Financial Planning Exercises

1. Student loan options. Marilyn Seacrest is a sophomore at State College and is running

out of money. Wanting to continue her education, Marilyn is considering a student loan.

Explain her options. How can she minimize her borrowing costs and maximize her

flexibility?

Exhibit 7.1 gives basic information on the type of student loans available. It’s important to

borrow as little as possible to cover college costs. This common-sense goal can be quantified by

borrowing in light of the student’s expected future salary. Based on that expected future salary,

figure out what monthly payment the student will be able to afford and then use a loan repayment

calculator to determine the maximum amount that can be borrowed at the expected interest rate

2. Evaluating finance packages. Assume that you’ve been shopping for a new car and

intend to finance part of it through an installment loan. The car you’re looking for has a

sticker price of $18,000. The local dealership has offered to sell it to you for $3,000 down

and finance the balance with a loan that will require 48 monthly payments of $333.67;

Adventure Vehicles will sell you the exact same vehicle for $3,500 down, plus a 60-month

loan for the balance, with monthly payments of $265.02.

Which of these two finance packages is the better deal? Explain.

The analysis should look at the total cost of the loan.

Local dealer: $3,000 down plus 48*$333.67; total payments of $19,016.16.

So the total cost of Local dealer is less. But the difference is not great. Adventure Vehicles has a

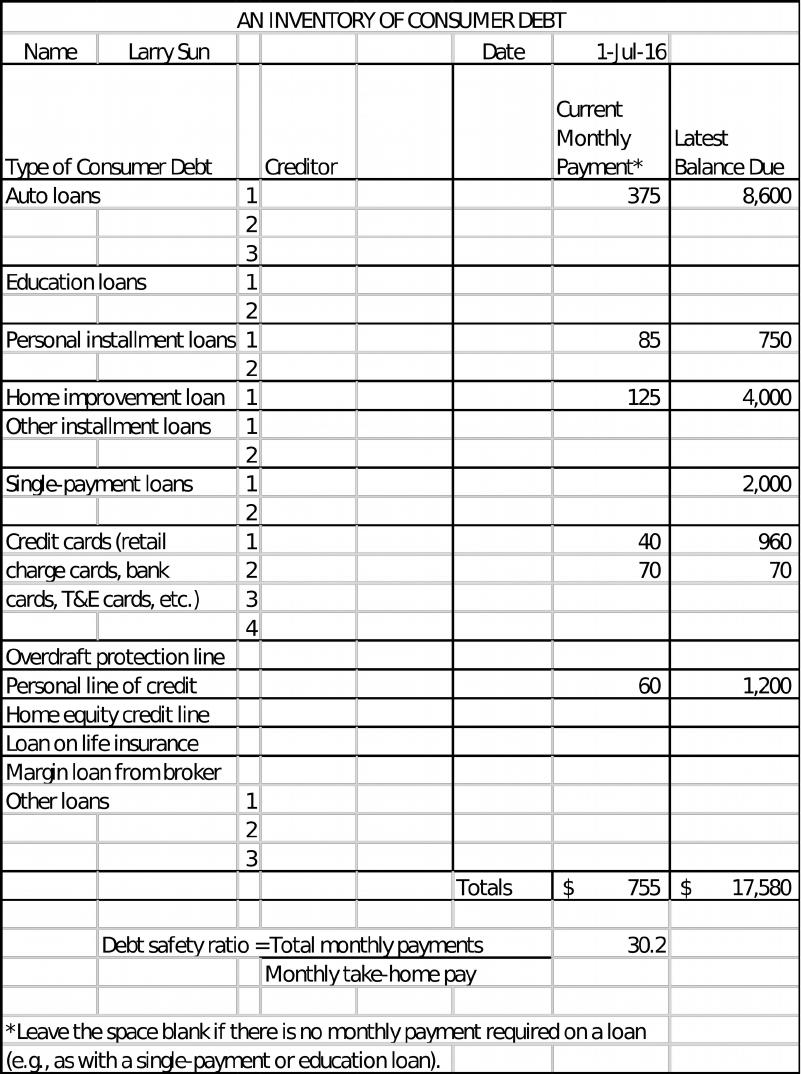

3. Calculating debt safety ratio. Use Worksheet 7.1. Every six months, Larry Sun takes an

inventory of the consumer debts that he has outstanding. His latest tally shows that he still

owes $4,000 on a home improvement loan (monthly payments of $125); he is making $85

monthly payments on a personal loan with a remaining balance of $750; he has a $2,000,

secured, single-payment loan that’s due late next year; he has a $70,000 home mortgage on

which he’s making $750 monthly payments; he still owes $8,600 on a new car loan (monthly

payments of $375); and he has a $960 balance on his MasterCard (minimum payment of

$40), a $70 balance on his Exxon credit card (balance due in 30 days), and a $1,200 balance

on a personal line of credit ($60 monthly payments). Use Worksheet 7.1 to prepare an

inventory of Larry’s consumer debt. Find his debt safety ratio given that his take-home pay

is $2,500 per month. Would you consider this ratio to be good or bad? Explain.

A useful credit guideline (and one widely used by lenders) is to make sure your monthly

repayment burden doesn’t exceed 20 percent of your monthly take-home pay. Most experts,

however, regard the 20 percent figure as the maximum debt burden and strongly recommend a

From Worksheet 7.1 below, Larry’s debt safety ratio is 30.2% which is over the desired

4. Calculating single payment loan amount due at maturity. Jim Grant plans to borrow

$8,000 for five years. The loan will be repaid with a single payment after five years, and the

interest on the loan will be computed using the simple interest method at an annual rate of

6 percent. How much will Jim have to pay in five years? How much will he have to pay at

maturity if he’s required to make annual interest payments at the end of each year?

$8,000 * (1.06)^5 = $10,705.80

$8,000 + .06*8000*5 = $10,400 over the life of the loan. The final payment would be the

principal plus one year’s interest, $8,000 + (.06*8,000) = $10,480

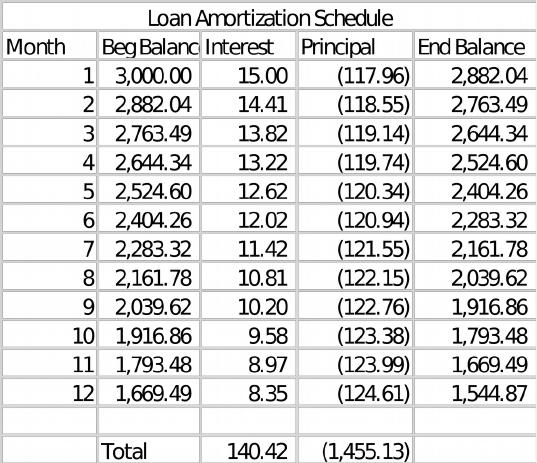

5. Calculating monthly installment loan payments. Using the simple interest method, find

the monthly payments on a $3,000 installment loan if the funds are borrowed for 24 months

at an annual interest rate of 6 percent. How much interest will be paid during the first year

of this loan? (Use a monthly payment analysis similar to the one in Exhibit 7.7.)

Computation of the monthly payment amount:

Using the financial calculator: Using Excel:

3,000+/- PV PMT = (.06/12,24,3000) = $132.96

24 N

6 I

PMT $132.96

Total interest paid first year $140.42.

6. Calculating the APR on simple interest and discount loans. Find the finance charges on a

6.5 percent, 18-month, single-payment loan when interest is computed using the simple

interest method. Find the finance charges on the same loan when interest is computed using

the discount method. Determine the APR in each case.

Using the simple interest method, the finance charges on a 6.5 %, 18-month single-payment loan

would be:

Finance charge = Principal × 6.5% × 1.5 years

= $1,000 × 0.065 × 1.5

= $97.50

Using the discount method, the finance charge is the same dollar amount as that obtained with

the simple interest method. However, the finance charges are subtracted first from the amount

requested, and then the borrower receives what’s left, or the proceeds. Using the same setup as in

the example above:

Amount requested – interest = loan proceeds received

$1,000 – $97.50 = $902.50

The real difference between these two loans is shown when you compute the APR:

Average annual finance charge

Average loan balance outstanding

APR for the simple interest method is calculated by dividing the finance charge by the life of the

loan and then dividing this annual charge by the loan balance ($1,000 in our example).

APR = ($97.50/1.5) = $65 = 6.5%

$1000 $1,000

The APR for the discount method is found in a similar manner:

APR = ($97.50/1.5) = $65 = 7.2%

$1,000 – $112.50 $902.50

7. Comparing the costs of single-payment discount and simple interest loans. Chris Jenkins

needs to borrow $4,000. First State Bank will lend her the money for 12 months through a

single-payment loan at 8 percent, discount; Home Savings and Loan will make her a

$4,000, single-payment, 12-month loan at 10 percent, simple interest. From where should

Kristin borrow the money? Explain.

First State Bank: $4,000 * 8% = $320 interest; net proceeds $4,000 – 320 = $3,680

APR = $320 / $3,680 = 8.7%

Home Savings and Loan: $4,000 * 10% = $400 interest; proceeds = $4,000

APR = $400 / $4,000 = 10%

First State Bank is the better loan—lower interest rate.

8. Todd Kowalski is borrowing $10,000 for five years at 7 percent. Payments are made on a

monthly basis, which are determined using the add-on method.

a. How much total interest will Chris pay on the loan if it is held for the full five-year term?

Add-on = $10,000 * 7% * 5 years = $3,500, the total interest.

b. What are Chris’s monthly payments?

Principal + interest = total payments, divided by 60 months = monthly payment

$10,000 + $3,500 = $13.500 / 60 = $225.00 per month.

c. How much higher are the monthly payments under the add-on method than under the

simple interest method?

Using simple interest, payments using Exhibit 7.6 for 7% over 60 months is $19.80 per thousand,

or $198 for $10,000. Thus, add-on payments are $27 per month [$225 – $198] higher than

simple interest.

9. Calculating interest and APR of installment loan. Assuming that interest is the only

finance charge, how much interest would be paid on a $5,000 installment loan to be repaid

in 36 monthly installments of $166.10? What is the APR on this loan?

Using a financial calculator: 5,000 + PV APR Annual rate, 12. 0119%

36 N APR Monthly rate .120119/12 = 1.001%

$166.10 PMT

I/YR 12.0119

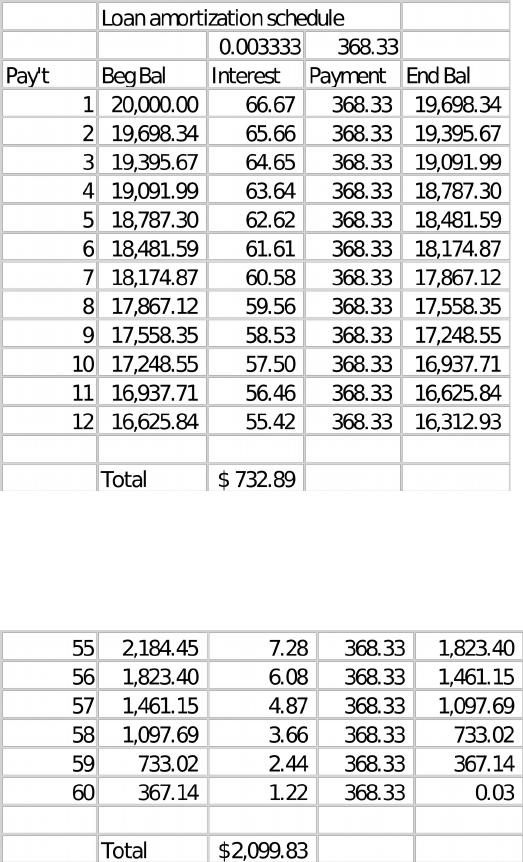

10. Calculating payments, interest, and APR on auto loan. After careful comparison

shopping, Bill Withers decides to buy a new Toyota Camry. With some options added, the

car has a price of $23,558—including plates and taxes. Because he can’t afford to pay cash

for the car, he will use some savings and his old car as a trade-in to put down $8,500. He

plans to finance the rest with a $20,000, 60-month loan at a simple interest rate of 4

percent.

a. What will his monthly payments be?

With Excel: PMT = (.04/12,60,20000) = $368.33

With Financial Calculator:

Set on End Mode and 12 payments/year:

20,000 +/- PV

60 N

4.0 I/YR

PMT $368.33

b. How much total interest will Bill pay in the first year of the loan? (Use a monthly

payment analysis procedure similar to the one in Exhibit 7.6.)

c. How much interest will Bill pay over the full (60-month) life of the loan?

[$368.33 * 60] = $22,099.80 – 20,000 = $2,099.80

d. What is the APR on this loan?

[(1 + .04/12)^12] − 1 = (1.0033)^12 − 1 = 1.0403 − 1 = 4.03%

The APR is 4%; the .03 is due to rounding in the computation.

11. Calculating and comparing APRs of competing financing alternatives. Lina Martinez

wants to buy a new high-end audio system for her car. The system is being sold by two

dealers in town, both of whom sell the equipment for the same price of $2,000. Lina can

buy the equipment from Dealer A, with no money down, by making payments of $119.20 a

month for 18 months; she can buy the same equipment from Dealer B by making 36

monthly payments of $69.34 (again, with no money down). Lina is considering purchasing

the system from Dealer B because of the lower payment. Find the APR for each alternative.

What do you recommend?

To solve for the APR, divide the purchase price of $2,000 by $1,000 to get 2. Then divide the

payments given by 2 and look up that amount in the Exhibit 7.6 in the column under the given

time periods. Clearly, Dealer A is offering the better deal.

Dealer A: Divide the quoted monthly payment of $119.20 by 2 to get $59.60. Look under the 18

month column to find that the APR is 9%.

Dealer B: Divide the quoted monthly payment of $69.34 by 2 to get $34.67. Look under the 36

month column to find that the APR is 15%.

You can also use the financial calculator to find the APR as shown below. Set your calculator on

End Mode and 12 payments/year. You must put in either the PV or PMT as a negative in order to

solve the problem.

Dealer

A

Dealer

B

2,000

+/-

PV 2,000

+/-

PV

119.2 PMT 69.34 PMT

18 N 36 N

I 9% I 15%

12. Calculating interest and APR of add-on loan. Sherman Jacobs plans to borrow $5,000

and to repay it in 36 monthly installments. This loan is being made at an annual add-on

interest rate of 7.5 percent.

a. Calculate the finance charge on this loan, assuming that the only component of the

finance charge is interest.

Finance Charge using Add-On Method = Principal × Rate × Time

FS = $5,000 × 0.075 × 3 = $1,125

b. Use your finding in part (a) to calculate the monthly payment on the loan.

[Principal + Interest] / time: $5,000 + $1,125 = $6,125 / 36 = $170.14

c. Using a financial calculator, determine the APR on this loan.

Use the financial calculator to find the annual percentage rate (APR) of interest on this loan. Set

your calculator on End Mode and 12 payments/year.

5,000 +/- PV

36 N

170.14 PMT

I/YR 13.69%