4-14 Is it possible to bounce a check because of insufficient funds when the checkbook

ledger shows a balance available to cover it? Explain what happens when a check bounces.

Can you obtain protection against overdrafts?

It is possible to bounce a check due to insufficient funds when the checkbook ledger

shows a balance available to cover it if certain deposits added to the checkbook ledger

have not yet been credited to the account by the bank. This situation could also arise

When a check bounces, the bank stamps the overdrawn check with the words

“insufficient balance (or funds)” and returns it to the party to whom it was written. The

account holder is notified of this action, and a penalty fee of $20 to $25or more is

To prevent bounced checks, you can arrange for overdraft protection through an overdraft

line of credit or automatic transfer program. Here the bank will go ahead and pay a check

that overdraws the account, but be aware that bank charges and policies vary widely on

4-15 Describe the procedure used to stop payment on a check. Why might you wish to

initiate this process?

Payment on a check is stopped by notifying the bank. Normally, the account holder fills

out a form with the check number and date, amount, and the name of the payee. Some

banks accept stop-payment orders over the telephone or online and may ask for a written

Several reasons to issue a stop payment order include:

A good or service paid for by check is found to be faulty.

4-16 What type of information is found in the monthly bank statement, and how is it used?

Explain the basic steps involved in reconciling an account.

Your monthly bank statement contains an itemized listing of all transactions (checks

written, deposits made, electronic funds transfer transactions such as ATM withdrawals

and deposits and automatic payments) within your checking account. It also includes

notice of any service charges levied or interest earned in the account. Many banks also

The basic steps in the account reconciliation process are:

1. Upon receipt of the bank statement, arrange all canceled checks in descending

2. Compare each check amount, from the check itself or the statement, with the

corresponding entry in the checkbook ledger to make sure that no recording errors

exist. Place a checkmark in the ledger alongside each entry compared. Also check off

3. List all checks and other deductions (ATM withdrawals, automatic payments) still

4. Repeat the process for deposits. All automatic deposits and deposits made at ATMs

5. Subtract the total amount of checks outstanding (from step 3) from the bank statement

6. Deduct the amount of any service charges levied by the bank and add any interest

earned to the checkbook ledger balance. The resulting amount is the new checkbook

4-17 Briefly describe each of these special types of checks:

a. A cashier’s check is drawn on the bank, rather than a personal or corporate account, so

b. Traveler’s checks provide a safe, convenient way to carry money while traveling because

c. A certified check is a personal check guaranteed by the bank as to availability of

4-18 In general, how much of your annual income should you save in the form of liquid

reserves? What portion of your investment portfolio should you keep in savings and other

short-term investment vehicles? Explain.

Although opinions differ as to how much you should keep as liquid reserves, the post-crisis

Many financial planning experts recommend keeping a minimum of 10 percent to 25 percent of

your investment portfolio in savings-type instruments in addition to the 6 to 9 months of liquid

4-19 Define and distinguish between the nominal (stated) rate of interest and the effective

rate of interest. Explain why a savings and loan association that pays a nominal rate of 4.5

percent interest, compounded daily, actually pays an effective rate of 4.6 percent.

The nominal rate of interest is the stated rate of interest, so in this instance the S&L’s

nominal interest rate is 4.5%. The effective rate of interest is the interest rate actually

We can determine the effective rate when the S&L has a stated rate of 4.5% by calculating how

much interest is actually paid during the year. The easiest way is with a financial

1,000 +/- PV

4.5 365 I

1 × 365 N

FV $1,046.03

During the year, this account earned $46.03 in interest, so we take the interest earned and

4-20 What factors determine the amount of interest you will earn on a deposit account?

Which combination provides the best return?

The amount of interest earned depends on several factors, including frequency of

compounding, how the bank calculates the balances on which interest is paid, and the

interest rate itself. Look for daily or continuous compounding and a balance calculation

4-21 Briefly describe the basic features of each of the following savings vehicles:

(a) CDs, (b) U.S. Treasury bills, (c) Series EE bonds, and (d) I savings bonds.

a. Certificates of deposit (CDs) are savings instruments that require funds to remain on

deposit for a specified period of time and can range from seven days to a year or more.

Although it is possible to withdraw funds prior to maturity, an interest penalty usually

makes withdrawal somewhat costly. While the bank or other depository institution can

b. U.S. Treasury bills (T-bills) are obligations of the U.S. Treasury issued as part of the

on-going process of funding the national debt. T-bills are sold on a discount basis now in

minimum denominations as low as $1,000 and are issued with 3-month (13-week), 6-

month (26-week), and one-year maturities. They carry the full faith and credit of the U.S.

c. Series EE bonds are the well-known savings bonds that have been around for

decades. They are often purchased through payroll deduction plans or at banks or other

depository institutions. Though issued by the U.S. Treasury, they are very different from

U.S. Treasury bills. The fixed interest rate is set every six months in May and November,

d. I Savings Bonds are similar to Series EE bonds in numerous ways. Both are issued

by the U.S. Treasury and are accrual-type securities. I bonds are available in

denominations between $25 and $10,000. Interest compounds semiannually for 30 years

There are some significant differences between the two savings vehicles. Whereas Series

EE bonds are sold at a discount, I bonds are sold at face value. I savings bonds differ

from Series EE bonds in that their annual interest rate combines a fixed rate that remains

the same for the life of the bond with a semi-annual inflation rate that changes with the

Consumer Price Index for all Urban Consumers (CPI-U). In contrast, the rate on Series

Solutions to Financial Planning Exercises

1. Your parents are retired and have expressed concern about the really low interest rates

they’re earning on their savings. They’ve been approached by an advisor who says he has a

“sure-fire” way to get them higher returns. What would you tell your parents about the

low-interest-rate environment, and how would you advise them to view the advisor’s new

prospective investments?

While it is true that low interest rates will result in reduced income to retirees, the search for

higher current returns has led many individuals to make investments of questionable risk. You

probably would be best to urge your parents to be very skeptical of “sure-fire” claims for higher

returns. If something sounds too good to be true, then it probably isn’t. Talk to your parents about

2. What type of bank serves your needs best? Visit the Web sites of the following

institutions and prepare a chart comparing the services offered, such as traditional and

online banking, investment services, and personal financial advice. Which one would you

choose to patronize, and why?

a. Bank of America (http://www.bankofamerica.com)—a nationwide full-service bank

b. A leading local commercial bank in your area

c. A local savings institution

d. A local credit union

Individual student answers will vary depending upon the needs of the student.

Commercial banks offer checking and savings accounts and a full range of financial products and

services. They can offer non-interest-paying checking accounts (demand deposits). They are the

Savings and loans (S&Ls) channel the savings of depositors primarily into mortgage loans for

purchasing and improving homes. Also offers many of the same checking, saving, and lending

Savings banks are similar to S&Ls, but are located primarily in the New England states. Most are

Credit unions are nonprofit, member-owned financial cooperatives that provide a full range of

financial products and services to its members, who must belong to a common occupation,

religious or fraternal order, or residential area. Generally, these are smaller institutions when

3. Suppose that someone stole your ATM card and withdrew $950 from your checking

account. How much money could you lose according to federal legislation if you reported

the stolen card to the bank: (a) the day the card was stolen, (b) 6 days after the theft, (c) 65

days after receiving your periodic statement?

If your ATM card was stolen and $950 was withdrawn from your checking account, you

would be liable for:

a. $50 if you notified the bank the next day;

b. $500 if you notified the bank six days later; and

4. You’re getting married and are unhappy with your present bank. Discuss your strategy

for choosing a new bank and opening an account. Consider the factors that are important

to you in selecting a bank—such as the type and ownership of new accounts and bank fees

and charges.

Factors that typically influence the choice of where to maintain a checking account are

convenience, services, and cost. Many people choose a bank based solely on convenience

factors: business hours, location, number of drive-thru windows, and number and location of

One advantage of the joint account over two individual accounts is lower service charges. In

5. Determine the annual net cost of these checking accounts:

a. Monthly fee $4, check-processing fee of 20 cents, average of 23 checks written per month

b. Annual interest of 2.5 percent paid if balance exceeds $750, $8 monthly fee if account

falls below minimum balance, average monthly balance $815, account falls below $750

during 4 months

Interest earned/month = .025/12 × $815 = $1.70

Add: total annual interest (for months

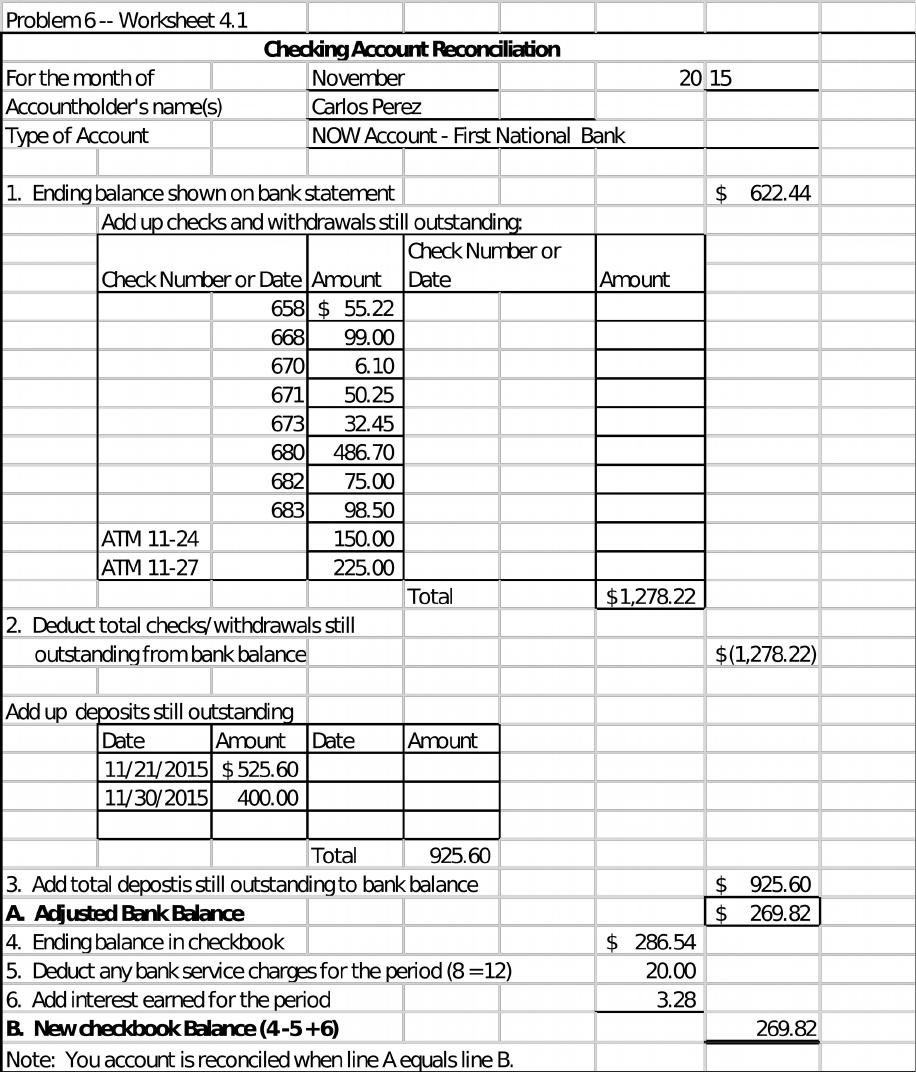

6. Use Worksheet 4.1. Carlos Perez has a NOW account at the First National Bank. His

checkbook ledger lists the following checks:

Check

Number Amount

Check

Number Amount

Check

Number Amount

654 206.05 672 24.90 678 38.04

658 55.22 673 32.45 679 97.99

Felipe also made the following withdrawals and deposits at an ATM near his home:

Date Amount Transaction

11/1 $50.00 Withdrawal

11/2 525.60 Deposit

11/6 100.00 Deposit

Carlos’s checkbook ledger shows an ending balance of $286.54. He has just received his bank

statement for the month of November. It shows an ending balance of $622.44; it also shows that

he earned interest for November of $3.28, had a check service charge of $8 for the month, and

had another $12 charge for a returned check. His bank statement indicates the following checks

7. If you put $6,000 in a savings account that pays interest at the rate of 4 percent,

compounded annually, how much will you have in 5 years? (Hint: Use the future value

formula.) How much interest will you earn during the 5 years? If you put $6,000 each year

into a savings account that pays interest at the rate of 4 percent a year, how much would

you have after 5 years?

Use the formula FV = PV × (1 + i)n as the tables in the appendix do not have 4%.

Using the financial calculator, set on END MODE and 1 P/YR:

6,000 +/- PV

Since you initially deposit $6,000 and end up with $7,299.92 in five years, the amount of

Calculate the future value of a series of 5 yearly $6,000 payments compounding at 4% per year

using the financial calculator, set on END MODE and 1 P/YR:

6,000 +/- PMT

8. Describe some of the short-term investment vehicles that can be used to manage your cash

resources. What would you focus on if you were concerned that the financial crisis inflation will

increase significantly in the future?

Short-term is generally understood to be less than a year. Given this short period the options are:

Each of these are very secure with the T–bill being the most secure.

If I was concerned with increasing inflation and with investing for a short-term, I would select a

blue chip stock that is very marketable and will react to inflation. In period of increasing

9. Owen and Audrey Nelson together earn approximately $82,000 a year after taxes.

Through an inheritance and some wise investing, they also have an investment portfolio

with a value of almost $150,000.

a. How much of their annual income do you recommend they hold in some form of liquid

savings as reserves? Explain.

The general rule is to keep 6 to 9 months of after tax income in liquid savings. Thus, the

b. How much of their investment portfolio do you recommend they hold in savings and

other short-term investment vehicles? Explain.

Many financial planning experts recommend keeping a minimum of 10 percent to 25 percent of

c. How much, in total, should they hold in short-term liquid assets?

The emergency fund is in addition to the savings type investment in their portfolio. So in total