Chapter 6

Risk and Return

ANSWERS TO END-OF-CHAPTER QUESTIONS

6-1 a. Stand-alone risk is only a part of total risk and pertains to the risk an investor takes by

holding only one asset. Risk is the chance that some unfavorable event will occur.

d. The standard deviation (σ) is a statistical measure of the variability of a set of

e. A risk averse investor dislikes risk and requires a higher rate of return as an

f. A risk premium is the difference between the rate of return on a risk-free asset and the

g. CAPM is a model based upon the proposition that any stock’s required rate of return

h. The expected return on a portfolio.

r

p, is simply the weighted-average expected

i. Correlation is the tendency of two variables to move together. A correlation

coefficient (ρ) of +1.0 means that the two variables move up and down in perfect

j. Market risk is that part of a security’s total risk that cannot be eliminated by

diversification. It is measured by the beta coefficient. Diversifiable risk is also known

k. The beta coefficient is a measure of a stock’s market risk, A stock with a beta greater

l. The security market line (SML) represents in a graphical form, the relationship

m. The slope of the SML equation is (rM – rRF), the market risk premium. The slope of the

n. Equilibrium is the condition under which the expected return on a security is just

equal to its required return,

r

= r, and the market price is equal to the intrinsic value.

The Efficient Markets Hypothesis (EMH) states (1) that stocks are always in

equilibrium and (2) that it is impossible for an investor to consistently “beat the

Weak-form efficiency assumes that all information contained in past price

movements is fully reflected in current market prices. Thus, information about recent

o. The Fama-French 3-factor model has one factor for the excess market return (the

market return minus the risk free rate), a second factor for size (defined as the return

p. Most people don’t behave rationally in all aspects of their personal lives, and

Anchoring bias is the human tendency to “anchor” too closely on recent events

6-3 Security A is less risky if held in a diversified portfolio because of its lower beta and

6-4 The risk premium on a high beta stock would increase more.

If risk aversion increases, the slope of the SML will increase, and so will the market risk

6-5 According to the Security Market Line (SML) equation, an increase in beta will increase

a company’s expected return by an amount equal to the market risk premium times the

SOLUTIONS TO END-OF-CHAPTER PROBLEMS

6-1 Investment Beta

6-2 rRF = 4%; rM = 12%; b = 0.8; rs = ?

6-3 rRF = 5%; RPM = 7%; rM = ?

6-4 Predicted return = ai + bi(rM,t rRF,t) + ci(rSMB,t) + di(rHML,t)

r

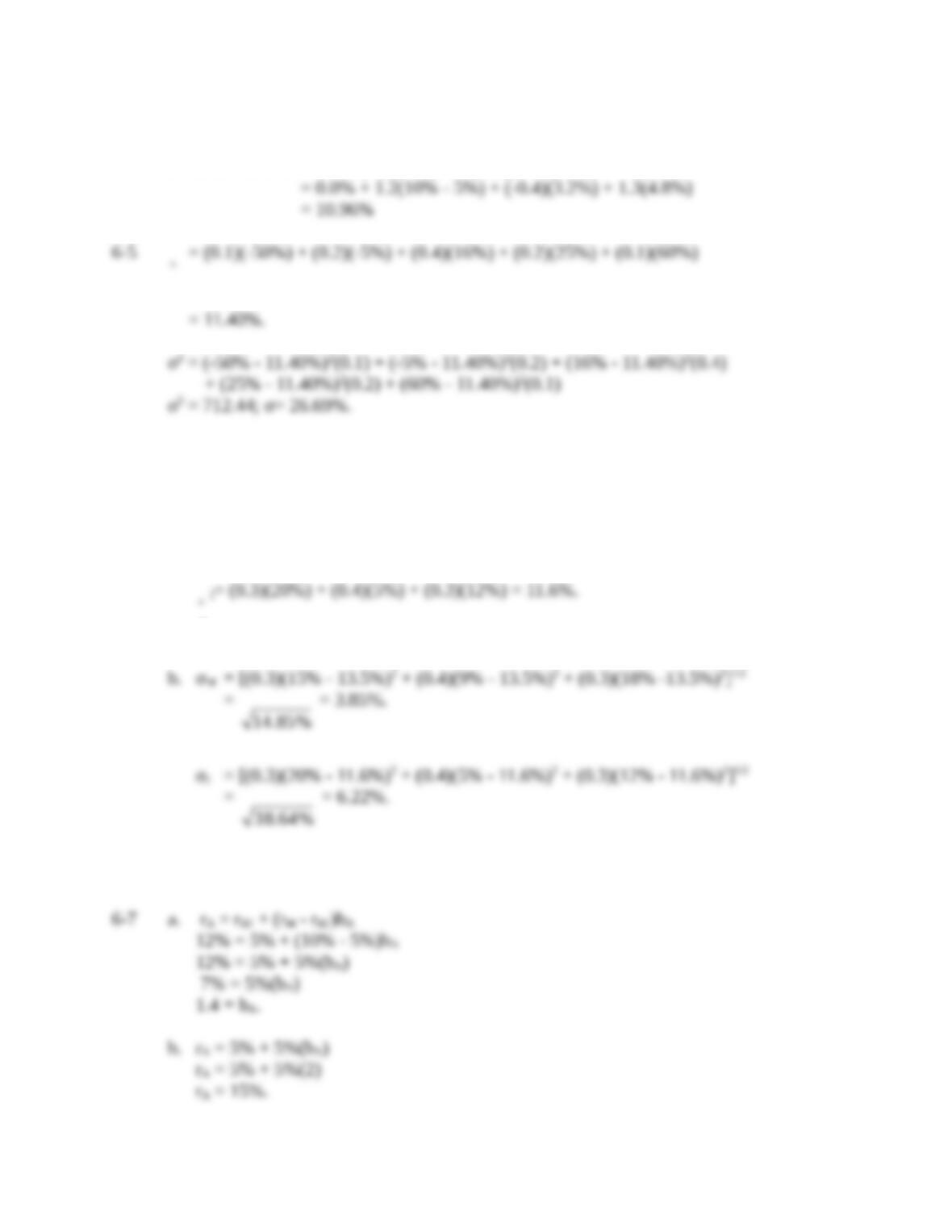

6-6 a.

r

m= (0.3)(15%) + (0.4)(9%) + (0.3)(18%) = 13.5%.

r

b. 1. rRF increases to 6%:

2. rRF decreases to 4%:

c. 1. rM increases to 14%:

2. rM decreases to 11%:

6-9 Old portfolio beta =

5,0007$

000,70$

(b) +

5,0007$

000,5$

(0.8)

Alternative Solutions:

2. bi excluding the stock with the beta equal to 0.8 is 18.0 – 0.8 = 17.2, so the beta of