e. 1. What would be the value of the bond described in part d if, just after it had been

issued, the expected inflation rate rose by 3 percentage points, causing investors

to require a 13 percent return? Would we now have a discount or a premium

bond?

Answer: With a financial calculator, just change the value of rd = I/YR from 10% to 13%, and

press the PV button to determine the value of the bond:

Using the formulas, we would have, at r = 13 percent,

In a situation like this, where the required rate of return, r, rises above the coupon

rate, the bonds’ values fall below par, so they sell at a discount.

e. 2. What would happen to the bonds’ value if inflation fell, and rd declined to 7

percent? Would we now have a premium or a discount bond?

Answer: In the second situation, where rd falls to 7 percent, the price of the bond rises above

Thus, when the required rate of return falls below the coupon rate, the bonds’ value

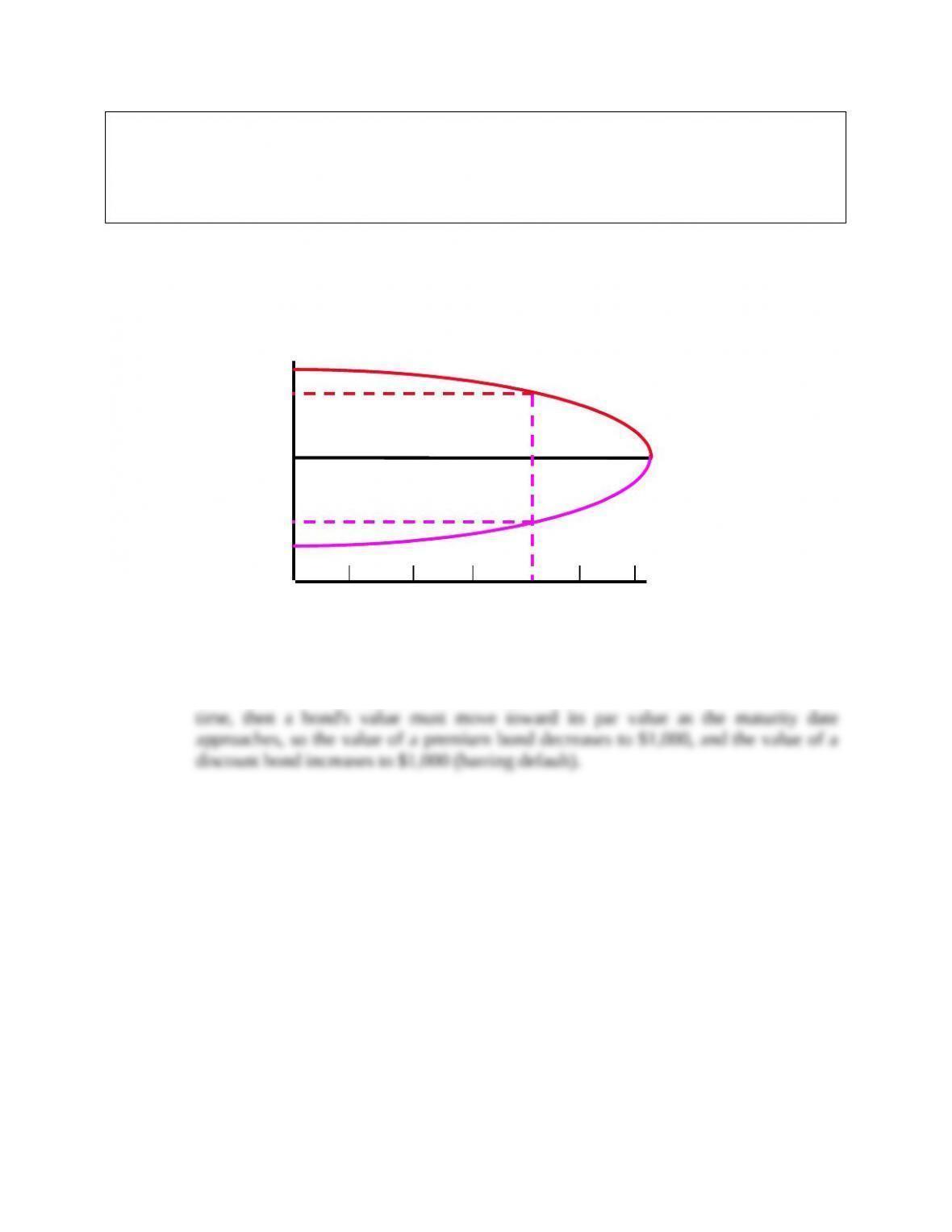

e. 3. What would happen to the value of the 10-year bond over time if the required

rate of return remained at 13 percent, or if it remained at

7 percent? (Hint: with a financial calculator, enter PMT, I/YR, FV, and N, and

then change (override) n to see what happens to the PV as the bond approaches

maturity.)

Answer: Assuming that interest rates remain at the new levels (either 7% or 13%), we could

find the bond’s value as time passes, and as the maturity date approaches. If we then

plotted the data, we would find the situation shown below:

M

Bond Value ($)

Years remaining to Maturity

837

775

30 25 20 15 10 5 0

rd= 7%.

rd= 13%.

rd = 10%. M

Bond Value ($)

Years remaining to Maturity

837

775

30 25 20 15 10 5 0

rd= 7%.

rd= 13%.

rd = 10%.

At maturity, the value of any bond must equal its par value (plus accrued interest).

Therefore, if interest rates, hence the required rate of return, remain constant over

f. 1. What is the yield to maturity on a 10-year, 9 percent annual coupon, $1,000 par

value bond that sells for $887.00? That sells for $1,134.20? What does the fact

that a bond sells at a discount or at a premium tell you about the relationship

between rd and the bond’s coupon rate?

Answer: The yield to maturity (YTM) is that discount rate which equates the present value of a

bond’s cash flows to its price. In other words, it is the promised rate of return on the

We want to find r in this equation:

.

)r + (1

M

+

)r + (1

INT

+ … +

)r + (1

INT

= PV =

V

NN1

B

We know n = 10, PV = -887, PMT = 90, and FV = 1000, so we have an equation with

Alternatively, we could use present value interest factors:

We can tell from the bond’s price, even before we begin the calculations, that the

If the bond were priced at $1,134.20, then it would be selling at a premium. In

f. 2. What are the total return, the current yield, and the capital gains yield for the

discount bond? (Assume the bond is held to maturity and the company does not

default on the bond.)

Answer: The current yield is defined as follows:

.

bond theof priceCurrent

paymentinterest coupon Annual

= YieldCurrent

The capital gains yield is defined as follows:

.

priceyear -of-Beginning

price sbond’in Change Expected

= yield gains Capital

The total expected return is the sum of the current yield and the expected capital gains

yield:

.

yield gains

capital Expected

+

yieldcurrent

Expected

=

Return Total

Expected

For our 9% coupon, 10-year bond selling at a price of $887 with a YTM of 10.91%,

the current yield is:

.%15.10 = 1015.0 =

887$

90$

= yieldCurrent

Knowing the current yield and the total return, we can find the capital gains yield:

And

The capital gains yield calculation can be checked by asking this question: “What is

the expected value of the bond 1 year from now, assuming that interest rates remain at

Capital Gains Yield =

V

)/

V

–

V

(

BBB

001

This agrees with our earlier calculation (except for rounding). When the bond is

and

The bond provides a current yield that exceeds the total return, but a purchaser would

incur a small capital loss each year, and this loss would exactly offset the excess

current yield and force the total return to equal the required rate.

g. How does the equation for valuing a bond change if semiannual payments are

made? Find the value of a 10-year, semiannual payment, 10 percent coupon

bond if nominal rd = 13%.

Answer: In reality, virtually all bonds issued in the U.S. have semiannual coupons and are

valued using the setup shown below:

M

PV1

.

.

.

We would use this equation to find the bond’s value:

.

)

2/

r

+ (1

M

+

)

2/

r

+ (1

2INT/

=

VN2

d

t

d

N2

1 =t

B

The payment stream consists of an annuity of 2N payments plus a lump sum equal to

the maturity value.

To find the value of the 10-year, semiannual payment bond, semiannual interest =

For example, if rd rose to 13%, we would input I/YR= 6.5 rather than 5%, and

At a 13 percent required return:

At a 7 percent required return:

h. Suppose a 10-year, 10 percent, semiannual coupon bond with a par value of

$1,000 is currently selling for $1,135.90, producing a nominal yield to maturity of

8 percent. However, the bond can be called after 5 years for a price of $1,050.

h. 1. What is the bond’s nominal yield to call (YTC)?

Answer: If the bond were called, bondholders would receive $1,050 at the end of year 5. Thus,

the time line would look like this:

The easiest way to find the YTC on this bond is to input values into your calculator:

This 7.5% is the rate brokers would quote if you asked about buying the bond.

You could also calculate the EAR on the bond:

Usually, people in the bond business just talk about nominal rates, which is OK so

h. 2. If you bought this bond, do you think you would be more likely to earn the YTM

or the YTC? Why?

Answer: Since the coupon rate is 10% versus YTC = rd = 7.53%, it would pay the company to

call the bond, get rid of the obligation to pay $100 per year in interest, and sell

i. Write a general expression for the yield on any debt security (rd) and define these

terms: real risk-free rate of interest (r*), inflation premium (IP), default risk

premium (DRP), liquidity premium (LP), and maturity risk premium (MRP).

Answer: rd = r* + IP + DRP + LP + MRP.

The inflation premium (IP) is a premium added to the real risk-free rate of interest

to compensate for expected inflation.

The default risk premium (DRP) is a premium based on the probability that the

A liquid asset is one that can be sold at a predictable price on short notice; a

liquidity premium is added to the rate of interest on securities that are not liquid.

The maturity risk premium (MRP) is a premium which reflects interest rate risk;