Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

1

2

3

4

5

6

7

8

9

10

11

12

13

15

16

17

18

19

26

27

28

29

30

31

35

36

37

A B C D E F G H I J

10/28/2015

Situation

250 60 Franchise L

320 80

0 1 2 3

(100) 10 60 80

Depreciation, salvage values, net working capital requirements, and tax effects are all included in these cash flows.

a. What is capital budgeting? Answer: See Chapter 10 Mini Case Show

b. What is the difference between independent and mutually exclusive projects? Answer: See Chapter 10 Mini Case

Chapter 10. Mini Case

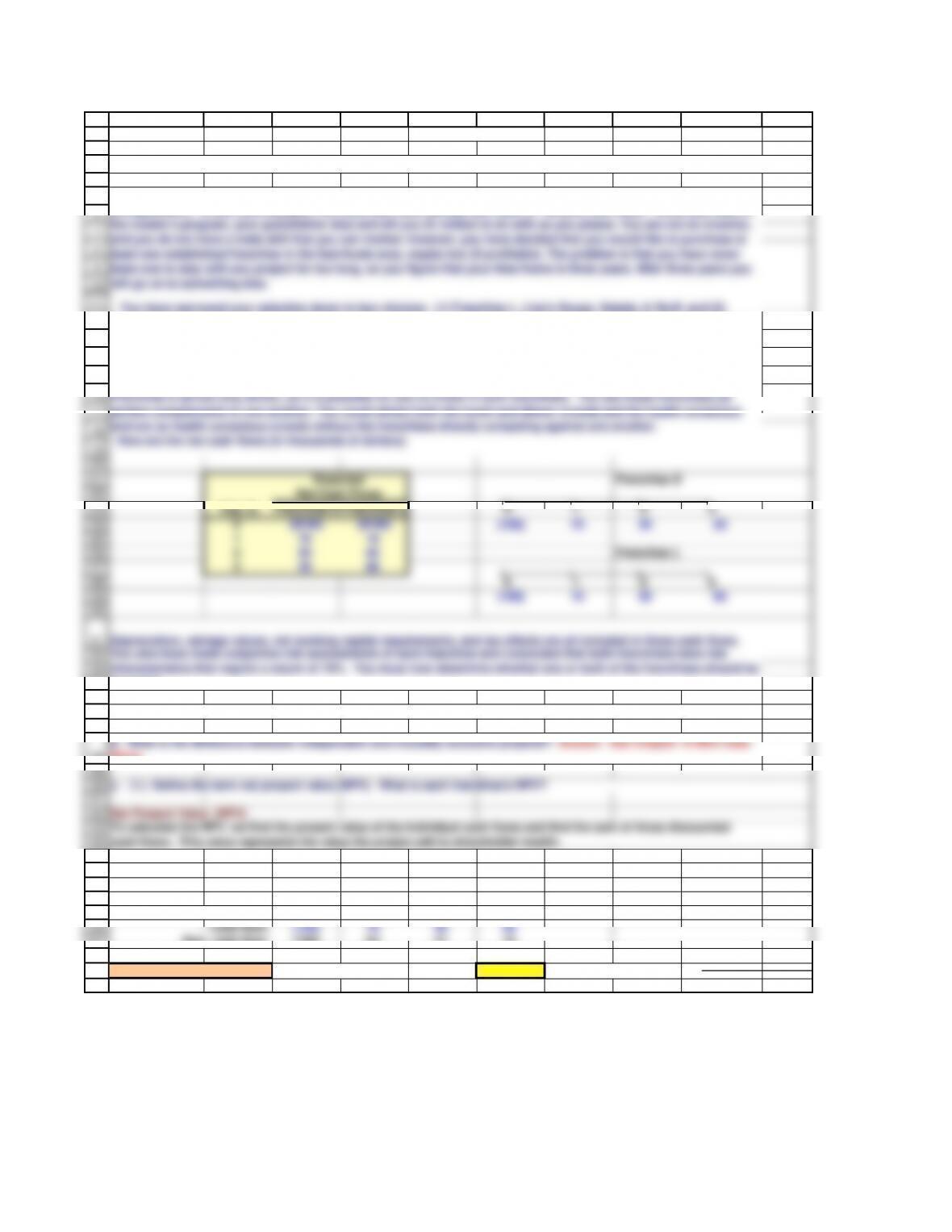

You have narrowed your selection down to two choices: (1) Franchise L, Lisa's Soups, Salads, & Stuff, and (2)

Franchise S, Sam's Fabulous Fried Chicken. The net cash flows shown below include the price you would receive for

selling the franchise in Year 3 and the forecast of how each franchise will do over the 3-year period. Franchise L's

cash flows will start off slowly but will increase rather quickly as people become more health conscious, while

Franchise S's cash flows will start off high but will trail off as other chicken competitors enter the marketplace and as

people become more health conscious and avoid fried foods. Franchise L serves breakfast and lunch, while

Franchise S serves only dinner, so it is possible for you to invest in both franchises. You see these franchises as

perfect complements to one another: You could attract both the lunch and dinner crowds and the health conscious

and not so health conscious crowds without the franchises directly competing against one another.

Here are the net cash flows (in thousands of dollars):

You have just graduated from the MBA program of a large university, and one of your favorite courses was "Today's

Entrepreneurs." In fact, you enjoyed it so much you have decided you want to "be your own boss." While you were in

the master's program, your grandfather died and left you $1 million to do with as you please. You are not an inventor,

and you do not have a trade skill that you can market; however, you have decided that you would like to purchase at

least one established franchise in the fast-foods area, maybe two (if profitable). The problem is that you have never

been one to stay with any project for too long, so you figure that your time frame is three years. After three years you

will go on to something else.

55

56

57

58

59

60

61

62

63

64

65

66

67

68

69

70

71

72

73

74

75

76

77

78

79

80

81

82

83

84

85

86

90

91

92

93

94

95

96

98

99

100

101

102

103

104

105

109

110

111

112

113

114

115

116

117

118

119

120

121

A B C D E F G H I J

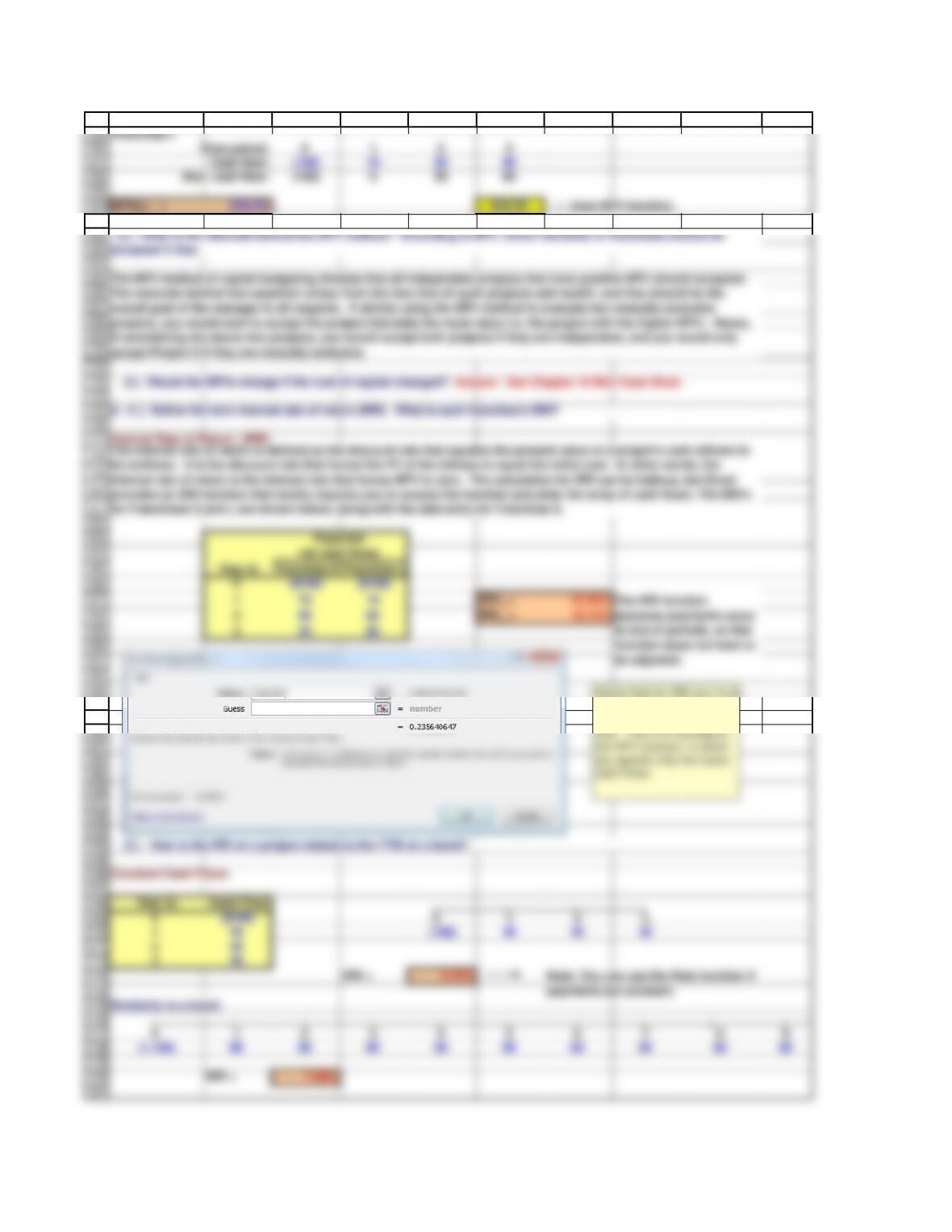

Franchise L

Time period: 0 1 2 3

Cash flow: (100) 10 60 80

Disc. cash flow: (100) 9 50 60

NPV(L) = $18.78 $18.78 = Uses NPV function.

Internal Rate of Return (IRR)

Year (t)

Franchise S

Franchise L

0($100) ($100)

0($100) 0 123

140 (100) 40 40 40

240

340

IRR = 9.70% Note: You can use the Rate function if

payments are constant.

Similarity to a bond:

0 1 2 3 4 5 6 7 8 9

(1,134) 90 90 90 90 90 90 90 90 90

IRR = 7.08%

The NPV method of capital budgeting dictates that all independent projects that have positive NPV should accepted.

The rationale behind that assertion arises from the idea that all such projects add wealth, and that should be the

overall goal of the manager in all respects. If strictly using the NPV method to evaluate two mutually exclusive

projects, you would want to accept the project that adds the most value (i.e. the project with the higher NPV). Hence,

if considering the above two projects, you would accept both projects if they are independent, and you would only

accept Project S if they are mutually exclusive.

(3.) Would the NPVs change if the cost of capital changed? Answer: See Chapter 10 Mini Case Show

The internal rate of return is defined as the discount rate that equates the present value of a project's cash inflows to

its outflows. It is the discount rate that forces the PV of the inflows to equal the initial cost. In other words, the

internal rate of return is the interest rate that forces NPV to zero. The calculation for IRR can be tedious, but Excel

provides an IRR function that merely requires you to access the function and enter the array of cash flows. The IRR's

for Franchises S and L are shown below, along with the data entry for Franchise S.

d. (1.) Define the term internal rate of return (IRR). What is each franchise's IRR?

(2.) How is the IRR on a project related to the YTM on a bond?

net cash flows

(2.) What is the rationale behind the NPV method? According to NPV, which franchise or franchises should be

accepted if they

Expected

be adjusted.

Notice that for IRR you must

specify all cash flows,

including the time zero cash

flow. This is in contrast to

you specify only the future

cash flows.

122

123

124

125

126

127

128

129

130

131

132

133

134

135

143

144

145

146

147

148

149

150

151

152

153

154

155

156

157

158

159

160

161

162

163

164

165

166

167

168

169

170

171

172

173

174

175

176

177

178

179

180

181

182

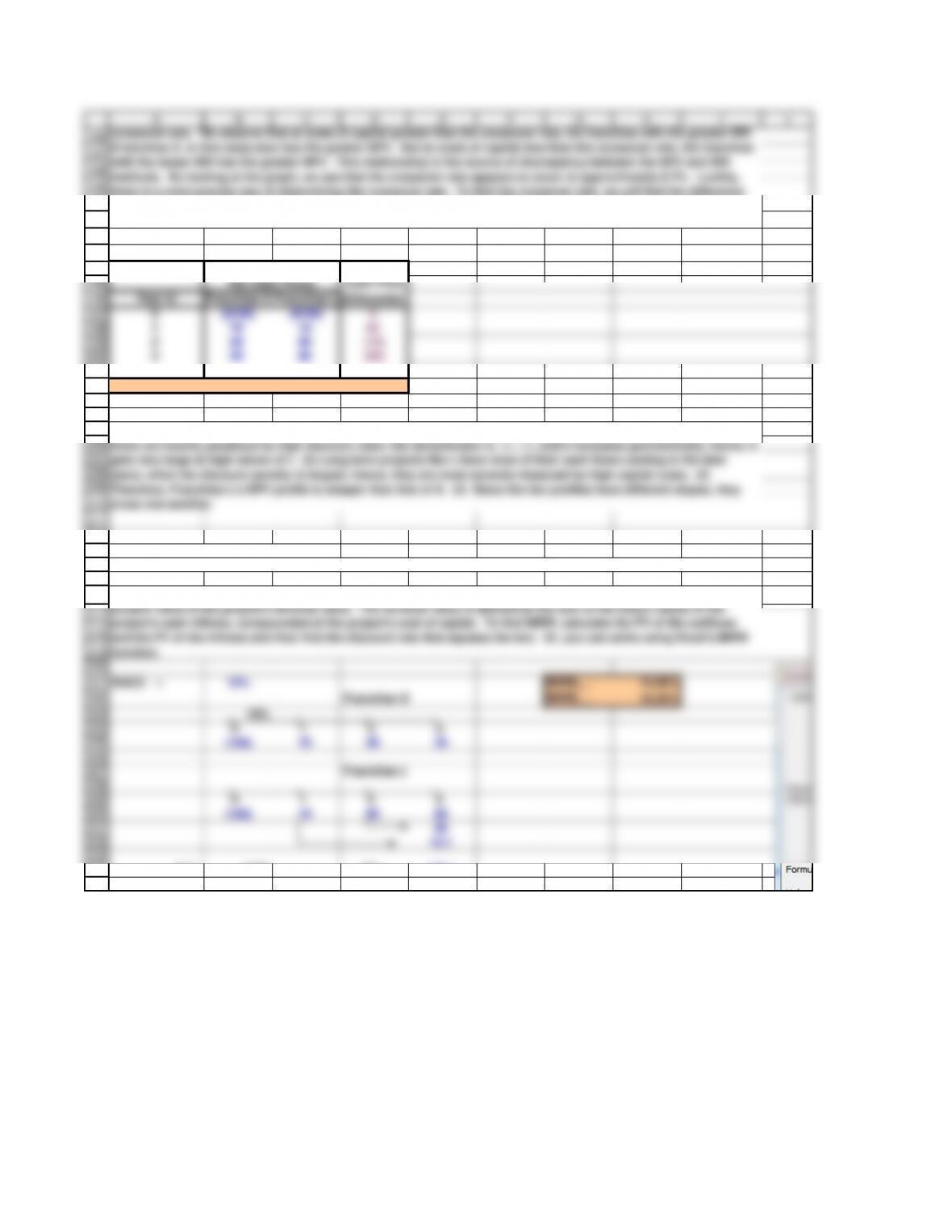

A B C D E F G H I J

2% 35.53 2% 42.86

4% 31.32 4% 36.21

6% 27.33 6% 30.00

8% 23.56 8% 24.21

10% 19.98 10% 18.78

12% 16.60 12% 13.70

14% 13.38 14% 8.94

16% 10.32 16% 4.46

18% 7.40 18% 0.26

20% 4.63 20% (3.70)

22% 1.98 22% (7.43)

24% (0.54) 24% (10.95)

f. What is the underlying cause of ranking conflicts between NPV and IRR?

The IRR method of capital budgeting maintains that projects should be accepted if their IRR is greater than the cost of

capital. Strict adherence to the IRR method would further dictate that mutually exclusive projects should be chosen

on the basis of the greatest IRR. In this scenario, both franchises have IRRs that exceed the cost of capital (10%) and

both should be accepted, if they are independent. If, however, the franchises are mutually exclusive, we would

choose Franchise S. Recall, that this was our determination using the NPV method as well. The question that

naturally arises is whether or not the NPV and IRR methods will always arrive at the same conclusion.

Previously, we had discussed that in some instances the NPV and IRR methods can give conflicting results. First, we

should attempt to define what we see in this graph. Notice, that the two franchises' profiles (S and L) intersect the X-

axis at costs of capital of 18.13% and 23.56%, respectively. Not coincidently, those are the IRRs of the franchises. If

we think about the definition of IRR, we remember that the internal rate of return is the cost of capital at which a

project will have an NPV of zero. Looking at our graph, it is a logical conclusion that the project IRR is defined as the

point at which its profile intersects the

X-axis.

(4.) Would the franchises' IRRs change if the cost of capital changed?

(2.) Look at your NPV profile graph without referring to the actual NPVs and IRRs. Which franchise or franchises

should be accepted if they are independent? Mutually exclusive? Explain. Are your answers correct at any cost of

capital less than 23.6%?

When dealing with independent projects, the NPV and IRR methods will always yield the same accept/reject result.

However, in the case of mutually exclusive projects, NPV and IRR can give conflicting results. One shortcoming of

the internal rate of return is that it assumes that cash flows received are reinvested at the project's internal rate of

return, which is not usually true. The nature of the congruence of the NPV and IRR methods is further detailed in a

latter section of this model.

(3.) What is the logic behind the IRR method? According to IRR, which franchises should be accepted if they are

independent?

(20)

(10)

0

10

20

30

40

50

60

0% 2% 4% 6% 8% 10% 12% 14% 16% 18% 20% 22% 24%

NPV ($)

Cost of Capital

NPV Profile of Franchises S and L

Project L

Project S

Franchise L- IRR

Franchise

S- IRR

Crossover Rate =

8.7%

186

187

188

189

190

191

192

193

194

195

196

197

198

199

200

201

202

203

204

205

206

207

208

212

213

214

215

216

217

218

A B C D E F G H I J

Cash Flow

Year (t)

Franchise S

Franchise L Differential

0($100) ($100) 0

170 10 60

250 60 (10)

320 80 (60)

IRR = Crossover rate = 8.68%

Modified Internal Rate of Return (MIRR)

The modified internal rate of return is the discount rate that causes a project's cost (or cash outflows) to equal the

present value of the project's terminal value. The terminal value is defined as the sum of the future values of the

project's cash inflows, compounded at the project's cost of capital. To find MIRR, calculate the PV of the outflows

g. Define the term modified IRR (MIRR). Find the MIRRs for Franchises L and S.

Expected

Net Cash Flows

The intuition behind the relationship between the NPV profile and the crossover rate is as follows: (1) Distant cash

flows are heavily penalized by high discount rates--the denominator is (1 + r)t, and it increases geometrically; hence, it

gets very large at high values of t. (2) Long-term projects like L have most of their cash flows coming in the later

crossover rate. We observe that at costs of capital greater than the crossover rate, the franchise with the greater IRR

(Franchise S, in this case) also has the greater NPV. But at costs of capital less than the crossover rate, the franchise

with the lesser IRR has the greater NPV. This relationship is the source of discrepancy between the NPV and IRR

methods. By looking at the graph, we see that the crossover rate appears to occur at approximately 8.7%. Luckily,

there is a more precise way of determining the crossover rate. To find the crossover rate, we will find the difference

between the two franchises' cash flows in each year, and then find the IRR of this series of differential cash flows.

This IRR is the crossover rate.

236

237

238

239

240

241

242

243

244

245

246

247

249

250

251

253

254

255

256

258

259

260

261

262

263

264

265

266

267

269

270

271

272

273

274

275

276

277

278

279

281

282

283

284

285

286

287

288

289

290

291

292

293

294

295

296

297

298

299

300

301

302

A B C D E F G H I J

PROFITABILITY INDEX

h. What does the profitability index (PI) measure? What are the PI's for Franchises S and L?

For Franchise S:

PI(S) = PV of future cash flows ÷Initial cost

PI(S) = $119.98 ÷$100

PI(S) = 1.1998

PI(L) = PV of future cash flows ÷Initial cost

PI(L) = $118.78 ÷$100

PI(L) = 1.1878

i. (1.) What is the payback period? Find the paybacks for Franchises L and S.

Payback Period

Franchise S

Time period: 0 1 2 3

Cash flow: (100) 70 50 20

Cumulative cash flow: (100) (30) 20 40

—1.60 —

Alternative calcuation using the Excel PERCENTRANK function

Payback: 1.600

Franchise L

Time period: 0 1 2 3

Cash flow: (100) 10 60 80

Cumulative cash flow: (100) (90) (30) 50

Payback: 2.375

Discounted Payback Period

r = 10%

Franchise S

Time period: 0 1 2 3

Cash flow: (100) 70 50 20

Disc. cash flow: (100) 64 41 15 Cash Flows Discounted ba

Disc. cum. cash flow: (100) (36) 5 20

The profitability index is the present value of all future cash flows divided by the intial cost. It measures the PV per

dollar of investment.

Discounted payback period uses the project's cost of capital to discount the expected cash flows. The calculation of

discounted payback period is identical to the calculation of regular payback period, except you must base the

calculation on a new row of discounted cash flows. Note that both projects have a cost of capital of 10%.

(3.) What is the difference between the regular and discounted payback periods?

inflows exceed the initial cash outflows. That is the payback year. Then we take the previous year and add to it the

fraction calculated as the unrecovered balance at the end of that year divided by the following year's cash flow.

Generally speaking, the shorter the payback period, the better the investment.

(2.) What is the rationale for the payback method? According to the payback criterion, which franchise or

franchises should

be accepted if the firm's maximum acceptable payback is 2 years, and if Franchise L and S are independent? If

See the discussion on the PERCENTRANK function in the

Toolkit for this Chapter. Note that if cash flows are

nonnormal, the PERCENTRANK function will not always give

correct result. In that case, use the onger procedure shown

above.

Intermediate calculation to

identify payback:

303

304

305

A B C D E F G H I J

Discounted Payback: 1.9

306

307

308

309

310

311

312

313

314

315

316

317

318

319

320

321

322

323

324

325

326

327

328

329

330

331

332

333

334

335

336

337

338

339

340

341

342

343

344

345

346

347

348

349

350

351

352

353

354

355

356

A B C D E F G H I J

Franchise L

Time period: 0 1 2 3 4

Cash flow: (100) 10 60 80 0

Disc. cash flow: (100) 9 50 60 0

Disc. cum. cash flow: (100) (91) (41) 19 19

Discounted Payback: 2.7

Multiple IRRs

Project M: 0 1 2

(800) 5,000 (5,000)

The project is estimated to be of average risk, so its cost of capital is 10%.

(2.) What is Project P's NPV? What is its IRR? Its MIRR?

NPVM = ($386.78)

IRR M

1 = 25.0% MIRR = 5.6%

IRR M

2 = 400% =IRR(C326:E326,200%)

012

(800.0) 5,000 (5,000)

(4.) What is the main disadvantage of discounted payback? Is the payback method of any real usefulness in capital

budgeting

The inherent problem with both paybacks is that they ignore cash flows that occur after the payback period mark and

neither provides a specific acceptance rule. While the discounted method accounts for timing issues (to some

extent), it still falls short of fully analyzing projects. However, all else equal, these two methods do provide some

information about projects' liquidity and risk.

(1.) What are normal and nonnormal cash flows? Answer: See Chapter 10 Mini Case Show

We will solve this IRR twice, the first time using the default guess of 10%, and the second time we will enter a guess of

200%. Notice, that the first IRR calculation is exactly as it was above.

The two solutions to this problem tell us that this project will have a positive NPV for all costs of capital between 25%

and 400%. We illustrate this point by creating a data table and a graph of the project NPVs.

j. As a separate project (Project P), you are considering sponsoring a pavilion at the upcoming World's Fair. The

pavilion would cost $800,000, and it is expected to result in $5 million of incremental cash inflows during its 1 year of

operation. However, it would then take another year, and $5 million of costs, to demolish the site and return it to its

original condition. Thus, Project P's expected net cash flows look like this (in thousands of dollars):

357

358

359

360

361

362

363

364

365

366

367

368

369

370

371

372

373

374

375

376

377

378

379

380

381

382

383

384

385

386

387

388

389

390

391

392

393

394

395

396

397

398

399

400

401

402

403

404

405

406

407

408

409

410

411

412

413

414

415

416

417

418

A B C D E F G H I J

r = 25.0%

NPV = 0.00

NPV

r$0.0

0% (800.00)

25% 0.00

50% 311.11

75% 424.49

100% 450.00 Max.

125% 434.57

150% 400.00

175% 357.02

200% 311.11

225% 265.09

250% 220.41

275% 177.78

300% 137.50

325% 99.65

350% 64.20

375% 31.02

400% 0.00

425% (29.02)

450% (56.20)

475% (81.66)

500% (105.56)

525% (128.00)

550% (149.11)

PROJECTS WITH UNEQUAL LIVES

Year Project T Project R

0($100,000) ($100,000)

160,000 33,500

260,000 33,500

333,500

433,500

Project T r: 10.0%

0 1 2 3 4

($100) $33.5 $33.5 $33.5 $33.5

NPV $6.19

Project F

0 1 2 3 4

($100) $60 $60

NPV $4.13

(1.) What is each project’s initial NPV without replication?

The projects provide a necessary service, so whichever one is selected is expected to be repeated into the foreseeable

future. Both projects have a 10% cost of capital.

(3.) Draw Project P's NPV profile. Does Project P have normal or nonnormal cash flows? Should this project be accept

k. In an unrelated analysis, you have the opportunity to choose between the following two mutually exclusive

projects, Project T (which lasts for two years) and Project F (which lasts for four years):

End of Period:

End of Period:

-1,000

-800

-600

-400

-200

0

200

400

600

-100% 0% 100% 200% 300% 400% 500%

NPV ($)

Cost of Capital

Multiple Rates of Return

419

420

421

422

423

424

425

426

427

428

429

430

431

432

434

435

438

439

440

441

442

443

444

445

446

447

448

450

451

452

453

454

455

456

457

458

459

460

461

462

463

464

465

466

467

468

469

470

471

472

473

474

475

476

A B C D E F G H I J

Equivalent Annual Annuity (EAA) Approach

Here are the steps in the EAA approach.

1. Find the NPV of each project over its initial life (we already did this in our previous analysis).

NPVC = $6.19

NPVR = $4.13

2. Convert the NPV into an annuity payment with a life equal to the life of the project.

EAAT = $1.95 Note: we used Excel's PMT function by using the function wizard.

EAAF = $2.38

Project T

($100) $60 $60

($100) $60 $60

($100) $60 ($40) $60 $60

NPV $7.55

Project T

0 1 2 3

($100) $60 $60

($105) $60 $60

($100) $60 ($45) $60 $60

NPV $3.42

ECONOMIC LIFE VS. PHYSICAL LIFE

Year

Operating

Cash Flow

Salvage

Value

0($5,000) $5,000

1$2,100 $3,100

2$2,000 $2,000

3$1,750 $0

3-Year NPV =

Initial Cost +

PV of

Operating

Cash Flow

+

PV of

Salvage

Value

=($5,000.00) +$4,876.78 +$0.00

3-Year NPV = ($123.22)

l. You are also considering another project which has a physical life of 3 years; that is, the machinery will be totally

worn out after 3 years. However, if the project were terminated prior to the end of 3 years, the machinery would have

a positive salvage value. Here are the project’s estimated cash flows:

The asset has a negative NPV if it is kept for three years. But even though the asset will last three years, it might be

better to operate the asset for either one or two years, and then salvage it.

(1.) Using the 10% cost of capital, what is the project's NPV If it is operated for the full 3 years?

End of Period:

End of Period:

(2.) What is each project’s equivalent annual annuity?

(4.) Now assume that the cost to replicate Project T in 2 years will increase to $105,000 because of inflationary

pressures.

(3.) Now apply the replacement chain approach to determine the projects’ extended NPVs. Which project should be

chosen?

482

483

484

485

486

487

488

489

490

A B C D E F G H I J

1-Year NPV =

Initial Cost +

PV of

Operating

+

PV of

Salvage

=($5,000.00) +$1,909.09 +$2,818.18

1-Year NPV = ($272.73)

The project's NPV will only be positive when it is operated for 2 years. Therefore, the project's economic life is 2 years.

(4.) What is the project’s optimal (economic) life?

(3.) At the end of Year 1?