Chapter 11

Cash Flow Estimation

and Risk Analysis

ANSWERS TO END-OF-CHAPTER QUESTIONS

11-1 a. Project cash flow, which is the relevant cash flow for project analysis, represents the

actual flow of cash, which includes investments in capital and working capital, but does

b. Incremental cash flows are those cash flows that arise solely from the asset that is being

evaluated. For example, assume an existing machine generates revenues of $1,000 per

year and expenses of $600 per year. A machine being considered as a replacement

would generate revenues of $1,000 per year and expenses of $400 per year. On an

incremental basis, the new machine would not increase revenues at all, but would

c. Net operating working capital changes are the increases in current operating assets

resulting from accepting a project less the resulting increases in current operating

d. Stand-alone risk is the risk a project would have if it was held in isolation. Corporate

(within-firm) risk is the risk that a project contributes to a company after taking into

e. Sensitivity analysis indicates exactly how much NPV or other output variables such as

IRR or MIRR will change in response to a given change in an input variable, other

things held constant. Sensitivity analysis is sometimes called “what if” analysis

f. A risk-adjusted discount rate incorporates the risk of the project’s cash flows. The cost

of capital to the firm reflects the average risk of the firm’s existing projects. Thus, new

g. A decision tree is a way of structuring a set of sequential decisions that depend on the

h. Real options occur when managers can influence the size and risk of a project’s cash

flows by taking different actions during the project’s life. They are referred to as real

i. Investment timing options give companies the option to delay a project rather than

implement it immediately. This option to wait allows a company to reduce the

uncertainty of market conditions before it decides to implement the project. Capacity

11-2 Only cash can be spent or reinvested, and since accounting profits do not represent cash,

they are of less fundamental importance than cash flows for investment analysis. Recall

11-3 Since the cost of capital includes a premium for expected inflation, failure to adjust cash

11-4 Capital budgeting analysis should only include those cash flows which will be affected by

the decision. Sunk costs are unrecoverable and cannot be changed, so they have no bearing

11-5 When a firm takes on a new capital budgeting project, it typically must increase its

investment in receivables and inventories, over and above the increase in payables and

11-6 Scenario analysis analyzes a limited number of outcomes. Although the base case scenario

may be the most likely, or expected outcome, the bad and good scenarios are frequently

worst case and best case scenarios, that is, when everything goes bad together, or

11-7 The costs associated with financing are reflected in the weighted average cost of capital.

11-8 Daily cash flows would be theoretically best, but they would be costly to estimate and

probably no more accurate than annual estimates because we simply cannot forecast

accurately at a daily level. Therefore, in most cases we simply assume that all cash flows

11-9 In replacement projects, the benefits are generally cost savings, although the new

machinery may also permit additional output. The data for replacement analysis are

11-10 Stand-alone risk is the project’s risk if it is held as a lone asset. It disregards the fact that

it is but one asset within the firm’s portfolio of assets and that the firm is but one stock in

a typical investor’s portfolio of stocks. Stand-alone risk is measured by the variability of

11-11 It is often difficult to quantify market risk. On the other hand, we can usually get a good

idea of a project’s stand-alone risk, and that risk is normally correlated with market risk:

SOLUTIONS TO END-OF-CHAPTER PROBLEMS

11-1 a. Equipment $ 17,000,000

c. The potential sale of the building represents an opportunity cost of conducting the project in

11-2 Operating Cash Flows: t = 1

Sales revenues $18,000,000

Operating costs 9,000,000

Place the cash flows on a time line:

With a financial calculator, input the appropriate cash flows into the cash flow register,

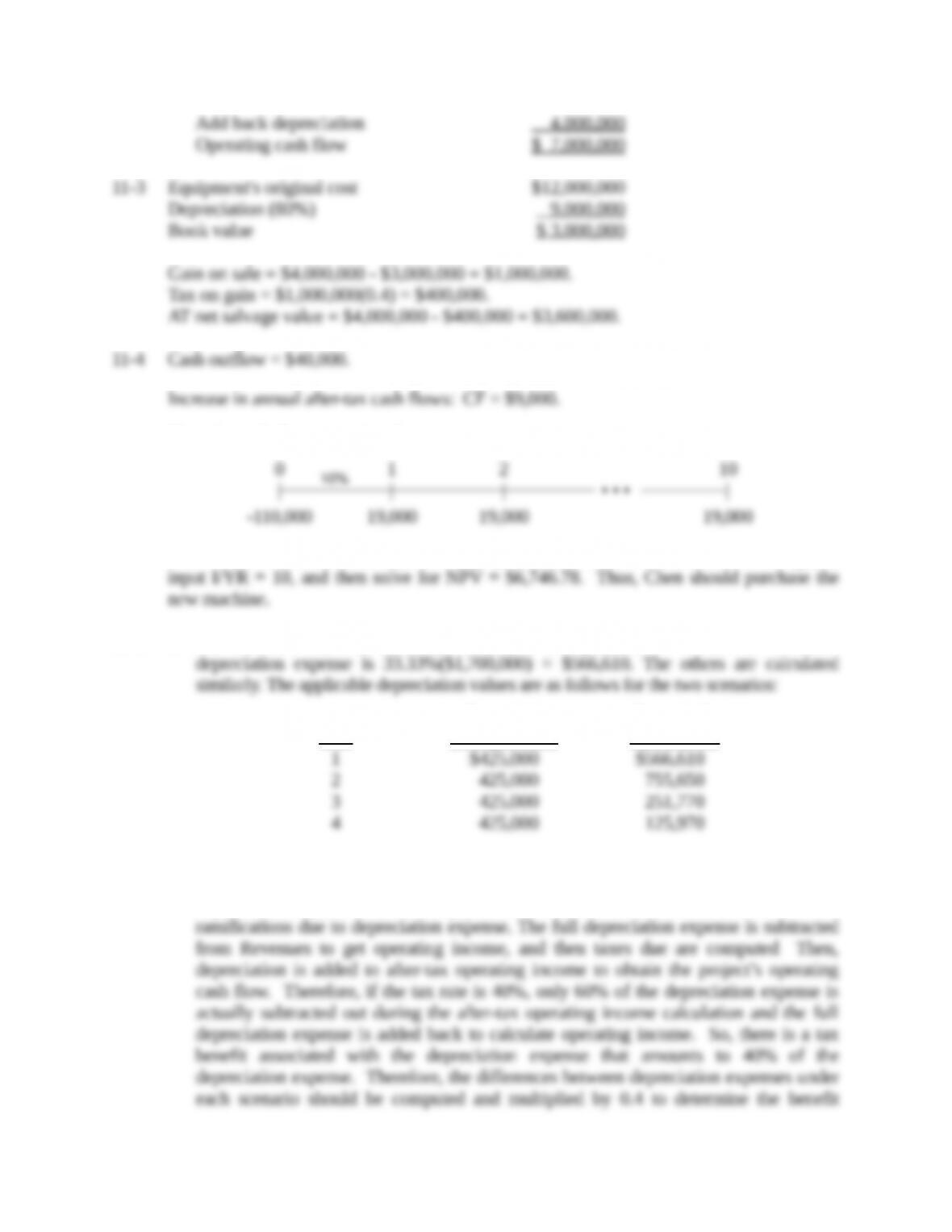

11-5 a. The MACRS rates are 33.33%, 44.45%, 14.81%, and 7.41%. The first MACRS

Scenario 1 Scenario 2

Year (Straight Line) (MACRS)

b. To find the difference in net present values under these two methods, we must

determine the difference in incremental cash flows each method provides. The

depreciation expenses cannot simply be subtracted from each other, as there are tax

provided by the depreciation expense.

Depreciation Expense Depreciation Expense

Year Difference (2 – 1) Diff. 0.4 (MACRS)

1 $141,610 $56,644

Now to find the difference in NPV to be generated under these scenarios, just enter the

cash flows that represent the benefit from depreciation expense and solve for net

present value based upon a cost of capital of 10%.

c. If Wendy’s boss has a bonus plan that depends on net income instead of cash flow, then

he will make a larger bonus in the first 2 years of the project if they use straight line

11-6 a. The net cost is $1,118,000:

Price ($1,080,000)

b. The operating cash flows follow:

Year 1 Year 2 Year 3

Notes:

2. The depreciation expense in each year is the depreciable basis, $1,102,500, times

c. The terminal year cash flow is $473,343:

Salvage value $605,000

d. The project has an NPV of $78,790; thus, it should be accepted.

Year Net Cash Flow PV @ 12%

0 ($1,118,000) ($1,118,000)

Alternatively, with a financial calculator, input the appropriate cash flows into the

11-7 a. The net cost is $89,000:

Price ($70,000)

b. The operating cash flows follow:

Year 1 Year 2 Year 3

Notes:

2. The depreciation expense in each year is the depreciable basis, $85,000, times the

Salvage value $30,000

d. The project has an NPV of -$6,700. Thus, it should not be accepted.

Year Net Cash Flow

0 ($89,000)