1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

A B C D E F G H I

Solution

Chapter:

8

Problem:

8

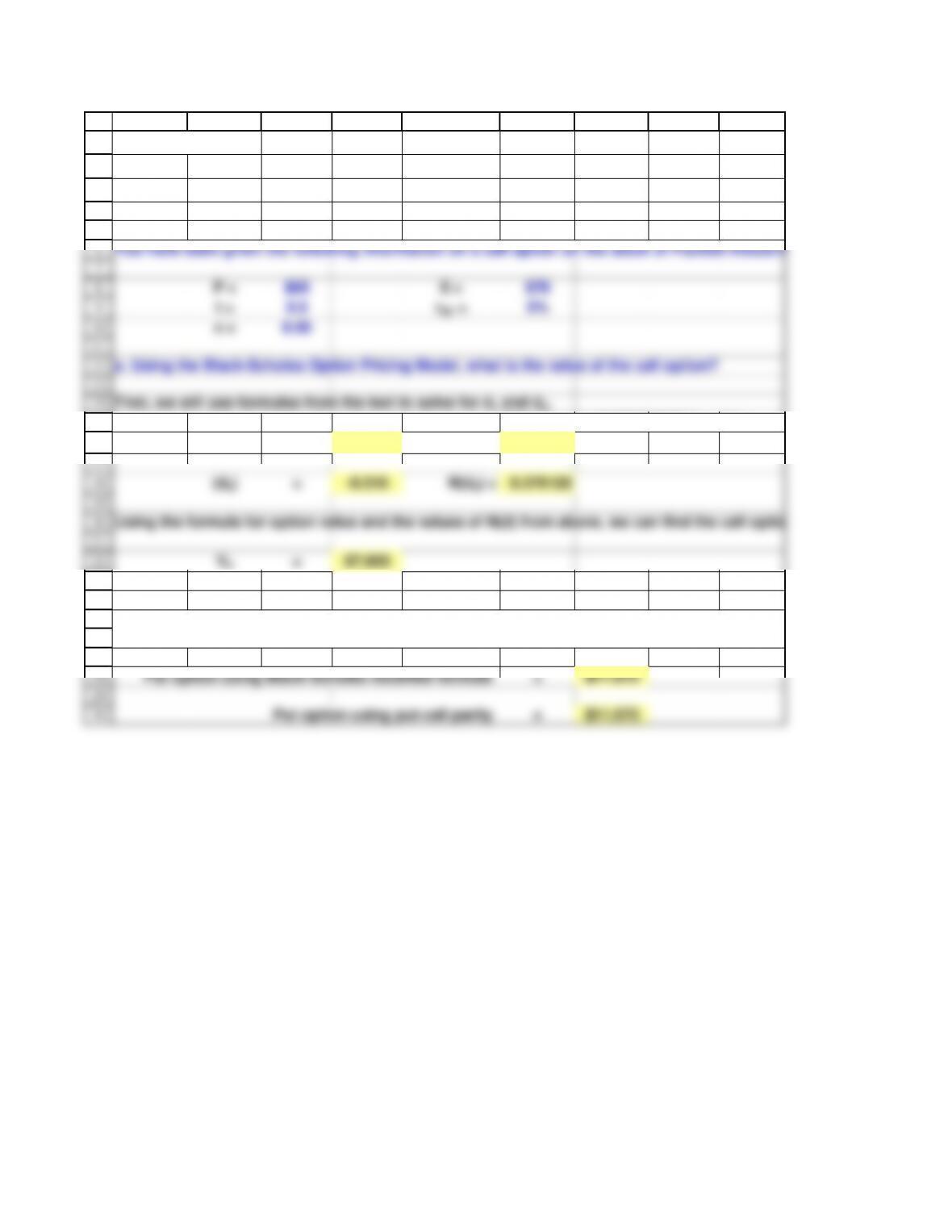

You have been given the following information on a call option on the stock of Puckett Industries:

P = $65 X = $70

t = 0.5

rRF = 5%

s = 0.50

a. Using the Black-Scholes Option Pricing Model, what is the value of the call option?

First, we will use formulas from the text to solve for d1 and d2.

Hint: use the NORMSDIST function.

(d1) = 0.038 N(d1) = 0.515108

(d2) = -0.316 N(d2) = 0.376125

Using the formula for option value and the values of N(d) from above, we can find the call option value.

VC= $7.803

Put option using Black-Scholes modified formula = $11.075

Put option using put-call parity = $11.075

b. Suppose there is a put option on Puckett’s stock with exactly the same inputs as the call option. What is

the value of the put?

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

29

30

J

7/16/2015

You have been given the following information on a call option on the stock of Puckett Industries:

Using the formula for option value and the values of N(d) from above, we can find the call option value.

b. Suppose there is a put option on Puckett‘s stock with exactly the same inputs as the call option. What is

the value of the put?