6-10 Portfolio beta =

$4,000,000

$400,000

(1.50) +

$4,000,000

$600,000

(-0.50)

+

$4,000,000

$1,000,000

(1.25) +

$4,000,000

$2,000,000

(0.75)

Alternative solution: First compute the return for each stock using the CAPM equation

[rRF + (rM – rRF)b], and then compute the weighted average of these returns.

rRF = 6% and rM – rRF = 8%.

Stock Investment Beta r = rRF + (rM – rRF)b Weight

A $ 400,000 1.50 18% 0.10

6-11 First, calculate the beta of what remains after selling the stock:

Answers and Solutions: 6 – 1

© 2017 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or

in part.

6-12 We know that bR = 1.50, bS = 0.75, rM = 13%, rRF = 7%.

6-13 The answers to a, b, and c are given below:

¯A ¯B Portfolio

2012 (20.00%) (5.00%) (12.50%)

2013 42.00 15.00 28.50

d. A risk-averse investor would choose the portfolio over either Stock A or Stock B

c. bp = 0.8(1.3471) + 0.2(0.6508) = 1.2078.

Answers and Solutions: 6 – 2

© 2017 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or

in part.

SOLUTION TO SPREADSHEET PROBLEM

6-15 The detailed solution for the spreadsheet problem is available in the file Ch06-P15 Build

a Model Solution.xlsx on the textbook’s Web site.

Answers and Solutions: 6 – 3

© 2017 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or

in part.

Assume that you recently graduated and landed a job as a financial planner

with Cicero Services, an investment advisory company. Your first client recently inherited

some assets and has asked you to evaluate them. The client owns a bond portfolio with $1

million invested in zero coupon Treasury bonds that mature in 10 years. The client also has

$2 million invested in the stock of Blandy, Inc., a company that produces

meat-and-potatoes frozen dinners. Blandy’s slogan is “Solid food for shaky times.”

Unfortunately, Congress and the president are engaged in an acrimonious dispute over the budget

and the debt ceiling. The outcome of the dispute, which will not be resolved until the end of the

year, will have a big impact on interest rates one year from now. Your first task is to determine

the risk of the client’s bond portfolio. After consulting with the economists at your firm, you

have specified five possible scenarios for the resolution of the dispute at the end of the year. For

each scenario, you have estimated the probability of the scenario occurring and the impact on

interest rates and bond prices if the scenario occurs. Given this information, you have calculated

the rate of return on 10-year zero coupon Treasury bonds for each scenario. The probabilities and

returns are shown below:

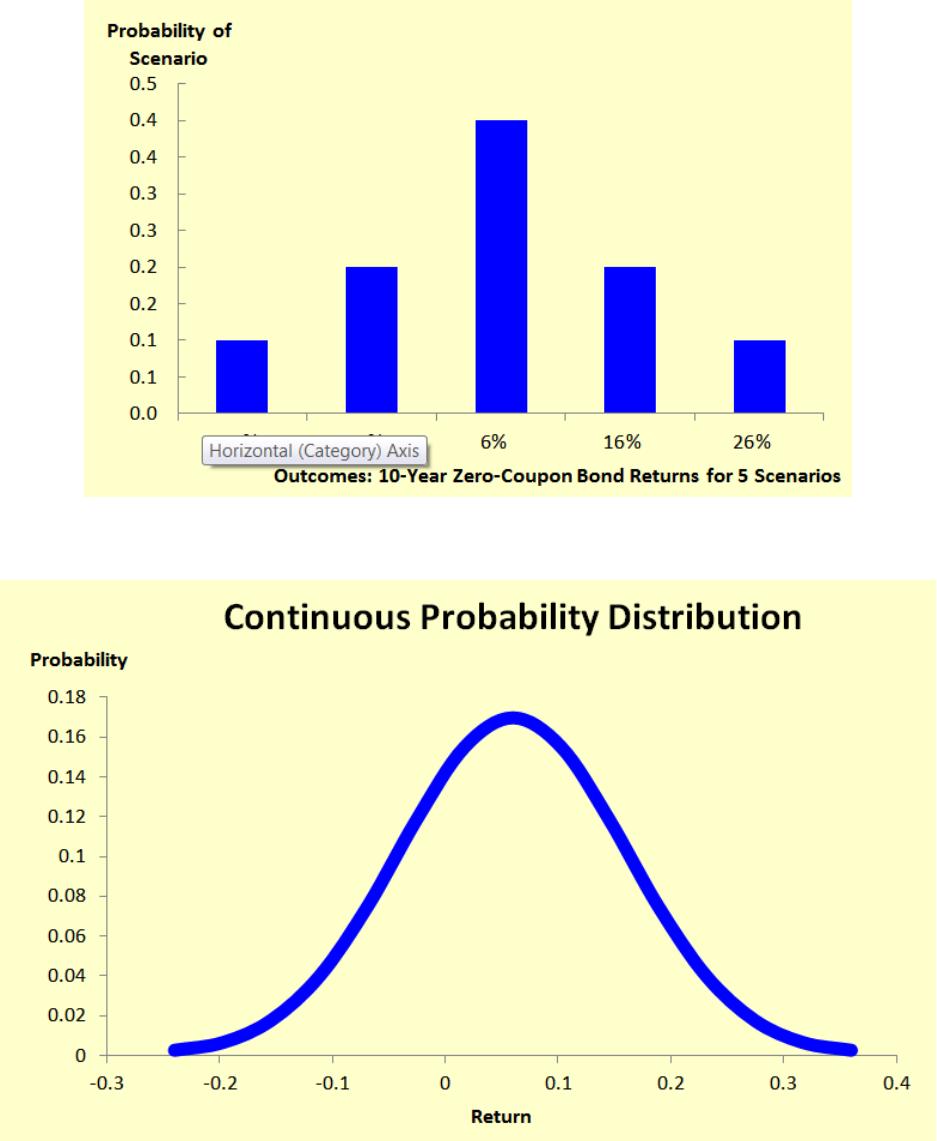

Scenario

Probability

of Scenario

Return on a 10-Year Zero

Coupon Treasury Bond

During the Next Year

Worst Case 0.10 −14%

Poor Case 0.20 −4%

Most Likely 0.40 6%

Good Case 0.20 16%

Best Case 0.10 26%

1.00

You have also gathered historical returns for the past 10 years for Blandy, Gourmange

Corporation (a producer of gourmet specialty foods), and the stock market.

Answers and Solutions: 6 – 4

© 2017 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or

in part.

MINI CASE

Historical Stock Returns

Year Market Blandy Gourmange

1 30% 26% 47%

2 7 15 −54

3 18 −14 15

Average return: 8.0% ? 9.2%

The risk-free rate is 4% and the market risk premium is 5%.

a. What are investment returns? What is the return on an investment that costs

$1,000 and is sold after 1 year for $1,060?

Answer: Investment return measures the financial results of an investment. They may be

b. Graph the probability distribution for the bond returns based on the 5 scenarios.

What might the graph of the probability distribution look like if there were an

infinite number of scenarios (i.e., if it were a continuous distribution and not a

discrete distribution)?

Answers and Solutions: 6 – 5

© 2017 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or

in part.

Answer: Here is the probability distribution for the five possible outcomes:

A continuous distribution might look like this:

Answers and Solutions: 6 – 6

© 2017 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or

in part.

c. Use the scenario data to calculate the expected rate of return for the 10-year zero

coupon Treasury bonds during the next year.

Answer: The expected rate of return,

r

, is expressed as follows:

.

rP

= r

ii

n

1=i

Here pi is the probability of occurrence of the ith state, ri is the estimated rate of return

for that state, and n is the number of states. Here is the calculation:

Answers and Solutions: 6 – 7

© 2017 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or

in part.

d. What is stand-alone risk? Use the scenario data to calculate the standard

deviation of the bond’s return for the next year.

Answer: Stand-alone risk is the risk of an asset if it is held by itself and not as a part of a

portfolio. Standard deviation measures the dispersion of possible outcomes, and for a

single asset, the stand-alone risk is measured by standard deviation.

The variance and standard deviation are calculated as follows:

)r

ˆ

–

r

(

p

= σ

i

i2

i

n

1 = i

2

.

)r

ˆ

–

r

(

p

= σ

i

i2

i

n

1 = i

22

σ2 = [(0.1) (-0.14 – 0.06)2 + (0.2) (-0.04 – 0.06)2 + (0.4) (0.06 – 0.06)2