Chapter 19

Lease Financing

ANSWERS TO END-OF-CHAPTER QUESTIONS

19-1 a. The lessee is the party leasing the property. The party receiving the payments from

the lease (that is, the owner of the property) is the lessor.

b. An operating lease, sometimes called a service lease, provides for both financing and

maintenance. Generally, the operating lease contract is written for a period

considerably shorter than the expected life of the leased equipment, and contains a

cancellation clause. A financial lease does not provide for maintenance service, is not

cancelable, and is fully amortized; that is, the lease covers the entire expected life of

c. Off-balance sheet financing refers to the fact that for many years neither leased assets

nor the liabilities under lease contracts appeared on the lessees’ balance sheets. To

d. FASB Statement 13 is the Financial Accounting Standards Board statement

e. A guideline lease is a lease that meets all of the IRS requirements for a genuine lease.

g. The lessee’s analysis involves determining whether leasing an asset is less costly than

buying the asset. The lessee will compare the present value cost of leasing the asset

with the present value cost of purchasing the asset (assuming the funds to purchase

The lessor’s analysis involves determining the rate of return on the proposed

i. The alternative minimum tax (AMT), which is figured at about 20 percent of the

19-2 An operating lease is usually cancelable and includes maintenance. Operating leases are,

frequently, for a period significantly shorter than the economic life of the asset, so the

19-3 You would expect to find that lessees, in general, are in relatively low income-tax

brackets, while lessors tend to be in high tax brackets. The reason for this is that owning

19-4 The banks, when they initially went into leasing, were paying relatively high tax rates.

However, since municipal bonds are tax-exempt, their heavy investments in municipals

19-5 a. Pros:

The use of the leased premises or equipment is actually an exclusive right, and the

A fixed policy of capitalizing leases among all companies would add to the

b. Cons:

Because the firm does not actually own the leased property, the legal aspect can

be cited as an argument against capitalization.

Some argue that other items should be listed on the balance sheet before leases;

19-6 Lease payments, like depreciation, are deductible for tax purposes. If a 20-year asset

were depreciated over a 20-year life, depreciation charges would be 1/20 per year (more

19-7 In fact, Congress did this in 1981. Depreciable lives were shorter than before; corporate

tax rates were essentially unchanged (they were lowered very slightly on income below

19-8 A cancellation clause would reduce the risk to the lessee since the firm would be allowed

to terminate the lease at any point. Since the lease is less risky than a standard financial

SOLUTIONS TO END-OF-CHAPTER PROBLEMS

19-1 a. (1) Reynolds’ current debt ratio is $400/$800 = 50%.

(2) If the company purchased the equipment its balance sheet would look like:

Current assets $300 Debt (including lease) $600

b. The company’s financial risk (assuming the implied interest rate on the lease is

equivalent to the loan) is no different whether the equipment is leased or purchased.

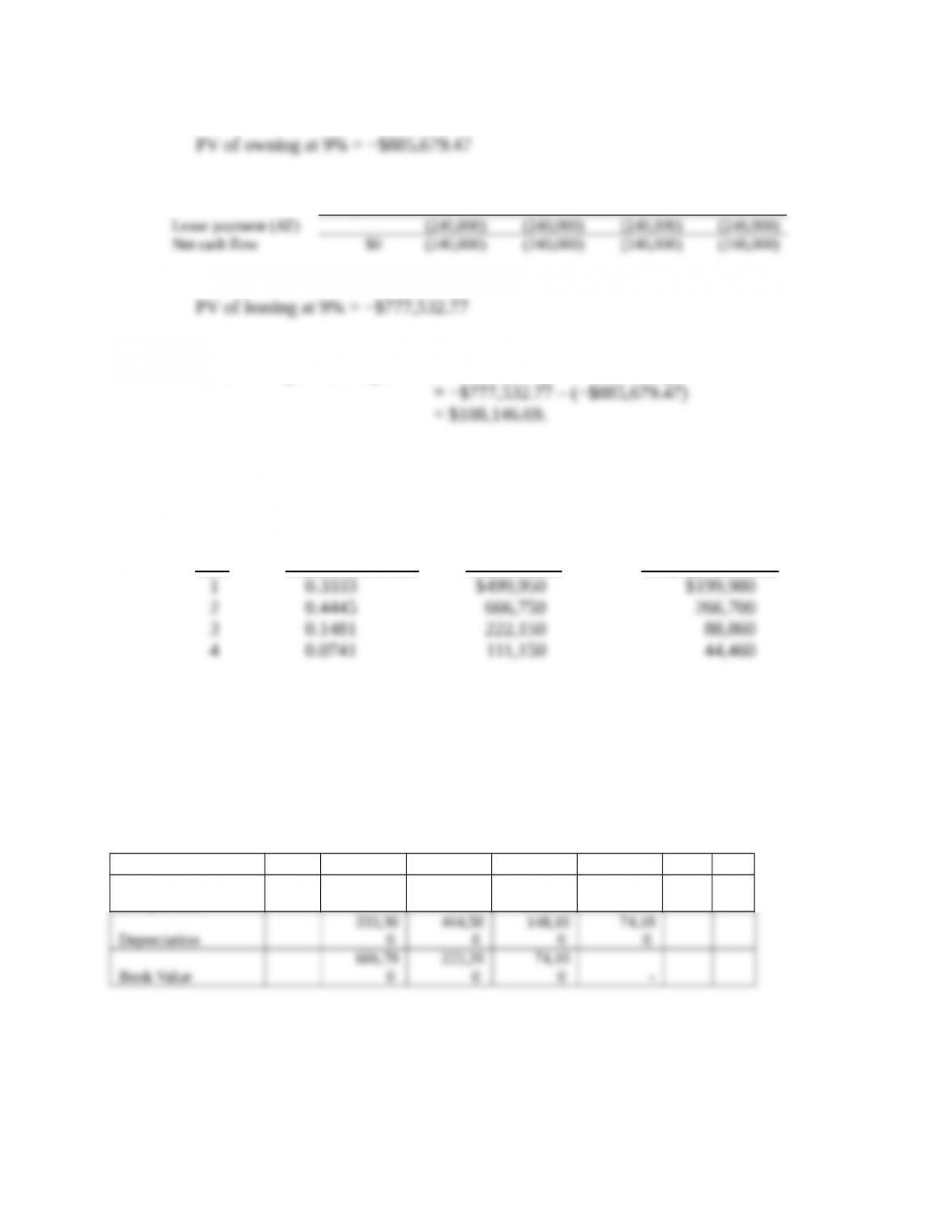

19-2 Cost of owning:

0 1 2

| | |

Cost (200)

0 1 2

| | |

After-tax lease payment (66) (66)

19-3 a. Balance sheets before lease is capitalized:

Energen

Balance Sheet (Owns new assets)

(Thousands of Dollars)

Hastings Corporation

Balance Sheet (Leases as operating lease)

(Thousands of Dollars)

b. Balance sheet after lease is capitalized:

Hastings Corporation

Balance Sheet (Capitalizes lease)

(Thousands of Dollars)

Current assets $ 25,000 Debt $ 50,000

19-4

I. Cost of Owning:

0 1 2 3 4

After-tax loan paymentsa($135,000) ($135,000) ($135,000) ($1,635,000)

II. Cost of Leasing:

0 1 2 3 4

III. Cost Comparison

Net advantage to leasing (NAL)= PV of leasing – PV of owning

aAfter-tax interest payments = (0.15)($1,500,000)(1-0.40) = $135,000.

bDepreciation tax savings, base on MACRS 3-year life and $1,500,000 cost of new

machinery:.

MACRS Deprec. Tax Savings

Year Allowance Factor Depreciation T (Depreciation)

Since the cost of leasing the machinery is less than the cost of owning it, Big Sky Mining

should lease the equipment.

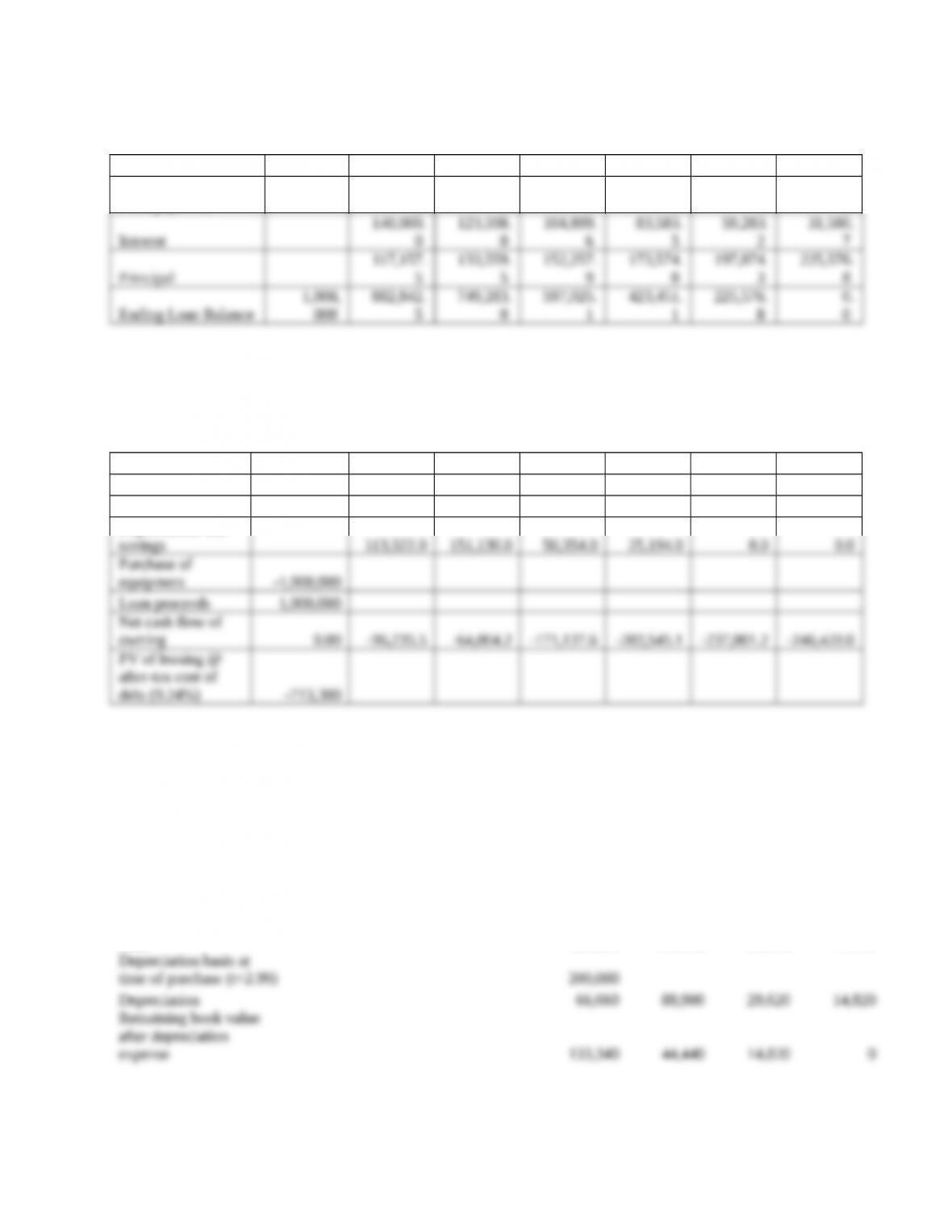

19-5 a. Borrow and buy analysis:

Cost of Owning: Intermediate Calculation: Depreciation Schedule of New Equipment Purchased

at t = 0.

Year 0 1 2 3 4 5 6

Depreciation rates for

new purchase 33.33% 44.45% 14.81% 7.41%

Cost of Owning: Intermediate Calculation: Amortization Schedule of Loan

Year 0 1 2 3 4 5 6

Loan payment

257,157.

5

257,157.

5

257,157.

5

257,157.

5

257,157.

5

257,157.

5

Cost of Owning: NPV Calculation

After-tax cost of debt = 14% x (1 – T) = 14% x (1 – 0.34) = 9.24%.

Depreciation tax savings = T(Depreciation).

Year 0 1 2 3 4 5 6

Loan payments -257,157.5 -257,157.5 -257,157.5 -257,157.5 -257,157.5 -257,157.5

Interest tax savings 47,600.0 42,023.3 35,665.9 28,418.4 20,156.3 10,737.5

Depreciation Tax

Cost of Leasing: Intermediate Calculation: Depreciation Schedule if Purchase Used Equipment

at End of Lease (Last day of 3rd t=2.99)

The machine will be depreciated according to the MACRS 3-year class schedule.

Year 0 1 2 3 4 5 6

Depreciation Schedule

for purchase at end of

lease 33.33% 44.45% 14.81% 7.41%

Cost of Leasing:

After-tax cost of lease = $320,000 (1 – T) = $320,000(1 – 0.34) = $211,200

Year 0 1 2 3 4 5 6

After-tax lease payment -211,200 -211,200 -211,200

Purchase of machine at end of

Because the NAL is positive, the company should choose the lease.

Note that the maintenance expense is excluded from the analysis since the firm

will have to bear the cost whether it buys or leases the machinery.

Because the firm is keeping the machine for at least 6 years (either because it

b. Using Goal Seek, we find that the purchase price can go up to $343,489 before the

NAL becomes negative.