Critical Thinking Cases

4.1 June Xu’s Savings and Banking Plans

June Xu is a registered nurse who earns $3,250 per month after taxes. She has been

reviewing her savings strategies and current banking arrangements to determine if she

should make any changes. June has a regular checking account that charges her a flat fee

per month, writes an average of 18 checks a month, and carries an average balance of $795

(although it has fallen below $750 during 3 months of the past year). Her only other

account is a money market deposit account with a balance of $4,250. She tries to make

regular monthly deposits of $50–$100 into her money market account but has done so only

about every other month.

Of the many checking accounts June’s bank offers, here are the three that best suit her

needs.

• Regular checking, per-item plan: Service charge of $3 per month plus 35 cents per check.

• Regular checking, flat-fee plan (the one June currently has): Monthly fee of $7 regardless

of how many checks written. With either of these regular checking accounts, she can avoid

any charges by keeping a minimum daily balance of $750.

• Interest checking: Monthly service charge of $7; interest of 3 percent, compounded daily

(refer to Exhibit 4.8). With a minimum balance of $1,500, the monthly charge is waived.

June’s bank also offers CDs for a minimum deposit of $500; the current annual interest

rates are 3.5 percent for 6 months, 3.75 percent for 1 year, and 4 percent for 2 years.

Critical Thinking Questions

1. Calculate the annual cost of each of the three accounts, assuming that June’s banking

habits remain the same. Which plan would you recommend and why?

a. Regular checking, per-item plan: Service charge of $3 per month plus 35 cents per check.

b. Regular checking, flat-fee plan (the one June currently has): Monthly fee of $7 regardless of

how many checks written.

c. Interest checking: Monthly service charge of $7; interest of 3 percent, compounded daily.

With a minimum balance of $1,500, the monthly charge is waived.

Since June’s balance is always under $1,500, she will have monthly charges each month.

Annual monthly service charge $7 * 12 = $84; Less interest earned $795 * .0305 = $24.25

2. Should June consider opening the interest checking account and increasing her

minimum balance to at least $1,500 to avoid service charges? Explain your answer.

In order to maintain $1,500 minimum balance, June would have to move $705 from her money

market account to the checking account. The rate on the money market account is most likely at

least the same as the 3.05% June will earned on the checking account. Thus, the interest gained

The interest checking account will be the better of the three if she is willing to move money from

3. What other advice would you give June about her checking account and savings

strategy?

June should start automatically transfer $100 per month to her money market account. The

automatic transfer feature will assure that the money is transferred each month without June

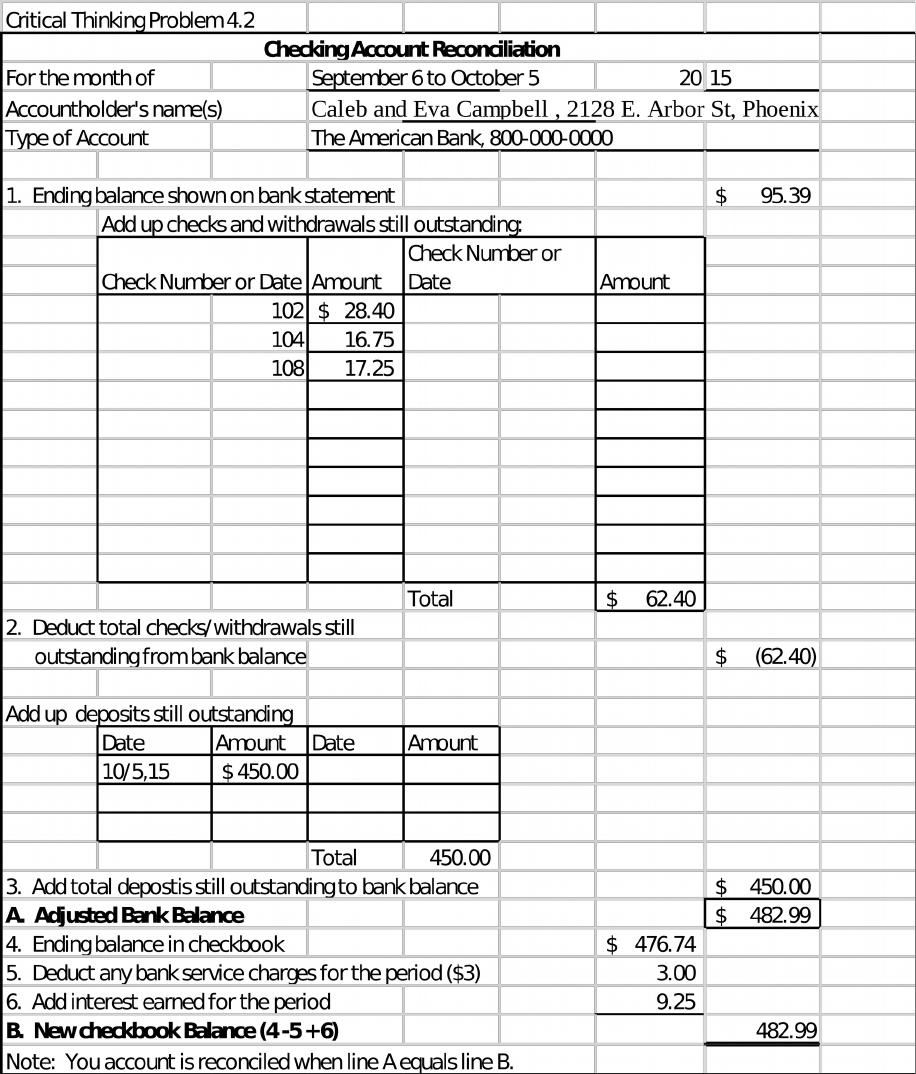

4.2 Reconciling the Campbell’s Checking Account

Caleb and Eva Campbell are college students who opened their first joint checking account

at the American Bank on September 14, 2015. They’ve just received their first bank

statement for the period ending October 5, 2015. The statement and checkbook ledger are

shown in the table on the next page.

Critical Thinking Questions

1. From this information, prepare a bank reconciliation for the Campbell’s as of October 5,

2015, using a form like the one in Worksheet 4.1.

Note: The problem information is not reproduced here. The bank reconciliation using

Worksheet 4.1 is on page following.

2. Given your answer to Question 1, what, if any, adjustments will the Campbell’s need to

make in their checkbook ledger? Comment on the procedures used to reconcile their

checking account and their findings.

They do not have the $3 bank charges or the additional deposit of $9.75 recorded. Since this was

the first month of the account, the reconciliation was simple. Bank charges frequently are

unknown until the statement comes, so they are always an adjustment item. The additional

3. If the Campbell’s earned interest on their idle balances because the account is a money

market deposit account, what impact would this have on the reconciliation process?

Explain.

Perhaps the bank charges could be avoided by using a money market account. Also, there would

Terms Found in the Chapter

account

reconciliation

Verifying the accuracy of your checking account balance in relation

to the bank’s records as reflected in the bank statement, which is an

itemized listing of all transactions in the checking account.

automated teller

machine (ATM)

A remote computer terminal that customers of depository

institutions can use to make basic transactions 24 hours a day, 7

days a week.

asset management

account (AMA)

A comprehensive deposit account, offered primarily by brokerage

houses and mutual funds.

cash management The routine, day-to-day administration of cash and near-cash

resources, also known as liquid assets, by an individual or family.

certificate of deposit

(CD)

A type of savings instrument issued by certain financial institutions

in exchange for a deposit; typically requires a minimum deposit

and has a maturity ranging from 7 days to as long as 7 or more

years.

checkbook ledger A booklet, provided with a supply of checks, used to maintain

accurate records of all checking account transactions.

compound interest When interest earned in each subsequent period is determined by

applying the nominal (stated) rate of interest to the sum of the

initial deposit and the interest earned in each prior period.

debit cards Specially coded plastic cards used to transfer funds from a

customer’s bank account to the recipient’s account to pay for goods

or services.

demand deposit An account held at a financial institution from which funds can be

withdrawn on demand by the account holder; same as a checking

account.

deposit insurance A type of insurance that protects funds on deposit against failure of

the institution; can be insured by the FDIC and the NCUA.

effective rate of

interest

The annual rate of return that is actually earned (or charged)

during the period the funds are held (or borrowed).

electronic funds Systems using the latest telecommunications and computer

transfer systems

(EFTSs)

technology to electronically transfer funds into and out of

customers’ accounts.

I Savings bond A savings bond, issued at face value by the U.S. Treasury, whose

partially fixed rate provides some inflation protection.

Internet bank An online commercial bank.

money market

deposit account

(MMDA)

A federally insured savings account, offered by banks and other

depository institutions that competes with money market mutual

funds.

money market

mutual fund

(MMMF)

A mutual fund that pools the funds of many small investors and

purchases high-return, short-term marketable securities.

negotiable order of

withdrawal (NOW)

account

A checking account on which the financial institution pays interest;

NOWs have no legal minimum balance.

nominal (stated)

rate of interest

The promised rate of interest paid on a savings deposit or charged

on a loan.

overdraft The result of writing a check for an amount greater than the current

account balance.

overdraft protection An arrangement between the account holder and the depository

institution wherein the institution automatically pays a check that

overdraws the account.

Series EE bond A savings bond issued in various denominations by the U.S.

Treasury.

share draft account An account offered by credit unions that is similar to interest-

paying checking accounts offered by other financial institutions

simple interest Interest that is paid only on the initial amount of the deposit.

stop payment An order made by an account holder instructing the depository

institution to refuse payment on an already issued check.

time deposit A savings deposit at a financial institution; remains on deposit for a

longer time than a demand deposit.

U.S. Treasury bill

(T-bill)

A short-term (3- or 6-month maturity) debt instrument issued at a

discount by the U.S. Treasury in the ongoing process of funding the

national debt.

Chapter 4

Managing Your Cash and Savings

Chapter Outline

Learning Goals

I. The Role of Cash Management in Personal Financial Planning

A. The Problem with Low Interest Rates

Test Yourself

II. Today’s Financial Services Marketplace

A. Types of Financial Institutions

1. Depository Financial Institutions

2. Nondepository Financial Institutions

B. How Safe Is Your Money?

1. Deposit Insurance

Test Yourself

III. A Full Menu of Cash Management Products

A. Checking and Savings Accounts

1. Checking Accounts

2. Savings Accounts

3. Interest-Paying Checking Accounts

a. NOW Accounts

b. Money Market Deposit Accounts

c. Money Market Mutual Funds

4. Asset Management Accounts

B. Electronic Banking Services

1. Electronic Funds Transfer Systems

a. Debit Cards and Automated Teller Machines

b. Preauthorized Deposits and Payments

c. Bank-by-Phone Accounts

2. Online Banking and Bill Payment Services

C. Regulation of EFTS Services

D. Other Bank Services

Test Yourself

IV. Maintaining a Checking Account

A. Opening and Using Your Checking Account

1. The Cost of a Checking Account

2. Individual or Joint Account?

3. General Checking Account Procedures

4. Overdrafts

5. Stopping Payment

B. Monthly Statements

1. Account Reconciliation

C. Special Types of Checks

1. Cashier’s Check

2. Traveler’s Check

3. Certi7ed Check

Test Yourself

V. Establishing a Savings Program

A. Starting Your Savings Program

B. Earning Interest on Your Money

1. The effect of Compounding

2. Compound Interest Generates Future Value

C. A Variety of Ways to Save

1. Certi7cates of Deposit

2. U.S. Treasury Bills

3 . Series EE Bonds

4. I Savings Bonds

Test Yourself

Summary

Financial Planning Exercises

Applying Personal Finance

Manage Your Cash!

Critical Thinking Cases

4.1 June Xu’s Savings and Banking Plans

4.2 Reconciling the Campbell’s Checking Account

Money Online!