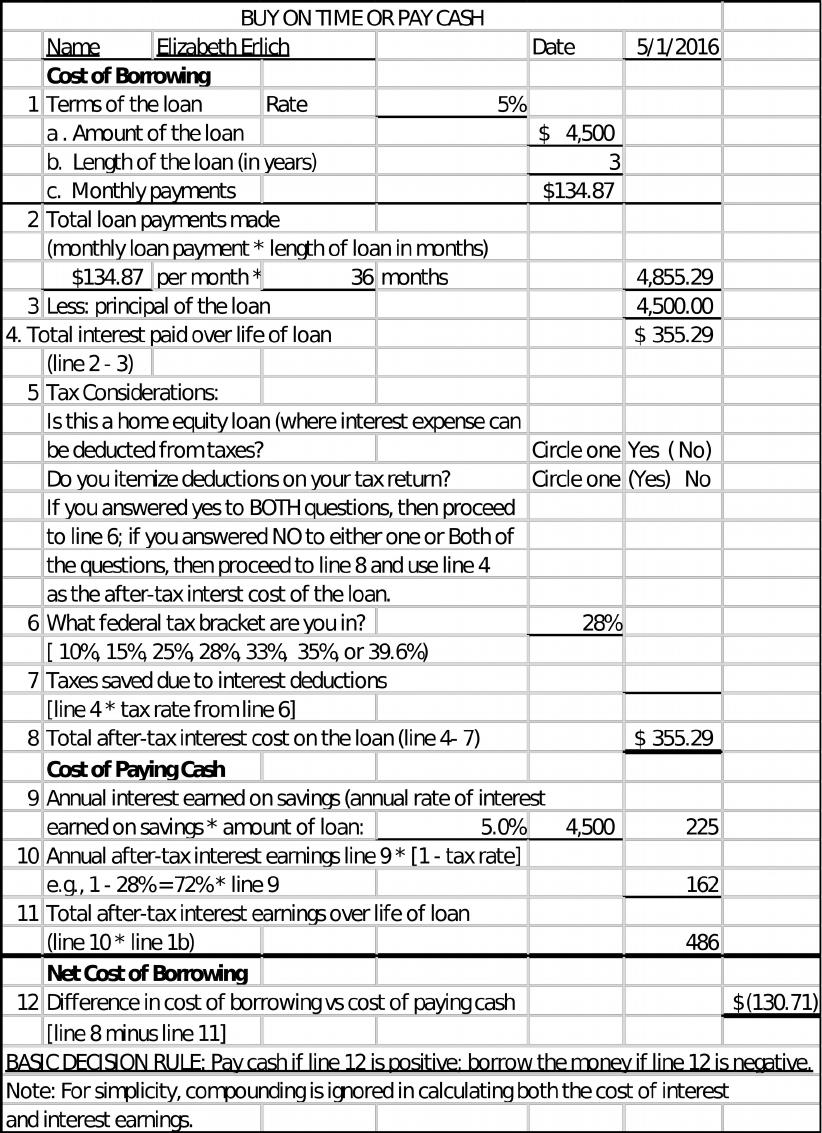

13. Deciding whether to pay cash or finance a purchase. Use Worksheet 7.2. Elizabeth Erlich

wants to buy a home entertainment center. Complete with a big-screen TV, DVD, and

sound system, the unit would cost $4,500. Elizabeth has over $15,000 in a money fund, so

she can easily afford to pay cash for the whole thing (the fund is currently paying 5 percent

interest, and Constance expects that yield to hold for the foreseeable future). To stimulate

sales, the dealer is offering to finance the full cost of the unit with a 36-month installment

loan at 5 percent, simple. Elizabeth wants to know: Should she pay cash for this home

entertainment center or buy it on time? (Note: Assume Elizabeth is in the 28 percent tax

bracket and that she itemizes deductions on her tax returns.) Briefly explain your answer.

a. Should she pay cash for the entertainment center?

Using the decision rule of Worksheet 7.2, she should borrow the $4,500. If she uses her money

fund, she will lose interest on the entire $4,500. By borrowing, the principal of the loan will

To help manage her funds, she can set up an automatic withdrawal from the money fund to her

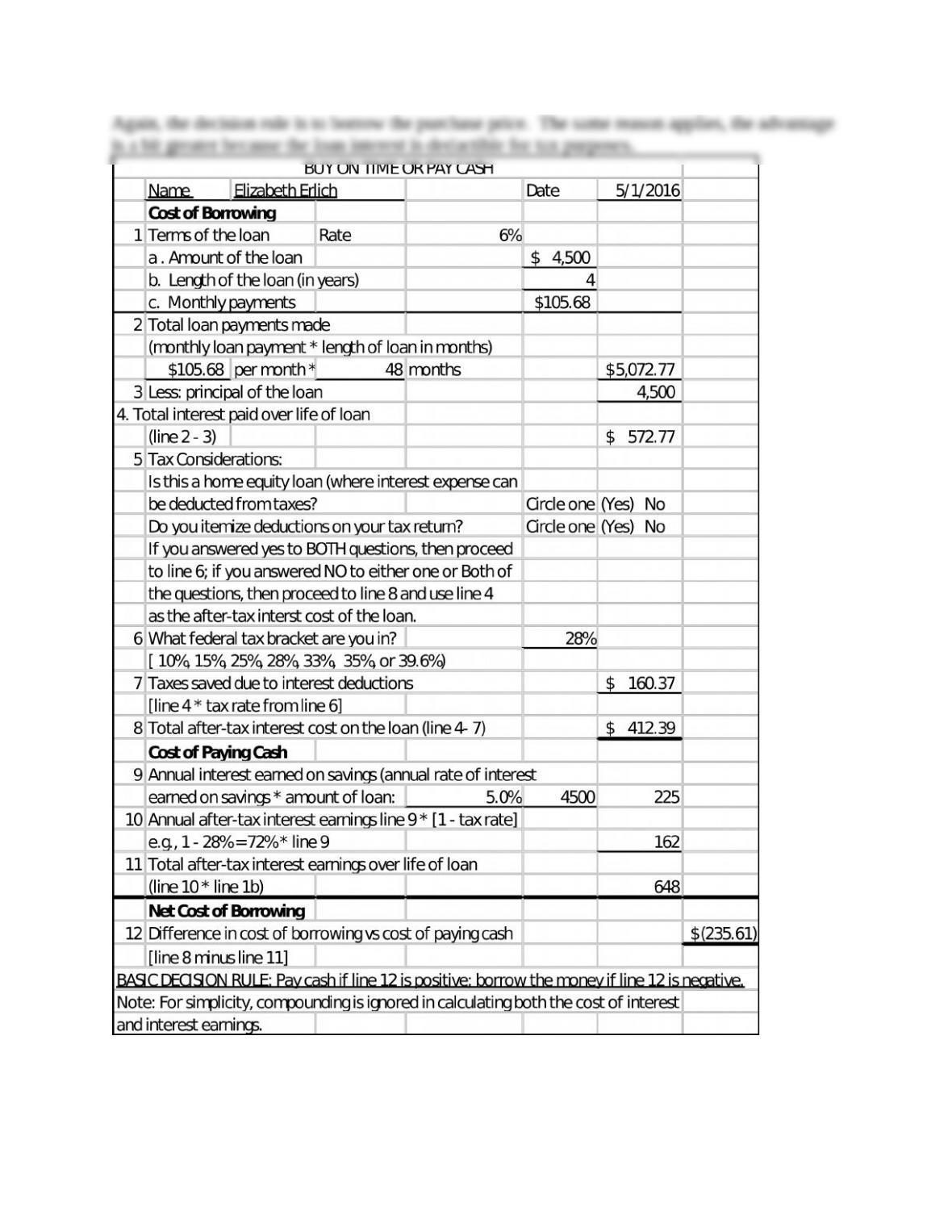

b. Rework the problem, assuming that Elizabeth has the option of using a 48-month, 6

percent home equity loan to finance the full cost of this entertainment center. Again, use

Worksheet 7.2 to determine if Elizabeth should pay cash or buy on time. Does your answer

change from the one you came up with in part (a)? Explain.

14. Comparing payments and APRs of financing alternatives. Because of a job change, Ben

Hardesty has just relocated to the southeastern United States. He sold his furniture before

he moved, so he’s now shopping for new furnishings. At a local furniture store, he’s found

an assortment of couches, chairs, tables, and beds that he thinks would look great in his

new two-bedroom apartment; the total cost for everything is $6,400. Because of moving

costs, Ben is a bit short of cash right now, so he’s decided to take out an installment loan for

$6,400 to pay for the furniture. The furniture store offers to lend him the money for 48

months at an add-on interest rate of 6.5 percent. The credit union at Ben’s firm also offers

to lend him the money—they’ll give him the loan at an interest rate of 6 percent simple, but

only for a term of 24 months.

a. Compute the monthly payments for both of the loan offers.

From Furniture store: $6,400 * .065 = 416 annual add-on interest; total cost $6,400 + (4 *416)

= $8,064. Divide by 48 months, equals monthly payment of $168.

From Credit Union: Monthly payment using financial calculator,

b. Determine the APR for both loans.

The APR for the loan from the furniture store can be calculated with the financial calculator,

because the time value of money equations programmed into the financial calculator use the

simple interest method, which yields the APR. Set your calculator on End Mode and 12

payments/year.

The credit union is using simple interest, thus, the APR is the simple interest rate of 6%.

c. Which is more important: low payments or a low APR? Explain.

Low APR is more important. With loans, it is all about the APR and your ability to make

payments.

Critical Thinking Cases

7.1 Financing Zoe’s Education

At age 19, Zoe Trainor is in the middle of her second year of studies at a community college

in Charlotte. She has done well in her course work; majoring in pre-business studies, she

currently has a 3.75 grade point average. Zoe lives at home and works part-time as a filing

clerk for a nearby electronics distributor. Her parents can’t afford to pay any of her tuition

and college expenses, so she’s virtually on her own as far as college goes. Zoe plans to

transfer to the University of Tennessee [Go Vols!] next year. (She has already been

accepted.) After talking with her counselor, Zoe feels she won’t be able to hold down a part-

time job and still manage to complete her bachelor’s degree program at UT in two years.

Knowing that on her 22nd birthday, she will receive approximately $35,000 from a trust

fund left her by her grandmother, Zoe has decided to borrow against the trust fund to

support herself during the next two years. She estimates that she’ll need $25,000 to cover

tuition, room and board, books and supplies, travel, personal expenditures, and so on

during that period. Unable to qualify for any special loan programs, Zoe has found two

sources of single-payment loans, each requiring a security interest in the trust proceeds as

collateral. The terms required by each potential lender are as follows:

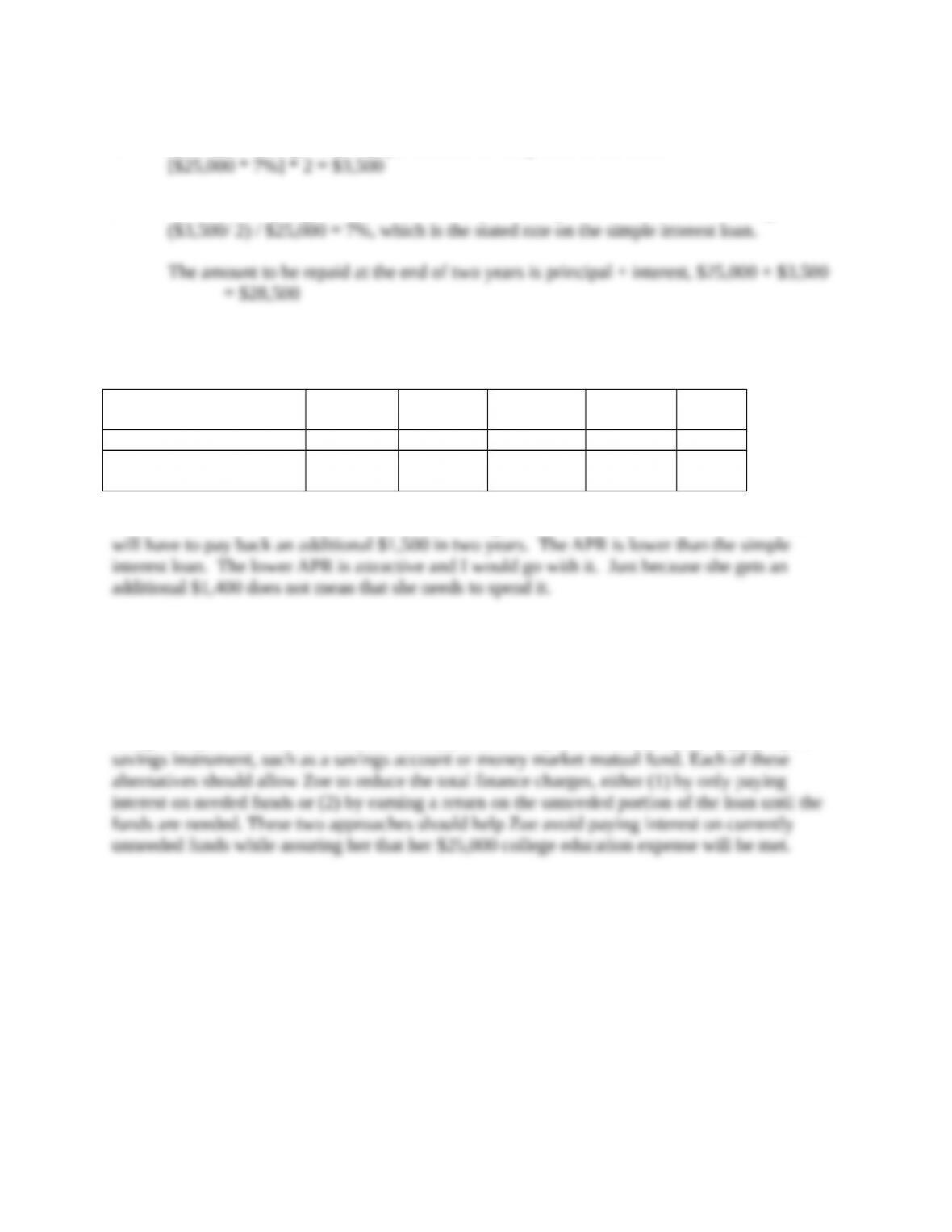

a. Tennessee State Bank will lend $30,000 at 6 percent discount interest. The loan principal

would be due at the end of two years.

b. National Bank of Knoxville will lend $25,000 under a two-year note. The note would

carry a 7 percent simple interest rate and would also be due in a single payment at the end

of two years.

Critical Thinking Questions

1. How much would Zoe (a) receive in initial loan proceeds and (b) be required to repay at

maturity under the Tennessee State Bank loan?

2. Compute (a) the finance charges and (b) the APR on the loan offered by Tennessee State

Bank.

a. The finance charges are the amount of discount, $3,600.

3. Compute (a) the finance charges and (b) the APR on the loan offered by the National

Bank of Knoxville. How big a loan payment would be due at the end of two years?

a. The finance charge is the simple interest for the period of the loan.

b. The APR is Average Annual Finance charge / Average Loan Balance Outstanding =

4. Compare your findings in Questions 2 and 3, and recommend one of the loans to Zoe.

Explain your recommendation.

Method

Stated

Rate

Finance

Charge

Amount

Received

Amount

Repaid APR

a. Discount loan 6% $3,600 $26,400 $30,000 6.8%

b. Simple interest

loan

7% $3,500 $25,000 $28,500 7%

The discount loan from Tennessee State Bank will give her an additional $1,400 now and she

5. What other recommendations might you offer Zoe regarding disposition of the loan

proceeds?

Since Zoe plans to spend the $25,000 over the following two years, she should either (1) try to

arrange a line of credit in which she can draw the money as needed, with the interest being

charged only as the funds are disbursed, or (2) immediately invest the funds in a highly liquid

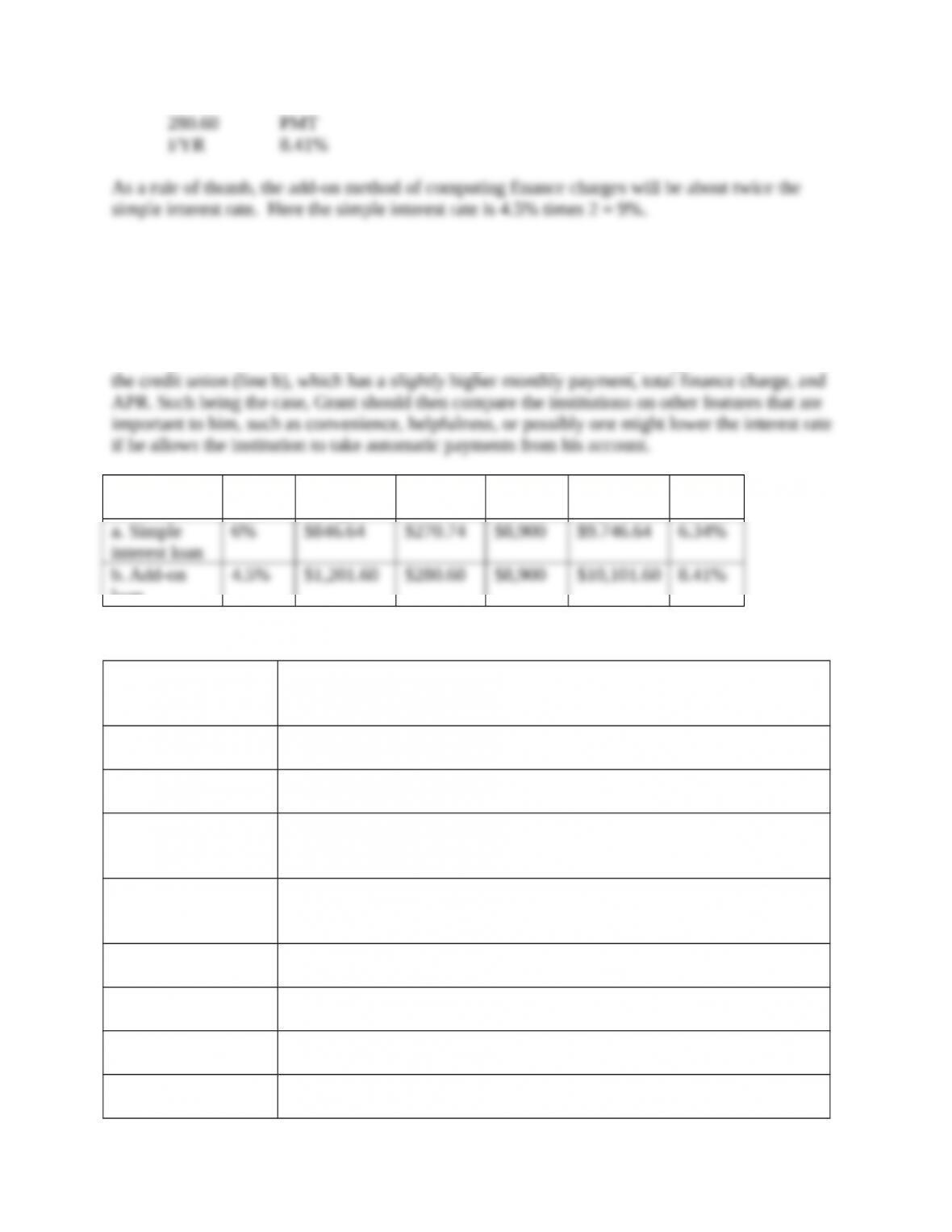

7.2 Grant Gets His Outback

Grant Tyson, a 27-year-old bachelor living in Arlington, Virginia, has been a high-school

teacher for five years. For the past four months, he’s been thinking about buying a Subaru

Outback, but he feels that he can’t afford a brand-new one. Recently, however, his friend

Martin Grubbs has offered to sell Grant his fully loaded Subaru Outback 3.6R. Martin

wants $26,900 for his Outback, which has been driven only 8,000 miles and is in very good

condition. Grant is eager to buy the vehicle but has only $10,000 in his savings account at

Central Bank. He expects to net $8,000 from the sale of his Chevrolet Malibu, but this will

still leave him about $8,900 short. He has two alternatives for obtaining the money:

a. Borrow $8,900 from the First National Bank of Arlington at a fixed rate of 6 percent per

annum, simple interest. The loan would be repaid in equal monthly installments over a

three-year (36-month) period.

b. Obtain a $8,900 installment loan requiring 36 monthly payments from the Arlington

Teacher’s Credit Union at a 4.5 percent stated rate of interest. The add-on method would

be used to calculate the finance charges on this loan.

Critical Thinking Questions

1. Using Exhibit 7.6 or a financial calculator, determine the required monthly payments if

the loan is taken out at First National Bank of Arlington.

Monthly payments using this method are calculated with the financial calculator as follows. Set

your calculator on End Mode and 12 payments/year.

8,900 +/- PV From Exhibit 7.6

2. Compute (a) the finance charges and (b) the APR on the loan offered by First National

Bank of Arlington.

3. Determine the size of the monthly payment required on the loan from the Arlington

Teacher’s Credit Union.

(Principal + interest ) / 36,

4. Compute (a) the finance charges and (b) the APR on the loan offered by the Arlington

Teacher’s Credit Union.

5. Compare the two loans and recommend one of them to Grant. Explain your

recommendation.

The following table summarizes the key characteristics of the two loans. Comparing the monthly

payment, total finance charges, and APR on the two loans, it’s clear that while the two loans are

about equal, the one from First National of Arlington (line a) has a slight edge over the one from

Method

Stated

Rate

Finance

Charge

Monthly

Pmt.

Amount

Rec’d.

Amount

Repaid APR

loan

Terms Found in the Chapter

529 college savings

plan

A government-sponsored investment vehicle that allows earnings to

grow free from federal taxes, so long as they are used to meet college

education expenses.

add-on method A method of calculating interest by computing finance charges on the

original loan balance and then adding the interest to that balance.

cash value (of life

insurance)

An accumulation of savings in an insurance policy that can be used as a

source of loan collateral.

captive finance

company

A sales finance company that is owned by a manufacturer of big-ticket

merchandise. GMAC is a captive finance company.

chattel mortgage A mortgage on personal property given as security for the payment of

an obligation.

collateral note A legal note giving the lender the right to sell collateral if the borrower

defaults on the obligation.

consumer finance

company

A firm that makes secured and unsecured personal loans to qualified

individuals; also called a small loan company.

consumer loans Loans made for specific purposes using formally negotiated contracts

that specify the borrowing terms and repayment.

credit life (or

disability)

A type of life (or disability) insurance in which the coverage decreases

at the same rate as the loan balance.

insurance

discount method A method of calculating finance charges in which interest is computed

and then subtracted from the principal, with the remainder being

disbursed to the borrower.

installment loan A loan that is repaid in a series of fixed, scheduled payments rather

than a lump sum.

interim financing The use of a single payment loan to finance a purchase or pay bills in

situations where the funds to be used for repayment are known to be

forthcoming in the near future.

lien A legal claim permitting the lender, in case the borrower defaults, to

liquidate the items serving as collateral to satisfy the obligation.

loan application An application that gives a lender information about the purpose of the

loan as well as the applicant’s financial condition.

loan disclosure

statement

A document, which lenders are required to supply borrowers, that

states both the dollar amount of finance charges and the APR

applicable to a loan.

loan rollover The process of paying off a loan by taking out another loan.

prepayment

penalty

An additional charge you may owe if you decide to pay off your loan

prior to maturity.

Rule of 78s (sum-of

the-digits method)

A method of calculating interest that has extra-heavy interest charges in

the early months of the loan.

sales finance

company

A firm that purchases notes drawn up by sellers of certain types of

merchandise, typically big-ticket items.

simple interest

method

A method of computing finance charges in which interest is charged on

the actual loan balance outstanding.

single-payment

loan

A loan made for a specified period, at the end of which payment is due

in full.

Using Consumer Loans

Chapter Outline

Learning Goals

I. Basic Features of Consumer Loans

A. Using Consumer Loans

B. Di3erent Types of Loans

1. Student Loans

a. Obtaining a Student Loan

b. Are Student Loans “Too Big to Fail”?

c. Strategies for Reducing Student Loan Costs

2. Single-Payment or Installment Loans

3. Fixed- or Variable-Rate Loans

C. Where Can You Get Consumer Loans?

1. Commercial Banks

2. Consumer Finance Companies

3. Credit Unions

4. S&L Associations

5. Sales Finance Companies

6. Life Insurance Companies

7. Friends and Relatives

*Test Yourself*

II. Managing Your Credit

A. Shopping for Loans

1. Finance Charges

2. Loan Maturity

3. Total Cost of the Transaction

4. Collateral

5. Other Loan Considerations

B. Keeping Track of Your Consumer Debt

*Test Yourself*

III. Single-Payment Loans

A. Important Loan Features

1. Loan Collateral

2. Loan Maturity

3. Loan Repayment

B. Finance Charges and the Annual Percentage Rate

1. Simple Interest Method

2. Discount Method

*Test Yourself*

IV. Installment Loans

A. A Real Consumer Credit Workhorse

B. Finance Charges, Monthly Payments, and the APR

1. Using Simple Interest

2. Add-on Method

3. Prepayment Penalties

4. Credit Life Insurance

C. Buy on Time or Pay Cash?

*Test Yourself*

Summary

Financial Planning Exercises

Applying Personal Finance

Making the Payments!

Critical Thinking Cases

7.1 Financing Zoe’s Education

7.2 Grant Gets His Outback

Money Online!