h. 1. Define (a) the stated, or quoted, or nominal rate, (iNom), and (b) the periodic rate

(iPer).

ANSWER: The quoted, or nominal, rate is merely the quoted percentage rate of return. The

h. 2. Will the future value be larger or smaller if we compound an initial amount

more often than annually, for example, every 6 months, or semiannually, holding

the stated interest rate constant? Why?

Answer: Accounts that pay interest more frequently than once a year, for example,

h. 3. What is the future value of $100 after 5 years under 12% annual compounding?

Semiannual compounding? Quarterly compounding? Monthly compounding?

Daily compounding

Answer: Under annual compounding, the $100 is compounded over 5 annual periods at a 12.0

percent periodic rate:

MN

NOM

M

I

1PV

5*1

1

12.0

1

Under semiannual compounding, the $100 is compounded over 10 semiannual

periods at a 6.0 percent periodic rate:

Mini Case: 4 -1

© 2017 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or

in part.

h. 4. What is the effective annual rate (EAR or EFF%)? What is the EFF% for a

nominal rate of 12%, compounded semiannually? Compounded quarterly?

Compounded monthly? Compounded daily?

Answer: The effective annual rate is the annual rate that causes the PV to grow to the same FV

EAR = Effective Annual Rate =

.0.1

M

I1

M

NOM

IF iNom = 12% and interest is compounded semiannually, then:

0.1

2

12.0

1

2

For quarterly compounding, the effective annual rate is:

For monthly compounding, the effective annual rate is:

For daily compounding, the effective annual rate is:

i. Will the effective annual rate ever be equal to the nominal (quoted) rate?

Answer: If annual compounding is used, then the nominal rate will be equal to the effective

Mini Case: 4 -2

© 2017 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or

in part.

j. 1. Construct an amortization schedule for a $1,000, 10% annual rate loan with 3

equal installments.

2. What is the annual interest expense for the borrower, and the annual interest

income for the lender, during Year 2?

Answer: To begin, note that the face amount of the loan, $1,000, is the present value of a

3-year annuity at a 10 percent rate:

We have an equation with only one unknown, so we can solve it to find PMT. The

easy way is with a financial calculator. Input N = 3, I/YR = 10, PV = -1,000, FV = 0,

and then press the PMT button to get PMT = 402.1148036, rounded to $402.11.

Now make the following points regarding the amortization schedule:

The $402.11 annual payment includes both interest and principal. Interest in the

first year is calculated as follows:

The repayment of principal is the difference between the $402.11 annual payment

and the interest payment:

The loan balance at the end of the first year is:

We would continue these steps in the following years.

Mini Case: 4 -3

© 2017 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or

in part.

Notice that the interest each year declines because the beginning loan balance is

The interest component is an expense which is deductible to a business or a

The payment may have to be increased by a few cents in the final year to take

The lender received a 10% rate of interest on the average amount of money that

k. Suppose on January 1 you deposit $100 in an account that pays a nominal, or

quoted, interest rate of 11.33463%, with interest added (compounded) daily.

How much will you have in your account on October 1, or 9 months later?

days between January 1 and October 1. Calculate FV as follows:

An alternative approach would be to first determine the effective annual rate of

interest, with daily compounding, using the formula:

365

365

1133463.0

1

(Some calculators, e.g., the hp 10b and 17b, have this equation built in under the

ICNV [interest conversion] function.)

Mini Case: 4 -4

© 2017 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or

in part.

Thus, if you left your money on deposit for an entire year, you would earn $12 of

interest, and you would end up with $112. The question, though, is this: how much

will be in your account on October 1?

Here you will be leaving the money on deposit for 9/12 = 3/4 = 0.75 of a year.

You would use the regular set-up, but with a fractional exponent:

Fractional time periods

Thus far all of our examples have dealt with full years. Now we are going to look at

the situation when we are dealing with fractional years, such as 9 months, or 10 years.

In these situations, proceed as follows:

As always, start by drawing a time line so you can visualize the situation.

Then think about the interest rate–the nominal rate, the compounding periods per

Here t can be a fraction of a year, such as 0.75, if you need to find the PV of

If you have an annuity with payments different from once a year, say every

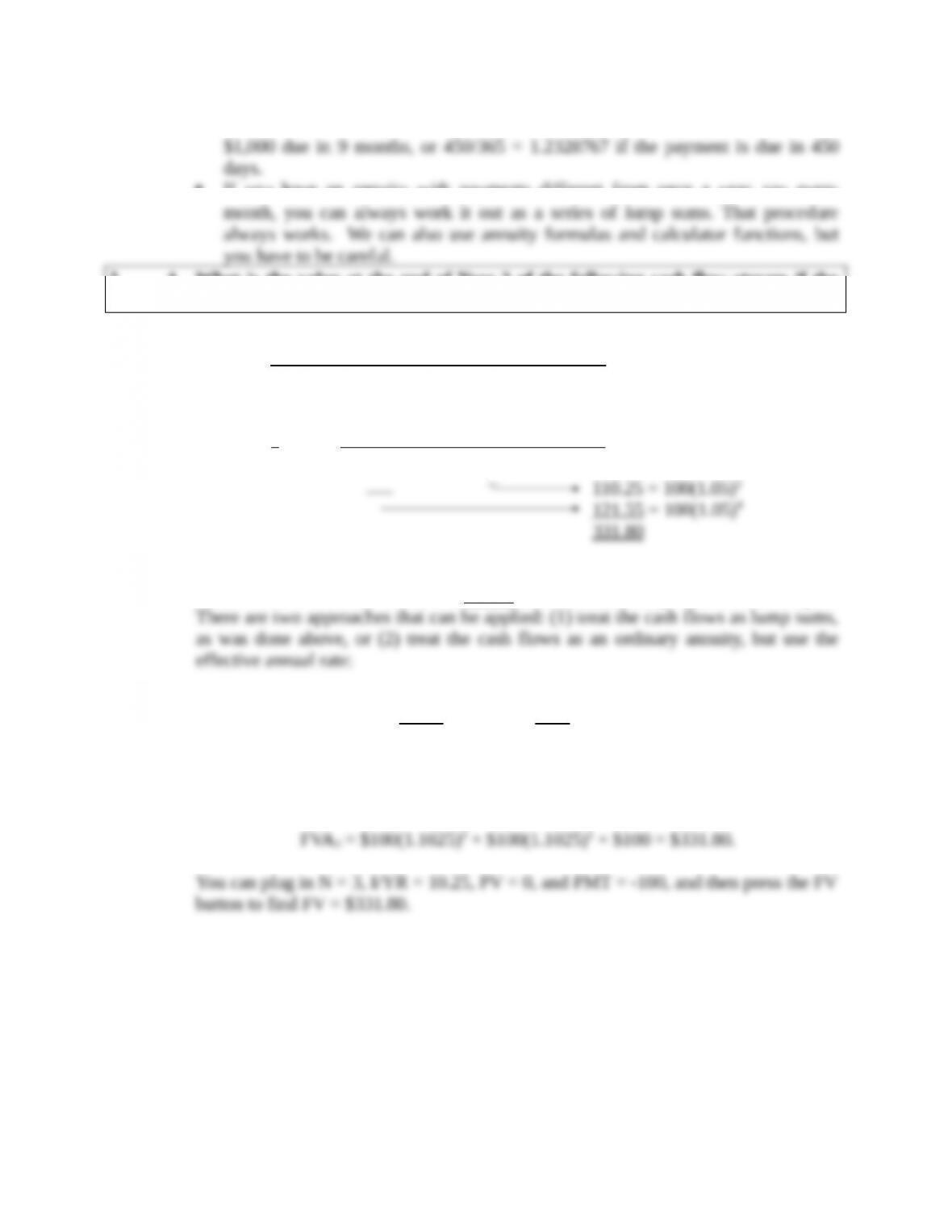

l. 1. What is the value at the end of Year 3 of the following cash flow stream if the

quoted interest rate is 10%, compounded semiannually?

0 1 2 3 Years

| | | | | | |

100 100 100

Answer: 0 1 2 3

| | | | | | |

100 100 100

Here we have a different situation. The payments occur annually, but compounding

occurs each 6 months. Thus, we cannot use normal annuity valuation techniques.

5%

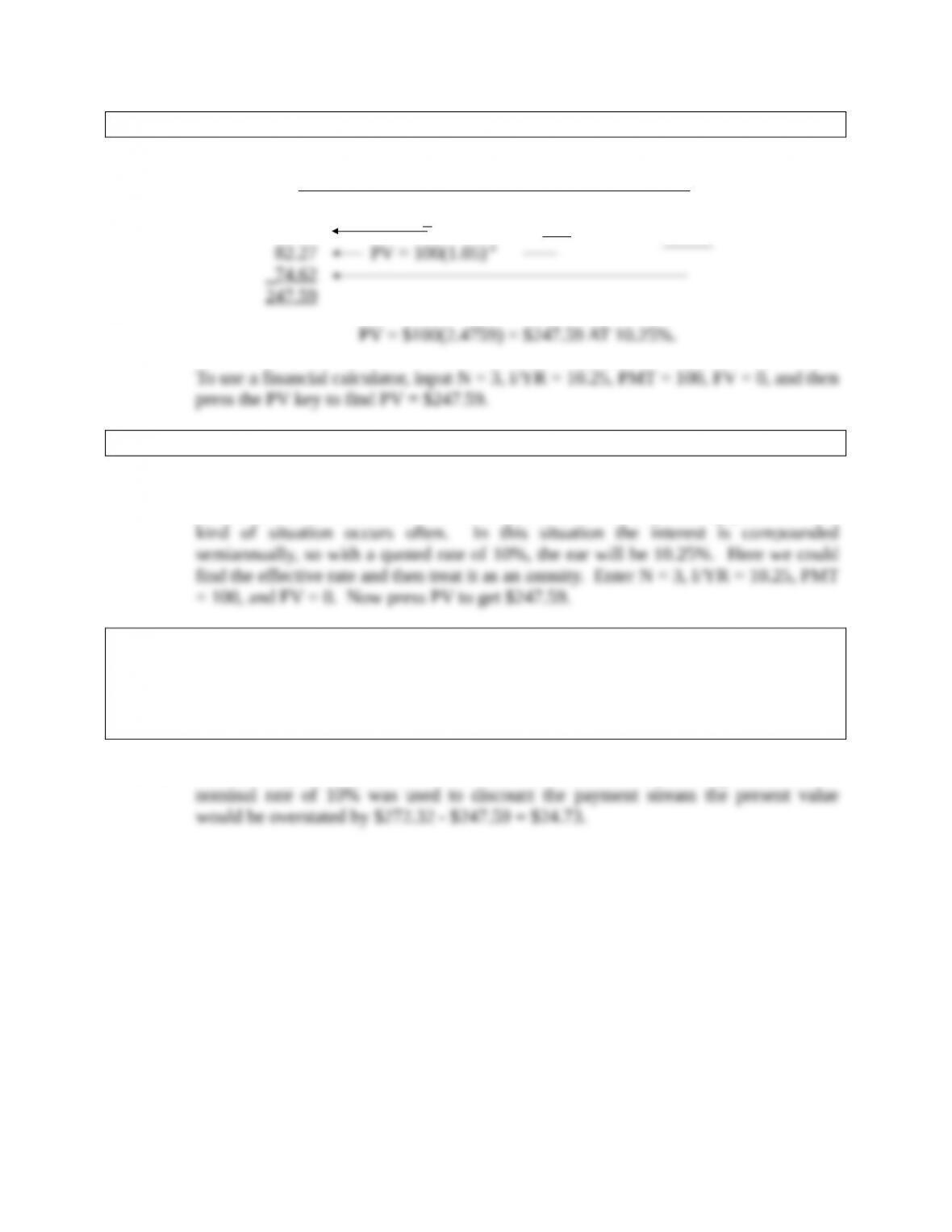

l. 2. What is the PV of the same stream?

Answer: 0 1 2 3

| | | | | | |

100 100 100

90.70

l. 3. Is the stream an annuity?

Answer: The payment stream is an annuity in the sense of constant amounts at regular

intervals, but the intervals do not correspond with the compounding periods. This

l. 4. An important rule is that you should never show a nominal rate on a time line or

use it in calculations unless what condition holds? (Hint: Think of annual

compounding, when INOM = EFF% = IPER.) What would be wrong with your

answer to questions l(1) and l(2) if you used the nominal rate (10%) rather than

the periodic rate (INOM /2 = 10%/2 = 5%)?

Answer: iNom can only be used in the calculations when annual compounding occurs. If the

Mini Case: 4 -7

© 2017 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or

in part.

5%

m. Suppose someone offered to sell you a note calling for the payment of $1,000 15

months from today. They offer to sell it to you for $850. You have $850 in a

bank time deposit which pays a 6.76649% nominal rate with daily compounding,

which is a 7% effective annual interest rate, and you plan to leave the money in

the bank unless you buy the note. The note is not risky–you are sure it will be

paid on schedule. Should you buy the note? Check the decision in three ways:

(1) by comparing your future value if you buy the note versus leaving your

money in the bank, (2) by comparing the PV of the note with your current bank

account, and (3) by comparing the EFF% on the note versus that of the bank

account.

Answer: You can solve this problem in three ways–(1) by compounding the $850 now in the

bank for 15 months and comparing that FV with the $1,000 the note will pay, (2) by

0 1 1.25

| | |

-850 1,000

Alternatively, 15 months = (1.25 years)(365 days per year) = 456.25 456

days.

The slight difference is due to using n = 456 rather than n = 456.25.

(2) PV = $1,000/(1.07)-1.25 = $918.90. Since the present value of the note is greater

Mini Case: 4 -8

© 2017 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or

in part.

7%

equation with one unknown, we can solve it for i. You will get a value of i =

13.88%. The easy way is to plug values into your calculator. Since this return

Alternatively, we could solve the following equation:

Mini Case: 4 -9

© 2017 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or

in part.

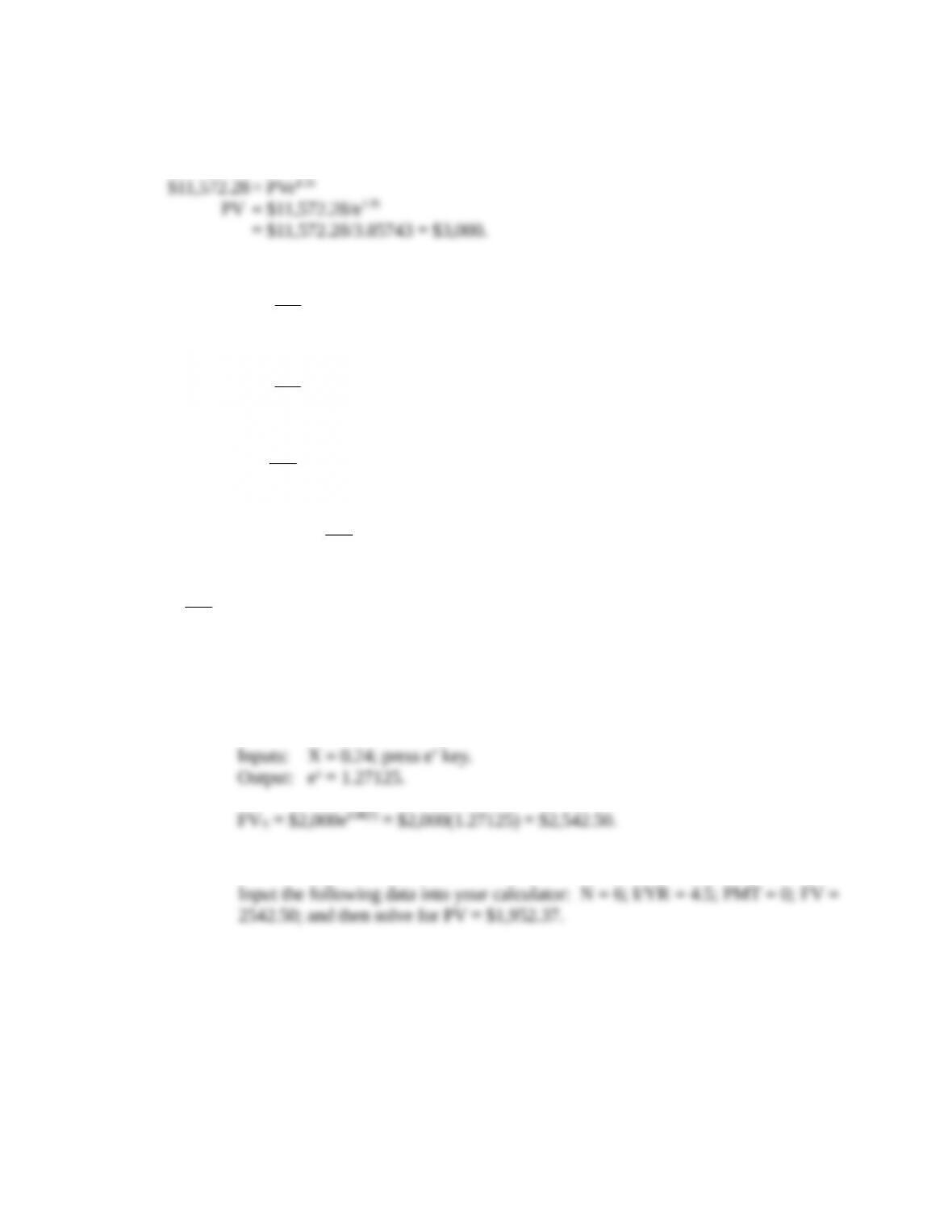

Web Extension 4C Continuous Compounding and Discounting

Solutions to Problems

4C-1 FV15 = $15,000e0.06(15) = $36,894.05.

4C-3 Daily compounding:

Continuous compounding:

4C-4 Calculate the growth factor using PV and FV which are given:

Take the natural logarithm of both sides:

I(6)ln e= ln 2.0

4C-5 Determine the effective annual rates.

a. 10.25% annually = 10.25%.

Web Extension 4C: 4 -10

© 2017 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or

in part.

4C-6 (Constant e = 2.7183 rounded.)

$11,572.28= PVe0.09(15)

4C-7 e(0.03)(10) =

20

N OM

2

I

1

e0.3 =

20

N OM

2

I

1

e0.3/20 = 1 +

2

I

N OM

1.01511 = 1 +

2

I

N OM

2

I

N OM

= 0.01511

INOM = 0.0302 = 3.02%.

4C-8 Step 1: Calculate the FV of the $2,000 deposit at 8% with continuous compounding:

Using ex key:

Step 2: Calculate the PV or initial deposit:

Web Extension 4C: 4 -11

© 2017 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or

in part.