Solution 7/16/2015

Chapter: 16

Problem: 18

Input Data

Collections during month of sale 15%

Collections during month after sale 65%

Collections during second month after sale 20%

Lease payments $5,000

Target cash balance $40,000

General and administrative salaries $15,000

Depreciation charges $7,500

Sales, labor, and RM adjustment factor 0%

a. Prepare a monthly cash budget for the last six months of the year.

Rusty Spears, CEO of Rusty’s Renovations, a custom building and repair company, is preparing

documentation for a line of credit request from his commercial banker. Among the required documents is a

detailed sales forecast for parts of 2014 and 2015.

Estimates obtained from the credit and collection department are as follows: collections within the month of

sale, 15%; collections during the month following the sale, 65%; collections the second month following the

sale, 20%. Payments for labor and raw materials are typically made during the month following the one in

which these costs were incurred. Total costs for labor and raw materials are estimated for each month as

General and administrative salaries will amount to approximately $15,000 a month; lease payments under

long-term lease contracts will be $5,000 a month; depreciation charges will be $7,500 a month; miscellaneous

expenses will be $2,000 a month; income tax payments of $25,000 will be due in both September and

December; and a progress payment of $80,000 on a new office suite must be paid in October. Cash on hand

on July 1 will amount to $60,000, and a minimum cash balance of $40,000 will be maintained throughout the

Note: When the percent collected

during the second month after sale

is changed, the percent for

collections during month after sale

is automatically changed so that

100% of sales are collected during

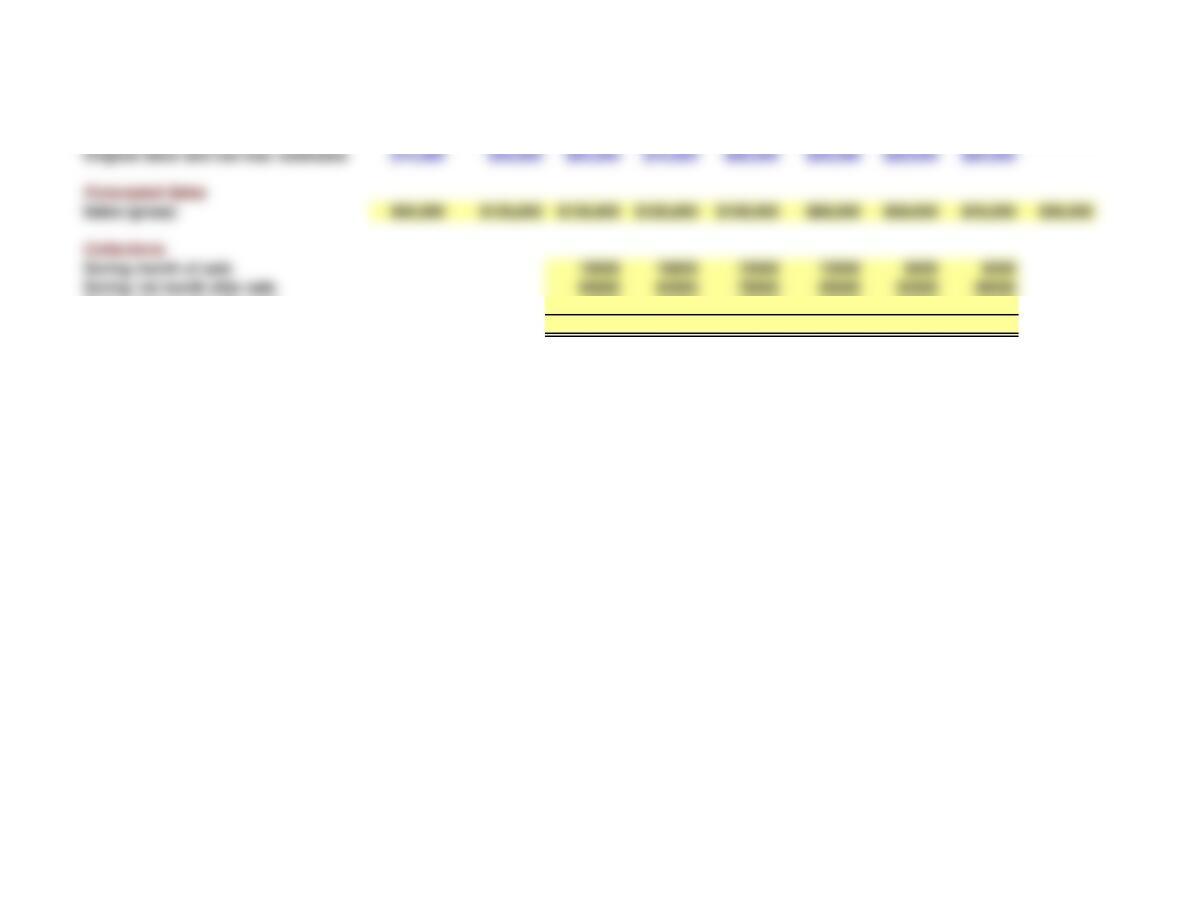

May June July August September October November December January

Original sales estimates $60,000 $100,000 $130,000 $120,000 $100,000 $80,000 $60,000 $40,000 $30,000

Original labor and raw mat. estimates $75,000 $90,000 $95,000 $70,000 $60,000 $50,000 $20,000 $20,000

Forecasted Sales

Sales (gross) $60,000 $100,000 $130,000 $120,000 $100,000 $80,000 $60,000 $40,000 $30,000

Collections

During month of sale 19500 18000 15000 12000 9000 6000

During 1st month after sale 65000 84500 78000 65000 52000 39000

During 2nd month after sale 12000 20000 26000 24000 20000 16000

Total collections $96,500 $122,500 $119,000 $101,000 $81,000 $61,000

Purchases

Labor and raw materials $75,000 $90,000 $95,000 $70,000 $60,000 $50,000 $20,000 $20,000

Payments for labor and raw materials $90,000 $95,000 $70,000 $60,000 $50,000 $20,000

Payments

Payments for labor and raw materials 90,000 95,000 70,000 60,000 50,000 20,000

General and administrative salaries 15,000 15,000 15,000 15,000 15,000 15,000

Lease payments 5,000 5,000 5,000 5,000 5,000 5,000

Miscellaneous expenses 2,000 2,000 2,000 2,000 2,000 2,000

Income tax payments 25,000 25,000

Total payments $112,000 $117,000 $117,000 $162,000 $72,000 $67,000

Net cash flow (NCF): Total collections – Total payments ($15,500) $5,500 $2,000 ($61,000) $9,000 ($6,000)

Cumulative NCF: Prior month cumulative + this month’s NCF $44,500 $50,000 $52,000 ($9,000) ($0) ($6,000)

Cash Surplus (or Loan Requirement)

Target cash balance $40,000 $40,000 $40,000 $40,000 $40,000 $40,000

Surplus cash or loan needed: Cum NCF – Target cash $4,500 $10,000 $12,000 ($49,000) ($40,000) ($46,000)

Max. Loan $49,000

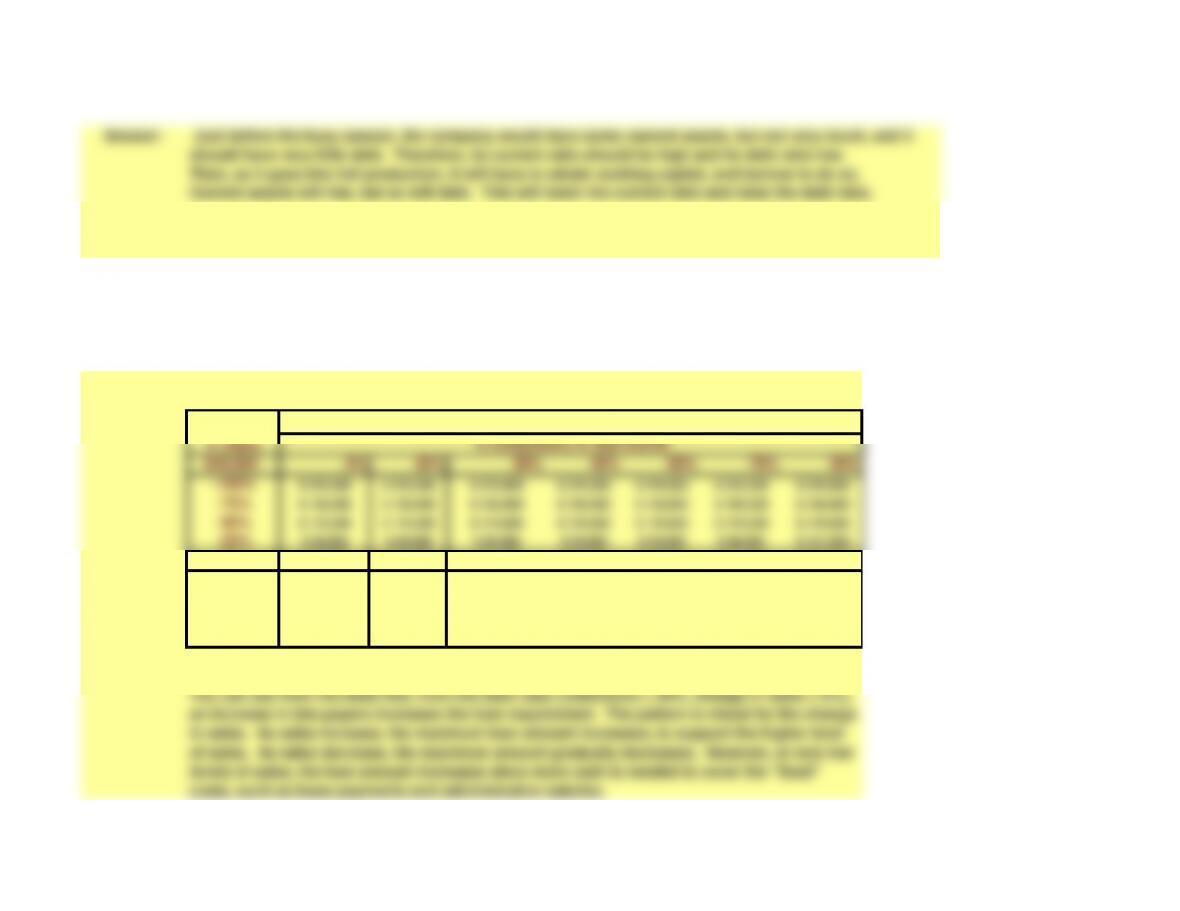

Answer: No. In the first month, only a little of the cash would have come in by the 5th, but all of the payments

would have to be made. There would be a big cash shortfall. To solve the problem, we would need a

daily cash budget.

d. If the company operates on a seasonal basis, how would this affect the current ratio and the debt ratio?

Answer: Just before the busy season, the company would have some current assets, but not very much, and it

should have very little debt. Therefore, its current ratio should be high and its debt ratio low.

Then, as it goes into full production, it will have to obtain working capital, and borrow to do so.

Current assets will rise, but so will debt. This will lower the current ratio and raise the debt ratio.

Although the company will look better at certain times of the year than at others, lenders will

Answer: The “Sales adjustment factor” can be used to cause sales to vary from the base levels. Similarly, we

can change the percentage of late paying customers. Here is the relevant data table:

Change

in Sales

$49,000 0% 20% 30% 45% 60% 75% 90%

-100% $ 242,000 $ 242,000 $ 242,000 $ 242,000 $ 242,000 $ 242,000 $ 242,000

-75% $ 193,000 $ 193,000 $ 193,000 $ 193,000 $ 193,000 $ 193,000 $ 193,000

-50% $ 144,000 $ 144,000 $ 144,000 $ 144,000 $ 144,000 $ 144,000 $ 144,000

-25% $ 95,000 $ 95,000 $ 95,000 $ 95,000 $ 95,000 $ 96,500 $ 101,000

0% $ 46,000 $ 49,000 $ 53,000 $ 59,000 $ 65,000 $ 71,000 $ 77,000

25% $ 8,000 $ 18,000 $ 23,000 $ 30,500 $ 38,000 $ 45,500 $ 53,000

50% -$ 19,750 -$ 7,750 -$ 1,750 $ 7,250 $ 16,250 $ 30,750 $ 46,500

75% -$ 23,375 -$ 9,375 -$ 2,375 $ 8,125 $ 18,625 $ 31,875 $ 50,250

100% -$ 27,000 -$ 11,000 -$ 3,000 $ 9,000 $ 21,000 $ 33,000 $ 54,000

You can see from the table that, from the base case (collections = 20%, change in sales = 0%),

an increase in late payers increases the loan requirement. The pattern is mixed for the change

in sales. As sales increase, the maximum loan amount increases, to support the higher level

of sales. As sales decrease, the maximum amount gradually decreases. However, at very low

levels of sales, the loan amount increases since more cash is needed to cover the “fixed”

costs, such as lease payments and administrative salaries.

Maximum Loan Required

% Collections in 2nd month

of these two factors on the max loan requirement. Assume the purchases of labor and raw material also vary by the

sales adjustment factor.