1

2

3

4

5

6

7

8

9

10

11

12

19

20

21

22

23

First, we want to lay out all of the input data in the problem.

30

31

32

33

34

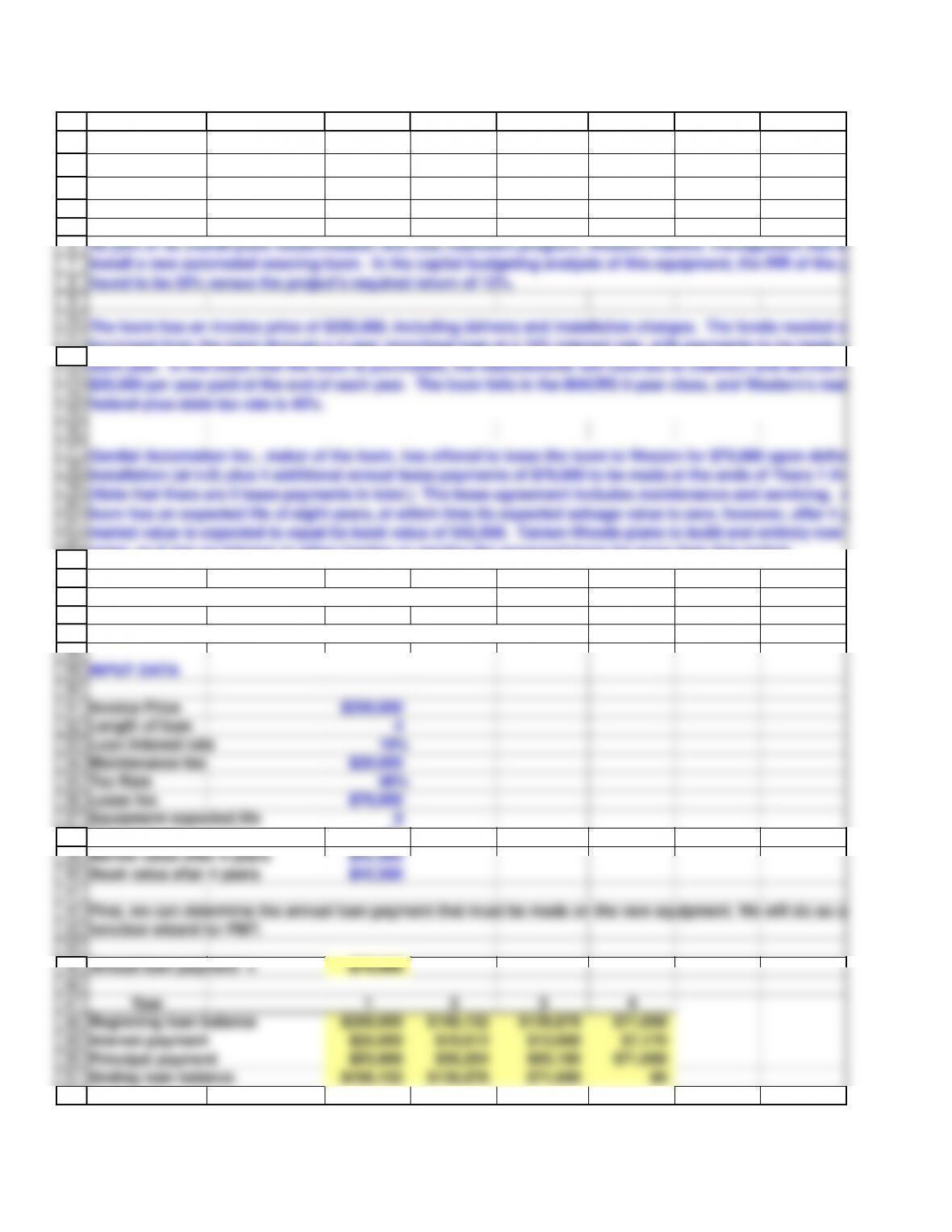

Tax Rate 40%

Lease fee $70,000

Equipment expected life 8

Expected salvage value $0

Market value after 4 years $42,500

Book value after 4 years $42,500

41

42

43

44

45

Beginning loan balance $250,000 $196,132 $136,878 $71,698

Interest payment $25,000 $19,613 $13,688 $7,170

Principal payment $53,868 $59,254 $65,180 $71,698

Ending loan balance $196,132 $136,878 $71,698 $0

52

A B C D E F G H

Solution

Chapter: 19

Problem: 6

Invoice Price $250,000

Length of loan 4

Loan Interest rate 10%

Maintenance fee $20,000

First, we can determine the annual loan payment that must be made on the new equipment. We will do so using the

function wizard for PMT.

Annual loan payment = $78,868

As part of its overall plant modernization and cost reduction program, Western Fabrics’ management has decided to

install a new automated weaving loom. In the capital budgeting analysis of this equipment, the IRR of the project was

found to be 20% versus the project’s required return of 12%.

The loom has an invoice price of $250,000, including delivery and installation charges. The funds needed could be

borrowed from the bank through a 4-year amortized loan at a 10% interest rate, with payments to be made at the end of

each year. In the event that the loom is purchased, the manufacturer will contract to maintain and service it for a fee of

installation (at t=0) plus 4 additional annual lease payments of $70,000 to be made at the ends of Years 1 through 4.

(Note that there are 5 lease payments in total.) The lease agreement includes maintenance and servicing. Actually, the

loom has an expected life of eight years, at which time its expected salvage value is zero; however, after 4 years, its

market value is expected to equal its book value of $42,500. Tanner-Woods plans to build and entirely new plant in 4

years, so it has no interest in either leasing or owning the proposed loom for more than that period.

53

54

55

56

57

58

A B C D E F G H

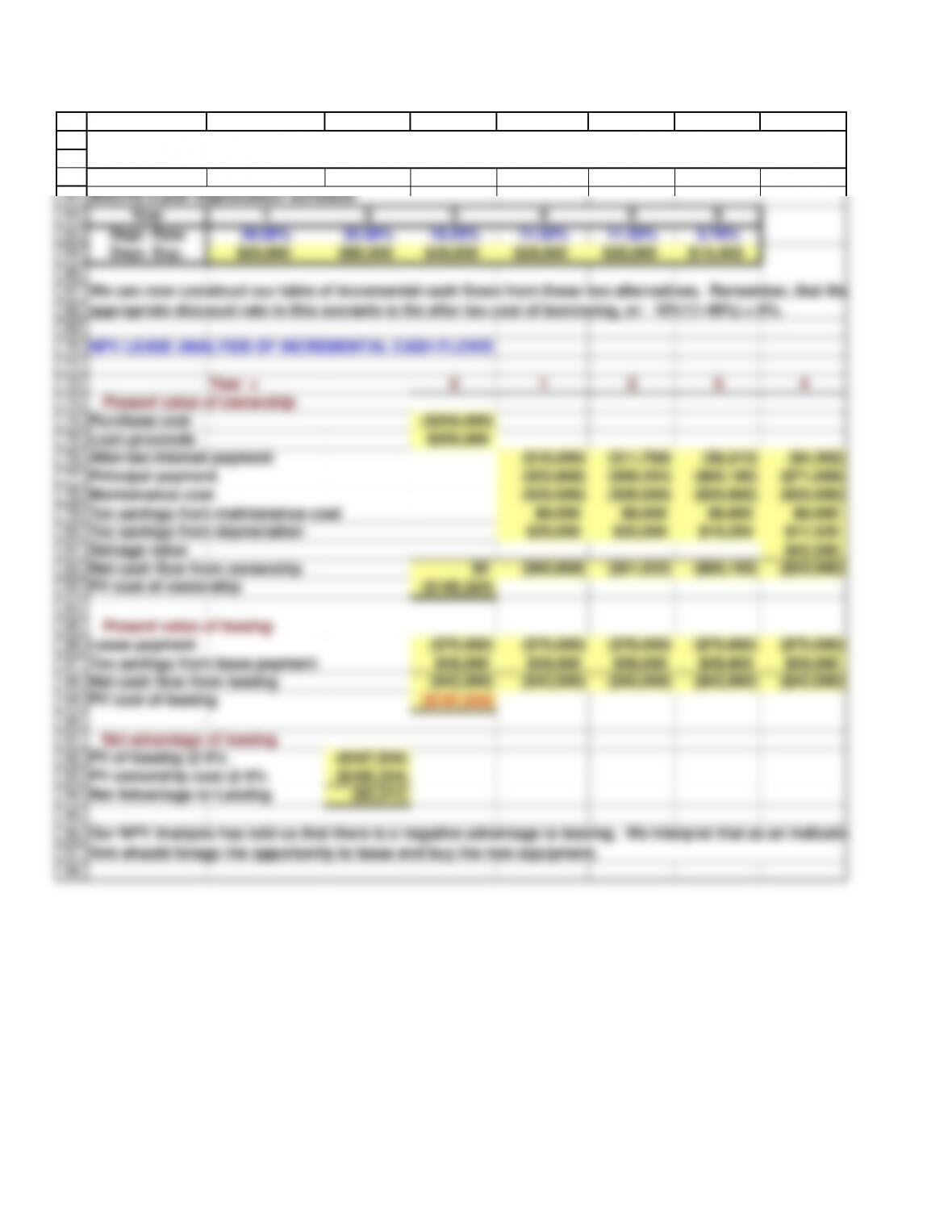

Now, we see that the decision being made is whether to purchase the equipment at a net cost of $250,000 (with annual

payments of $78,868) or lease the equipment and make annual payments of $70,000. To make this decision, we must

analyze the incremental cash flows.

59

60

61

62

63

64

65

66

67

68

69

70

71

72

73

74

75

76

77

78

79

80

81

82

83

PV cost of ownership ($185,324)

84

Present value of leasing

Lease payment ($70,000) ($70,000) ($70,000) ($70,000) ($70,000)

87

88

89

90

91

94

PV of leasing @ 6% ($187,534)

PV ownership cost @ 6% ($185,324)

Net Advantage to Leasing ($2,211)

Our NPV Analysis has told us that there is a negative advantage to leasing. We interpret that as an indication that the

97

98

A B C D E F G H

MACRS 5-year Depreciation Schedule

Year 1 2 3 4 5 6

Depr. Rate 20.00% 32.00% 19.20% 11.52% 11.52% 5.76%

Depr. Exp. $50,000 $80,000 $48,000 $28,800 $28,800 $14,400

NPV LEASE ANALYSIS OF INCREMENTAL CASH FLOWS

Year = 0 1 2 3 4

Present value of ownership

Purchase cost ($250,000)

Loan proceeds $250,000

After-tax interest payment ($15,000) ($11,768) ($8,213) ($4,302)

Principal payment ($53,868) ($59,254) ($65,180) ($71,698)

Maintenance cost ($20,000) ($20,000) ($20,000) ($20,000)

Tax savings from maintenance cost $8,000 $8,000 $8,000 $8,000

Tax savings from depreciation $20,000 $32,000 $19,200 $11,520

Salvage value $42,500

Net cash flow from ownership $0 ($60,868) ($51,022) ($66,193) ($33,980)

Tax savings from lease payment $28,000 $28,000 $28,000 $28,000 $28,000

Net cash flow from leasing ($42,000) ($42,000) ($42,000) ($42,000) ($42,000)

PV cost of leasing ($187,534)

Net advantage of leasing

Before proceeding with our NPV analysis we must determine the schedule of depreciation charges for this new

equipment.

We can now construct our table of incremental cash flows from these two alternatives. Remember, that the

appropriate discount rate in this scenario is the after tax cost of borrowing, or: 10%*(1-40%) = 6%.

firm should forego the opportunity to lease and buy the new equipment.

99

100

101

102

103

104

105

106

107

108

109

110

111

112

113

114

115

116

117

118

119

122

123

124

125

126

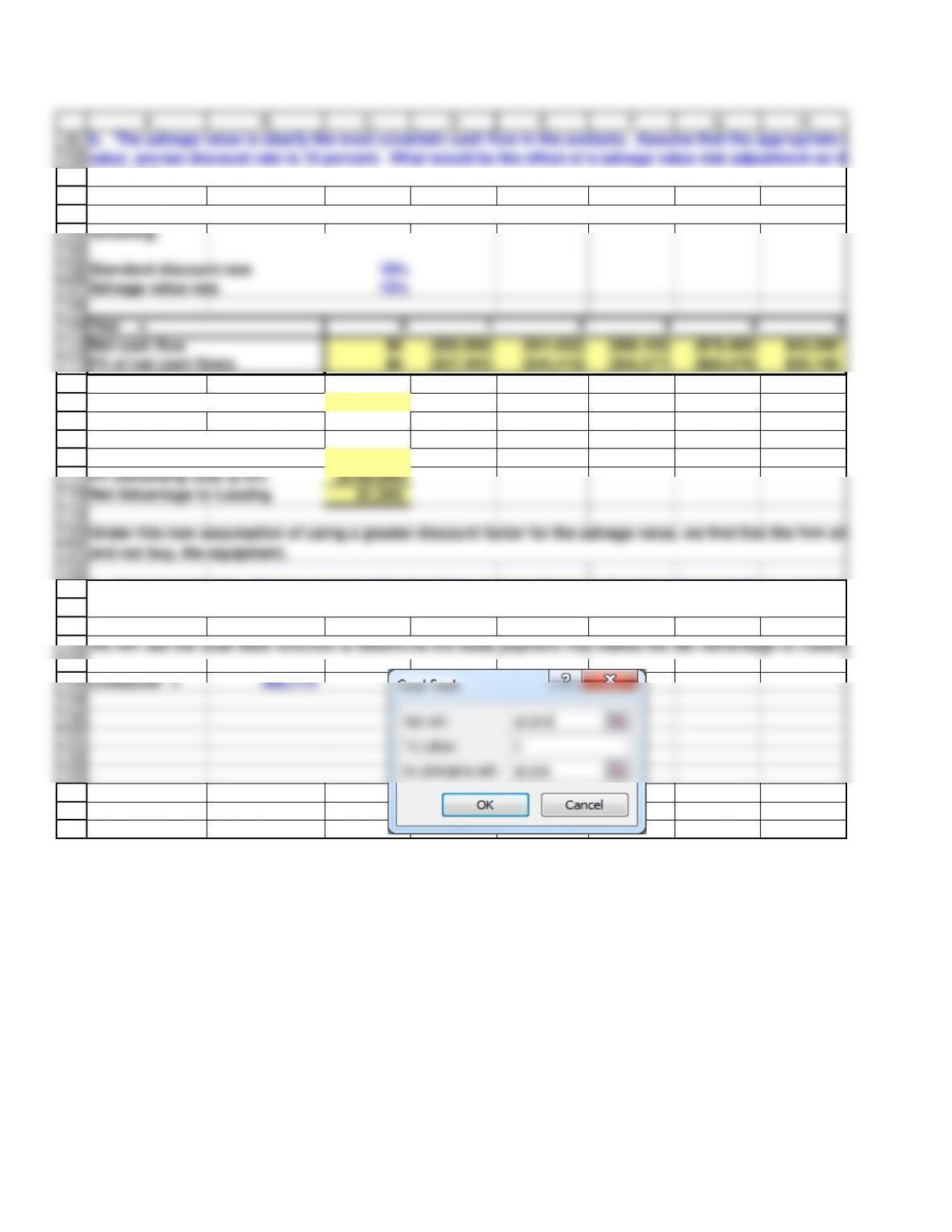

Crossover = $69,175

A B C D E F G H

All cash flows would remain unchanged except that of the salvage value. Our new array of cash flows would resemble the

following:

Standard discount rate 10%

Salvage value rate 15%

Year = 0 1 2 3 4 4

Net cash flow $0 ($60,868) ($51,022) ($66,193) ($76,480) $42,500

PV of net cash flows $0 ($57,422) ($45,410) ($55,577) ($60,579) $30,108

NPV of ownership ($188,880)

Net advantage of leasing

PV of leasing @ 6% ($187,534)

PV ownership cost @ 6% ($188,880)

Net Advantage to Leasing $1,345

We will use the Goal Seek function to determine the lease payment that makes the Net Advantage to Leasing zero.

c. Assuming that the after-tax cost of debt should be used to discount all anticipated cash flows, at what lease

payment would the firm be indifferent to either leasing or buying?

b. The salvage value is clearly the most uncertain cash flow in the analysis. Assume that the appropriate salvage

value pre-tax discount rate is 15 percent. What would be the effect of a salvage value risk adjustment on the

decision?

1

2

3

4

5

6

7

8

9

16

17

18

19

20

27

28

29

30

31

38

39

40

41

42

49

50

51

52

I J K

7/16/2015

First, we can determine the annual loan payment that must be made on the new equipment. We will do so using the

As part of its overall plant modernization and cost reduction program, Western Fabrics‘ management has decided to

install a new automated weaving loom. In the capital budgeting analysis of this equipment, the IRR of the project was

found to be 20% versus the project‘s required return of 12%.

Gardial Automation Inc., maker of the loom, has offered to lease the loom to Westen for $70,000 upon delivery and

installation (at t=0) plus 4 additional annual lease payments of $70,000 to be made at the ends of Years 1 through 4.

(Note that there are 5 lease payments in total.) The lease agreement includes maintenance and servicing. Actually, the

loom has an expected life of eight years, at which time its expected salvage value is zero; however, after 4 years, its

53

54

55

56

57

58

I J K

Now, we see that the decision being made is whether to purchase the equipment at a net cost of $250,000 (with annual

payments of $78,868) or lease the equipment and make annual payments of $70,000. To make this decision, we must

analyze the incremental cash flows.

59

60

61

62

63

64

65

66

67

68

69

70

71

72

73

74

75

76

77

81

82

83

84

85

86

87

88

89

94

95

96

97

98

I J K

Before proceeding with our NPV analysis we must determine the schedule of depreciation charges for this new

equipment.

We can now construct our table of incremental cash flows from these two alternatives. Remember, that the

appropriate discount rate in this scenario is the after tax cost of borrowing, or: 10%*(1–40%) = 6%.

Our NPV Analysis has told us that there is a negative advantage to leasing. We interpret that as an indication that the

firm should forego the opportunity to lease and buy the new equipment.

99

100

101

102

103

104

105

106

107

108

109

110

111

112

113

114

115

116

117

118

119

123

124

125

126

127

134

135

136

I J K

All cash flows would remain unchanged except that of the salvage value. Our new array of cash flows would resemble the

We will use the Goal Seek function to determine the lease payment that makes the Net Advantage to Leasing zero.

c. Assuming that the after-tax cost of debt should be used to discount all anticipated cash flows, at what lease

payment would the firm be indifferent to either leasing or buying?

b. The salvage value is clearly the most uncertain cash flow in the analysis. Assume that the appropriate salvage

value pre–tax discount rate is 15 percent. What would be the effect of a salvage value risk adjustment on the

decision?