8-21 Explain the basic settlement options available for the payment of life insurance

proceeds upon a person’s death.

• Lump sum: This is the most common settlement option, chosen by more than 95 percent of

• Interest only: The insurance company keeps policy proceeds for a specified time; the

beneficiary receives interest payments, usually at some guaranteed rate. This option can be useful

• Fixed period: The face amount of the policy, along with interest earned, is paid to the

• Fixed amount: The beneficiary receives policy proceeds in regular payments of a fixed

• Life income: The insurer guarantees to pay the beneficiary a certain payment for the rest of his

or her life, based on the beneficiary’s sex, age when benefits start, life expectancy, policy face

value, and interest rate assumptions. This option appeals to beneficiaries who don’t want to

8-22 What do nonforfeiture options accomplish? Differentiate between paid-up insurance

and extended term insurance.

A nonforfeiture option gives a cash value life insurance policyholder some benefits even when a

Extended term insurance: The insured uses the accumulated cash value to buy a term life

With paid-up insurance, you have insurance for life. With extended term insurance, you have

8-23 Explain the following clauses often found in life insurance policies: (a) multiple indemnity

clause, (b) disability clause, and (c) suicide clause. Give some examples of common exclusions.

a. Multiple indemnity clause: Multiple indemnity clauses increase the face amount of the

b. Disability clause: A disability clause may contain a waiver-of-premium benefit alone or

c. Suicide clause: Nearly all life insurance policies have a suicide clause that voids the contract

Exclusions: Although all private insurance policies exclude some types of losses, life policies

8-24 Describe what is meant by a participating policy, and explain the role of policy dividends in

these policies.

In a participating policy, the policyholder is entitled to receive policy dividends reflecting the

8-25 Describe the key elements of an insurance policy illustration and explain what a

prospective client should focus on in evaluating an illustration.

A life insurance policy illustration is a hypothetical representation of a policy’s performance

that reflects the most important assumptions that the company relies on when presenting the

When you look at an insurance illustration, focus first on the basic assumptions that the company

used to compute it, including your age, sex, and underwriting health status. Check to make sure

Financial Planning Exercises

Planning Exercises

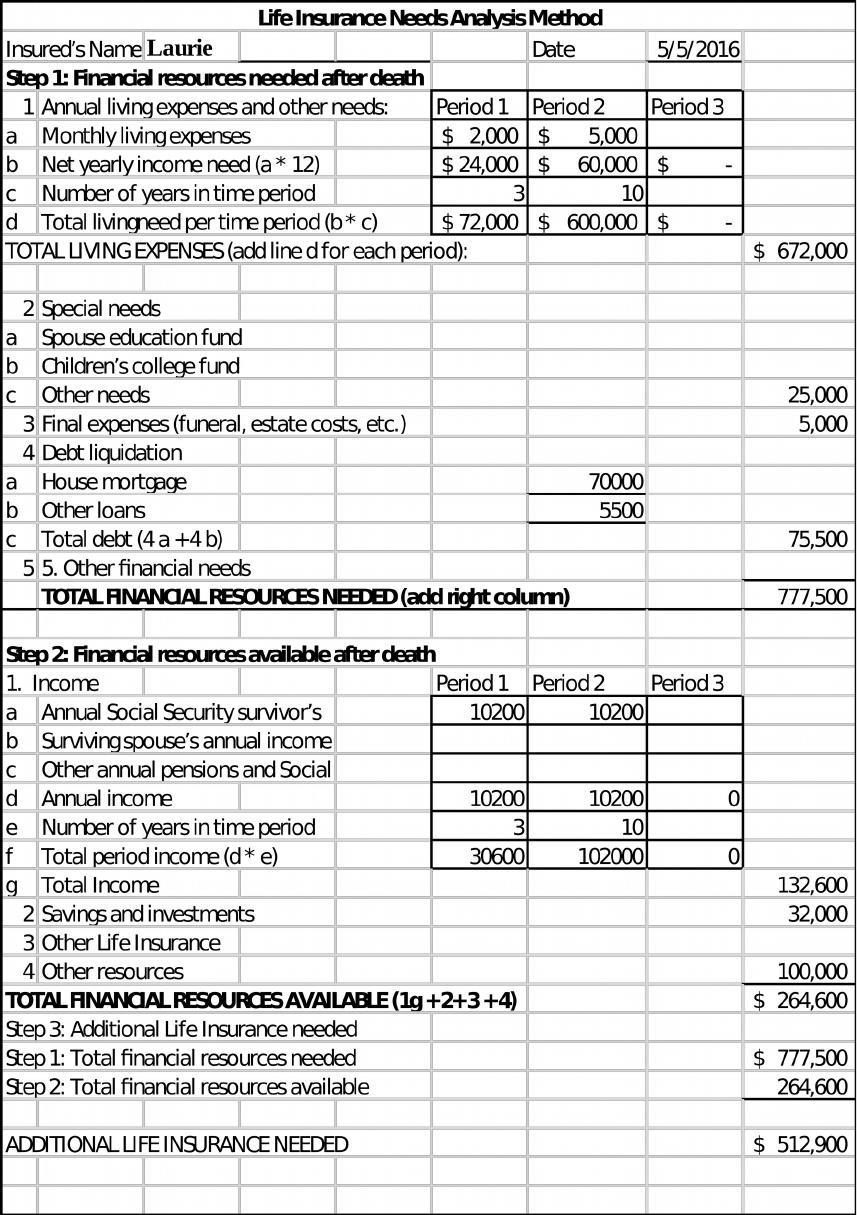

1. Estimating life insurance needs. Use Worksheet 8.1. Katie Holt is a 72-year-old widow who

has recently been diagnosed with Alzheimer’s disease. She has limited financial assets of

her own and has been living with her daughter Laurie for two years. Her only income is

$850 a month in Social Security survivor’s benefits. Laurie wants to make sure her mother

will be taken care of if Laurie should die. Laurie, 40, is single and earns $55,000 a year as a

human resources manager for a small manufacturing firm. She owns a condo with a

current market value of $100,000 and has a $70,000 mortgage. Other debts include a $5,000

auto loan and $500 in various credit card balances. Her 401(k) plan has a current balance

of $24,500, and she keeps $7,500 in a money market account for emergencies. After talking

with her mother’s doctor, Laurie believes that her mother will be able to continue living

independently for another two to three years. She estimates that her mother would need

about $2,000 a month to cover her living expenses and medical costs during this time. After

that, Laurie’s mother will probably need nursing home care. Laurie calls several local

nursing homes and finds that it will cost about $5,000 a month when her mother enters a

nursing home. Her mother’s doctor says it is difficult to estimate her mother’s life

expectancy but indicates that with proper care some Alzheimer’s patients can live 10 or

more years after diagnosis. Laurie also estimates that her personal final expenses would be

around $5,000, and she’d like to provide a $25,000 contingency fund that would be used to

pay a trusted friend to supervise her mother’s care if Laurie were no longer alive. Use

Worksheet 8.1 to calculate Laurie’s total life insurance requirements and recommend the

type of policy that she should buy.

Laurie is concerned that she should die and leave her mother not able to get the care she needs.

While it is difficult to estimate lives, Laurie believes that her mother will live no more than 13

additional years. At Laurie’s death, Katie [Mother] will only have her social security which does

Given Laurie’s middle age and the need for insurance of only an additional 13 years, Laurie

If Laurie does not die, she will have to find funds to cover her mother’s costs. Perhaps the

mother will qualify for Medicaid given her Alzheimer’s disease. With a salary of $55,000,

2. Deciding if life insurance is needed. Use Worksheet 8.1. Given your current personal

financial situation, do you feel you need life insurance coverage? Why or why not? Use

Worksheet 8.1 to confirm your answer and calculate how much additional insurance (if

any) you might need to purchase.

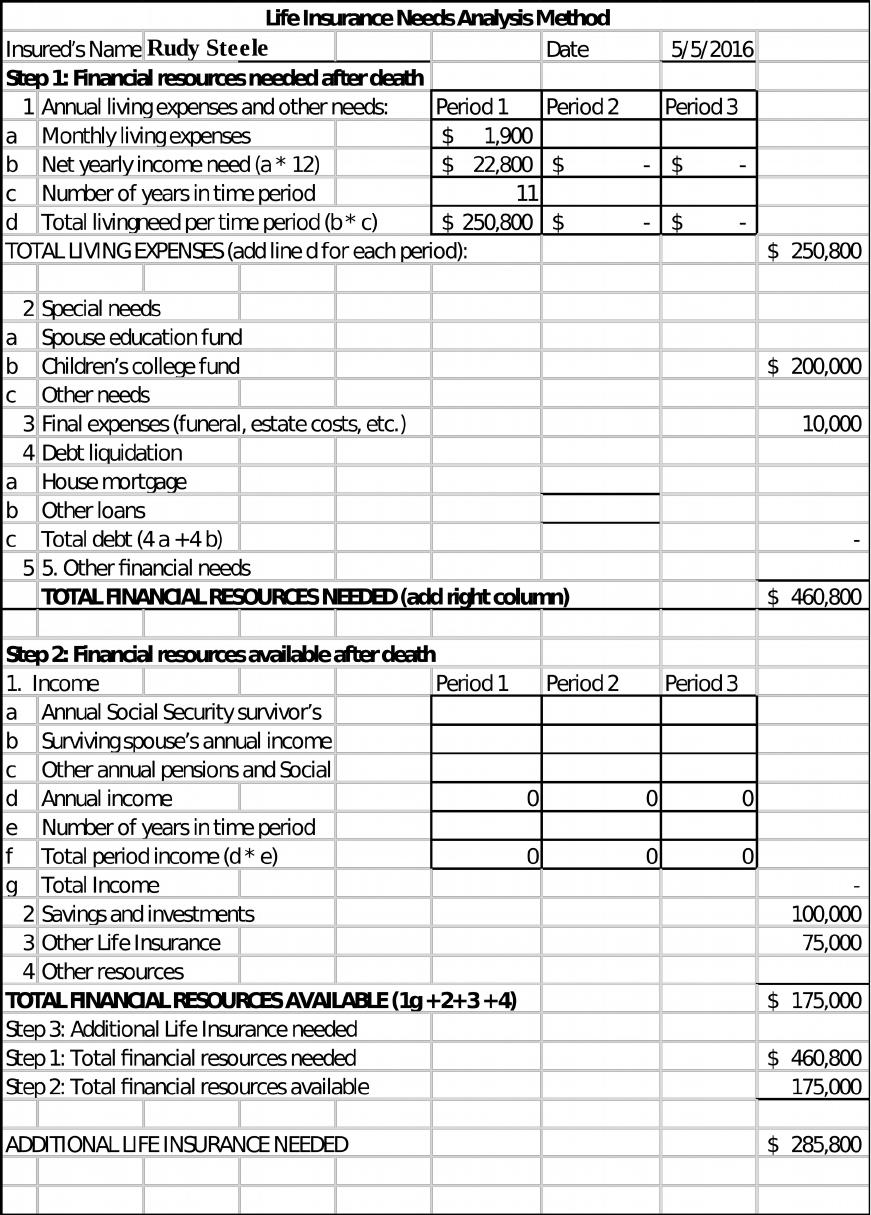

3. Deciding if additional life insurance is needed and, if so, appropriate type. Use Worksheet

8.1. Rudy Steele, 43, is a recently divorced father of two children, ages 9 and 7. He

currently earns $95,000 a year as an operations manager for a utility company. The divorce

settlement requires him to pay $1,500 a month in child support and $400 a month in

alimony to his ex-wife, who currently earns $25,000 annually as a preschool teacher. Rudy

is now renting an apartment, and the divorce settlement left him with about $100,000 in

savings and retirement benefits. His employer provides a $75,000 life insurance policy.

Rudy’s ex-wife is currently the beneficiary listed on the policy. What advice would you give

to Rudy? What factors should he consider in deciding whether to buy additional life

insurance at this point in his life? If he does need additional life insurance, what type of

policy or policies should he buy? Use Worksheet 8.1 to help answer these questions for

Rudy.

Divorce is always a difficult situation, especially with children involved. Rudy has to decide the

level of support he wishes to give his children. I he wants to provide a college fund for his kids,

Assuming $200,000 college fund and funeral expenses of $10,000, Rudy needs insurance of

Given his age, I would suggest term insurance. Since the major expense will be at the end of the

4. Life insurance premiums and comparison of types. Using the premium schedules

provided in Exhibits 8.2, 8.3, and 8.5, how much in annual premiums would a 25-year-old

male have to pay for $100,000 of annual renewable term, level premium term, and whole

life insurance? (Assume a five-year term or period of coverage.) How much would a 25-

year-old woman have to pay for the same coverage? Consider a 40-year-old male (or

female): Using annual premiums, compare the cost of 10 years of coverage under annual

renewable and level premium term options and whole life insurance coverage. Relate the

advantages and disadvantages of each policy type to their price differences.

Policy is $100,000, for 10 years

Insured Annual renewable term Level premium term Whole life insurance

25-yr male $97 * 5 + $107 * 5 =

$1,020

$106* 10 = $1,060 $603 * 5 + $727 * 5

= $6,650

25-yr female $63 * 5 + $88 * 5 =

$755

$102* 10 = $1,020 $525 * 5 + $683 * 5

= $6,040

$1,725

I did not interpolate to estimate the yearly premium for the annual renewable term or the whole

The premiums demonstrate that, in general, rates for men are higher than for women of the same

age; that premiums increase with age; and that term insurance is far less expensive than whole

life. The annual renewable term is the lowest cost for the 25-yr olds and the level term for the 40-

5. Appropriateness of whole life insurance. Ramona and Pablo Valdez are a dual-career

couple who just had their first child. Pablo age 29, already has a group life insurance

policy, but Ramona’s employer does not offer life insurance. A financial planner is

recommending that the 25-year-old Ramona buy a $250,000 whole life policy with an

annual premium of $1,670 (the policy has an assumed rate of earnings of 5 percent a year).

Help Ramona evaluate this advice and decide on an appropriate course of action.

Issues are the need for insurance and then what type of insurance best meet that need. We do not

know the amount of Pablo’s insurance. Frequently employer provided group life insurance is

The second issue is what type of insurance. For younger couples, term insurance is normally

preferred versus whole life. Using the table is Exhibit 8.3, the premium for 20 year level

premium term life of $100,000 for a female is $116, thus, for $250,000 the premium would be

My advice to Ramona is to first determine the need for insurance. Once the amount is

Note the Financial Impact of Personal Choices, Matt and Jan Consider

“Buying Term and Investing the Rest” that is at the end of the chapter.

[Above in these materials.]

6. Appropriateness of variable life insurance. While at lunch with a group of coworkers,

one of your friends mentions that he plans to buy a variable life insurance policy because it

provides a good annual return and is a good way to build savings for his 5-year-old’s

college education. Another colleague says that she’s adding coverage through the group

plan’s additional insurance option. What advice would you give them?

A variable life insurance policy goes further than whole and universal life policies in combining

death benefits and savings. The policyholder decides how to invest the money in the savings

(cash-value) component. The investment accounts are set up just like mutual funds, and most

The friend is mixing investment and insurance. If the goal is to build an education fund, then the

funds need to be investment in stocks or mutual funds, securities that will build in value over the

If you want the benefits of higher investment returns, then you must also be willing to assume