c. 3. Would the NPVs change if the cost of capital changed?

Answer: The NPV of a project is dependent on the cost of capital used. Thus, if the cost of

d. 1. Define the term internal rate of return (IRR). What is each franchise’s IRR?

Answer: The internal rate of return (IRR) is the discount rate that forces the NPV of a project

to equal zero:

0123

||||

CF0CF1CF2CF3

Expressed as an equation, we have:

Franchise L’s IRR is 18.1%:

0123

||||

IRR

18.1%

A financial calculator is extremely helpful when calculating IRRs. The cash flows are

entered sequentially, and then the IRR button is pressed. For Franchise S, IRRS ≈

d. 2. How is the IRR on a project related to the YTM on a bond?

d. 3. What is the logic behind the IRR method? According to IRR, which franchises

should be accepted if they are independent? Mutually exclusive?

Answer: IRR measures a project’s profitability in the rate of return sense: If a project’s IRR

equals its cost of capital, then its cash flows are just sufficient to provide investors

Projects’ IRRs are compared to their costs of capital, or hurdle rates. Since

d. 4. Would the franchises’ IRRs change if the cost of capital changed?

Answer: IRRs are independent of the cost of capital. Therefore, neither IRRS nor IRRL would

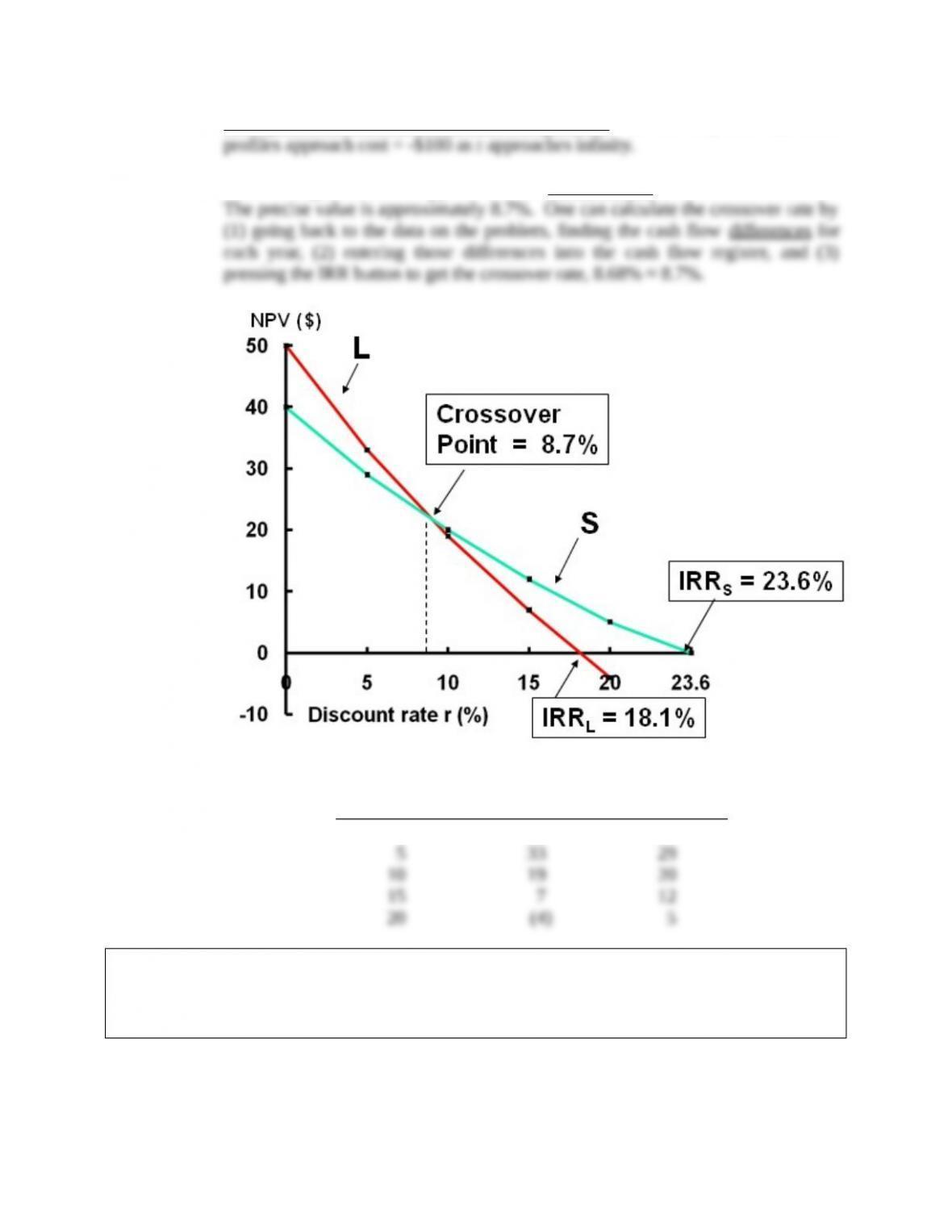

e. 1. Draw NPV profiles for Franchises L and S. At what discount rate do the profiles

cross?

Answer: The NPV profiles are plotted in the figure below.

Note the following points:

3. NPV profiles are curves rather than straight lines. To see this, note that these

4. From the figure below, it appears that the crossover rate is between 8% and 9%.

r NPVLNPVS

0% $50 $40

e. 2. Look at your NPV profile graph without referring to the actual NPVs and IRRs.

Which franchise or franchises should be accepted if they are independent?

Mutually exclusive? Explain. Are your answers correct at any cost of capital

less than 23.6%?

Answer: The NPV profiles show that the IRR and NPV criteria lead to the same accept/reject

decision for any independent project. Consider Franchise L. It intersects the X-axis

Now assume that L and S are mutually exclusive. In this case, a conflict might

f. What is the underlying cause of ranking conflicts between NPV and IRR?

Answer: For normal projects’ NPV profiles to cross, one project must have both a higher

vertical axis intercept and a steeper slope than the other. A project’s vertical axis

intercept typically depends on (1) the size of the project and (2) the size and timing

g. Define the term modified IRR (MIRR). Find the MIRRs for Franchises L and S.

Answer: MIRR is the discount rate that equates the present value of the terminal value of the

0123

||||

PV of TV = 100.00

MIRR = ?

r = 10%

i. 1. What is the payback period? Find the paybacks for Franchises L and S.

Answer: The payback period is the expected number of years required to recover a project’s

cost. We calculate the payback by developing the cumulative cash flows as shown

below for Franchise L (in thousands of dollars):

Expected NCF

Year Annual Cumulative

0 ($100) ($100)

0123

||||

Franchise L’s $100 investment has not been recovered at the end of Year 2, but it has

been more than recovered by the end of Year 3. Thus, the recovery period is between

i. 2. What is the rationale for the payback method? According to the payback

criterion, which franchise or franchises should be accepted if the firm’s

maximum acceptable payback is 2 years, and if Franchises L and S are

independent? If they are mutually exclusive?

Answer: Payback represents a type of “breakeven” analysis: The payback period tells us when

and t = 3

r = 10%

i. 3. What is the difference between the regular and discounted payback periods?

Answer: Discounted payback is similar to payback except that discounted cash flows are used.

Setup for Franchise L’s discounted payback, assuming a 10% cost of capital:

Expected Net Cash Flows

Cash Discounted Cumulative

Year Flows Cash Flows Cash Flows

i. 4. What is the main disadvantage of discounted payback? Is the payback method

of any real usefulness in capital budgeting decisions?

Answer: Regular payback has 3 critical deficiencies: (1) It ignores the time value of money,

(2) it ignores the cash flows that occur after the payback period, and (3) it does not