d. 2. Suppose you write 1 call option and buy Ns shares of stock. How many shares

must you buy to create a portfolio with a riskless payoff (which is called a hedge

portfolio)? What is the payoff of the portfolio?

Answer:

:

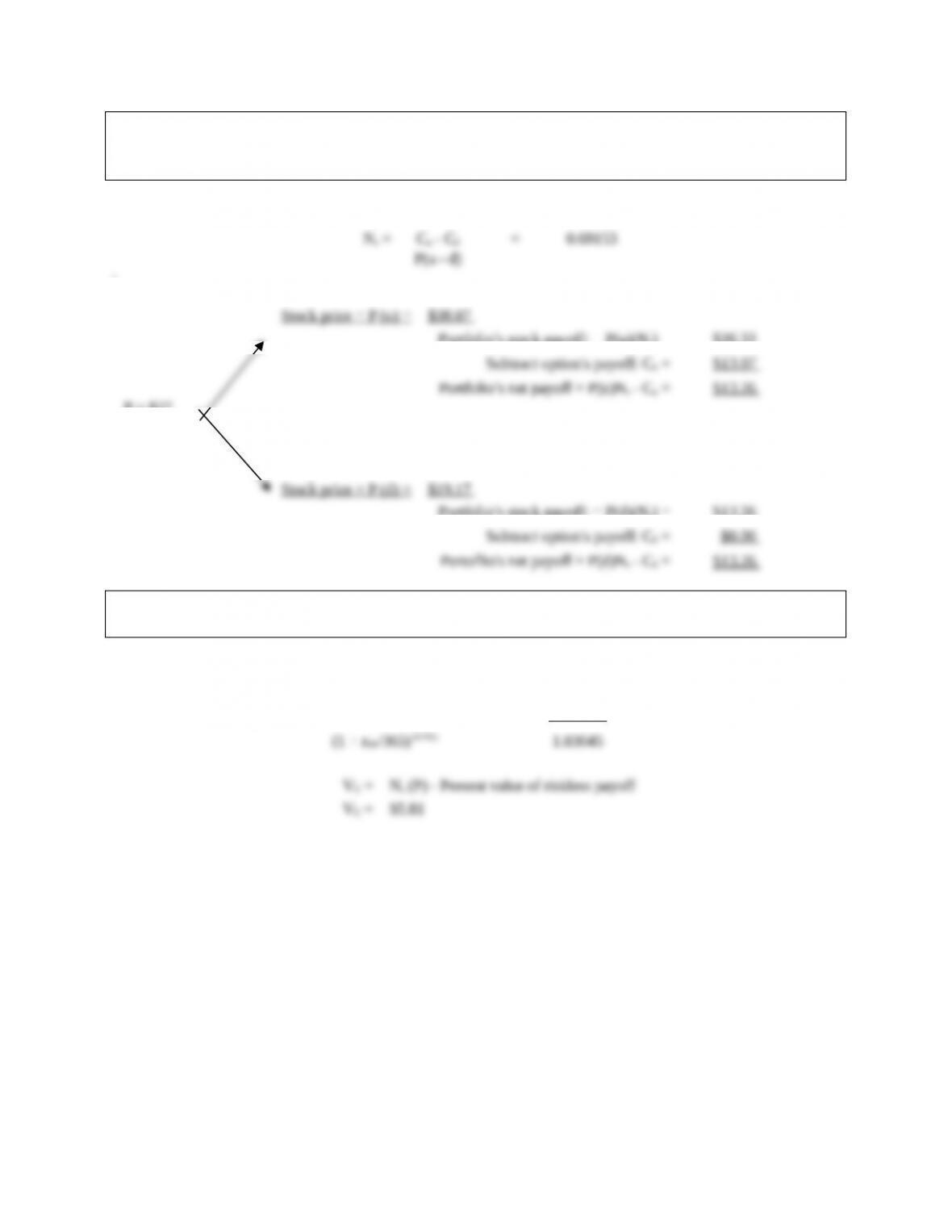

Portfolio’s stock payoff: = P(u)(Ns) = $26.33

P = $27

Portfolio’s stock payoff: = P(d)(Ns) = $13.26

d. 3. What is the present value of the hedge portfolio’s riskless payoff? What is the

value of the call option?

Answer:

PV of payoff = Payoff = $13.2567 = $12.865

Mini Case: 8 – 1

© 2017 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or

in part.

d. 4. What is a replicating portfolio? What is arbitrage?

Answer: If you borrow an amount equal to the present value of the hedge portfolio’s

The option’s value must be the same as the portfolio’s cost, otherwise you would

have an opportunity for arbitrage, which is a situation in which you have none of

e. In 1973, Fischer Black and Myron Scholes developed the Black-Scholes Option

Pricing Model (OPM).

1. What assumptions underlie the OPM?

Answer: The assumptions which underlie the OPM are as follows:

The stock underlying the call option provides no dividends during the life of the

option.

Mini Case: 8 – 2

© 2017 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or

in part.

e. 2. Write out the three equations that constitute the model.

Answer: The OPM consists of the following three equations:

V = P[N(d1) –

tr

RF

Xe

[N(d2)].

d1 =

t

t)]/2(r[)P/Xln(

2

RF

.

d2 = d1 –

t

.

Here,

V = current value of a call option with time t until expiration.

P = current price of the underlying stock.

N(di) = probability that a deviation less than di will occur in a standard normal

rRF = risk-free interest rate.

Mini Case: 8 – 3

© 2017 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or

in part.

e. 3. What is the value of the following call option according to the OPM?

Stock Price = $27.00.

Strike Price = $25.00

Time To Expiration = 6 Months = 0.5 years.

Risk-Free Rate = 6.0%.

Stock Return Standard Deviation = 0.49.

Answer: The input variables are:

Now, we proceed to use the OPM:

d1 =

5.0)49.0(

)5.0)](/20.4906.0[()$27/$25ln(

2

= 0.4819.

d2 = 0.4819 – (0.49)

5.0

= 0.1355.

N(d1) = 0.6851 (From Excel NORMSDIST function).

N(d2) = 0.5539.

Therefore,

Mini Case: 8 – 4

© 2017 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or

in part.

f. What impact does each of the following call option parameters have on the value

of a call option?

1. Current Stock Price

2. Strike Price

3. Option’s Term To Maturity

4. Risk-Free Rate

5. Variability Of The Stock Price

Answer: 1. The value of a call option increases (decreases) as the current stock price

increases (decreases).

3. As the expiration date of the option is lengthened, the value of the option

4. As the risk-free rate increases, the value of the option tends to increase as well.

5. The greater the variance in the underlying stock price, the greater the possibility

g. What is put-call parity?

Answer: Put-call parity specifies the relationship between puts, calls, and the underlying stock

price that must hold to prevent arbitrage:

Mini Case: 8 – 5

© 2017 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or

in part.