10-12 a. Purchase price $ 900,000

CF0 = -1065000; CF1-5 = 350000; I/YR = 14; NPV = ?

c. Environmental effects could be added by estimating penalties or any other cash

10-13 a.

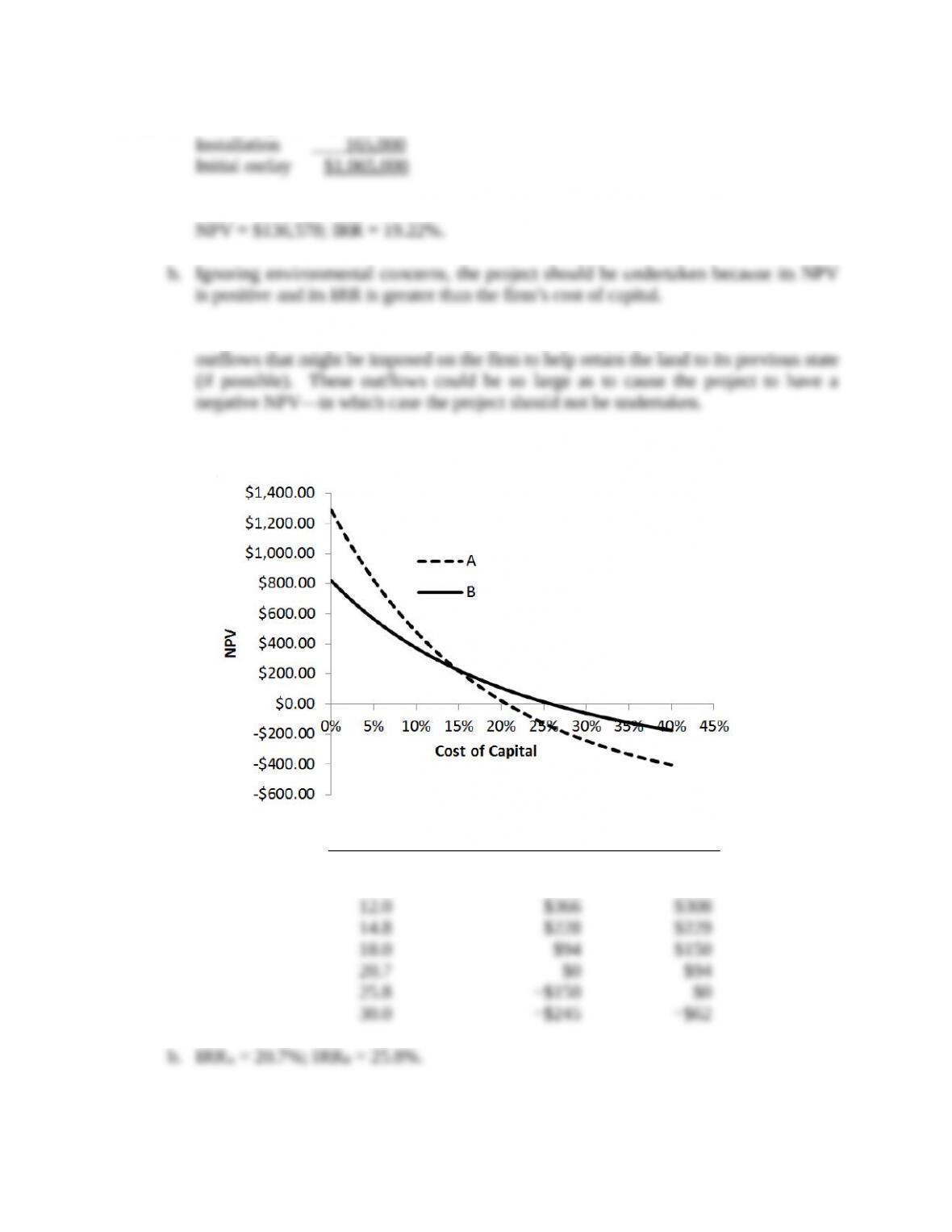

rNPVANPVB

0.0% $1,288 $820

10.0 $479 $372

c. At r = 10%, Project A has the greater NPV, specifically $478.83 as compared to

d. Here is the MIRR for Project A when r = 10%:

Now, MIRR is that discount rate which forces the PV of $3,545.30 in 7 years to equal

PV costs = 600.

At r = 17%,

e. To find the crossover rate, construct a Project ∆ which is the difference in the two

projects’ cash flows:

Year Project ∆ = CFA – CFB

0 $250

1 −738

Projects A and B are mutually exclusive, thus, only one of the projects can be chosen.

As long as the cost of capital is greater than the crossover rate, both the NPV and IRR

Because of the sign changes and the size of the cash flows, Project ∆ has multiple

IRRs. Thus, the IRR function for some calculators will not work (it will work,

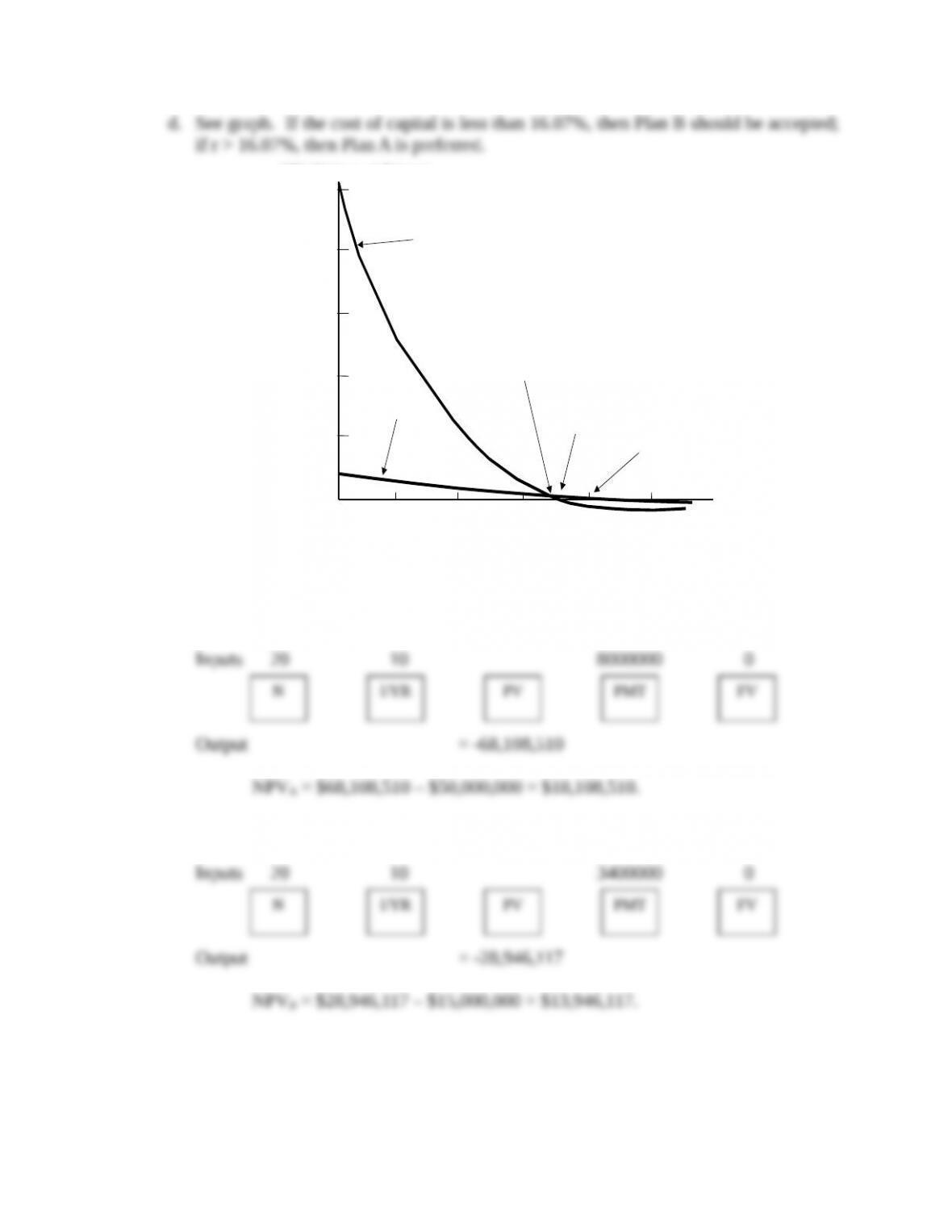

10-14 a. Incremental Cash

Year Plan B Plan A Flow (B – A)

b. If the firm could invest the incremental $10,250,000 at a return of 16.07%, it would

Financial calculator solution:

Output = 16.0665

c. Yes, assuming (1) equal risk among projects, and (2) that the cost of capital is a

constant and does not vary with the amount of capital raised.

10-15 a. Financial calculator solution:

Plan A

Plan B

N P V ( M i l l i o n s o f D o l l a r s )

B

C r o s s o v e r R a t e = 1 6 . 0 7 %

I R R

B

= 1 6 . 7 %

I R R

A

= 2 0 %

A

C o s t o f

C a p i t a l ( % )

5

2 5

1 0

2 0

1 5

1 5

2 0

1 0

2 5

5

Plan A

Plan B

b. If the company takes Plan A rather than B, its cash flows will be (in millions of dollars):

Cash Flows Cash Flows Project ∆

Year from A from B Cash Flows

0 ($50) ($15.0) ($35.0)

So, Project ∆ has a “cost” of $35,000,000 and “inflows” of $4,600,000 per year for 20

years.

Since IRR∆ > r, we should accept ∆. This means we should accept the larger project

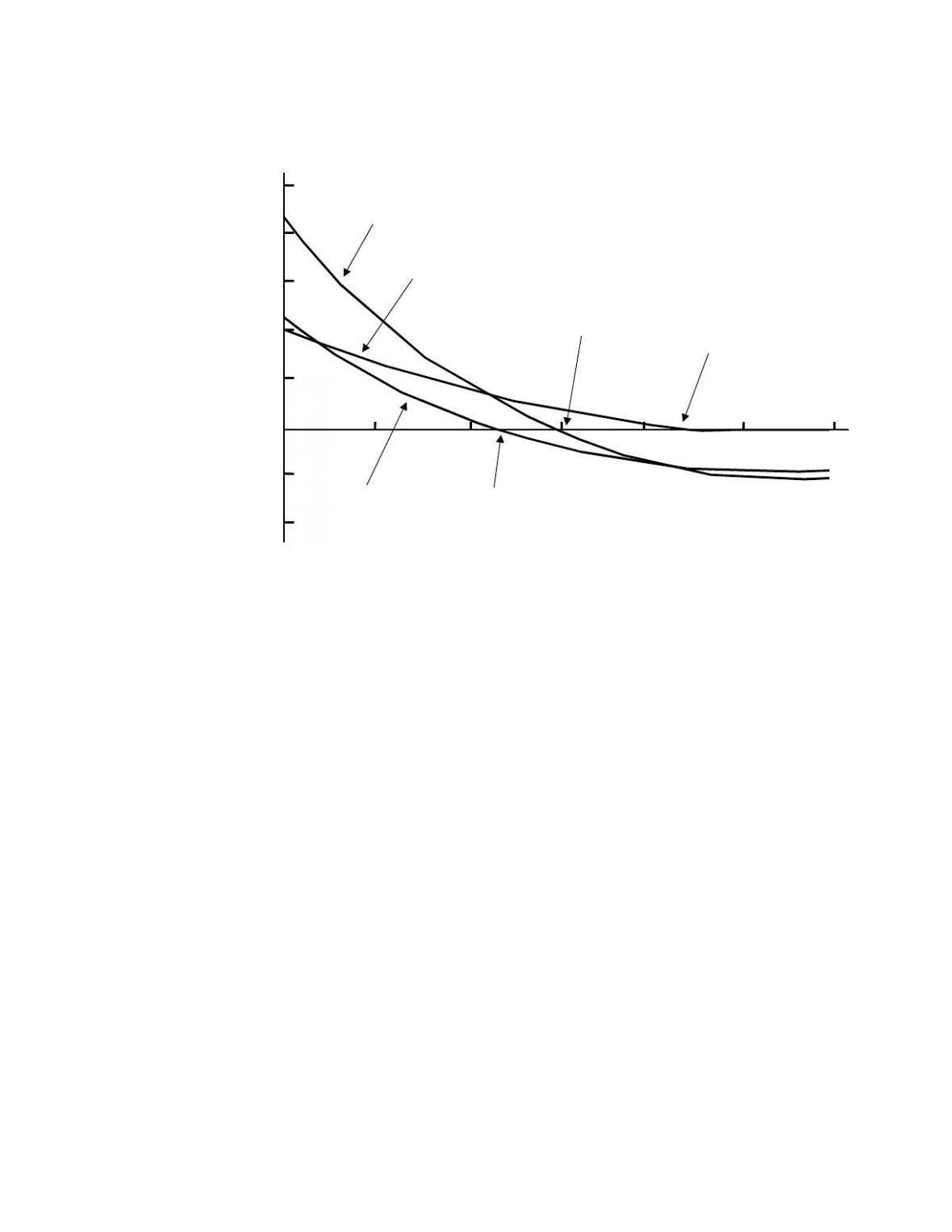

c.

N P V ( M i l l i o n s o f D o l l a r s )

C r o s s o v e r R a t e = 1 1 . 7 %

I R R A = 1 5 . 0 3 %

I R R B = 2 2 . 2 6 %

A

B

C o s t o f C a p i t a l ( % )

1 2 5

I R R = 1 1 . 7 %

1 0

1 0 0

7 5

1 5

5 0

2 0

2 5

2 5

– 2 5

3 0

– 5 0

5

10-16 Plane A: Expected life = 5 years; Cost = $100 million; NCF = $30 million;

COC = 12%.

Plane B: Expected life = 10 years; Cost = $132 million; NCF = $25 million;

COC = 12%.

-100

-70

012345678910

B:|||||||||||

-132 25 25 25 25 25 25 25 25 25 25

Enter these cash flows into the cash flow register, along with the interest rate, and

Project A is the better project and will increase the company’s value by $12.764

million.

The EAA of plane A is found by first finding the PV: N = 5, I/YR = 12, PMT = 30,

12%

12%

10-17 012345678

A:|||||||||

-10 4 4 4 4 4 4 4 4

-10

-6

Machine A’s simple NPV is calculated as follows: Enter CF0 = -10 and CF1-4 = 4. Then

enter I/YR = 10, and press the NPV key to get NPVA = $2.679 million. However, this

012345678

B:|||||||||

-15 3.5 3.5 3.5 3.5 3.5 3.5 3.5 3.5

For Machine B’s NPV, enter these cash flows into the cash flow register, along with

Machine A is the better project and will increase the company’s value by $4.51

million.

The EAA of Machine A is found by first finding the PV: N = 4, I/YR = 10, PMT =

For Machine B, we already found the NPV of $3.672 million. We convert this to

Again, the EAA method demonstrates that Machine A is the better project since

EAAA > EAAB.

10-18 Cash flow time line for Machine 190-3:

0123

||||

EAA190-3: Using a financial calculator, input the following data:

14%

10%

10%

Cash flow time line for Machine 360-6:

0123456

|||||||

EAA360-6: Using a financial calculator, input the following data:

Both new machines have positive NPVs; hence, the old machine should be replaced.

14%