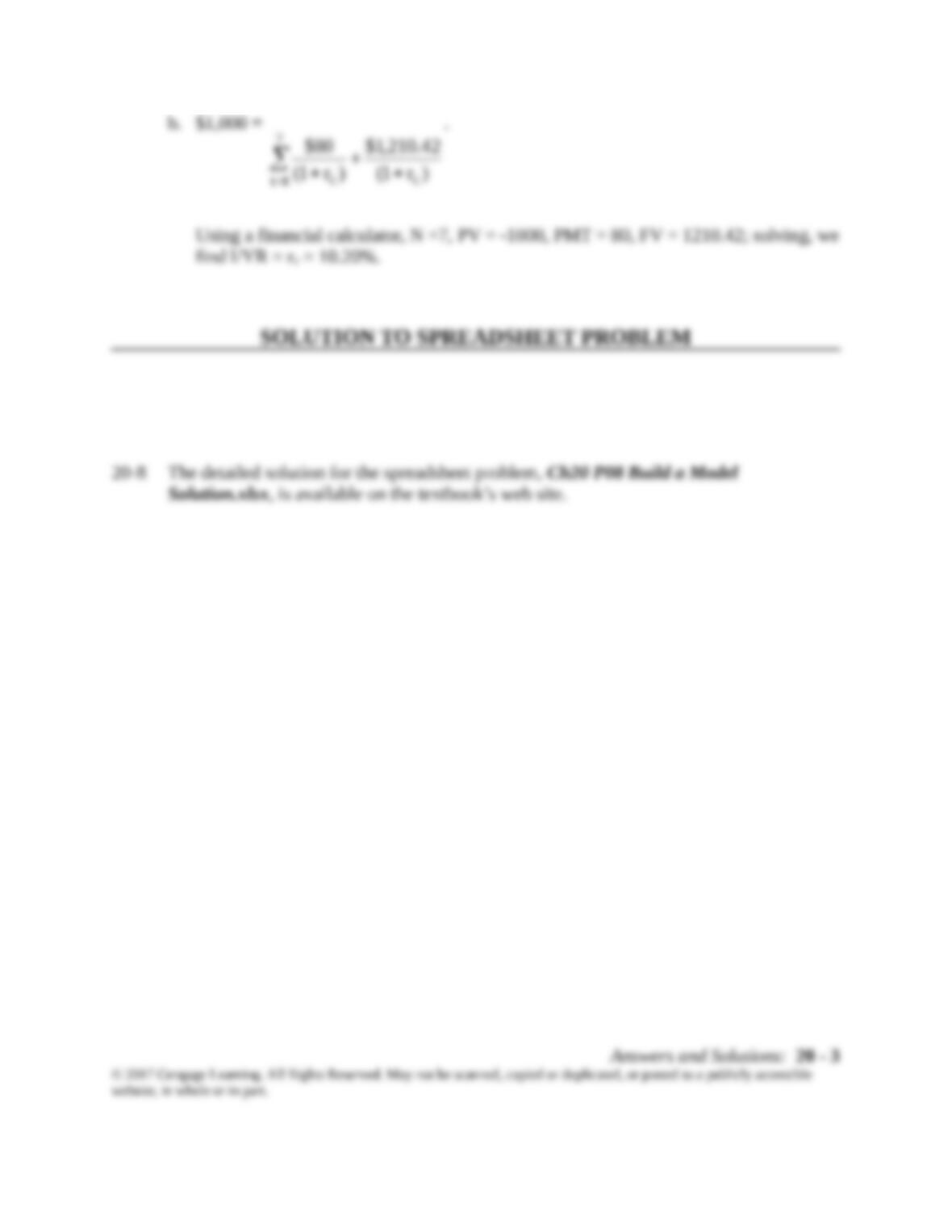

20-7 a.

Stock data and stock required return:

rd = 9%.

Convertible bond data:

Par = $1,000, 20-year.

Coupon = 8%.

Find N (number of years) to anticipated call/conversion:

We need to find the number of years that it takes $805 to grow to $1,200 at a 6% interest

We could also calculate this as:

(CR)(P0)(1 + g)N= $1,200

($23)(35)(1 + 0.06)N= $1,200

Straight-debt value of the convertible at t = 0:

(Assumes annual payment of coupon)

Answers and Solutions: 20 – 1

© 2017 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible

website, in whole or in part.

At t = 0 (N = 20): N = 20, I/YR = 9, PMT = 80, FV = 1,000; solving, PV = -908.715.

Alternatively,

V =

20

1t

20t

)09.01(

000,1$

)09.01(

80$

= $908.715.

Repeating, we can find the straight bond value for different values of N:

V at t = 5 (N = 15): $919.39.

Conversion value:

The stock price should grow at the 6%. The conversion value at Year t is equal to the

expected stock price multiplied by the conversion ratio:

Repeating for different values of N:

CV0 = $23(35) = $805.

For the expected time of conversion (N = 7), the conversion value is:

The cash flow at the time of conversion (N = 7), is equal to the conversion value plus the

coupon payment:

Answers and Solutions: 20 – 2

© 2017 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible

website, in whole or in part.

MINI CASE

Paul Duncan, financial manager of Edusoft Inc., is facing a dilemma. The firm was

founded five years ago to provide educational software for the rapidly expanding primary

and secondary school markets. Although Edusoft has done well, the firm’s founder believes

that an industry shakeout is imminent. To survive, Edusoft must grab market share now,

and this will require a large infusion of new capital.

Because he expects earnings to continue rising sharply and looks for the stock price to

follow suit, Mr. Duncan does not think it would be wise to issue new common stock at this

time. On the other hand, interest rates are currently high by historical standards, and with

the firm’s B rating, the interest payments on a new debt issue would be prohibitive. Thus,

he has narrowed his choice of financing alternatives to: (1) preferred stock; (2) bonds with

warrants; or (3) convertible bonds.

As Duncan’s assistant, you have been asked to help in the decision process by answering

the following questions:

a. How does preferred stock differ from both common equity and debt? Is

preferred stock more risky than common stock? What is floating rate preferred

stock?

Answer: Preferred stock is a hybrid–it contains some features that are similar to debt and some

features that are similar to common equity. Like debt, preferred payments to

investors are contractually fixed, but like common equity, preferred dividends can be

omitted without putting the company into default and thus into bankruptcy. Note,

Answers and Solutions: 20 – 4

© 2017 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible

website, in whole or in part.

b. What is a call option? How can knowledge of call options help a financial

manager to better understand warrants and convertibles?

Answer: A call option is a contract which gives the holder the right, but not the obligation, to

Answers and Solutions: 20 – 5

© 2017 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible

website, in whole or in part.