Critical Thinking Cases

8.1 Jun Hsieh’s Insurance Decision: Whole Life, Variable Life, or Term Life?

Jun Hsieh, a 38-year-old widowed mother of three children (ages 12, 10, and 4), works as a

product analyst for Panama Hats. Although she’s covered by a group life insurance policy

at work, she feels, based on some rough calculations, that she needs additional protection.

Phil Griffin, an insurance agent from Safety First Insurance, has been trying to persuade

Jun to buy a $150,000, 25-year, limited payment whole life policy. However, Jun favors a

variable life policy. To further complicate matters, Jun’s father feels that term life

insurance is more suitable to the needs of her young family.

Critical Thinking Questions

1. Explain to Jun the differences between (a) a whole life policy, (b) a variable life policy,

and (c) a term life policy.

a. Three major types of whole life policies are available: continuous premium, limited payment,

and single premium.

Under a continuous premium whole life policy—or straight life, as it’s more commonly called—

With a limited payment whole life policy, you’re covered for your entire life, but the premium

payment is based on a specified period—for example, so-called 20-pay life and 30-pay life

A single premium whole life policy is purchased with one cash premium payment at the inception

b. A variable life insurance policy goes further than whole and universal life policies in

combining death benefits and savings. The policyholder decides how to invest the money in the

savings (cash-value) component. The investment accounts are set up just like mutual funds, and

c. term life insurance is insurance that provides only death benefits, for a specified period, and

2. What are the major advantages and disadvantages of each type of policy?

Whole life: Advantages include the ability to have insurance protection your entire life

regardless of your insurability in later years, Ability to borrow against the cash value of the

policy with repayment deferred until death, and Ability to purchase “paid-up at year 20” policies

Variable life: If you want the benefits of higher investment returns, then you must also be

Term life: The advantages is that you get the most insurance for the premium dollar. The

3. In what way is a whole life policy superior to either a variable life or term life policy? In

what way is a variable life policy superior? How about term life insurance?

Whole life gives a set amount of insurance that will not be cancelled as long as premiums are

paid. It will build some cash value and you may be able to borrow that cash value. With

4. Given the limited information in the case, which type of policy would you recommend for

Ms. Hsieh? Defend and explain your recommendations.

In 25 years Ms. Hsieh will have no one depending on her for resources. The youngest child will

be 29 and should be on their own. Ms. Hsieh will be 63 and approaching retirement. Her need

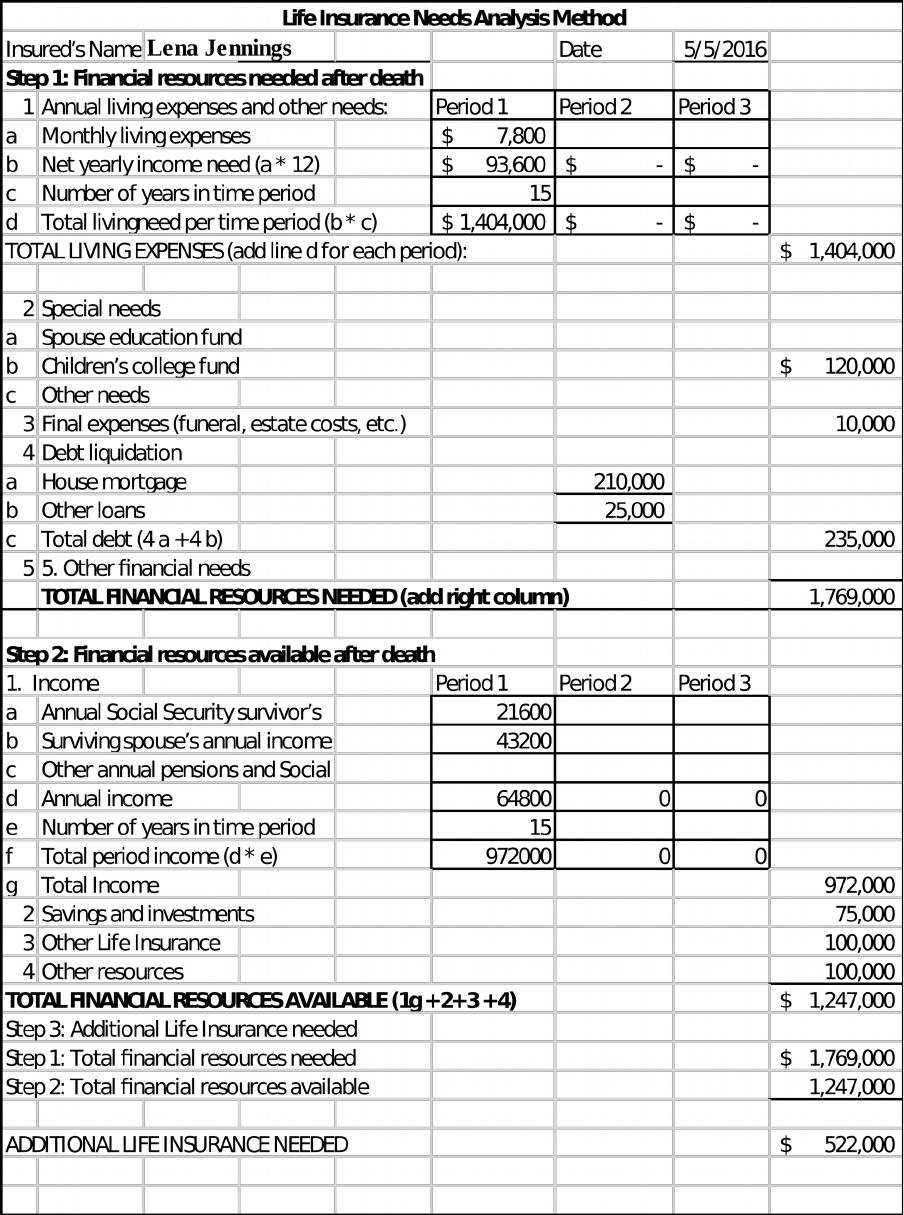

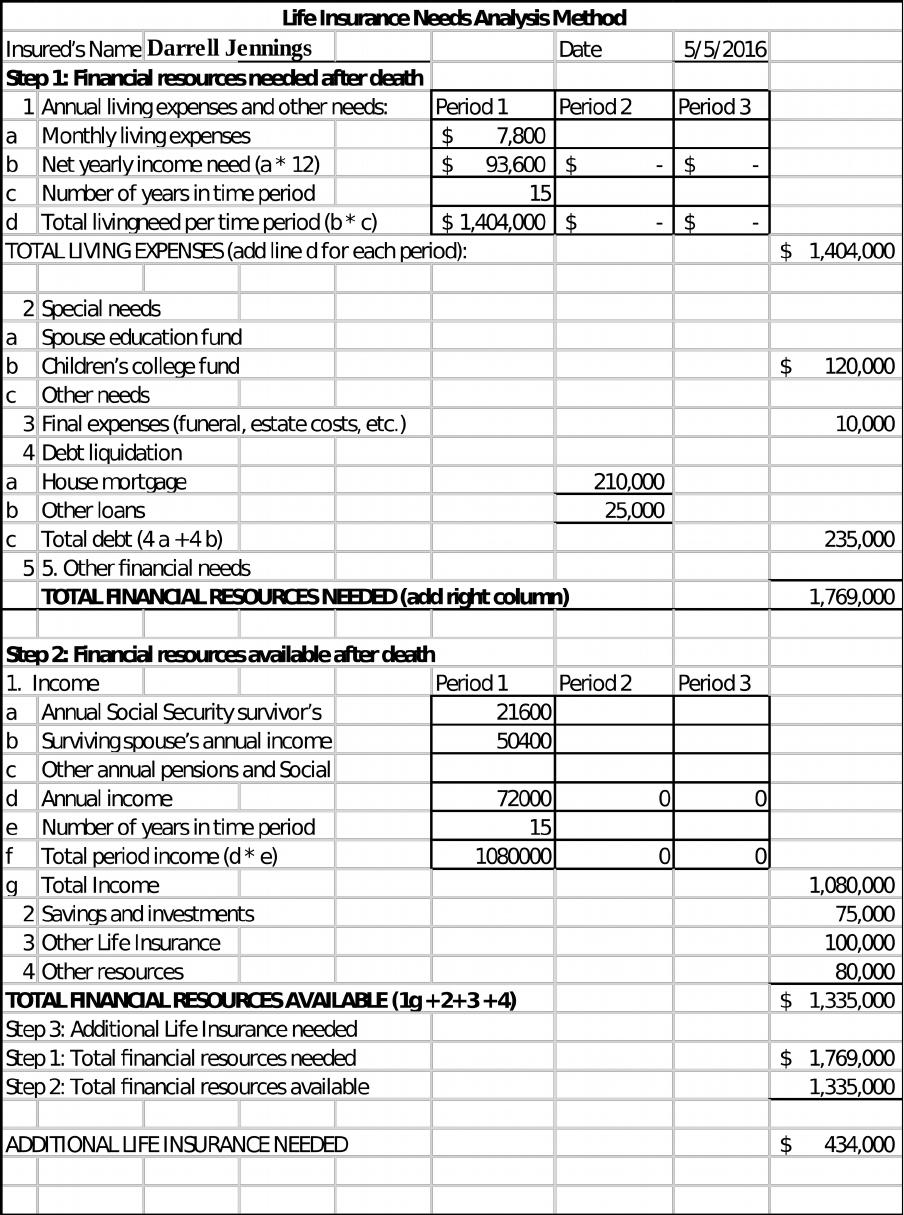

8.2 The Jennings Want to Know: How Much Is Enough?

Darrell and Lena Jennings are a two-income couple in their early 30s. They have two

children, ages 6 and 3. Darrell’s monthly take-home pay is $3,600, and Lena’s is $4,200.

The Jennings feel that, because they’re a two-income family, they both should have

adequate life insurance coverage. Accordingly, they are now trying to decide how much life

insurance each one of them needs.

To begin with, they’d like to set up an education fund for their children in the amount of

$120,000 to provide college funds of $15,000 a year—in today’s dollars—for four years for

each child. Moreover, if either spouse should die, they want the surviving spouse to have the

funds to pay off all outstanding debts, including the $210,000 mortgage on their house.

They estimate that they have $25,000 in consumer installment loans and credit cards. They

also project that if either of them dies, the other probably will be left with about $10,000 in

final estate and burial expenses.

Regarding their annual income needs, Darrell and Lena both feel strongly that each should

have enough insurance to replace her or his respective current income level until the

youngest child turns 18 (a period of 15 years). Although neither Darrell nor Lena would be

eligible for Social Security survivor’s benefits because they both intend to continue

working, both children would qualify in the (combined) amount of around $1,800 a month.

The Jennings have amassed about $75,000 in investments, and they have a decreasing term

life policy on each other in the amount of $100,000, which could be used to partially pay off

the mortgage. Darrell also has an $80,000 group policy at work and Lena a $100,000 group

policy.

Critical Thinking Questions

1. Assume that Darrell’s gross annual income is $54,000 and Lena’s is $64,000. Their

insurance agent has given them a multiple earnings table showing that the earnings

multiple to replace 75 percent of their lost earnings is 8.7 for Jacob and 7.4 for Lena. Use

this approach to find the amount of life insurance each should have if they want to replace

75 percent of their lost earnings.

Using the earnings multiple calculation, the Jennings’ insurance needs are:

2. Use Worksheet 8.1 to find the additional insurance needed on both Darrell’s and Lena’s

lives. (Because Darrell and Lena hold secure, well-paying jobs, both agree that they won’t

need any additional help once the kids are grown; both also agree that they’ll have plenty

of income from Social Security and company pension benefits to take care of themselves in

retirement. Thus, when preparing the worksheet, assume “funding needs” of zero in

Periods 2 and 3.)

The worksheets are below. One assumption is that the decreasing term that they each have pays

The worksheet results suggest that Darrell needs to have insurance on his life of $434,000, which

3. Is there a difference in your answers to Questions 1 and 2? If so, why? Which number do

you think is more indicative of the Jennings’ life insurance needs? Using the amounts

computed in Question 2 (employing the needs approach), what kind of life insurance policy

would you recommend for Darrell? For Lena? Briefly explain your answers.

One difference is that the earnings multiple calculation is designed to replace 75% of the lost

income. In the Worksheet analysis, the assumption is that 100% of the income is needed. Also,

The insurance needs are for a specific period of 15 years, until the children completes college.

After that time, they believe that their income and retirement income will be sufficient and they

Terms Found in the Chapter

beneficiary A person who receives the death benefits of a life insurance policy after

the insured’s death.

disability clause A clause in a life insurance contract containing a waiver-of-premium

benefit alone or coupled with disability income.

cash value The accumulated refundable value of an insurance policy; results from

the investment earnings on paid-in insurance premiums.

convertibility A term life policy provision allowing the insured to convert the policy

to a comparable whole life policy.

credit life

insurance

Life insurance sold in conjunction with installment loans.

decreasing term

policy

A term insurance policy that maintains a level premium throughout all

periods of coverage while the amount of protection decreases.

guaranteed

purchase option

An option in a life insurance contract giving the policyholder the right

to purchase additional coverage at stipulated intervals without

providing evidence of insurability.

group life

insurance

Life insurance that provides a master policy for a group; each eligible

group member receives a certificate of insurance.

industrial life

insurance (home

service life

insurance)

Whole life insurance issued in policies with relatively small face

amounts, often $1,000 or less.

insurance policy A contract between the insured and the insurer under which the insurer

agrees to reimburse the insured for any losses suffered according to

specified terms.

life insurance

policy

illustration

A hypothetical representation of a life insurance policy’s performance

that reflects the most important assumptions that the insurance

company relies on when presenting the policy results to a prospective

client.

loss control Any activity that lessens the severity of loss once it occurs.

loss prevention Any activity that reduces the probability that a loss will occur.

mortgage life

insurance

A term policy designed to pay off the mortgage balance in the event of

the borrower’s death.

multiple indemnity

clause

A clause in a life insurance policy that typically doubles or triples the

policy’s face amount if the insured dies in an accident.

multiple-of-

earnings

method

A method of determining the amount of life insurance coverage needed

by multiplying gross annual earnings by some selected number.

needs analysis

method

A method of determining the amount of life insurance coverage needed

by considering a person’s financial obligations and available financial

resources in addition to life insurance.

nonforfeiture right A life insurance feature giving the whole life policyholder, upon policy

cancellation, the portion of those assets that were set aside to provide

payment for the future death claim.

participating policy A life insurance policy that pays policy dividends reflecting the

difference between the premiums that are charged and the amount of

premium necessary to fund the actual mortality experience of the

company.

policy loan An advance, secured by the cash value of a whole life insurance policy,

made by an insurer to the policyholder.

renewability A term life policy provision allowing the insured to renew the policy at

the end of its term without having to show evidence of insurability.

risk assumption The choice to accept and bear the risk of loss.

risk avoidance Avoiding an act that would create a risk.

Social Security

survivor’s benefits

Benefits under Social Security intended to provide basic, minimum

support to families faced with the loss of a principal wage earner.

straight term

policy

A term insurance policy written for a given number of years, with

coverage remaining unchanged throughout the effective period.

term life insurance

.

Insurance that provides only death benefits, for a specified period, and

does not provide for the accumulation of cash value

underwriting The process used by insurers to decide who can be insured and to

determine applicable rates that will be charged for premiums.

universal life

insurance

Permanent cash-value insurance that combines term insurance (death

benefits) with a tax-sheltered savings/ investment account that pays

interest, usually at competitive money market rates.

variable life

insurance

Life insurance in which the benefits are a function of the returns being

generated on the investments selected by the policyholder.

whole life

insurance

Life insurance designed to offer ongoing insurance coverage over the

course of an insured’s entire life.

Insuring Your Life

Chapter Outline

Learning Goals

I. Basic Insurance Concepts

A. The Concept of Risk

1. Risk Avoidance

2. Loss Prevention and Control

3. Risk Assumption

4. Insurance

B. Underwriting Basics

*Test Yourself*

II. Why Buy Life Insurance?

A. Benefits of Life Insurance

B. Do You Need Life Insurance?

*Test Yourself*

III. How Much Life Insurance is Right for You?

A. Step 1: Assess Your Family’s Total Economic Needs

B. Step 2: Determine What Financial Resources Will Be Available After Death

C. Step 3: Subtract Resources from Needs to Calculate How Much Life Insurance

You Require

D. Needs Analysis in Action: The Meese Family

1. Financial Resources Needed After Death (Step 1)

2. Financial Resources Available After Death (Step 2)

3. Additional Life Insurance Needed (Step 3)

E. Life Insurance Underwriting Considerations

*Test Yourself*

IV. What Kind of Policy is Right for You?

A. Term Life Insurance

1. Types of Term Insurance

a. Straight Term

b. Decreasing Term

2. Advantages and Disadvantages of Term Life

3. Who Should Buy Term Insurance?

B. Whole Life Insurance

1. Types of Whole Life Policies

a. Continuous Premium

b. Limited Payment

c. Single Premium

2. Advantages and Disadvantages of Whole Life

3. Who Should Buy Whole Life Insurance?

C. Universal Life Insurance

1. Advantages and Disadvantages of Universal Life

2. Who Should Buy Universal Life Insurance?

D. Other Types of Life Insurance

1. Variable Life Insurance

2. Group Life Insurance

3. Other Special-Purpose Life Policies

*Test Yourself*

V. Buying Life Insurance

A. Compare Costs and Features

B. Select an Insurance Company

C. Choose an Agent

*Test Yourself*

VI. Key Features of Life Insurance Policies

A. Life Insurance Contract Features

1. Beneficiary Clause

2. Settlement Options

3. Policy Loans

4. Premium Payments

5. Grace Period

6. Nonforfeiture Options

7. Policy Reinstatement

8. Change of Policy

B. Other Policy Features

C. Understanding Life Insurance Policy Illustrations

*Test Yourself*

Summary

Financial Impact of Personal Choices

Financial Planning Exercises

Critical Thinking Cases

8.1 Jun Hsieh’s Insurance Decision: Whole Life, Variable Life, or Term Life?

8.2 The Jennings Want to Know: How Much Is Enough?

Money Online!