3-a. Solvency Ratio: This term refers to having a positive net worth. The calculation for her

solvency ratio is as follows:

This indicates that Denise could withstand about a 33% decline in the market value of her assets

3-b. Liquidity: A simple analysis of Denise’s balance sheet reveals that she’s not very

liquid. In comparing current liquid assets ($870) with current bills outstanding ($1,300), it is

obvious that she cannot cover her bills and is, in fact, $430 short (i.e., $1,300 current debt – $870

If we assume that her installment loan payments for the year are about $2,000 (half the auto loan

balance and all of the furniture loan balance) and add them to the bills outstanding, the liquidity

This indicates that should her income be curtailed, she could cover only about 29% of her

3-c. Equity in her Dominant Asset: Denise’s dominant asset is her condo and property, which is

currently valued at $68,000. Since the loan outstanding on this asset is $52,000, the equity is

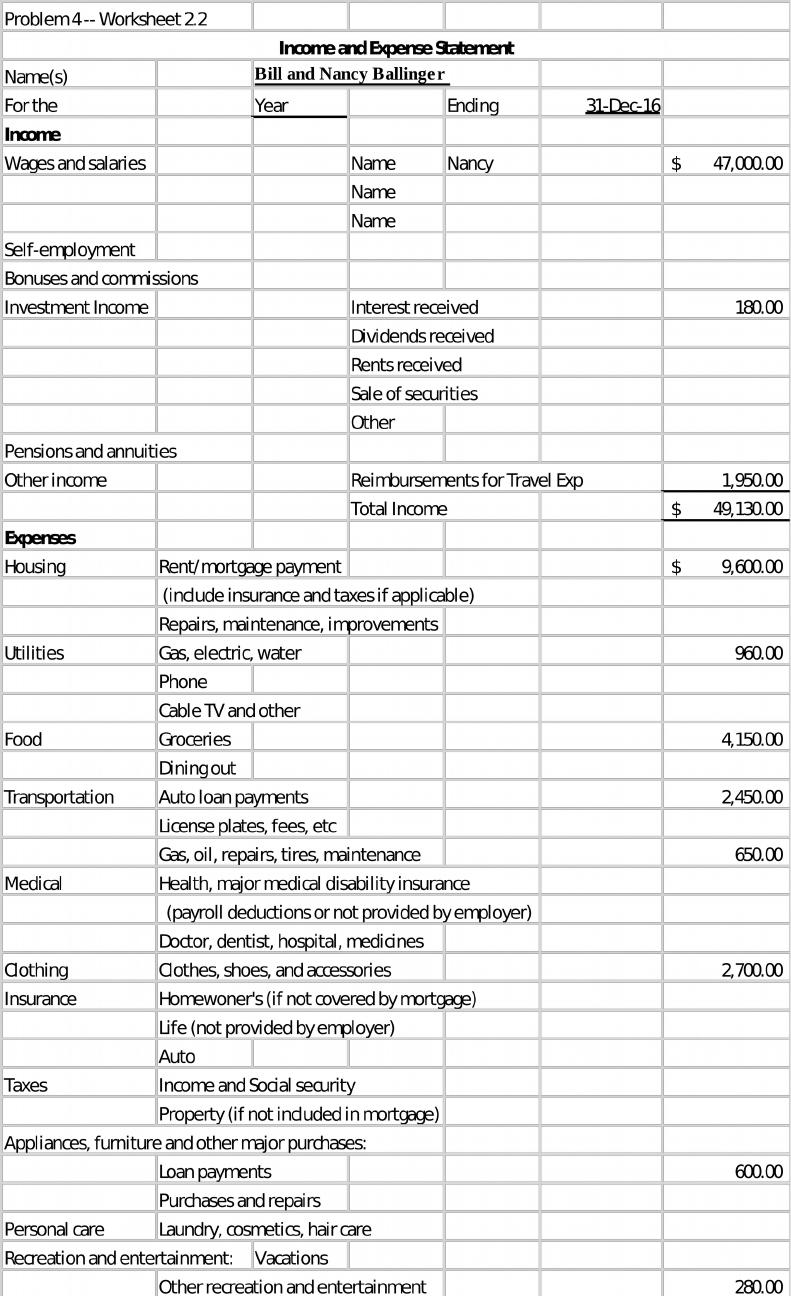

4. Preparing Income and Expense Statement: Use Worksheet 2.2. Bill and Nancy Ballinger are

about to construct their income and expense statement for the year ending December 31, 2016.

They have put together the following income and expense information for 2016:

Nancy’s salary $47,000

Interest on:

Groceries 4,150

Rent 9,600

Utilities 960

Gas and auto expenses 650

Bill’s tuition, books, and supplies 3,300

Books, magazines, and periodicals 280

Using the information provided, prepare an income and expense statement for the Ballinger’s for

the year ending December 31, 2016 (follow the form shown in Worksheet 2.2).

See worksheet on following page.

5. Preparing Cash Budget: Richard and Elizabeth Walker are preparing their 2017 cash budget.

Help the Walkers reconcile the following differences, giving reasons to support your answers.

a. Their only source of income is Richard’s salary, which amounts to $5,000 a month before

taxes. Elizabeth wants to show the $5,000 as their monthly income, whereas Richard argues

that his take-home pay of $3,917 is the correct value to show.

Like many questions it depends. If the taxes and other payroll deductions are considered out of their

control, then only the take home pay would be listed. But, since they have some options in the

b. Elizabeth wants to make a provision for fun money, an idea that Richard cannot

understand.

He asks, “Why do we need fun money when everything is provided for in the budget?”

By having an allowance for “fun money,” the Walkers have specifically set

aside a certain portion of their income for a little self-indulgence. This will

serve three basic purposes: (1) it will give a little financial independence to

6. Identifying Missing Budget Items: Here is a portion of Chuck Schwartz’s budget record for

April 2016. Fill in the blanks in columns 5 and 6. Note the answers are included. They may be

deleted if you wish to use in classroom.

Item

(1)

Amount

Budgeted

(2)

Amount Spent

(3)

Beginning

Balance

(4)

Monthly

Surplus

(Deficit)

(5)

Cumulative

Surplus

(Deficit)

(6)

Rent $550 $575 $50 -$25 $25

Utilities 150 145 15 5 20

Entertainment

7. Use Worksheet 2.3. Prepare a record of your income and expenses for the last 30 days; then

prepare a personal cash budget for the next three months. (Use the format in Worksheet 2.3, but fill

out only three months and the Total column.) Use the cash budget to control and regulate your

expenses during the next month. Discuss the impact of the budget on your spending behavior, as

well as any differences between your expected and actual spending patterns.

This question requires a personal response that will differ for each student. Therefore, a specific

example has not been provided. However, the Critical Thinking cases below provide several

The question provides an effective means to involve the student in the budgeting process. Most

students are somewhat amazed when they find out how they have actually been spending their

money. Before assigning this question, it is interesting to ask the students to estimate how they

PLEASE NOTE: Problems 8 through 10 deal with time value of money, and

solutions using both the tables and the financial calculator will be presented. The

factors are taken from the tables as follows: future value–Appendix A; future value

annuity–Appendix B; present value–Appendix C; present value annuity–Appendix D.

If using the financial calculator, set on End Mode and 1 Payment/Year. The +/-

indicates the key to change the sign of the entry, in these instances from positive to

negative. This keystroke is required on some financial calculators in order to make

the programmed equation work. Other calculators require that a “Compute” key be

pressed to attain the answer.

8. Calculating present and future values: Use future or present value techniques to solve the

following problems.

a. Starting with $15,000, how much will you have in 10 years if you can earn 6 percent on your

money? If you can earn only 4 percent?

FV = PV x FV factor 6%, 10 yrs. 15000 +/

–

PV

FV $26,862.7

2

FV = PV x FV factor 4%, 10 yrs. 15000 +/

–

PV

b. If you inherited $45,000 today and invested all of it in a security that paid a 7 percent rate of

return, how much would you have in 25 years?

FV = PV x FV factor 7%, 25 yrs. 45000 +/- PV

c. If the average new home costs $275,000 today, how much will it cost in 10 years if the price

increases by 5 percent each year?

FV = PV x FV factor 5%, 10 yrs. 275000 +/- PV

d. You think that in 15 years, it will cost $212,000 to provide your child with a 4-year college

education. Will you have enough if you take $70,000 today and invest it for the next 15 years

at 5 percent? If you start from scratch, how much will you have to save each year to have

$212,000.

No, you will have $145,530, which is less than your $212,000 goal.

FV = PV x FV factor 5%, 15 yrs. 70000 +/- PV

You will need to deposit $10,587.30 at the end of each year for 15 years In

order to reach the $212,000 goal.

PMT = FV FVA factor 4%, 15 yrs. 212000 +/- FV

e. If you can earn 4 percent, how much will you have to save each year if you want to retire in

35 years with $1 million?

You will need to invest $13,577.55 at the end of each year at a rate of 4% for the next 35 years in

order to retire with $1 million.

PMT = FV FVA factor 4%, 35 yrs. 1000000 +/- FV

f. You plan to have $750,000 in savings and investments when you retire at age 60. Assuming that

you earn an average of 8 percent on this portfolio, what is the maximum annual withdrawal you

can make over a 25-year period of retirement?

You will be able to withdraw $70,257.61 at the end of each year for 25 years if you retire with $750,000

invested at 8%.

PMT = PV PVA factor 8%, 25 yrs. 750000 +/- PV

9. Quantifying and Evaluating a Saving Goal: Over the past several years, Catherine Lee has been

able to save regularly. As a result, she has $54,188 in savings and investments today. She wants to

establish her own business in five years and feels she will need $100,000 to do so.

a. If she can earn 4 percent on her money, how much will her $54,188 in savings/investments

be worth in five years? Will Catherine have the $100,000 she needs? If not, how much more money

will she need?

If Catherine can earn 4% on her money, $54,188 will be worth about $65,947 in 5

years:

FV = PV x FV factor 4%, 5 yrs. 54188 +/- PV

9

b. Given your answer to part a, how much will Catherine have to save each year over the next

five years to accumulate the additional money? Assume that she can earn interest at a rate

of 4 percent.

b. Assuming that Catherine adds a payment to her savings at the end of each year for the next

five years so that the fifth payment comes at the end of the time period, she would have to save

$5,077.55 per year. This calculation is as follows:

FV = PMT x FVA factor 4%, 5 yrs. 34072 +/

–

FV

c. If Catherine can afford to save only $4,000 a year, then given your answer to part a,

will she have the $100,000 she needs to start her own business in five years?

If Catherine saves only $4,000 per year she would have an additional $21,664 for a total of

$87,611 ($65,947 + $21,664) and will fall $12,389 short of her $100,000 goal.

FV = PMT x FVA factor 4%, 5 yrs. 4000 +/

–

PMT

10. Funding a Retirement Goal: Chris Jones wishes to have $800,000 in a retirement fund 20

years from now. He can create the retirement fund by making a single lump-sum deposit today.

a. If he can earn 6 percent on his investments, how much must Chris deposit today to create the

retirement fund? If he can earn only 4 percent on his investments? Compare and discuss the results

of your calculations.

Note what a difference of 2% makes over the 20-year time period! You would have to initially invest

about 46% more money to end up with the same future value [($364,800 – $249,600)

$249,600].

PV = FV x PV factor 6%, 20 yrs. 800000 +/

–

FV

If Chris only earns 4%, he will need another $115,666 to meet his goal.

PV = FV x PV factor 4%, 20 yrs. 800000 +/

–

FV

b. If, upon retirement in 20 years, Chris plans to invest the $800,000 in a fund that earns 4

percent, what is the maximum annual withdrawal he can make over the following 15 years?

Chris can withdraw $71,955.39 at the end of every year for 15 years.

PV = PMT x PVA factor 4%, 15 yrs. 800000 +/

–

PV

b. How much would Chris need to have on deposit at retirement to annually withdraw

$35,000 over the 15 years if the retirement fund earns 4 percent?

To withdraw $35,000 at the end of every year for 15 years, Chris would need a retirement fund of $389,130.

PV = PMT x PVA factor 4%, 5 yrs. 35000 +/

–

PMT

d. To achieve his annual withdrawal goal of $35,000 calculated in part c, how much more than the

amount calculated in part a must Chris deposit today in an investment earning

4 percent annual interest?

11. Funding a College Goal: Dan Weaver wants to set up a fund to pay for his daughter’s

education. In order to pay her expenses, he will need $23,000 in four years, $24,300 in five years,

$26,000 in six years, and $28,000 in seven years. If he can put money into a fund that pays 4 percent

interest, what lump-sum payment must Dan place in the fund today to meet his college funding

goals?

Dan needs $81,459.60 today to fund college.

PV = FV x PV factor 4%, 4 yrs.

PV = FV x PV factor 4%, 5 yrs.

PV = FV x PV factor 4%, 6 yrs.

PV = FV x PV factor 4%, 7 yrs.

Add $19,665 + $19,974.60 + $20,540 + $21,280 = $81,459.60

Using a financial calculator, specifically a TI BAII+

CFO = 0

C01 = 0, F01 = 3

C02 = 23000, F02 = 1

12. Calculating a Future Value of an Investment: Jessica Wright has always been interested in

stocks. She has decided to invest $2,000 once every year into an equity mutual fund that is expected

to produce a return of 6 percent a year for the foreseeable future. Jessica is really curious how

much money she can reasonably expect her investment to be worth in 20 years. What would you tell

her?

It should be noted, that you are calculating this amount using an expected rate of return. Should the

FV = PMT x FVA factor 6%, 20 yrs. 2000 +/

–

PMT