5-15 What role does a real estate agent play in the purchase of a house? What is the benefit

of the MLS? How is the real estate agent compensated, and by whom?

Most home buyers rely on real estate agents because they’re professionals who are in daily

contact with the housing market. Once you describe your needs to an agent, he or she can begin

to search for appropriate properties. Your agent will also help you negotiate with the seller,

Buyers should remember that agents typically are employed by sellers. Unless you’ve agreed to

pay a fee to a sales agent to act as a buyer’s agent, a realtor’s primary responsibility, by law, is to

5-16 Describe a real estate short sales transaction. What are the potential benefits and costs

from the perspective of the homeowner?

A real estate short sale is the sale of property in which the proceeds are less than the balance

owed on a loan secured by the property sold. This procedure is an effort by mortgage lenders to

come to terms with homeowners who are about to default or are defaulting on their mortgage

loans. Although it certainly can reduce a lender’s losses, it can also be beneficial for the

5-17 Why should you investigate mortgage loans and prequalify for a mortgage early in the

home-buying process?

Prequalification can work to your advantage in several ways. You’ll know ahead of time the

specific mortgage amount that you qualify for—subject, of course, to changes in rates and terms

—and can focus your search on homes within an affordable price range. Prequalification also

provides estimates of the required down payment and closing costs for different types of

5-18 What information is normally included in a real estate sales contract? What is an

earnest money deposit? What is a contingency clause?

State laws generally specify that, to be enforceable in court, real estate buy–sell agreements must

be in writing and contain certain information, including: (1) the names of buyers and sellers,

(2) a description of the property sufficient for positive identification, (3) specific price and other

terms, and (4) usually the signatures of the buyers and sellers. An earnest money deposit is the

5-19 Describe the steps involved in closing the purchase of a home.

An overview of these closing requirements may be found on HUD’s Web site (go to the “Homes”

section of http://www.hud.gov). Exhibit 5.11 provides some tips to help you sail smoothly

5-20 Describe the various sources of mortgage loans. What role might a mortgage broker

play in obtaining mortgage financing?

The major sources of home mortgages today are commercial banks, thrift institutions, and

mortgage bankers or brokers; also, some credit unions make mortgage loans available to their

5-21 Briefly describe the two basic types of mortgage loans. Which has the lowest initial

rate of interest? What is negative amortization, and which type of mortgage can experience

it? Discuss the advantages and disadvantages of each mortgage type.

The fixed-rate mortgage still accounts for a large portion of all home mortgages. Both the rate

The adjustable-rate mortgage (ARM) provides that the rate of interest, and therefore the size

of the monthly payment, is adjusted based on market interest rate movements. Typically the

ARM will have lower rated than the fixed-rate mortgage, at least initially. The rates will change

5-22 Differentiate among conventional, insured, and guaranteed mortgage loans.

A conventional mortgage is a mortgage offered by a lender who assumes all the risk of loss. To

To promote homeownership, the federal government, through the Federal Housing

Administration (FHA), offers lenders mortgage insurance on loans with a high loan-to-value

Guaranteed loans are similar to insured loans, but better—if you qualify. VA loan guarantees are

Financial Planning Exercises

1. Planning a new car purchase: Janet Wilhite has just graduated from college and needs to

buy a car to commute to work. She estimates that she can afford to pay about $450 per

month for a loan or lease and has about $2,000 in savings to use for a down payment.

Develop a plan to guide her through her first car-buying experience, including researching

car type, deciding whether to buy a new or used car, negotiating the price and terms, and

financing the transaction.

Exhibit 5.1 lists the steps in buying a new car.

Research which car best meets your needs and determine how much you can afford to

spend on it. Choose the best way to pay for your new car—cash, financing, or lease. Ask

Check Web sites like Edmunds.com and TV and newspapers for incentives and rebates on

Decide on a price based on the dealer’s cost for the car and options, plus a markup for the

Test-drive the car—and the car salesperson. Test-drive the car at least once, both on local

If you are trading in your old car, you are not likely to get as high a price as if you sell it

Negotiate the lowest price on your new car by getting bids from at least three dealers.

Close the deal after looking not just at the cost of the car but also the related expenses.

Review and sign the paperwork. If you have a worksheet for the deal, the contract should

Inspect the car for scratches and dents. If anything is missing—like floor mats, for

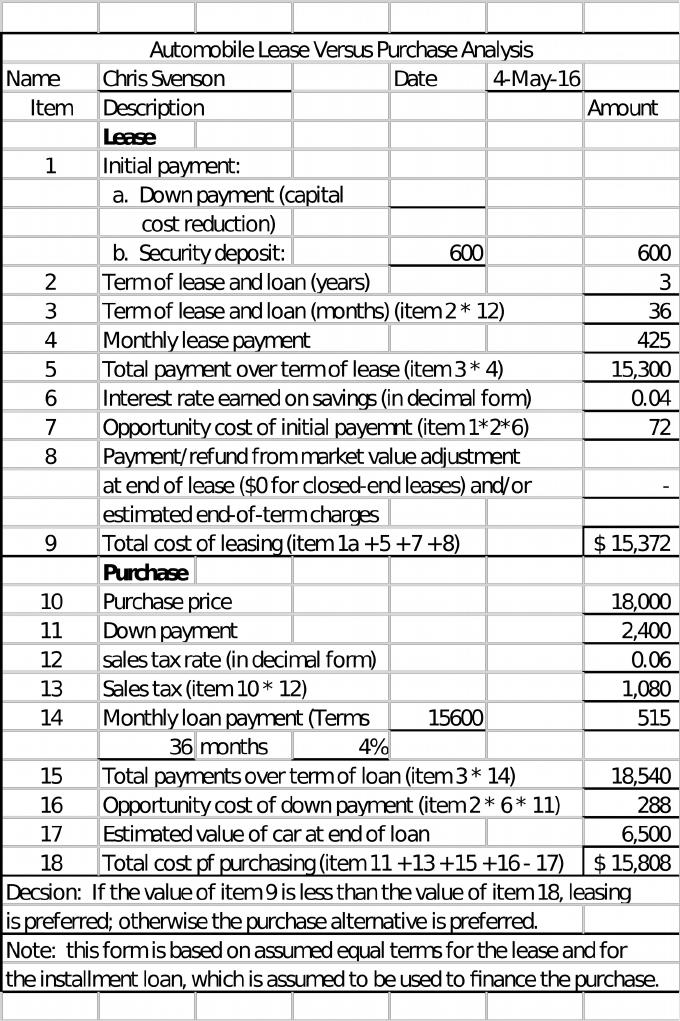

2. Lease vs purchase car decision: Use Worksheet 5.1. Chris Svenson is trying to decide

whether to lease or purchase a new car costing $18,000. If he leases, he’ll have to pay a $600

security deposit and monthly payments of $425 over the 36-month term of the closed-end

lease. On the other hand, if he buys the car then he’ll have to make a $2,400 down payment

and will finance the balance with a 36-month loan requiring monthly payments of $515;

he’ll also have to pay a 6 percent sales tax ($1,080) on the purchase price, and he expects

the car to have a residual value of $6,500 at the end of 3 years. Chris can earn 4 percent

interest on his savings. Use the automobile lease versus purchase analysis form in

Worksheet 5.1 to find the total cost of both the lease and the purchase and then recommend

the best strategy for Chris.

From Worksheet 5.1 below, better alternative is to lese the car. However, if the value at the end

of three years is understated by $500, it is better to purchase.

3. Interpreting the rent ratio. Art Patton has equally attractive job offers in Miami and Los

Angeles. The rent ratios in the cities are 8 and 20, respectively. Art would really like to buy

rather than rent a home after the moves. Explain how to interpret the rent ratio and what

it tells Art about the relative attractiveness of moving to Miami rather than Los Angeles,

given his stated goal.

The rent ratio is the ratio of the average house price to the average annual rent, which provides

insight into the relative attractiveness of buying a house versus renting in a given area of

potential interest. Rent ratios between 31 and 35 indicate that it is more attractive to rent than to

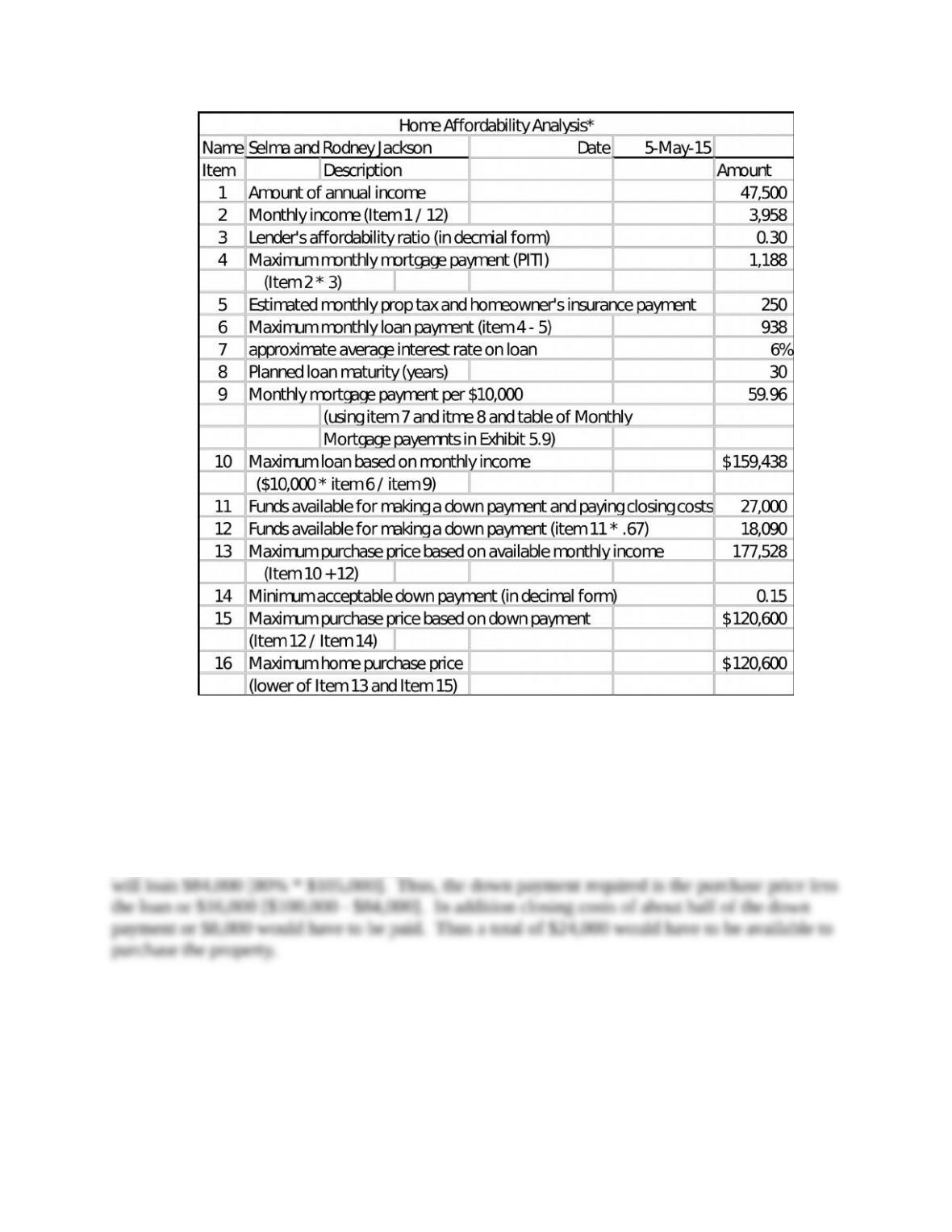

4. Home affordability analysis. Use Worksheet 5.3. Selma and Rodney Jackson need to

calculate the amount that they can afford to spend on their first home. They have a

combined annual income of $47,500 and have $27,000 available for a down payment and

closing costs. The Jacksons estimate that homeowner’s insurance and property taxes will be

$250 per month. They expect the mortgage lender to use a 30 percent (of monthly gross

income) mortgage payment affordability ratio, to lend at an interest rate of 6 percent on a

30-year mortgage, and to require a 15 percent down payment. Based on this information,

use the home affordability analysis form in Worksheet 5.3 to determine the highest-priced

home that the Jacksons can afford.

Based upon the Worksheet 5.3 below, the maximum purchase the Jacksons can afford is

5. Calculating required down payment on home purchase. How much would you have to put

down on a house costing $100,000 if the house had an appraised value of $105,000 and the

lender required an 80 percent loan-to-value ratio?

A loan to value ratio of 80 percent indicates the maximum amount that a lender will loan on a

property. The “value” refers to the appraised value, thus, with a ratio of 80 percent, the lender

6. Using the maximum ratios for a conventional mortgage, how big a monthly payment

could the Danforth family afford if their gross (before-tax) monthly income amounted to

$4,000?

Would it make any difference if they were already making monthly installment loan

payments totaling $750 on two car loans?

The range for mortgage payments over income is from 25 to 30 percent. The range for the total of all

installment payments is 33 to 38 percent. So, if the Taylor family income is $4,000 per month:

7. Estimating closing costs on home purchase. How much might a home buyer expect to pay

in closing costs on a $220,000 house with a 10 percent down payment? How much would

the home buyer have to pay at the time of closing, taking into account closing costs, down

payment, and a loan fee of 3 points?

Closing costs are about 50% of the down payment. For a $220,000 purchase price, with a 10%

8. Changes in mortgage principal and interest over time. Explain how the composition of the

principal and interest components of a fixed-rate mortgage change over the life of the

mortgage. What are the implications of this change?

Exhibit 5.8 graphs the relationship between principal and interest payments over the life of a