Chapter

Using Financial

Statements and Budgets

Chapter 2

How Will This Affect Me?

Recent polls show that 57 percent of households have no budget, and 50 percent of Americans have less

than one month of savings set aside for emergencies.* These are scary numbers . . . and this chapter

shows what you can do to avoid being part of these alarming statistics.

Everyone knows that it’s hard to get where you need to go if you don’t know where you are. Financial

goals describe your destination, and financial statements and budgets are the tools that help you determine

exactly where you are in the journey. This chapter helps you define your financial goals and explains how

to gauge your progress carefully over time.

Hopefully most of your students have had a semester of financial accounting. If so, while this chapter

will be a review for them, they may need help understanding the differences between cash and accrual

accounting. The chapter deals with cash accounting; the previous accounting course dealt with accrual

accounting. If they have not had an accounting course, the students may have a hard time. If this

material is new to them, it will be helpful if you go over worksheets (2.1 and 2.2) and then discuss the

Financial Planning Exercises 3 (preparing a balance sheet) and 4 (preparing an income statement).

Learning Goals

LG1 Understand the relationship between financial plans and statements.

The statement above “it’s hard to get where you need to go if you don’t know where you are” is very true.

The financial statements help you to understand where you are. If not consistent with your financial goal,

you know you need to make some changes. To get a feel for where your students are in their ability to

account for their financial transactions, ask the students if they have a checking account. Then ask them

if they know the balance of that account. Exhibit 2.1 presents the impact of the financial statements on

the financial plan. The statements give feedback to the plan.

LG2 Prepare a personal balance sheet.

The Balance Sheet computes the net worth as of a given date. By comparing the current balance sheet

with the previous one from a year ago, you can see if you are moving toward your goal, or not. While

liquid assets and investments may look the same, their purpose is very different. The liquid assets are

available to spend or pay off debt, while the investments are for the long term. Recall that here we are

discussing personal balance sheet. Therefore, the concept of depreciation is not the same as with

generally accepted accounting principles (GAAP). With GAAP, depreciation is the allocation of a past

cost over its useful life. With a personal balance sheet, depreciation is a decline in value – the assets are

stated at their market value. Accordingly it is common for personal property to decline in value and real

property to increase in value – though it is not guaranteed.

Liabilities are amounts owed to others. The classification as current [due within one year] and long-term

is important. The current liabilities have to be paid in the short run, while long-term liabilities may be

paid in the future or be paid with a monthly payment – which is a current liability. Worksheet 2.1 gives a

format for a personal balance sheet—a fill-in-the-blanks approach that is useful for financial planning.

This is followed with an example for Susan and Meghan Kane.

Exhibit 2.2 gives the student hope that in the future they will have a net worth.

LG3 Generate a personal income and expense statement.

While the balance sheet reports financial position as of a given day, the income statement covers a stated

period, typically a month or year. The Financial Planning Exercises Number 5 should lead the students to

consider what income is. The exercise asks the question is income gross pay or net pay. If you take the

position that it is net pay, you are saying that you have no control over the payroll deductions. But you

can control at least some of them and your actions should be consistent with your financial plan. You

decide how many exemptions to claim for income taxes. You may have some choice as to what health

insurance you select, what life insurance to select, or perhaps other benefits such as child care or

additional health benefits.

Worksheet 2.2 lists the typical income and expenses items. The example for Susan and Meghan Kane

gives the students an example of an income statement.

LG4 Develop a good record-keeping system and use ratios to evaluate personal financial statements.

Without records, you are flying blind. It like the person who says they can spend money as long as they

have a check in their checkbook. Records give you a way to prepare financial reports which allow you to

evaluate where you are on your financial plan. There is inexpensive software that will help you keep

records, but you still have to record the transactions in order to have data for your financial statements.

With financial statements you may use ratio analysis to better understand how you are doing. Exhibit 2.5

gives a list of useful ratios. It will be useful to do some sensitivity analysis, that is, ask the students is it

good or bad to move from a solvency ratio of 35% to 50%; liquidity ratio from 13% to 8%; and so on.

This will help student understand the information in the ratio.

LG5 Construct a cash budget and use it to monitor and control spending.

The income statement reports the cash surplus or deficit for the period. But is the surplus of $2,000 good

or not. You need something to compare it to. Frequently you compare to the previous period. While that

is better than no comparison, comparing to your planned surplus is better. Your planned surplus is the

bottom line of your budget. The budget is a statement in dollars of your planned income and expenses for

the period, typically month or year. By comparing the current expenses with budgeted expenses, you

create a budget variance. That variance tells you if you need to hold the course or change your direction.

The actual income or expense compared to the budgeted amount gives you the ability to monitor and

control your expenses.

Worksheet 2.3 gives a common format for a cash budget, your planned expenditures for the year. The

cash budget for Susan and Meghan Kane is an example. Worksheet 2.4 gives an example of comparing

actual to budget and the resulting variance.

LG6 Apply time value of money concepts to put a monetary value on financial goals.

Financial plans are concerned with what future amounts you will need to be able to provide for your

desired lifestyle at that time. Since the time is in the future, typically you need to apply the concept called

the time value of money, the idea that a dollar today is worth more than a dollar received or spent in the

future. Hopefully your students have been exposed to this concept in previous courses. If not, use short

time periods [3 or 5 years] to demonstrate the concept. Perhaps use financing of a car as an example:

You can pay $20,000 today or $400 per month for 5 years. With a 6% annual rate, the present value of an

annuity of $400 per month, for 60 months, at .06/12 monthly rate, is $20,690. If you are OK with a 6%

rate, pay cash.

The book discusses using a financial calculator. You could discuss spreadsheets financial functions such

as PV, DCF, FV, or IRR. It depends upon the culture of your program whether you use calculators or

spreadsheets. The Rule of 72 is very useful for quick comparisons. Discuss it.

Financial Facts or Fantasies?

These may be used as “teasers” to get the students on the right page with you. Also, they may be used as

quizzes after you covered the material or as “pre-test questions” to get their attention.

• Whereas the balance sheet summarizes your financial condition at a given point in time, the income and

expense statement reports on your financial performance over time.

Fact: A balance sheet is like a photograph of your financial condition (covering just one day out of the

year), while an income and expense statement is like a motion picture (covering the full year or some

other time period).

• Because financial statements are used to record actual results, they’re really not that important in

personal financial planning.

Fantasy: Personal financial statements let you know where you stand financially. As such, they not only

help you set up realistic financial plans and strategies but also provide a system for monitoring the

amount of progress you’re making toward the financial goals you’ve set.

• A leased car should be listed as an asset on your personal balance sheet.

Fantasy: You are only “using” the leased car and do not own it. Consequently, it should not be included

as an asset on the balance sheet.

• Only the principal portion of a loan should be recorded on the liability side of a balance sheet.

Fact: The principal portion of a loan represents the unpaid balance and is the amount of money you owe.

In contrast, interest is a charge that will be levied over time for the use of the money.

• Generating a cash surplus is desirable, because it adds to your net worth.

Fact: You can only increase your net worth by generating a cash surplus, someone giving you additional

assets, or through increases in market values. The only one of the three you control is generating cash

surplus.

• When evaluating your income and expenses statement, primary attention should be given to the top line:

income received.

Fantasy: If you focus on only income and ignore expenses, you will quickly find yourself with a cash

deficit and your net worth will decrease. Expenses are equally important and must be controlled.

Financial Facts or Fantasies?

These may be used as a quiz or as a pre-test to get the students interested.

1. True False Whereas the balance sheet summarizes your financial condition at a given point in time,

the income and expense statement reports on your financial performance over time.

2. True False Because financial statements are used to record actual results, they’re really not that

important in personal financial planning.

3. True False A leased car should be listed as an asset on your personal balance sheet.

4. True False Only the principal portion of a loan should be recorded on the liability side of a balance

sheet.

5. True False Generating a cash surplus is desirable, because it adds to your net worth.

6. True False When evaluating your income and expenses statement, primary attention should be given

to the top line: income received.

YOU CAN DO IT NOW

The “You Can Do It Now” cases may be assigned to the students as short cases or problems. They will

help make the topic more real or relevant to the students. In most cases, it will only take about ten

minutes to do, that is, until the student starts looking around at the web site. But they will learn by doing

so.

Track Your Expenses

It’s easy for spending to become so automatic that we’re not aware we’re doing it. So where does your

money go? The only way to find out is to keep track of it. Writing down what you spend in a paper

journal or using an app like Expensify (www.expensify.com) is simple and will make you more aware of

where your money goes. Knowing where you are will probably make you feel better too – so do it now.

Save Automatically

We all know we should save regularly. One way to create a savings “habit” is to literally make it

automatic.

Open a savings account apart from your checking account. This will separate your savings from what you

have available to spend. And then set up an automatic deposit to your savings account each month. This

sets your “habit.” You can do it now.

Financial Impact of Personal Choices

Read and think about the choices being made. Do you agree or not? Ask the students to discuss the

choices being made.

No Budget, No Plan: Sean Bought a Boat!

Sean is 28 and has a good job as a sales rep. He’s always found budgeting boring and has been intending

to start a financial plan for years.

Recently Sean went out with some friends on a rented boat to fish. He had a great time and saw a boat

sale on his way home. Before he knew it, the salesman convinced Sean that the deal was just too good to

pass up. So Sean bought a $10,000 boat and financed 80 percent of the cost for the next 5 years. Sean

now finds himself relying more on his credit card to get by each month.

What if Sean had kept track of his money, used a budget, and had a set of financial goals? Knowing where

his money went and having a financial plan would have increased the chance that Sean would make more

deliberate, informed financial decisions.

Solutions to “Test Yourself” Questions

2-1 What are the two types of personal financial statements? What is a budget, and how does it differ

from personal financial statements? What role do these reports play in a financial plan?

Personal financial statements provide important information needed in the personal financial planning

process. The balance sheet describes your financial condition [that is what assets and liabilities you have]

at one point in time. The income and expense statement measures financial performance [cash surplus or

2-2 Describe the balance sheet, its components, and how you would use it in personal financial

planning. Differentiate between investments and real and personal property.

The balance sheet summarizes your financial position by showing your assets (what you own listed at fair

market value), your liabilities (what you owe), and your net worth (the difference between assets and

Investments are intangible assets that have market value [such as stock] and you hold in hpes of future

2-3 What is the balance sheet equation? Explain when a family may be viewed as technically

insolvent.

The balance sheet equation is:

Net Worth = Total Assets – Total Liabilities

2-4 Explain two ways in which net worth could increase (or decrease) from one period to the next.

There are basically two ways to achieve an increase in net worth. First, one could prepare a

budget for the pending period to specifically provide for an increase in net worth by acquiring

more assets and/or paying down debts. This is accomplished by planning and requires strict

2-5 What is an income and expense statement? What role does it serve in personal financial

planning?

The income and expense statement captures the result of financial activities that you hoped would

increase your wealth summarized for a month or a year. In personal financial planning, the

2-6 Explain what cash basis means in this statement: “An income and expense statement

should be prepared on a cash basis.” How and where are credit purchases shown when statements

are prepared on a cash basis?

The cash basis only records income that is received in cash or expenses that are paid in cash

during the period. It ignores any amount that you are due [receivables] or that you will have to

pay in the future [liabilities]. Payments on liabilities should be divided into payment of interest

2-7 Distinguish between fixed and variable expenses, and give examples of each.

Fixed expenses are contractual, predetermined expenses that are made each period, such as rent,

2-8 Is it possible to have a cash deficit on an income and expense statement? If so, how?

Yes, a cash deficit appears on an cash basis income and expense statement whenever the period’s

expenses exceed income. Deficit spending is made possible by using up an asset, such as taking

2-9 How can accurate records and control procedures be used to ensure the effectiveness of the

personal financial planning process?

Before you can set realistic goals, develop your financial plans, or effectively manage

2-10 Describe some of the areas or items you would consider when evaluating your balance sheet

and income and expense statement. Cite several ratios that could help in this effort.

Ratios are used to relate items from the financial statements. These ratios provide useful information for

specific decisions. From the Balance sheet:

Liquidity ratio: Total liquid assets divided by total current debts; measures the ability to pay current

debts.

From the Income Statement:

2-11 Describe the cash budget and its three parts. How does a budget deficit differ from a budget

surplus?

A cash budget is a summary of estimated cash income and cash expenses for a specific time period,

typically a year. The three parts of the cash budget include: the income section where all expected income

is listed; the expense section where expected expenses are listed by category; and the surplus or deficit

2-12 The Gonzales family has prepared their annual cash budget for 2016. They have divided it into

12 monthly budgets. Although only 1 monthly budget balances, they have managed to balance the

overall budget for the year. What remedies are available to the Gonzales family for meeting the

monthly budget deficits?

Monthly deficits may be handled by shifting expenses to a later month or income to an earlier month. If

that is not possible, the Gonzales family may withdraw an amount from savings or borrow a short-term

2-13 Why is it important to analyze actual budget surpluses or deficits at the end of each month?

By examining end-of-month budget balances, and the associated surpluses or deficits for all

accounts, a person can initiate any required corrective actions to assure a balanced budget for the

2-14 Why is it important to use time value of money concepts in setting personal financial goals?

A dollar today and a dollar in the future will be able to purchase different amounts of goods and

services, because if you have a dollar today, you can invest it and it will grow to more than a

dollar in the future. At the same time, inflation works against the dollar, because rising prices

2-15 What is compounding? Explain the rule of 72.

Interest is earned over a given period of time. When interest is compounded, this given period of

time is broken into segments, such as months. Interest is then calculated one segment at a time,

with the interest earned in one segment added back to become part of the principal for the next

2-16 When might you use future value? Present value? Give specific examples.

Future value calculations show how much an amount will grow over a given time period. Future

value is used to evaluate investments and to determine how much to save each year to accumulate

Solutions to Financial Planning Exercises

1. Preparing Financial Statements: Chad Livingston is preparing his balance sheet and

income and expense statement for the year ending June 30, 2016. He is having difficulty

classifying six items and asks for your help. Which, if any, of the following transactions are

assets, liabilities, income, or expense items?

a. Chad rents a house for $1,350 a month.

b. On June 21, 2016, Chad bought diamond earrings for his wife and charged them using his

MasterCard. The earrings cost $900, but he hasn’t yet received the bill.

The purchase will result in a new asset, personal property for $900. Since he purchase using a

c. Chad borrowed $3,500 from his parents last fall, but so far, he has made no payments to

them.

Since no loan payments were made during the period, a corresponding expense would not appear.

Whether or not the “loan” is a real loan or a gift from the parents is a question of fact to be

d. Chad makes monthly payments of $225 on an installment loan; about half of it is interest,

and the balance is repayment of principal. He has 20 payments left, totaling $4,500.

The income statement will show an expense: payment of loan $225 per month times 12 months, a

e. Chad paid $3,800 in taxes during the year and is due a tax refund of $650, which he hasn’t

yet received.

The payment of taxes is an expense recorded as paid, typically monthly or when paycheck is

f. Chad invested $2,300 in some common stock.

2. Projecting Financial Statements: Put yourself 10 years into the future. Construct a fairly

detailed and realistic balance sheet and income and expense statement reflecting what you

would like to achieve by that time.

While everyone’s financial statements will differ based on their own

expectation of the future, each should have similar elements such as: assets

like a home, automobiles and investments; liabilities like a mortgage, an auto

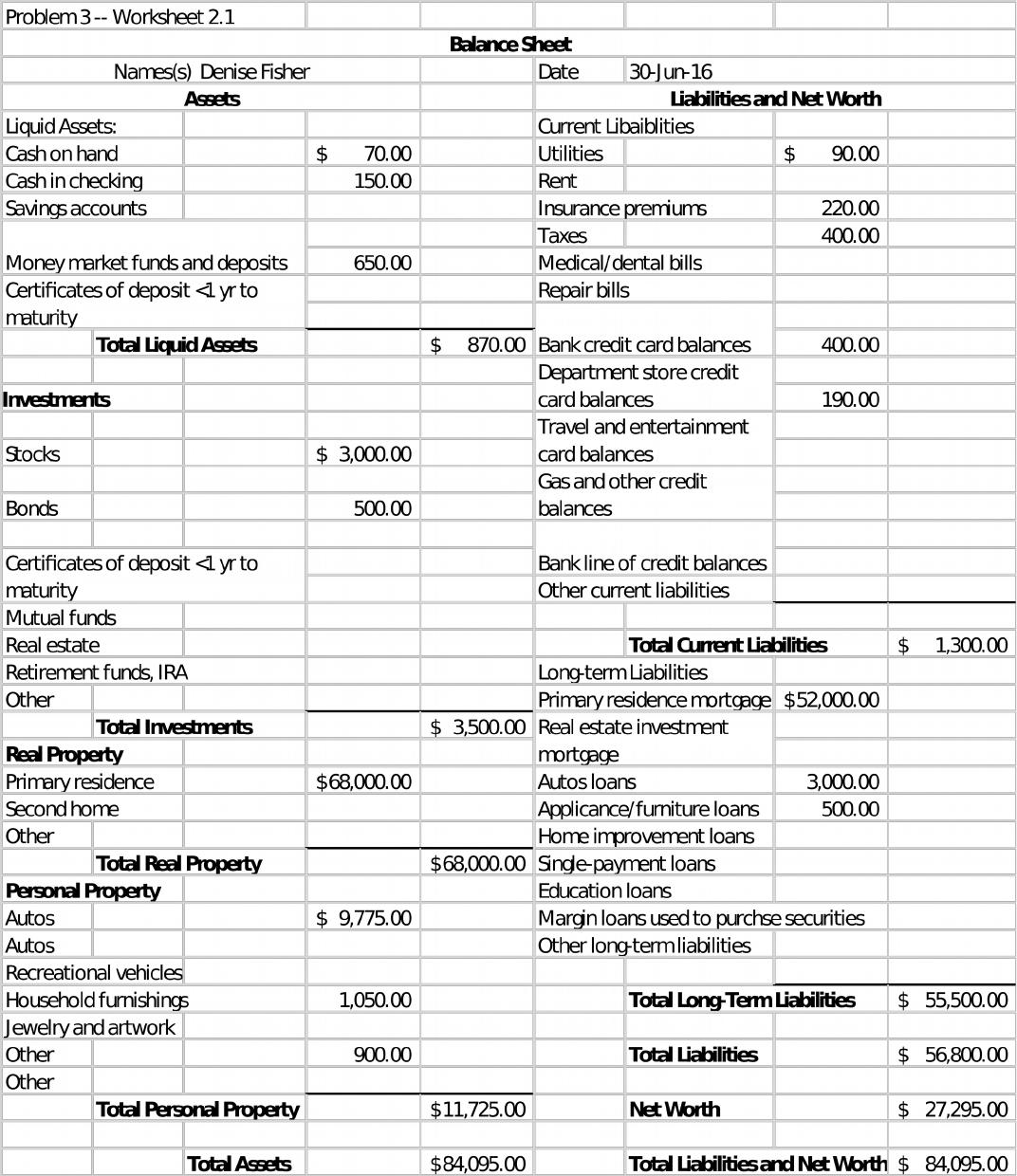

3. Preparing Personal Balance Sheet: Use Worksheet 2.1. Denise Fisher’s banker has asked her to

submit a personal balance sheet as of June 30, 2016, in support of an application for a $6,000 home

improvement loan. She comes to you for help in preparing it. So far, she has made the following list

of her assets and liabilities as of June 30, 2016:

Cash on hand $ 70

Balance in checking account 180

Bills outstanding:

Telephone $ 20

Electricity 70

Condo and property 68,000

Condo mortgage loan 52,000

Automobile: 2012 Honda Civic 9,775

Installment loan balances:

Personal property:

Investments:

From the data given, prepare Denise Fisher’s balance sheet, dated June 30, 2016 (follow the balance

sheet form shown in Worksheet 2.1). Then evaluate her balance sheet relative to the following

factors: (a) solvency, (b) liquidity, and (c) equity in her dominant asset.

See following page for Worksheet 2.1 for Denise Fisher.