Output: NPV = $88,010

Shipping charge $10,000

Installation charge $30,000

Economic Life 4

Salvage Value $25,000

Tax Rate 40%

Cost of Capital 10%

Units Sold 1,250

Sales Price Per Unit $200

Incremental Cost Per Unit $100

NWC/Sales 12%

Inflation rate 3%

Shrieves Casting Company is considering adding a new line to its product mix, and the capital budg

analysis is being conducted by Sidney Johnson, a recently graduated MBA. The production line wou

up in unused space in Shrieves' main plant. The machinery’s invoice price would be approximately $200,000,

another $10,000 in shipping charges would be required, and it would cost an additional $30,000 to inst

equipment. The machinery has an economic life of 4 years, and Shrieves has obtained a special tax r

places the equipment in the MACRS 3-year class. The machinery is expected to have a salvage value of

$25,000 after 4 years of use.

The new line would generate incremental sales of 1,250 units per year for 4 years at an incremental cost

$100 per unit in the first year, excluding depreciation. Each unit can be sold for $200 in the first year. T

price and cost are both expected to increase by 3% per year due to inflation. Further, to handle the new

the firm’s net working capital would have to increase by an amount equal to 12% of sales revenues. The firm’s

tax rate is 40%, and its overall weighted average cost of capital, which is the risk-adjusted cost of ca

an average project (r), is 10%.

a. Define “incremental cash flow.” Answer: See Chapter 11 Mini Case Show

(2.) Suppose the firm had spent $100,000 last year to rehabilitate the production line site. Should t

included in the analysis? Explain. Answer: See Chapter 11 Mini Case Show

(1.) Should you subtract interest expense or dividends when calculating project cash flow? Answ

Chapter 11 Mini Case Show

(3.) Now assume that the plant space could be leased out to another firm at $25,000 per year. Sh

be included in the analysis? If so, how? Answer: See Chapter 11 Mini Case Show

(4.) Finally, assume that the new product line is expected to decrease sales of the firm’s other lines by

$50,000 per year. Should this be considered in the analysis? If so, how? Answer: See Chapter 11

Case Show

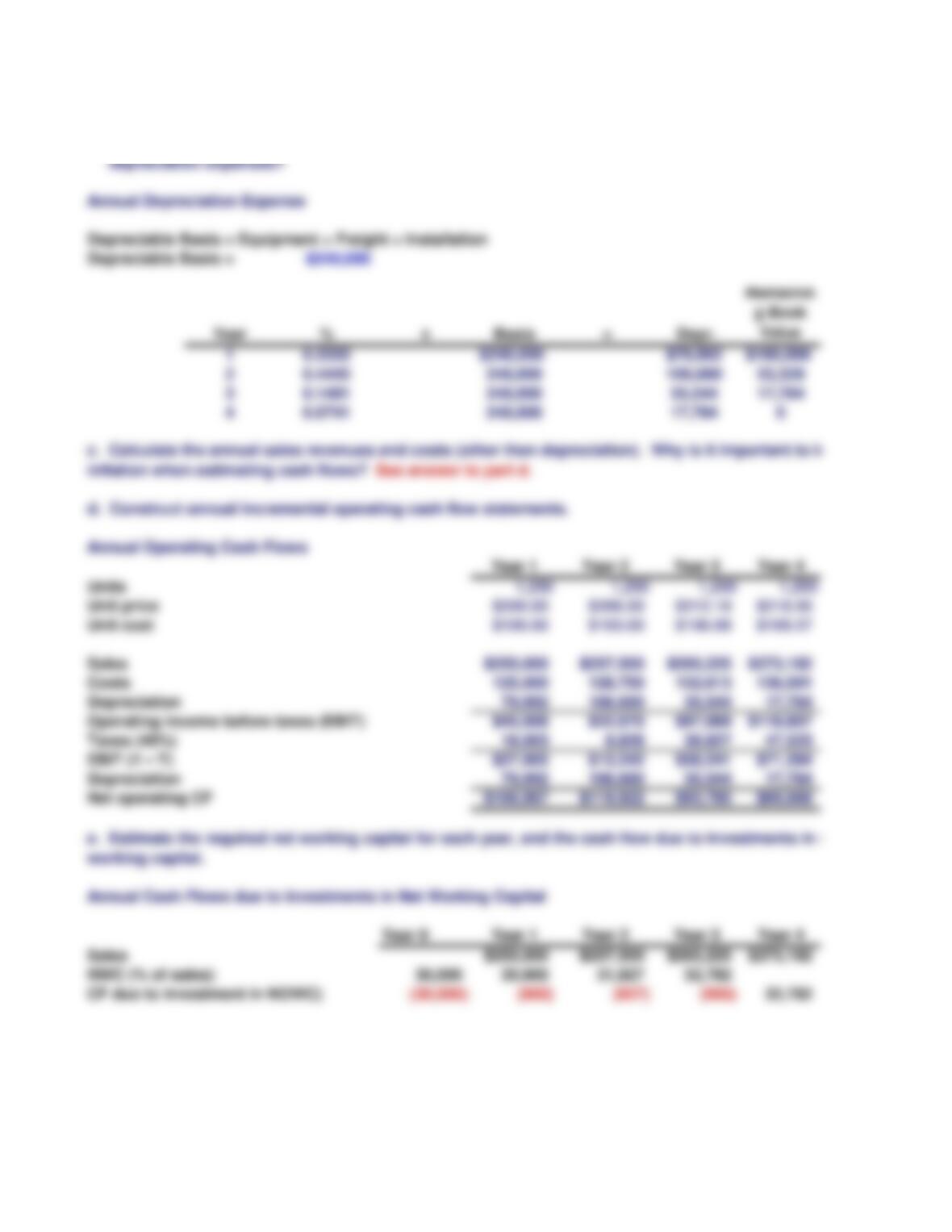

Annual Depreciation Expense

Depreciable Basis = Equipment + Freight + Installation

Depreciable Basis = $240,000

Year % x Basis = Depr.

Remainin

g Book

Value

10.3333 $240,000 $79,992 $160,008

20.4445 240,000 106,680 53,328

30.1481 240,000 35,544 17,784

40.0741 240,000 17,784 0

d. Construct annual incremental operating cash flow statements.

b. Disregard the assumptions in Part a. What is Shrieves' depreciable basis? What are the annual

depreciation expenses?

c. Calculate the annual sales revenues and costs (other than depreciation). Why is it important to includ

inflation when estimating cash flows? See answer to part d.

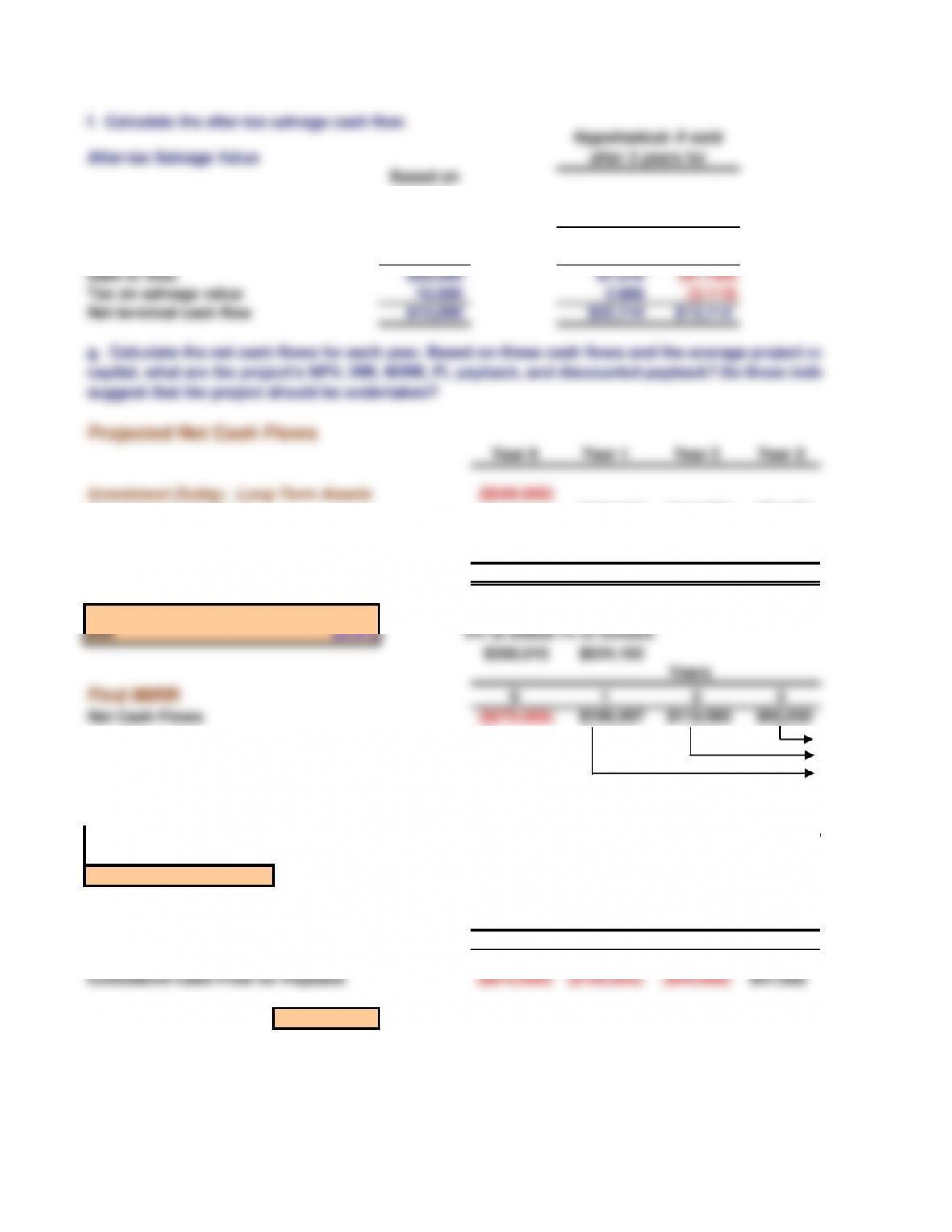

f. Calculate the after-tax salvage cash flow.

After-tax Salvage Value

Based on

facts in

case:

$25,000 $10,000

Salvage value $25,000 $25,000 $10,000

Book value 017,784 17,784

Gain or loss $25,000 $7,216 ($7,784)

Tax on salvage value 10,000 2,886 (3,114)

Net terminal cash flow $15,000 $22,114 $13,114

Projected Net Cash Flows

Year 0 Year 1 Year 2 Year 3

Investment Outlay: Long Term Assets ($240,000)

Operating Cash Flows $106,997 $119,922 $93,785

CF due to investment in NWC (30,000) (900) (927) (955)

Salvage Cash Flows

Net Cash Flows ($270,000) $106,097 $118,995 $92,830

Hypothetical: If sold

after 3 years for

g. Calculate the net cash flows for each year. Based on these cash flows and the average project co

capital, what are the project’s NPV, IRR, MIRR, PI, payback, and discounted payback? Do these indicators

suggest that the project should be undertaken?

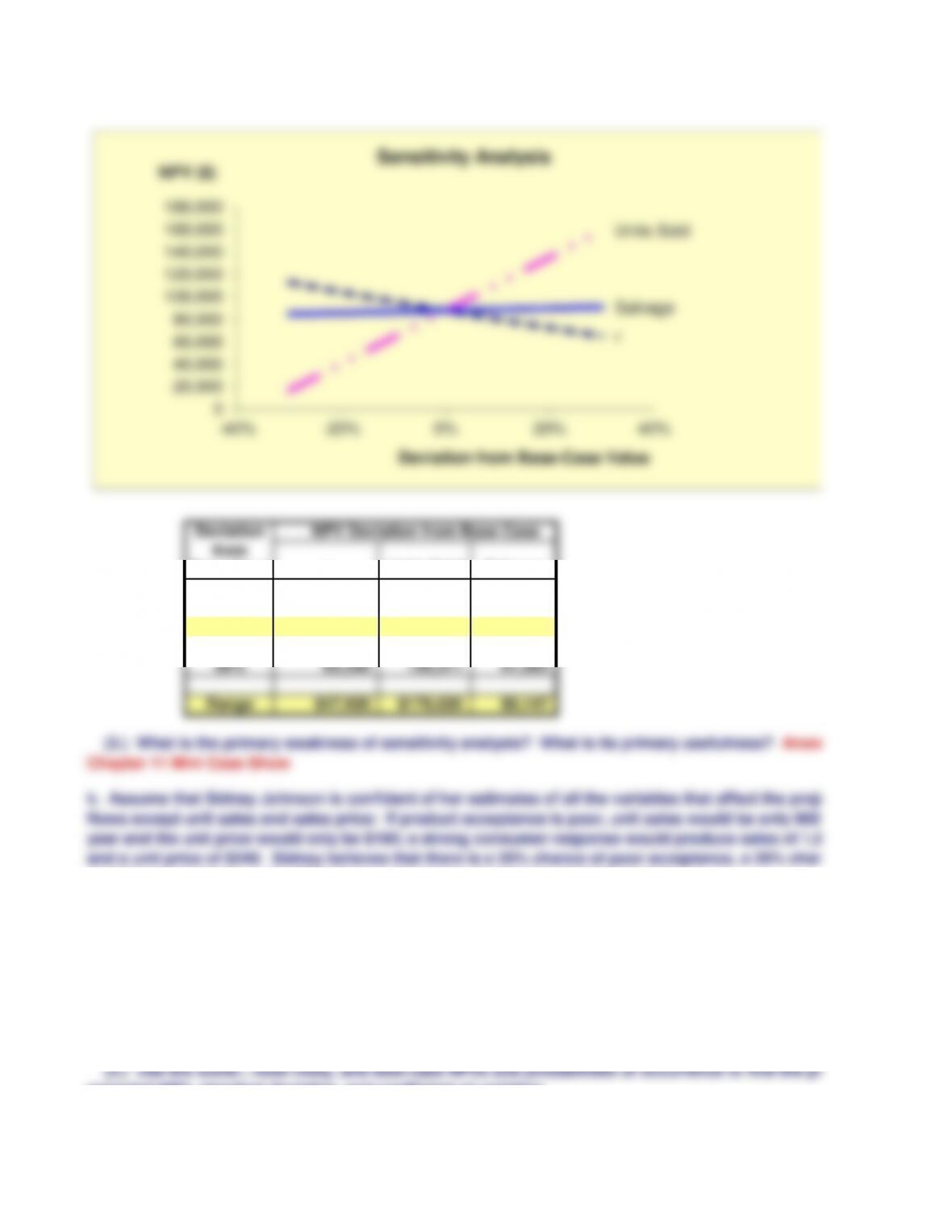

% Deviation % Deviation

% Deviation

from Base r NPV from Base units NPV from

Base Salv.

Base Case 10.0% $88,010 Base Case 1,250 $88,010 Base Case $25,000

-30% 7.0% $113,270 -30% 875 $16,649 -30% $17,500

-15% 8.5% $100,291 -15% 1,063 $52,329 -15% $21,250

0% 10.0% $88,010 0% 1,250 $88,010 0% $25,000

15% 11.5% $76,378 15% 1,438 $123,690 15% $28,750

30% 13.0% $65,350 30% 1,625 $159,371 30% $32,500

i. (1.) What are the three types of risk that are relevant in capital budgeting? Answer: See Chapter

Case Show

(3.) How is each type of risk used in the capital budgeting process? Answer: See Chapter 11 Mini Case

Show

(2.) Perform a sensitivity analysis on the unit sales, salvage value, and cost of capital for the projec

Assume that each of these variables can vary from its base-case, or expected, value by plus and min

10%, 20%, and 30%. Include a sensitivity diagram, and discuss the results.

(2.) How is each of these risk types measured, and how do they relate to one another? Answer:

Chapter 11 Mini Case Show

h. What does the term ”risk” mean in the context of capital budgeting; to what extent can risk be quantified;

and when risk is quantified, is the quantification based primarily on statistical analysis of historical dat

subjective, judgmental estimates?

j. (1.) What is sensitivity analysis? Answer: See Chapter 11 Mini Case Show

Risk in capital budgeting really means the probability that the actual outcome will be worse than the e

outcome. For example, if there were a high probability that the expected NPV as calculated above w

turn out to be negative, then the project would be classified as relatively risky. The reason for a wor

expected outcome is, typically, because sales were lower than expected, costs were higher than expected

and/or the project turned out to have a higher than expected initial cost. In other words, if the assumed

turn out to be worse than expected then the output will likewise be worse than expected. We use Exc

examine the project's sensitivity to changes in the input variables.

r

Here we use an Excel "Data Table" to find the NPVs for changes in unit sales, salvage value, and WA

holding other things constant--changing one variable at a time. This produces the sensitivity analys a

below.

We summarize the data tables and show the sensitivity analysis graph below:

1st YEAR UNIT SALES

SALV

Deviation NPV Deviation from Base Case

from

Base Case r Units Sold Salvage

-30% $113,270 $16,649 $84,936

-15% 100,291 52,329 86,473

0% 88,010 88,010 88,010

15% 76,378 123,690 89,546

30% 65,350 159,371 91,083

Range $47,920 $176,020 $6,147

k. Assume that Sidney Johnson is confident of her estimates of all the variables that affect the project’s cash

flows except unit sales and sales price: If product acceptance is poor, unit sales would be only 900 un

year and the unit price would only be $160; a strong consumer response would produce sales of 1,60

and a unit price of $240. Sidney believes that there is a 25% chance of poor acceptance, a 25% chance of

excellent acceptance, and a 50% chance of average acceptance (the base case).

(1.) What is scenario analysis?

(3.) What is the primary weakness of sensitivity analysis? What is its primary usefulness? Answer

Chapter 11 Mini Case Show

(2.) What is the worst-case NPV? The best-case NPV?

(3.) Use the worst-, most likely, and best-case NPVs and probabilities of occurrence to find the project’s

expected NPV, standard deviation, and coefficient of variation.

Scenario analysis extends risk analysis in two ways: (1) It allows us to change more than one variable a

time, hence to see the combined effects of changes in several variables on NPV, and (2) it allows us to

in the probabilities of changes in the key variables.

r

Units Sold

Salvage

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

-40% -20% 0% 20% 40%

NPV ($)

Deviation from Base-Case Value

Sensitivity Analysis

Scenario Analysis

Probability Unit Sales Unit Price NPV

25% 1,600 $240 $278,940

50% 1,250 $200 $88,010

25% 900 $160 ($48,527)

Quick calculation:

Expected NPV = $101,608 $101,608

Standard Deviation = $116,573 $116,573

Coefficient of Variation = Std Dev / Expected NPV = 1.15

$7,861,657,811.87

Squared Deviation

times Probability

$92,456,383.34

$5,635,163,606.11

Best Case

Scenario

Base Case

Worst Case

We could find the NPV by entering the value of unit sales and price for each scenario and then recordin

NPV (this is what we did for the table below). Alternatively, we could use Tools, Scenarios to define t

for each scenario, which we did and show in the Scenario Summary Tab below. In fact, you could ev

Tools, Scenarios, and then click the Summary button on the dialog box, and it will automatically crea

similar to the one below. This is a powerful feature of Excel, and we encourage you to explore it.

10/28/2015

dgeting

ould be set

up in unused space in Shrieves' main plant. The machinery’s invoice price would be approximately $200,000,

install the

ax ruling that

alue of

al cost of

ear. The sales

e new line,

the firm’s net working capital would have to increase by an amount equal to 12% of sales revenues. The firm’s

capital for

a. Define “incremental cash flow.”

uld this be

nswer: See

. Should this

(4.) Finally, assume that the new product line is expected to decrease sales of the firm’s other lines by

er 11 Mini

n net

al

include

Year 4

$89,068

32,782

15,000

$136,850

4

$136,850

102,113

143,984

141,215

$524,162

4

$136,850

$184,772

age project cost of

capital, what are the project’s NPV, IRR, MIRR, PI, payback, and discounted payback? Do these indicators

use the MIRR

NPV

$88,010

$84,936

$86,473

$88,010

$89,546

$91,083

apter 11 Mini

ini Case

e project.

d minus

er: See

h. What does the term ”risk” mean in the context of capital budgeting; to what extent can risk be quantified;

l data or on

he expected

e will actually

orse-than-

an expected,

umed inputs

Excel to

ACC

analys as shown

LVAGE