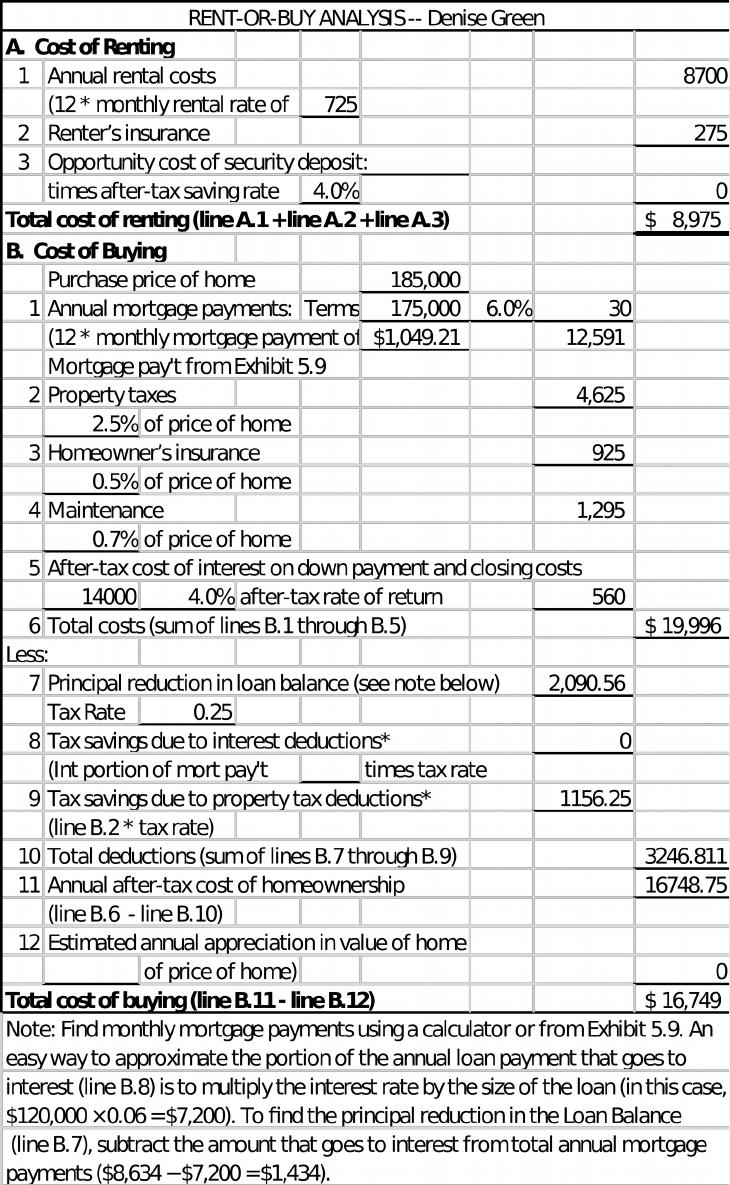

9. Rent vs Buy home. Use Worksheet 5.2. Denise Green is currently renting an apartment

for $725 per month and paying $275 annually for renter’s insurance. She just found a small

townhouse that she can buy for $185,000. She has enough cash for a $10,000 down payment

and $4,000 in closing costs. Her bank is offering 30-year mortgages at 6 percent per year.

Denise estimated the following costs as a percentage of the home’s price: property taxes, 2.5

percent; homeowner’s insurance, 0.5 percent; and maintenance, 0.7 percent. She is in the

25 percent tax bracket and has an after-tax rate of return on invested funds of 4 percent.

Using Worksheet 5.2, calculate the cost of each alternative and recommend the less costly

option—rent or buy—for Denise.

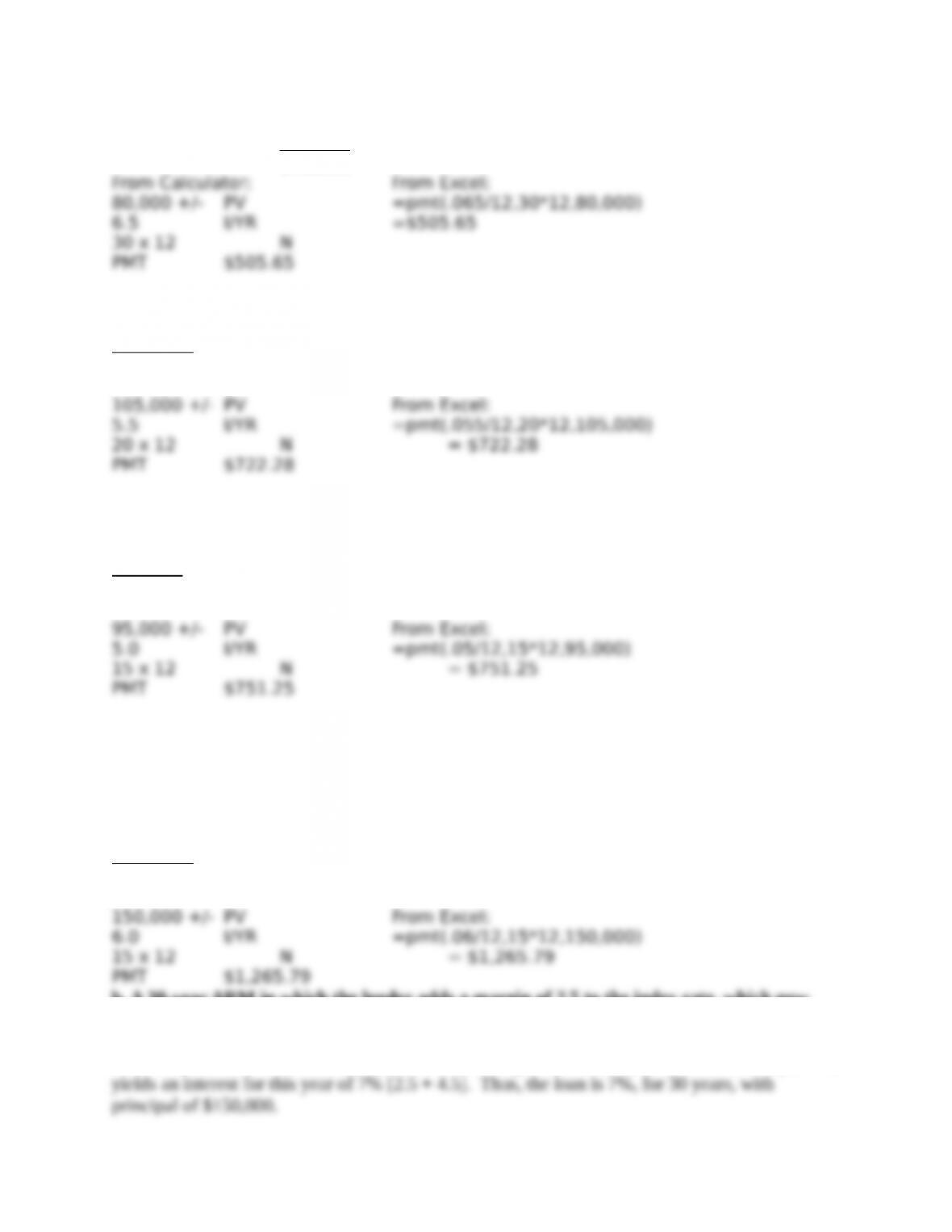

10. Calculating monthly mortgage payments. Find the monthly mortgage payments on the

following mortgage loans using either your calculator or the table in Exhibit 5.8:

a. $80,000 at 6.5 percent for 30 years

From Exhibit 5.9: $80,000 = 8.0 8.0 x $63.21 = $505.68 payment

$10,000

b. $105,000 at 5.5 percent for 20 years

From Exhibit 5.9:

$105,000 = 10.5 10.5 x $68.79 = $722.30 payment

$10,000

c. $95,000 at 5 percent for 15 years

From Exhibit 5.9:

$95,000 = 9.5 9.5 x $79.08 = $751.26 payment

$10,000

11. Conventional vs. ARM mortgage payments. What would the monthly payments be on a

$150,000 loan if the mortgage were set up as:

a. A 15-year, 6 percent fixed-rate loan?

From Exhibit 5.9:

$150,000 = 15 15 x $84.39 = $1,265.85 payment

$10,000

b. A 30-year ARM in which the lender adds a margin of 2.5 to the index rate, which now

stands at 4.5 percent?

For a 30-year, ARM loan where the lender adds a margin of 2.5% to the index rate of 4.5 percent,

From Exhibit 5.9:

$150,000 = 15 15 * 66.53 = $997.95

$ 10,000

Find the monthly mortgage payments for the first year only.

12. Adding to monthly mortgage payments. What are the pros and cons of adding $100 a

month to your fixed-rate mortgage payment?

Pros: The higher your extra payment, the sooner you pay off your mortgage. This would

provide extra future flexibility to meet needs like funding a child’s college education or

13. Refinancing a mortgage. Use Worksheet 5.4. Latha Yang purchased a condominium

four years ago for $180,000, paying $1,250 per month on her $162,000, 8 percent, 25-year

mortgage. The current loan balance is $152,401. Recently, interest rates have dropped

sharply, causing Latha to consider refinancing her condo at the prevailing rate of 6 percent.

She expects to remain in the condo for at least four more years and has found a lender that

will make a 6 percent, 21-year, $152,401 loan requiring monthly payments of $1,065.

Although there is no prepayment penalty on her current mortgage, Latha will have to pay

$1,500 in closing costs on the new mortgage. She is in the 15 percent tax bracket. Based on

this information, use the mortgage refinancing analysis form in Worksheet 5.4 to determine

whether she should refinance her mortgage under the specified terms.

From the worksheet below, it will take 9.6 months to breakeven on the refinancing. Since she

plans to stay in the home for another 4 years, it will be to her advantage to refinance the

mortgage.

Worksheet 5.4

MORTGAGE REFINANCING ANALYSIS

Name Latha Yang Date: May 5, 2016

Item Description Amount

3 Monthly savings, pretax (Item 1 + Item 2) $ 185

4 Tax on monthly savings [Item 3 * tax rate (_15_%)] $ 27.75

Critical Thinking Problems

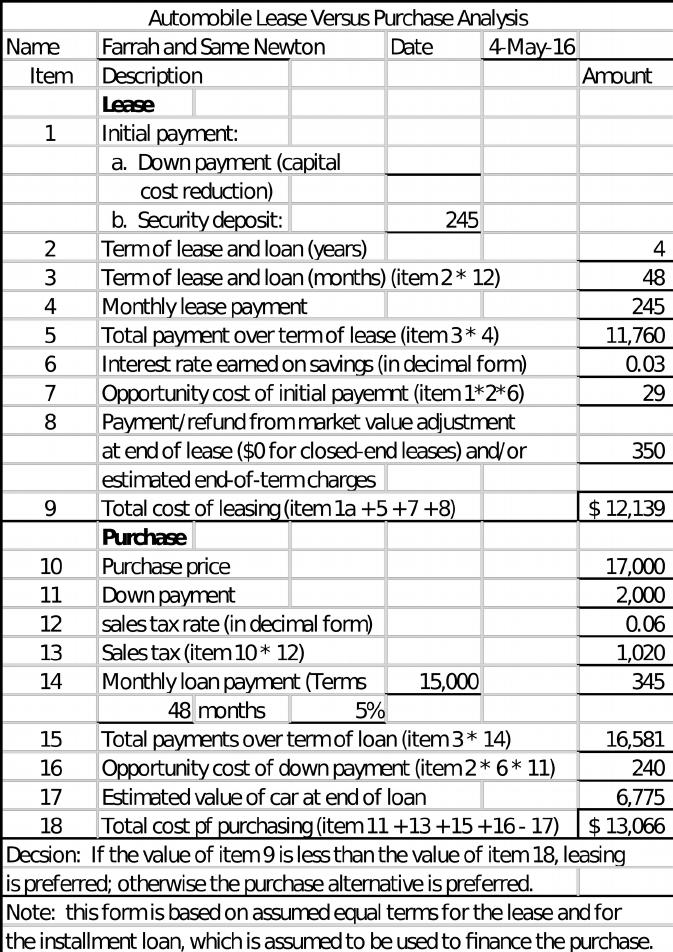

5.1 The Newtons New Car Decision: Lease versus Purchase

Farrah and Same Newton, a dual-income couple in their late 20s, want to replace their

seven-year-old car, which has 90,000 miles on it and needs some expensive repairs. After

reviewing their budget, the Newtons conclude that they can afford auto payments of not

more than $350 per month and a down payment of $2,000. They enthusiastically decide to

visit a local dealer after reading its newspaper ad offering a closed-end lease on a new car

for a monthly payment of $245. After visiting with the dealer, test-driving the car, and

discussing the lease terms with the salesperson, they remain excited about leasing the car

but decide to wait until the following day to finalize the deal. Later that day, the Newtons

begin to question their approach to the new car acquisition process and decide to

reevaluate their decision carefully.

Critical Thinking Questions

1. What are some basic purchasing guidelines that the Newtons should consider when

choosing which new car to buy or lease? How can they find the information they need?

Exhibit 5.1 lists key steps in buying a new car whether you purchase or lease the car. There are

many web pages that give information about various cars that you can reach via the internet.

2. How would you advise the Newtons to research the lease-versus-purchase decision before

visiting the dealer? What are the advantages and disadvantages of each alternative?

Until you understand how leasing works and compare lease terms with bank financing, you

The most important question to ask yourself is why you need a new car every few years.

Leasing may make sense if:

• You value purchasing flexibility. A lease allows you to put off the purchasing decision while

• You’re self-employed and can write off your leasing payment as a business expense.

If you like to drive a car until the wheels fall off, you do not want a lease. If you decide to

3. Assume that the Newtons can get the following terms on a lease or a bank loan for the

car, which they could buy for $17,000. This amount includes tax, title, and license fees.

• Lease: 48 months, $245 monthly payment, 1 month’s payment required as a security

deposit,

$350 end-of-lease charges; a residual value of $6,775 is the purchase option price at the end

of the lease.

• Loan: $2,000 down payment, $15,000, 48-month loan at 5 percent interest requiring a

monthly payment of $345.44; assume that the car’s value at the end of 48 months will be

the same as the residual value and that sales tax is 6 percent.

The Newtons can currently earn interest of 3 percent annually on their savings. They

expect to drive about the same number of miles per year as they do now.

a. Use the format given in Worksheet 5.1 to determine which deal is best for the Newtons.

b. What other costs and terms of the lease option might affect their decision?

c. Based on the available information, should the Newtons lease or purchase the car? Why?

The worksheet is below. Based on the worksheet, there is an advantage to leasing of $927.

Thus, if you have faith in all of the estimates in the worksheet, leasing is the way to go. You may

be able to earn more on your down payment than you estimate; if so, another reason to lease.

You will never be completely accurate in your estimates. You do your best and then consider

5.2 Evaluating a Mortgage Loan for the Gerrards

Ben and Marie Gerrard, both in their mid-20s, have been married for four years and have

two preschool-age children. Ben has an accounting degree and is employed as a cost

accountant at an annual salary of $62,000. They’re now renting a duplex but wish to buy a

home in the suburbs of their rapidly developing city. They’ve decided they can afford a

$215,000 house and hope to find one with the features they desire in a good neighborhood.

The insurance costs on such a home are expected to be $800 per year, taxes are expected to

be $2,500 per year, and annual utility bills are estimated at $1,440—an increase of $500

over those they pay in the duplex. The Gerrards are considering financing their home with

a fixed-rate, 30-year, 6 percent mortgage. The lender charges 2 points on mortgages with 20

percent down and 3 points if less than 20 percent is put down (the commercial bank that

the Gerrards will deal with requires a minimum of 10 percent down). Other closing costs

are estimated at 5 percent of the home’s purchase price. Because of their excellent credit

record, the bank will probably be willing to let the Gerrards’ monthly mortgage payments

(principal and interest portions) equal as much as 28 percent of their monthly gross

income. Since getting married, the Gerrards have been saving for the purchase of a home

and now have $44,000 in their savings account.

Critical Thinking Questions

1. How much would the Gerrards have to put down if the lender required a minimum 20

percent down payment? Could they afford it?

With a 20% down payment, the Gerrands need 20% * $215,000 or $43,000 just for the down

2. Given that the Gerrards want to put only $25,000 down, how much would their closing

costs be?

With $25,000 down, the principal on the loan will be $190,000. Closing costs are estimated at

Considering only principal and interest, how much would their monthly mortgage

payments be?

Loan of $190,000, 30-year, 6% will require a payment of $1,139.15

[=pmt(.06/12,30*12,190,000) using Excel or with Exhibit 5.9

Would they qualify for a loan using a 28 percent affordability ratio?

3. Using a $25,000 down payment on a $215,000 home, what would the Gerrards’ loan-to-

value ratio be? Calculate the monthly mortgage payments on a PITI basis.

Loan-to-value ratio would be 190,000/215,000 or 88.4%. As a rule, lenders prefer no more than

80%. The payment on a PITI basis includes principal, interest, property taxes and insurance.

For this loan,

4. What recommendations would you make to the Gerrards? Explain.

They can afford to purchase the home with their current income level. The down payment,