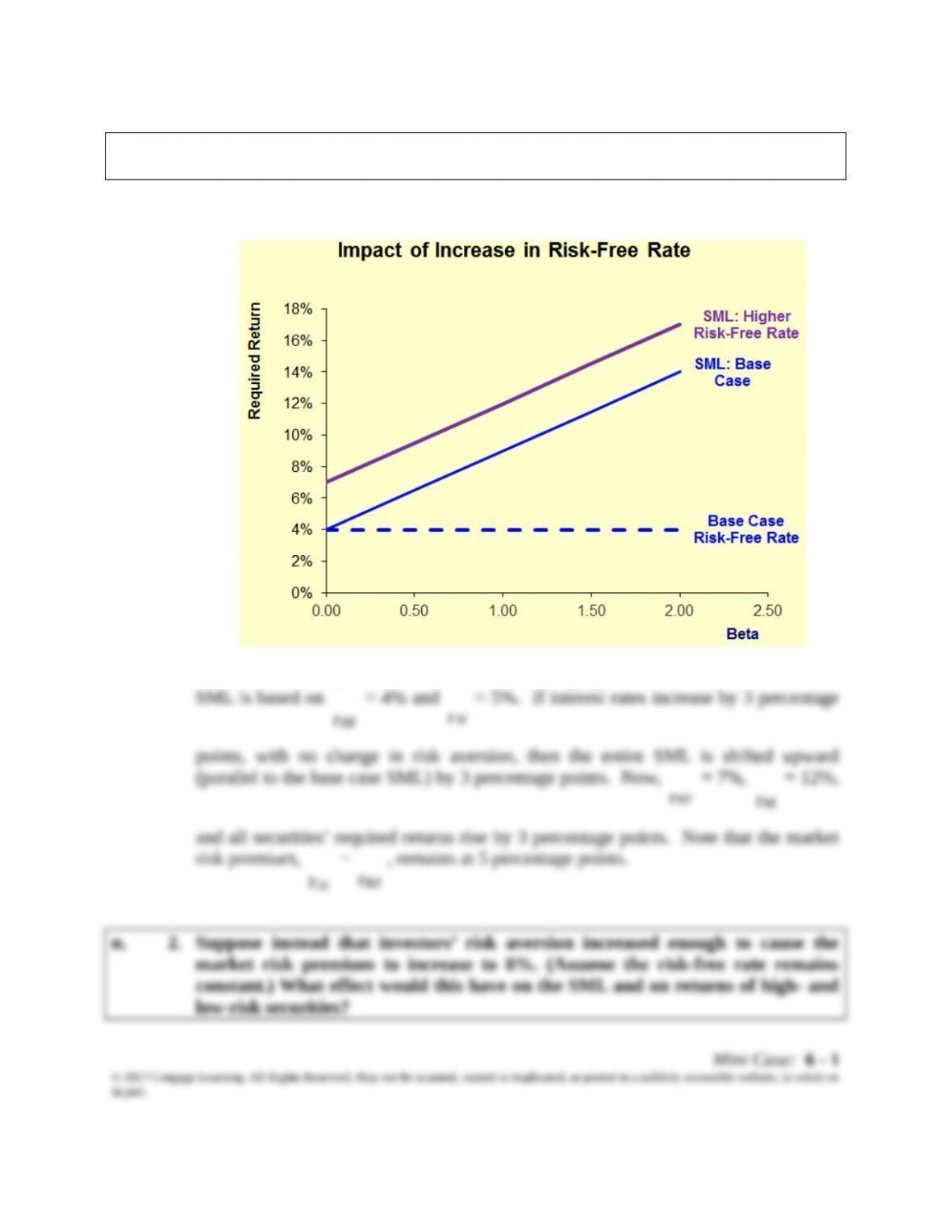

n. 1. Suppose the risk-free rate goes up to 7%. What effect would higher interest rates have

on the SML and on the returns required on high-risk and low-risk securities?

Answer: The SML is shifted higher, but the slope is unchanged.

Here we have plotted the SML for betas ranging from 0 to 2.0. The base case

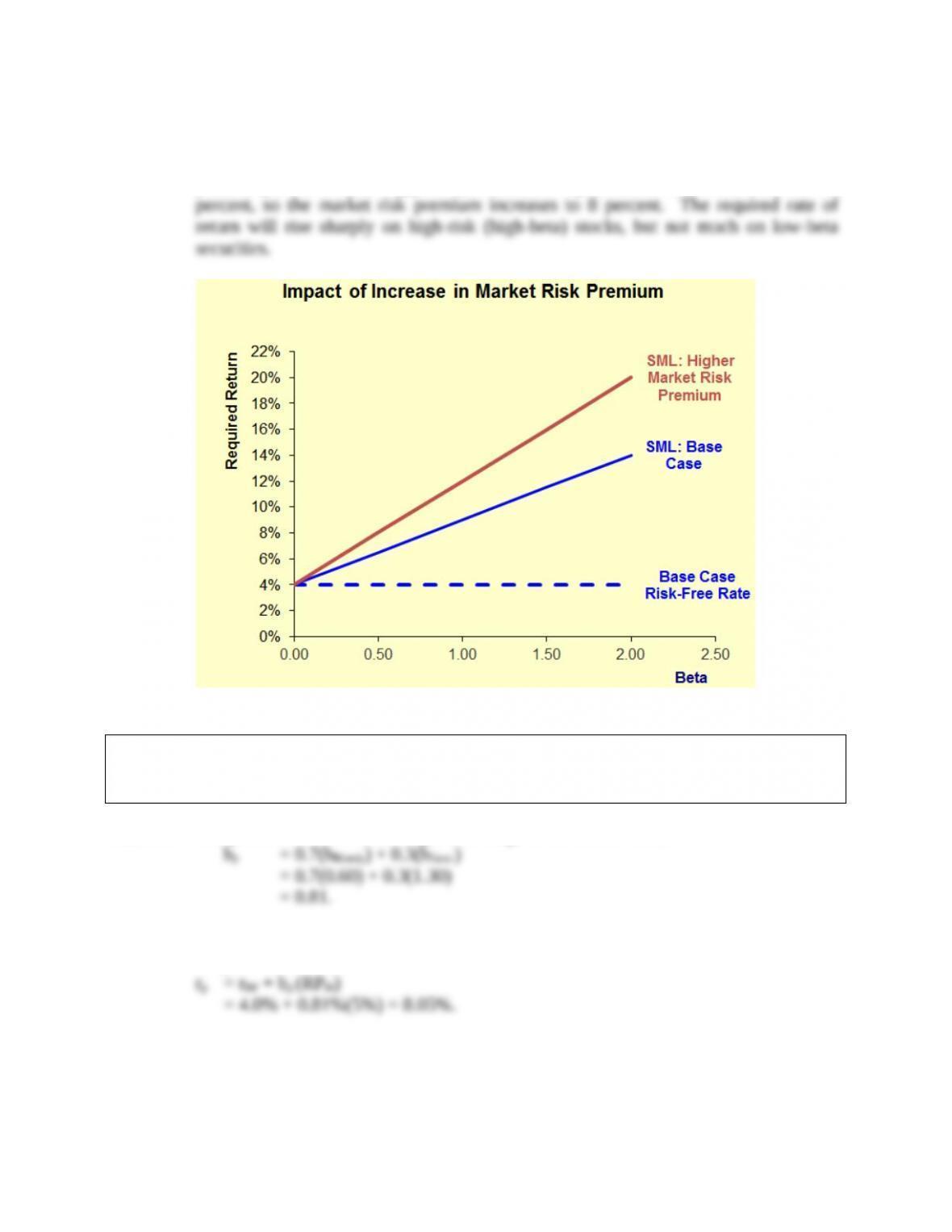

Answer: When investors’ risk aversion increases, the SML is rotated upward about the

y-intercept, which is rRF. Suppose rRF remains at 4 percent, but now rM increases to 12

o. Your client decides to invest $1.4 million in Blandy stock and $0.6 million in

Gourmange stock. What are the weights for this portfolio? What is the

portfolio’s beta? What is the required return for this portfolio?

Answer: The portfolio’s beta is the weighted average of the stocks’ betas:

There are two ways to calculate the portfolio’s expected return. First, we can use

the portfolio’s beta and the SML:

Mini Case: 6 – 2

© 2017 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or

in part.

Second, we can find the weighted average of the stocks’ expected returns:

rp=

n

1i

iirw

p. Jordan Jones (JJ) and Casey Carter (CC) are portfolio managers at your firm.

Each manages a well-diversified portfolio. Your boss has asked for your opinion

regarding their performance in the past year. JJ’s portfolio has a beta of 0.6 and

had a return of 8.5%; CC’s portfolio has a beta of 1.4 and had a return of 9.5%.

Which manager had better performance? Why?

Answer: To evaluate the managers, calculate the required returns on their portfolios using the

SML and compare the actual returns to the required returns, as follows:

Portfolio Manager

JJ CC

Portfolio beta = 0.7 1.4

Notice that JJ’s portfolio had a higher return than investors required (given the

q. What does market equilibrium mean? If equilibrium does not exist, how will it

be established?

Answer: Market equilibrium means that marginal investors (the ones whose trades determine

Mini Case: 6 – 3

© 2017 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or

in part.

Market price = Intrinsic value

Market equilibrium also means that the expected return a security must equal its

required return (which reflects the security’s risk).

^

r

= r

If the market is not in equilibrium, then some assets will be undervalued and/or

some will be overvalued. If this is the case, traders will attempt to make a profit by

r. What is the Efficient Markets Hypothesis (EMH) and what are its three forms?

What evidence supports the EMH? What evidence casts doubt on the EMH?

Answer: The EMH is the hypothesis that securities are normally in equilibrium, and are

“priced fairly,” making it impossible to “beat the market.”

Weak-form efficiency says that investors cannot profit from looking at past

Semistrong-form efficiency says that all publicly available information is

Strong-form efficiency says that all information, even inside information, is

Most empirical evidence supports weak-form EMH because very few trading

Most empirical evidence supports the semistrong-form EMH. For example, the

Mini Case: 6 – 4

© 2017 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or

in part.

In addition, there are times when a market becomes overvalued. This is often

Mini Case: 6 – 5

© 2017 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or

in part.

Web Appendix 6B

Calculating Beta Coefficients With a Financial Calculator

Solutions to Problems

6B-1 a.

c. 1. Stand-alone risk as measured by would be greater, but beta and hence systematic

2. CAPM assumes that company-specific risk will be eliminated in a portfolio, so the

d. 1. The stock‘s variance and would not change, but the risk of the stock to an investor

Web Solutions: 6B – 6

© 2017 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or

in part.

(%)r

Y

2. Because of a relative scarcity of such stocks and the beneficial net effect on portfolios

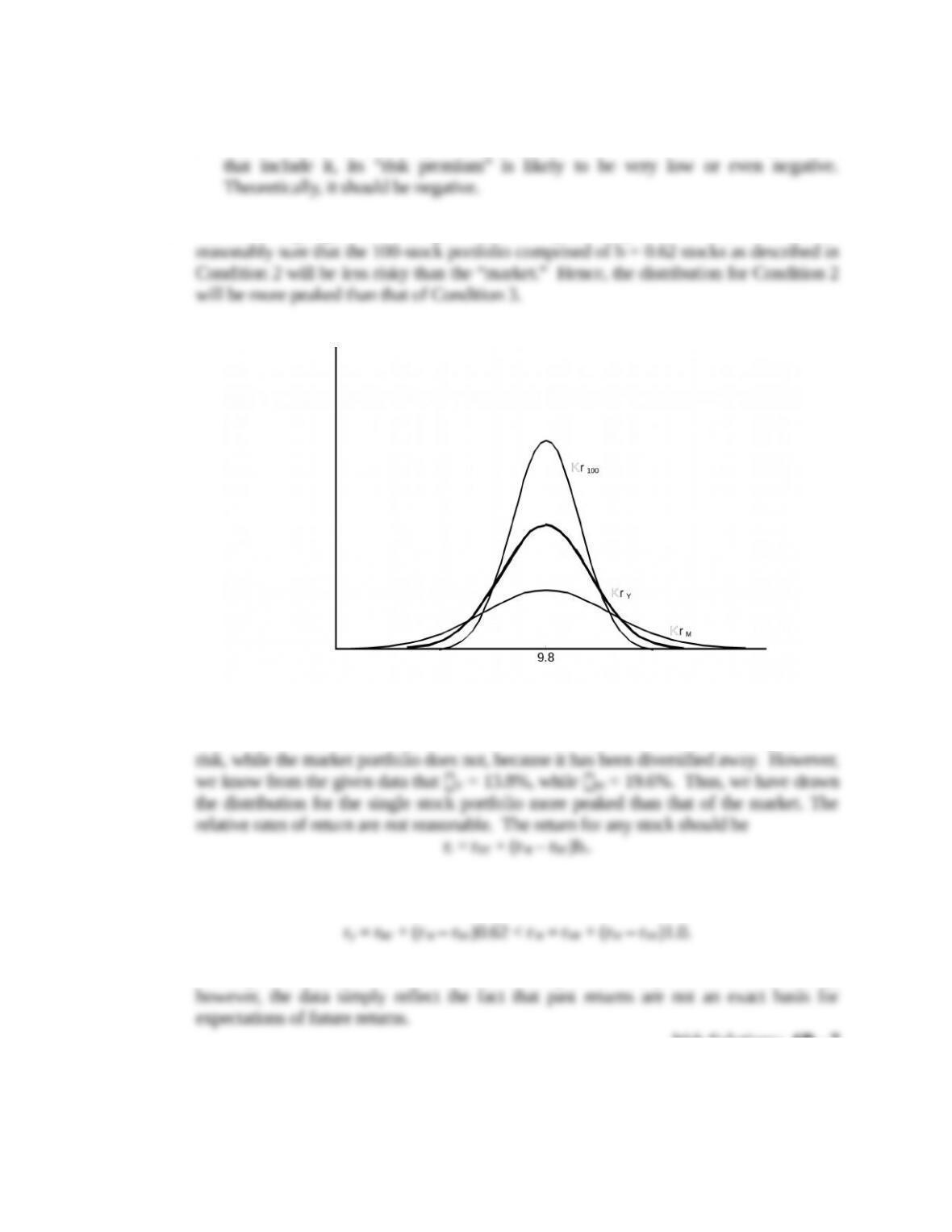

e. The following figure shows a possible set of probability distributions. We can be

We can also say on the basis of the available information that Y is smaller than M;

Stock Y’s market risk is only 62% of the “market,” but it does have company-specific

Stock Y has b = 0.62, while the average stock (M) has b = 1.0; therefore,

A disequilibrium exists—Stock Y should be bid up to drive its yield down. More likely,

Web Solutions: 6B – 7

© 2017 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or

in part.

g. The beta would decline to 0.53. A decline indicates that the stock has become less risky;

6B-2 a.

The slope of the characteristic line is the stock’s beta coefficient.

Slope =

M

i

r

r

Run

Rise

.

SlopeA = BetaA =

20.1500.29

20.1500.29

= 1.0.

Web Solutions: 6B – 8

© 2017 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or

in part.

The graph of the SML is as follows:

The equation of the SML is thus:

c. Required rate of return on Stock A:

Required rate of return on Stock B:

C

r

ˆ

Return on Stock C if it is in equilibrium:

Web Solutions: 6B – 9

© 2017 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or

in part.

C

r

ˆ

A stock is in equilibrium when its required return is equal to its expected return.

Web Solutions: 6B – 10

© 2017 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or

in part.