j. Define the real risk-free rate (r*). What security can be used as an estimate of

r*? What is the nominal risk-free rate (rRF)? What securities can be used as

estimates of rRF?

Answer: The real risk-free rate, r*, is the rate that a hypothetical riskless security pays each

moment if zero inflation were expected. The real risk-free rate is not constant—r*

The nominal risk-free rate, rRF, can be approximate by the yield on a Treasury

There is no truly riskless security, but the closest thing is a short-term U. S.

k. Describe a way to estimate the inflation premium (IP) for a T-Year bond.

Answer: Treasury Inflation-Protected Securities (TIPS) are indexed to inflation. The IP for a

.

l. What is a bond spread and how is it related to the default risk premium? How

are bond ratings related to default risk? What factors affect a company’s bond

rating?

Answer: A “bond spread” is often calculated as the difference between a corporate bond’s yield

and a Treasury security’s yield of the same maturity. Therefore:

Mini Case: 5 – 1

© 2017 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible

website, in whole or in part.

1. Financial performance–determined by ratios such as the debt, TIE, FCC, and

current ratios.

2. Provisions in the bond contract:

A. Secured vs. Unsecured debt

3. Other factors:

A. Earnings stability

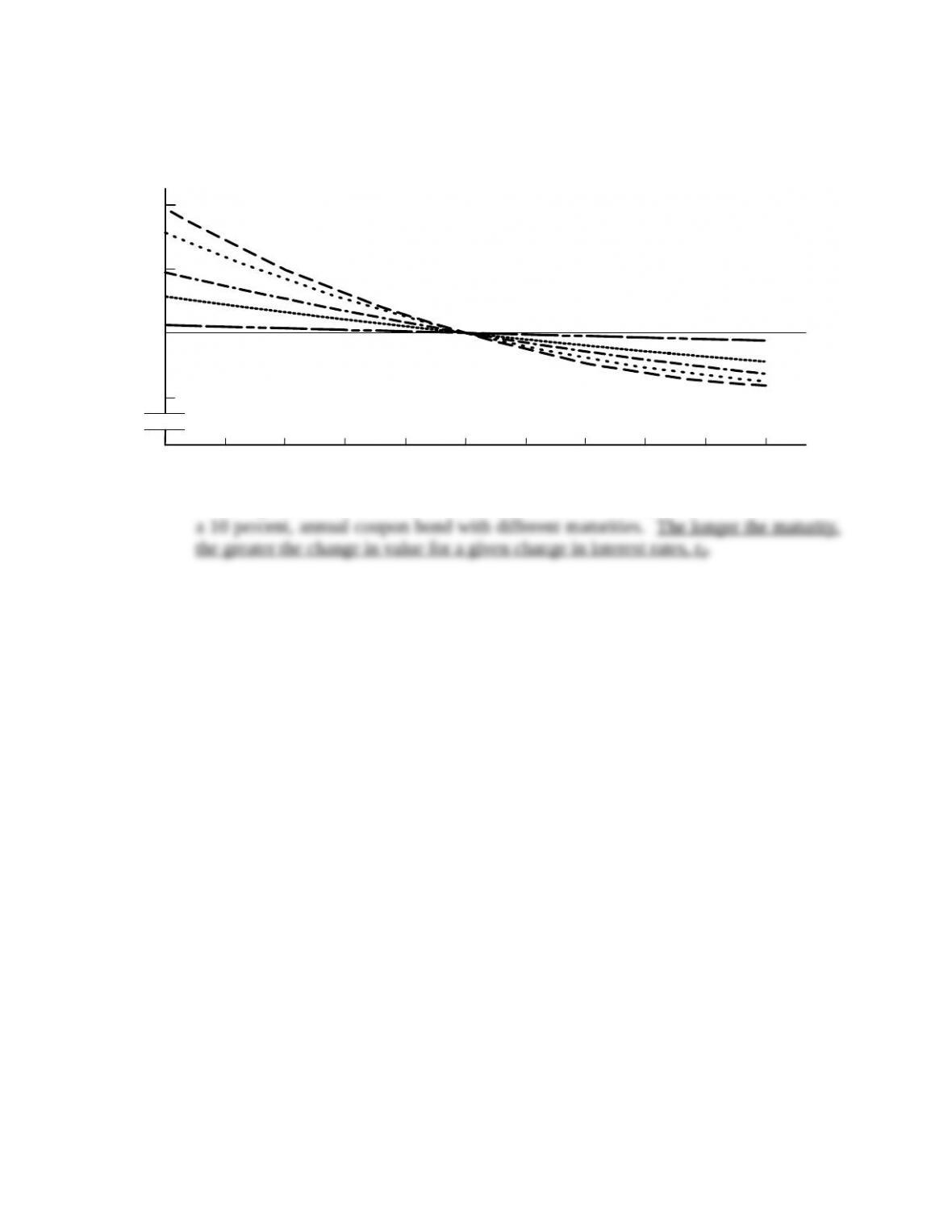

m. What is interest rate (or price) risk? Which bond has more interest rate risk, an

annual payment 1-year bond or a 10-year bond? Why?

Answer: Interest rate risk, which is often just called price risk, is the risk that a bond will lose

value as the result of an increase in interest rates. Earlier, we developed the following

values for a 10 percent, annual coupon bond:

Maturity

rd 1-Year Change 10-Year Change

A 5 percentage point increase in r causes the value of the 1-year bond to decline by

Mini Case: 5 – 2

© 2017 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible

website, in whole or in part.

The graph above shows the relationship between bond values and interest rates for

Mini Case: 5 – 3

© 2017 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible

website, in whole or in part.

I n t e r e s t R a t e P r i c e R i s k f o r 1 0 P e r c e n t C o u p o n

B o n d s w i t h D i f f e r e n t M a t u r i t i e s

B o n d V a l u e

( $ )

Interest Rate (%)

1 – Y e a r

5 – Y e a r

1 0 – Y e a r

2 0 – Y e a r

3 0 – Y e a r

1 , 8 0 0

1 , 4 0 0

1 , 0 0 0

6 0 0

5

9

6

7

8

1 0

1 1

1 2

1 3

1 4

1 5

n. What is reinvestment rate risk? Which has more reinvestment rate risk, a

1-year bond or a 10-year bond?

Answer: Investment rate risk is defined as the risk that cash flows (interest plus principal

repayments) will have to be reinvested in the future at rates lower than today’s rate.

To illustrate, suppose you just won the lottery and now have $500,000. You plan to

invest the money and then live on the income from your investments. Suppose you

o. How are interest rate risk and reinvestment rate risk related to the maturity risk

premium?

Answer: Long-term bonds have high interest rate risk but low reinvestment rate risk.

Mini Case: 5 – 4

© 2017 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible

website, in whole or in part.

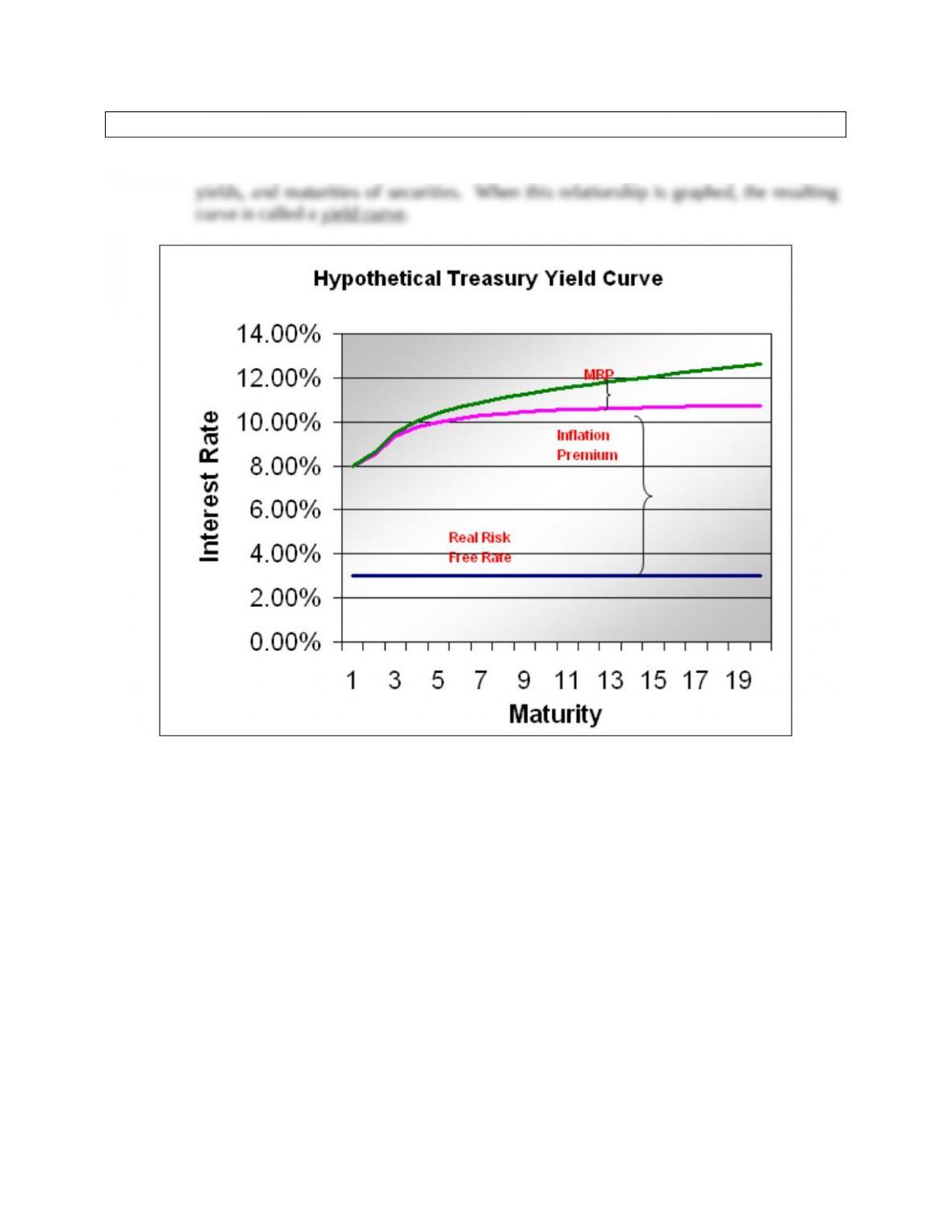

p. What is the term structure of interest rates? What is a yield curve?

Answer: The term structure of interest rates is the relationship between interest rates, or

Mini Case: 5 – 5

© 2017 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible

website, in whole or in part.

q. Briefly describe bankruptcy law. If this firm were to default on the bonds,

would the company be immediately liquidated? Would the bondholders be

assured of receiving all of their promised payments?

Answer: When a business becomes insolvent, it does not have enough cash to meet scheduled

The decision to force a firm to liquidate or to permit it to reorganize depends on

whether the value of the reorganized firm is likely to be greater than the value of the

firm’s assets if they were sold off piecemeal. In a reorganization, a committee of

If the firm is deemed to be too far gone to be saved, it will be liquidated and the

priority of claims would be as follows:

1. Secured creditors.

2. Trustee’s costs.

If the firm’s assets are worth more “alive” than “dead,” the company would be

Mini Case: 5 – 6

© 2017 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible

website, in whole or in part.

Web Appendix 5A

A Closer Look at Zero Coupon Bonds

Answers to Questions

5A-1 No, not all original issue discount bonds have zero coupons. Zero coupon bonds are just

5A-2 Shortly after corporations began to issue zeros, investment bankers figured out a way to

create zeros from U.S. Treasury bonds, which at the time were issued only in coupon

form. In 1983, Salomon Brothers bought $1 billion of 12%, 30-year Treasuries. Each

Stripped U.S. Treasury bonds (Treasury zeros) generally are not callable because

the Treasury normally sells noncallable bonds.

5A-3 Treasury zeros are not protected from interest rate (price) risk, because the principal is

totally susceptible to interest rate movements. You can see this by changing interest rates

Mini Case: 5 – 7

© 2017 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible

website, in whole or in part.

Solutions to Problems

5A-1

Year 0 1 2 3 4

Enter the following data into your calculator to determine the price of each bond:

Accrued valuet = Accrued valuet – 1(1.09).

Interest = Accrued valuet – Accrued valuet – 1.

Tax savings = Interest(T).

Note that in Year 4, the company must pay the maturity value of the bond; therefore, the

cash flow in Year 4 is equal to -$1,000 + Tax savings.

Mini Case: 5 – 8

© 2017 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible

website, in whole or in part.

5A-2 0 1 2 3 4

Accrued value 708.43 772.19 841.69 917.44 1,000.00

Enter the following data into your calculator to determine the price of each bond:

Accrued valuet = Accrued valuet – 1(1.09).

Interest = Accrued valuet – Accrued valuet – 1.

Tax savings = Interest(T).

Note that in Year 4, the investor receives the maturity value of the bond; however, he

must pay taxes on the interest income in Year 4. Thus, cash flow in Year 4 equals $1,000

– Taxes.

To solve for the IRR of this cash flow stream, using a financial calculator, enter the

5A-3

5A-4 Step 1: Find out what was paid for the bond:

Step 2: Determine the Year 1 accrued interest:

Step 3: Calculate the tax on the accrued interest:

Mini Case: 5 – 9

© 2017 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible

website, in whole or in part.

5A-5 First find the yields on one-year and two-year zero coupon bonds, so you can find the

implied rate on a one-year bond, one year from now. Then use this implied rate to find its

price.

1-Year:

2-Year:

Therefore, if the implied rate = X, then:

Now find the price of a 1-year zero, 1 year from now:

5A-6 0 10 50

-87.2037 1,000

1.10

Step 1: Using a financial calculator, we find the PV of the zeros at Time 0 by entering the

following data:

Step 2: Using a financial calculator, we can find the investor’s effective annual rate of

return by entering the following data:

(Remember, this is a periodic semiannual rate.)

Mini Case: 5 – 10

© 2017 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible

website, in whole or in part.

Web Appendix 5D

The Pure Expectations Theory and Estimation of Forward

Rates

Solutions to Problems

5D-1 rT1 = 5%; 1rT1 = 6%; rT2 = ?

5D-2 Let X equal the yield on 2-year securities 4 years from now:

5D-3 a. (1.045)2= (1.03)(1 + X)

b. For riskless bonds under the expectations theory, the interest rate for a bond of any

maturity is

rN = r* + average inflation over N years. If r* = 1%, we can solve for IPN:

Note also that the average inflation rate is (2% + 5%)/2 = 3.5%, which, when added

Mini Case: 5 – 11

© 2017 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible

website, in whole or in part.

X represents the one-year rate on a bond one year from now (Year 2).

The average interest rate during the 2-year period differs from the 1-year interest rate

expected for Year 2 because of the inflation rate reflected in the two interest rates. The

inflation rate reflected in the interest rate on any security is the average rate of inflation

expected over the security’s life.

Mini Case: 5 – 12

© 2017 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible

website, in whole or in part.