Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

6-13 Describe credit scoring and explain how it’s used (by lenders) in making a credit

decision.

Using the data provided by the credit applicant, along with any information obtained from the

credit bureau, the store or bank must decide whether to grant credit. Very likely, some type of

The biggest provider of credit scores is, by far, Fair Isaac & Co.—the firm that produces the

widely used FICO scores. Unlike some credit score providers, Fair Isaac uses only credit

information in its calculations. There’s nothing in them about your age, marital status, salary,

occupation, employment history, or where you live. Instead, FICO scores are derived from the

6-14 Describe the basic operations and functions of a credit bureau.

A credit bureau is a type of reporting agency that gathers and sells information about individual

borrowers. If, as is often the case, the lender doesn’t know you personally, it must rely on a cost-

effective way of verifying your employment and credit history. It would be far too expensive

6-15 What is the most common method used to compute finance charges?

According to the Truth in Lending Act, lenders disclose the rate of interest that they charge and

The amount of interest you pay for open credit depends partly on the method the lender uses to

calculate the balances on which they apply finance charges. Most bank and retail charge card

issuers use one of two variations of the average daily balance (ADB) method, which applies

• ADB, including new purchases: For each day in the billing cycle, take the outstanding

balance, including new purchases, and subtract payments and credits; then divide by the

6-16 The monthly statement is a key feature of bank and retail credit cards. What does this

statement typically disclose?

If you use a credit card, you’ll receive monthly statements similar to the sample bank card

Financial Planning Exercises

1. Establish a credit history. After graduating from college last fall, Nicole butler took a job

as a consumer credit analyst at a local bank. From her work reviewing credit applications,

she realizes that she should begin establishing her own credit history. Describe for Nicole

several steps that she could take to begin building a strong credit record. Does the fact that

she took out a student loan for her college education help or hurt her credit record?

Here are some things you can do to build a strong credit history:

• Use credit only when you can afford it and only when the repayment schedule fits comfortably

into the family budget—in short, don’t overextend yourself.

Having a student loan on which you may consistent and regular payments can help you build a

2. Evaluating debt burden. Isaac Wright has a monthly take-home pay of $1,685; he makes

payments of $410 a month on his outstanding consumer credit (excluding the mortgage on

his home). How would you characterize Isaac’s debt burden? What if his take-home pay

were $850 a month and he had monthly credit payments of $150?

The debt safety ratio is total monthly consumer credit payments divided by the monthly take-

home pay. In Isaac’s case, with monthly take-home pay of $1,685 and payments of $410, his

In Isaac’s second case, with monthly take-home pay of $850 and payments of $150, his debt

safety ratio is 150/850 = 17.6. This ratio is under the maximum of 20. It is over the preferred

3. Calculating and interpreting personal debt safety ratio. Calculate your own debt safety

ratio. What does it tell you about your current credit situation and your debt capacity?

Does this information indicate a need to make any changes in your credit use patterns? If

so, what steps should you take?

The easiest way to avoid repayment problems and ensure that your borrowing won’t place an

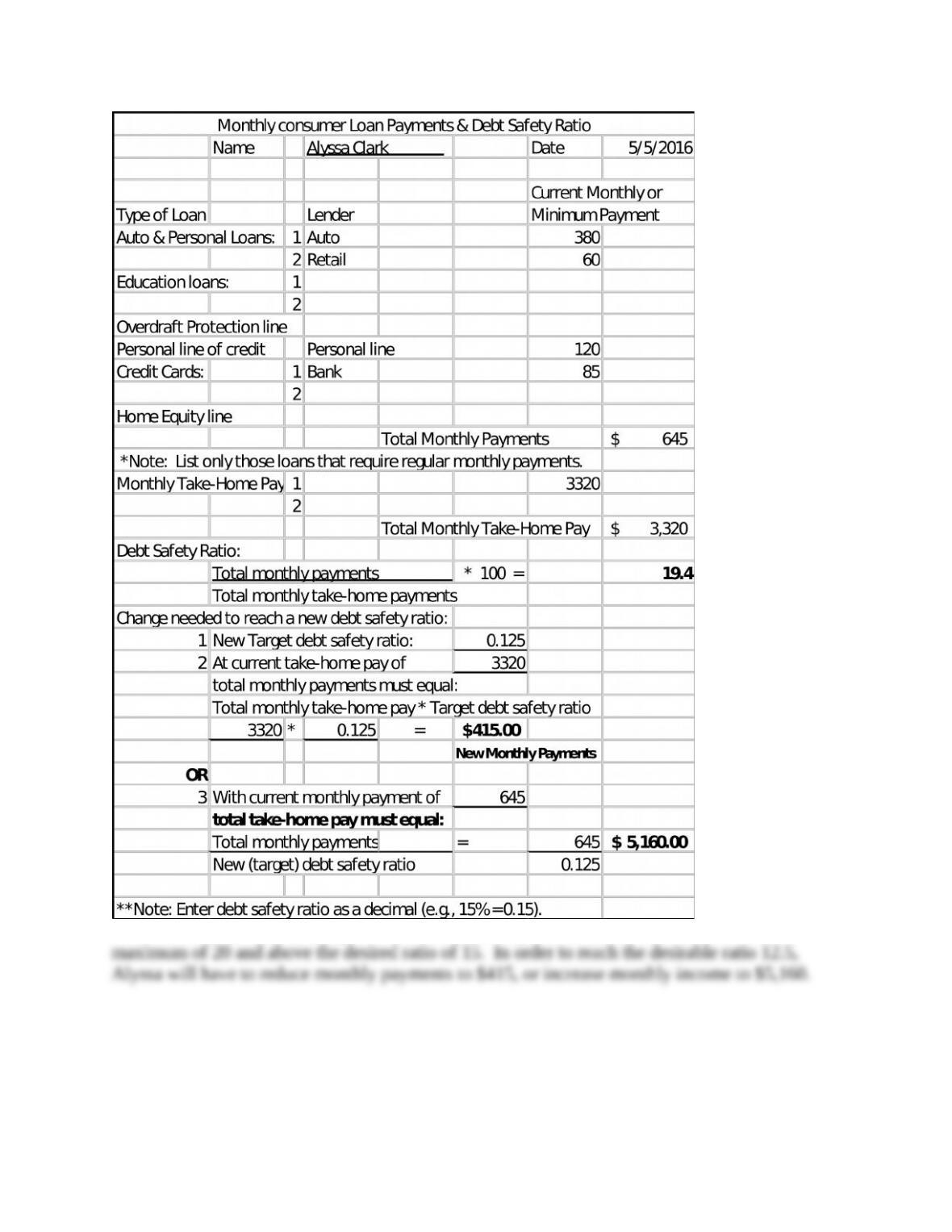

4. Evaluating debt safety ratio. Use Worksheet 6.1. Alyssa Clark is evaluating her debt safety

ratio. Her monthly take- home pay is $3,320. Each month, she pays $380 for an auto loan,

$120 on a personal line of credit, $60 on a department store charge card, and $85 on her

bank credit card. Complete Worksheet 6.1 by listing Alyssa’s outstanding debts, and then

calculate her debt safety ratio. Given her current take-home pay, what is the maximum

amount of monthly debt payments that Alyssa can have if she wants her debt safety ratio to

be 12.5 percent? Given her current monthly debt payment load, what would Alyssa’s take-

home pay have to be if she wanted a 12.5 percent debt safety ratio?

From Worksheet 6.1 above, Alyssa’s current debt safety ratio is 19.4 which is close to the

5. Implication of Credit Card Act. What are the main features and implications of the

Credit Card Act of 2009?

See Exhibit 6.4.

6. Using overdraft protection line. Isabella Harris has an overdraft protection line. Assume

that her October 2015 statement showed a latest (new) balance of $862. If the line had a

minimum monthly payment requirement of 5 percent of the latest balance (rounded to the

nearest $5 figure), then what would be the minimum amount that she’d have to pay on her

overdraft protection line?

7. Home equity line interest. Sean and Amy Anderson have a home with an appraised value

of $180,000 and a mortgage balance of only $90,000. Given that an S&L is willing to lend

money at a loan-to-value ratio of 75 percent, how big a home equity credit line can Sean

and Amy obtain? How much, if any, of this line would qualify as tax-deductible interest if

their house originally cost $100,000?

Current appraised value $180,000

First mortgage balance 90,000

The interest on the entire home equity loan of either $90,000 or $45,000 may be deducted as an

itemized deduction. The deductible interest in limited to the interest on a first mortgage of a

maximum $1,000,000 from the acquisition of up to two homes. The deductible interest on home

8. Calculating credit card interest. Ryan Gray, a student at State College, has a balance of

$380 on his retail charge card; if the store levies a finance charge of 21 percent per year,

how much monthly interest will be added to his account?

The monthly interest is the annual interest divided by 12. Thus, an annual interest of 21% is a

monthly interest of .21/12 = .0175 or 1.75%. With a balance of $380, that is $6.65 per month.

9. Choosing between credit cards. Wyatt Collins recently graduated from college and is

evaluating two credit cards. Card A has an annual fee of $75 and an interest rate of 9

percent. Card B has no annual fee and an interest rate of 16 percent. Assuming that Wyatt

intends to carry no balance and to pay off his charges in full each month, which card

represents the better deal? If Wyatt expected to carry a significant balance from one month

to the next, which card would be better? Explain.

Assuming that Wyatt intends to carry no balance and to pay off his charges in full each month

Assuming Wyatt expected to carry a significant balance from one month to the next, Card A

would cost an annual fee of $75 plus 9% of the monthly balance. Card B has no annual fee, but

a rate of 18%. If Wyatt has a monthly balance of $100, Card A would cost total fees of $75 +

9%*100 = $84 per year. Card B would have total fees of 18% * 100 = $18. The difference in

10. Balance transfer credit cards. Martina Lopez has several credit cards, on which she is

carrying a total current balance of $14,500. She is considering transferring this balance to

a new card issued by a local bank. The bank advertises that, for a 2 percent fee, she can

transfer her balance to a card that charges a 0 percent interest rate on transferred balances

for the first nine months. Calculate the fee that Martina would pay to transfer the balance,

and describe the benefits and drawbacks of balance transfer cards.

Martina has a fairly large balance of $14,500 on her credit cards. If her current cards charge her

12% per year, she would be paying $1,740/year or $145/month ($14,500 x .12/12) in interest on

this amount. Therefore, if she feels she would not be able to pay off this balance fairly rapidly,

she might indeed wish to transfer her balance to a 0% interest rate card for 9 months. If such a

card charges a 2% transfer fee, she would pay $290 to transfer her $14,500 balance. She would

have paid that amount in interest in 2 months anyway by leaving her balance with her old cards.

11. Calculating credit card finance charge. Parker Young recently received his monthly

MasterCard bill for the period June 1–30, 2015, and wants to verify the monthly finance

charge calculation, which is assessed at a rate of 15 percent per year and based on ADBs,

including new purchases. His outstanding balance, purchases, and payments are as follows:

Previous Balance: $386

Purchases:

June 4 $137

What is his ADB and the finance charge for the period? (Use a table like the one in Exhibit

6.8 for your calculations.)

The calculation of Joel’s interest is as follows:

Number of Days

(1)

Balance

(2)

(1) x (2) =

(3)

Previous balance 4 $386 $ 1,544

Purchases and payments:

June 4–11 balance ($386 + $137) 8 523 4,184

June 12–19 balance ($78 + $523) 8 601 4,808

12. Credit v debit card. Henry Stewart is trying to decide whether to apply for a credit card

or a debit card. He has $8,500 in a savings account at the bank and spends his money

frugally. What advice would you have for Henry? Describe the benefits and drawbacks of

each type of card.

Credit cards provide a line of credit and can be used worldwide as well as on the Internet to

make purchases or pay for services. Credit cards also allow the holder to obtain cash advances,

either from a financial institution or at an ATM machine. Other features offered by credit cards

may include a buyer protection plan on merchandise purchased with the card, travel accident

insurance, auto rental insurance coverage or other added attractions, such as a rebates or frequent

flyer miles. Even though most credit cards carry a fairly high interest rate, cardholders who pay

Debit cards do not provide credit but rather are like writing a check. Purchases on debit cards

come directly from one’s checking account and therefore incur no finance charges. People who

have difficulty managing credit many times prefer a debit card because they are not as tempted to

Henry would be a convenience user of either type card. He is a disciplined spender and probably

would not be tempted to overspend. He likely will not need credit for emergency purposes,

13. Credit card liability. Christine Lin was reviewing her credit card statement and noticed

several charges that didn’t look familiar to her. Christine is unsure whether she should pay

the bill in full and forget about the unfamiliar charges, or “make some noise.” If some of

these charges aren’t hers, is she still liable for the full amount? Is she liable for any part of

these charges, even if they’re fraudulent?

Christine should immediately notify the credit card issuer of any charges on her statement which

are not hers. The customer service representative of the issuing card can give her more

information concerning the purchases so that she can determine if she indeed made them and