Chapter 19 ♦ Pricing Concepts 1

CHAPTER 19 Pricing Concepts

This chapter begins with the learning outcome summaries, followed by a set of lesson plans for you to use to

deliver the content in Chapter 19.

• Lecture (for large sections) on page 4

• Company Clips (video) on page 5

• Group Work (for smaller sections) on page 6

Review and Assignments begin on page 8

Review questions

Application questions

Application exercise

Ethics Exercise

Video assignment

Case assignment

Great Ideas for Teaching Marketing from faculty around the country begin on page 18

2 Chapter 19 ♦ Pricing Concepts

LEARNING OUTCOMES

19-1 Discuss the importance of pricing decisions to the economy and to the individual firm

Pricing plays an integral role in the U.S. economy by allocating goods and services among consumers, governments, and

businesses. Pricing is essential in business because it creates revenue, which is the basis of all business activity. In setting

prices, marketing managers strive to find a level high enough to produce a satisfactory profit. Profit drives growth, salary

increases, and corporate investment.

Price × Sales Unit = Revenue

Revenue − Costs = Profit

Profit drives growth, salary increases, and corporate investment

19-2 List and explain a variety of pricing objectives

Establishing realistic and measurable pricing objectives is a critical part of any firm’s marketing strategy. Pricing

objectives are commonly classified into three categories: profit oriented, sales oriented, and status quo. Profit-oriented

pricing is based on profit maximization, a satisfactory level of profit, or a target return on investment (ROI). The goal of

profit maximization is to generate as much revenue as possible in relation to cost. Often, a more practical approach than

profit maximization is setting prices to produce profits that will satisfy management and stockholders. The most common

profit-oriented strategy is pricing for a specific ROI relative to a firm’s assets. The second type of pricing objective is

sales oriented, and it focuses on either maintaining a percentage share of the market or maximizing dollar or unit sales.

The third type of pricing objective aims to maintain the status quo by matching competitors’ prices.

19-3 Explain the role of demand in price determination

Demand is a key determinant of price. When establishing prices, a firm must first determine demand for its product. A

typical demand schedule shows an inverse relationship between quantity demanded and price: when price is lowered,

sales increase; when price is increased, the quantity demanded falls. For prestige products, however, there may be a

direct relationship between demand and price: the quantity demanded will increase as price increases.

Marketing managers must also consider demand elasticity when setting prices. Elasticity of demand is the degree to

which the quantity demanded fluctuates with changes in price. If consumers are sensitive to changes in price, demand is

elastic; if they are insensitive to price changes, demand is inelastic. Thus, an increase in price will result in lower sales

for an elastic product and little or no loss in sales for an inelastic product.

19-4 Understand the concepts of dynamic pricing and yield management systems

When competitive pressures are high, a company must know when it can raise prices to maximize its revenues. Dynamic

pricing allows companies to adjust prices on the fly to meet demand. Yield management systems use complex

mathematical software to fill unused capacity profitably. The software uses techniques such as discounting early

purchases, limiting early sales at these discounted prices, and overbooking capacity. These systems are used in service

and retail businesses and are substantially raising revenues.

19-5 Describe cost-oriented pricing strategies

The other major determinant of price is cost. Marketers use several cost-oriented pricing strategies. To cover their own

expenses and obtain a profit, wholesalers and retailers commonly use markup pricing: they tack an extra amount on to

the manufacturer’s original price. Another pricing strategy determines how much a firm must sell to break even; this

amount in turn is used as a reference point for adjusting price.

19-6 Demonstrate how the product life cycle, competition, distribution and promotion strategies,

customer demands, the Internet and extranets, and perceptions of quality can affect price

The price of a product normally changes as it moves through the life cycle and as demand for the product and

competitive conditions change. Management often sets a high price at the introductory stage, and the high price tends to

attract competition. The competition usually drives prices down because individual competitors lower prices to gain

market share. Adequate distribution for a new product can sometimes be obtained by offering a larger-than-usual profit

margin to wholesalers and retailers. The Internet enables consumers to compare products and prices quickly and

Chapter 19 ♦ Pricing Concepts 3

efficiently. Price is also used as a promotional tool to attract customers. Special low prices often attract new customers

and entice existing customers to buy more. Large buyers can extract price concessions from vendors. Such demands can

squeeze the profit margins of suppliers. Perceptions of quality can also influence pricing strategies.

19-7 Describe the procedure for setting the right price

The process of setting the right price on a product involves four major steps: (1) establishing pricing goals; (2) estimating

demand, costs, and profits; (3) choosing a price policy to help determine a base price; and (4) fine-tuning the base price

with pricing tactics. A price strategy establishes a long-term pricing framework for a good or service. The three main

types of price policies are price skimming, penetration pricing, and status quo pricing.

19-8 Identify the legal constraints on pricing decisions

Government regulation helps monitor four major areas of pricing: unfair trade practices, price fixing, price

discrimination, and predatory pricing. Many states have enacted unfair trade practice acts that protect small businesses

from large firms that operate efficiently on extremely thin profit margins; the acts prohibit charging below-cost prices.

The Sherman Act and the Federal Trade Commission Act prohibit both price fixing, which is an agreement between two

or more firms on a particular price, and predatory pricing, in which a firm undercuts its competitors with extremely low

prices to drive them out of business. Finally, the Robinson-Patman Act of 1936 makes it illegal for firms to discriminate

between two or more buyers in terms of price. Predatory pricing is the practice of charging a very low price for a product

with the intent of driving competitors out of business or out of a market.

19-9 Explain how discounts, geographic pricing, and other pricing tactics can be used to fine-tune

a base price

Several techniques enable marketing managers to adjust prices within a general range in response to changes in

competition, government regulation, consumer demand, and promotional and positioning goals. Techniques for fine–

tuning a price can be divided into three main categories: discounts, allowances, rebates, and value-based pricing;

geographic pricing; and other pricing tactics.

The first type of tactic gives lower prices to those who pay promptly, order a large quantity, or perform some

function for the manufacturer. Additional tactics in this category include seasonal discounts, promotion allowances, and

rebates (cash refunds).

Geographic pricing tactics—such as FOB origin pricing, uniform delivered pricing, zone pricing, freight absorption

pricing, and basing-point pricing—are ways of moderating the impact of shipping costs on distant customers.

A variety of other pricing tactics stimulate demand for certain products, increase store patronage, and offer more

merchandise at specific prices.

More and more customers are paying price penalties, which are extra fees for violating the terms of a purchase

contract. The perceived fairness or unfairness of a penalty may affect some consumers’ willingness to patronize a

business in the future.

TERMS

bait pricing

inelastic demand

promotional allowance (trade

allowance)

base price

keystoning

quantity discount

basing-point pricing

leader pricing (loss-leader pricing)

rebate

break-even analysis

market share

return on investment (ROI)

cash discount

markup pricing

revenue

consumer penalty

noncumulative quantity discount

seasonal discount

cumulative quantity discount

odd-even pricing (psychological

pricing)

single-price tactic

demand

penetration pricing

status quo pricing

dynamic pricing

predatory pricing

supply

elastic demand

price

two-part pricing

elasticity of demand

price bundling

unfair trade practice acts

extranet

price fixing

uniform delivered pricing

4 Chapter 19 ♦ Pricing Concepts

fixed cost

price lining

value-based pricing

flexible pricing (variable pricing)

price skimming

variable cost

FOB origin pricing

price strategy

yield management systems

(YMS)

freight absorption pricing

profit

zone pricing

functional discount (trade

discount)

LESSON PLAN FOR LECTURE

Brief Outline and Suggested PowerPoint Slides:

Learning Outcomes and Topics

PowerPoint Slides

LO1 Discuss the importance of pricing decisions to the

economy and to the individual firm

19-1 The Importance of Price

1: Pricing Concepts

2: Learning Outcomes

3: Learning Outcomes

4: Learning Outcomes

5: The Importance of Price

6: The Importance of Price

7: What Is Price?

8: The Importance of Price to Marketing Managers

LO2 List and explain a variety of pricing objectives

19-2 Pricing Objectives

9: Pricing Objectives

10: Pricing Objectives

11: Profit-Oriented Pricing Objectives

12: Profit Maximization

13: Return on Investment (ROI)

14: Sales-Oriented Pricing Objectives

15: Market Share

16: Sales Maximization

17: Status Quo Pricing Objectives

LO3 Explain the role of demand in price determination

19-3 The Demand Determinant of Price

18: The Demand Determinant of Price

19: The Demand Determinant of Price

20: How Demand and Supply Establish Price

21: Elasticity of Demand

22: Factors that Affect Elasticity of Demand

LO4 Understand the concepts of dynamic pricing and

yield management systems

19-4 The Power of Dynamic Pricing and Yield

Management Systems

23: The Power of Dynamic Pricing and Yield

Management Systems

24: Dynamic Pricing

25: Yield Management Systems

26: Yield Management Systems

LO5 Describe cost-oriented pricing strategies

19-5 The Cost Determinant of Price

27: The Cost Determinant of Price

28: The Cost Determinant of Price

29: Setting Prices

30: Markup Pricing

Chapter 19 ♦ Pricing Concepts 5

Learning Outcomes and Topics

PowerPoint Slides

LO6 Demonstrate how the product life cycle,

competition, distribution and promotion strategies,

customer demands, the Internet and extranets, and

perceptions of quality can affect price

19-6 Other Determinants of Price

31: Other Determinants of Price

32: Other Determinants of Price

33: Stages in the Product Life Cycle

34: The Competition

35: Distribution Strategy

36: The Impact of the Internet and Extranets

37: Promotion Strategy

38: Demands of Large Customers

39: The Relationship of Price to Quality

40: Dimensions of Quality

LO7 Describe the procedure for setting the right price

19-7 How to Set a Price on a Product

41: How to Set a Price on a Product

42: Setting the Right Price

43: Choose a Price Strategy

44: Price Skimming

45: Penetration Pricing

46: Status Quo Pricing

LO8 Identify the legal constraints on pricing decisions

19-8 The Legality of Price Strategy

47: The Legality of Price Strategy

48: The Legality of Price Strategy

49: Unfair Trade Practices and Price Fixing

50: Price Discrimination

51: Price Discrimination

52: Predatory Pricing

LO 9 Explain how discounts, geographic pricing, and

other pricing tactics can be used to fine-tune a base

price

19-9 Tactics for Fine-Tuning the Base Price

53: Tactics for Fine-Tuning the Bae Price

54: Tactics for Fine-Tuning the Bae Price

55: Discounts, Allowances, Rebates, and Value-Based

Pricing

56: Geographic Pricing

57: Other Pricing Tactics

58: Consumer Penalties

59: Chapter 19 Video

60: Part 6 Video

Suggested Homework:

• The end of this chapter contains assignments on the Ski Butternut video.

• This chapter’s online study tools include flashcards, visual summaries, practice quizzes, and other resources that can

be assigned or used as the basis for longer investigations into marketing.

LESSON PLAN FOR VIDEO

Company Clips

Segment Summary: Ski Butternut

Ski Butternut is a ski mountain in the Berkshires dedicated to offering a great family ski value. In this video, Matt

Sawyer discusses the various ways that Ski Butternut uses pricing to drive new business and local business to the

mountain. He also discusses how correct pricing can help the next year’s business model through season pass sales.

These teaching notes combine activities that you can assign students to prepare before class, that you can do in class

before watching the video, that you can do in class while watching the video, and that you can assign students to

complete as assignments after watching the video in class.

6 Chapter 19 ♦ Pricing Concepts

During the viewing portion of the teaching notes, stop the video periodically where appropriate to ask students the

questions or perform the activities listed on the grid. You may even want to give the students the questions before

starting the video and have them think about the answer while viewing the segment. That way, students will be engaged

in active rather than passive viewing.

PRE-CLASS PREP FOR YOU:

PRE-CLASS PREP FOR YOUR STUDENTS:

• Preview the Company Clips video segment for

Chapter 19. This exercise reviews concepts for LO1–

LO6.

• Review your lesson plan.

• Make sure you have all of the equipment needed to

show the video to the class, including the DVD and a

way to project the video.

• You can also stream the video HERE

• Have students review and familiarize themselves with

the following terms and concepts: importance of

pricing decisions, pricing objectives, demand

determinant of price, and cost determinant of price.

• Have students bring written definitions of the above

terms or concepts to class.

• Ask students to visit http://www.skibutternut.com/ and

review its current pricing.

VIDEO REVIEW EXERCISE

ACTIVITY

Warm Up

Briefly discuss students’ findings from the Pre-Class Prep activity about the Ski Butternut Web site.

Was pricing straightforward and easy to understand? Who is the target market?

In-class

Preview

• Discuss pricing objectives with the class. Highlight the concepts of profit maximization, target

ROI, and sales maximization.

• Discuss demand determinants of price with the class. Point out how demand and supply work

together to determine price, the elasticity of demand, and how yield management systems work.

• Have copies of the Company Clips questions (below) available for students to take notes on

while viewing the video segment.

Viewing

(solutions

below)

1. How do the product, place, and promotion elements of Ski Butternut’s marketing mix influence

the pricing strategy the company has chosen?

2. Would you expect demand for Ski Butternut lift tickets to be elastic? Why or why not?

3. What role do the product life cycle, competition, and perceptions of quality play in Ski

Butternut’s pricing?

Follow-up

• Divide students into groups of three to five and have them figure out a way to apply a yield

management system (YMS) to Ski Butternut’s business model. Give them about 5 to 10 minutes

to come up with a solution, and, time permitting, have them share their ideas with the class.

• What type of pricing strategy does Ski Butternut employ?

Solutions for Viewing Activities

1. How do the product, place, and promotion elements of Ski Butternut’s marketing mix influence the pricing

strategy the company has chosen?

Ski Butternut offers rentals, lift tickets, and classes on its beginner-level mountain, which is located relatively near

2. Would you expect demand for Ski Butternut lift tickets to be elastic? Why or why not?

3. What role do the product life cycle, competition, and perceptions of quality play in Ski Butternut’s pricing?

PLC plays less of a role in Butternut’s pricing. Skiing is a very mature industry, but it is challenging for new

Chapter 19 ♦ Pricing Concepts 7

addressed the simplicity of its mountain by adding terrain parks, which attract a younger audience. Ski Butternut

wants to be a family mountain that offers quality skiing for the target market, but its pricing reflects that it is for

families and to encourage college students to Ski Butternut.

LESSON PLAN FOR GROUP WORK

Class Activity 1 – Retail Price Comparison

To demonstrate to students the wide variation in pricing of an identical item, ask them to visit three different stores and

compare prices on similar items.

First, each student should select a category of store. Some suggestions are:

• Grocery: large chain store, local chain store, convenience store

• Health and beauty aids: grocery store, drugstore, discount store

• Over-the-counter drugs: chain drugstore, local drugstore, discount store

• Clothing: specialty store, department store, discount store

A student who chooses to investigate clothing stores could compare the price of Levi’s 501 jeans for men at the three

different types of stores. A student who chooses health and beauty aids could compare the price of a certain brand of

shampoo (same size, weight, and so on) at the three stores. Students may come up with other categories and items of

interest.

If possible, each student should select several items to compare in his or her category. For example, in the grocery

category, a student may want to compare a type of cereal, a canned soup, and a snack item.

Students who travel home every weekend may want to compare prices between towns, which is also a very interesting

exercise.

After the investigation, ask students what factors they believe lead to the variations in prices. Is it worthwhile for

consumers to compare prices when they shop?

This assignment can lead to a very interesting discussion of price competition, nonprice competition, odd–even pricing,

promotional pricing, price lining, and unit pricing.

Class Activity 2 – Pricing Strategies

The goal of this exercise is to make students aware of pricing strategies used by the airline industry.

• Have your students collect price quotes for airline tickets to a city with departure dates that are less than 7, 14,

and over 21 days from the present date. How do the prices differ?

• Then have them include a Saturday night stay and no Saturday night stay. How do the prices vary now?

• Have them check the same flight schedule comparing coach, business, and first class fares.

• What kind of pricing strategy is being used?

8 Chapter 19 ♦ Pricing Concepts

REVIEW AND ASSIGNMENTS FOR CHAPTER 19

REVIEW QUESTIONS

1. Why is pricing so important to the marketing manager?

2. How does price allocate goods and services?

Price sets the image of the good. In conjunction with quality, price is part of the formula for value. Even though

3. Why do many firms not maximize profits?

One reason that firms do not maximize value is that they can only charge a price that equates to a perceived value.

4. Explain the role of supply and demand in determining price.

The price that is set depends on pricing goals and the demand for the good or service, the cost to the seller for that

5. Explain the concepts of elastic and inelastic demand. Why should managers understand these concepts?

Elasticity of demand refers to consumers’ responsiveness or sensitivity to changes in price. Elastic demand occurs

6. Explain the relationship between supply and demand and yield management systems.

Students’ answers will vary.

7. Why are so many companies adopting yield management systems?

A yield management system (YMS) is a technique for adjusting prices so that unused capacity is filled. YMSs are

8. Why is it important for managers to understand the concept of break-even points? Are there any drawbacks?

The advantage of break-even analysis is that a firm can quickly discover how much it must sell to cover costs and

9. Give an example of each major type of pricing objective.

Pricing objectives are commonly classified into three categories and students are to come up with one example of

each:

10. What are the three basic defenses that a seller can use if accused under the Robinson-Patman Act?

The Robinson-Patman Act provides three defenses for the seller charged with price discrimination (in each case the

APPLICATION QUESTIONS

1. If a firm can increase its total revenue by raising its price, shouldn’t it?

It may only increase revenue in the short run. In the long run, buyers may find substitutes for the good, or

2. Your firm has based its pricing strictly on cost in the past. As the newly hired marketing manager, you

believe this policy should change. Write the president a memo explaining your reasons.

Although students’ answers will vary, they should address some of these points: Prices determined strictly on the

3. Divide the class into teams of five. Each team will be assigned a different grocery store from a different chain

(an independent store is fine, too). Appoint a group leader. The group leaders should meet as a group and

pick fifteen nationally branded grocery items. Each item should be specifically described as to brand name

and size of the package. Each team will then proceed to its assigned store and collect price data on the fifteen

items. The team should also gather price data on fifteen similar store brands and fifteen generics, if possible.

Each team should present its results to the class and discuss why there are price variations between stores,

national brands, store brands, and generics.

As a next step, go back to your assigned store and share the overall results with the store manager. Bring

back the manager’s comments and share them with the class.

Results will vary by group.

4. How does the stage of a product’s life cycle affect price? Give some examples.

10 Chapter 19 ♦ Pricing Concepts

Demand factors and competitive conditions tend to change as a product moves through the different stages of its life

5. Go to Priceline.com. Can you research a ticket’s price before purchasing it? What products and services are

available for purchase? How comfortable are you with naming your own price? Relate the supply and

demand curves to customer-determined pricing.

Student answers will vary as to their comfort with naming their own price. Periodically, Priceline.com changes the

6. You are contemplating a price change for an established product sold by your firm. Write a memo analyzing

the factors you need to consider in your decision.

Although students’ answers will vary, they should address some of these points: Before instituting a price change,

7. Develop a price line strategy for each of these firms: a) a college bookstore, b) a restaurant, c) a video-rental

firm.

Product line pricing is setting prices for an entire line of products, which is a broader concern than setting the right

8. The U.S. Postal Service regularly raises the price of a first-class stamp but continues to operate in the red

year after year. Is uniform delivered pricing the best choice for first-class mail?

Students’ responses will vary. In general, it would seem more lucrative for the USPS to use zone pricing, but the

APPLICATION EXERCISE

Reliance on price as a predictor of quality seems to occur for all products. Does this mean that high-priced products are

superior? Well, sometimes. Price can be a good predictor of quality for some products, but for others, price is not always

the best way to determine the quality of a product or service before buying it. This exercise (and worksheet) will help

you examine the price–quality relationship for a simple product: canned goods.

Activities

Chapter 19 ♦ Pricing Concepts 11

1. Take a trip to a local supermarket where you are certain to find multiple brands of canned fruits and

vegetables. Pick a single type of vegetable or fruit you like, such as cream corn or peach halves, and list

five or six brands in the worksheet on the following page.

Price

1

2

3

4

5

6

7

Brand

QualityRank

(y)

Price/Weight

Price per

Ounce

Price

Rank (x)

d

(y-x)

d2

TOTAL

2. Before going any further, rank the brands according to which you think is the highest quality (1) to the

lowest quality (5 or 6, depending on how many brands you find). This ranking will be y.

3. Record the price and the volume of each brand. For example, if a 14-ounce can costs $.89, you would list

$.89/14 oz.

4. Translate the price per volume into price per ounce. Our 14-ounce can costs $.064 per ounce.

5. Now rank the price per ounce (we’ll call it x) from the highest (1) to the lowest (5 or 6, again depending on

how many brands you have).

6. We’ll now begin calculating the coefficient of correlation between the price and quality rankings. The first

step is to subtract x from y. Enter the result, d, in column 6.

7. Now calculate d2 and enter the value in column 7. Write the sum of all the entries in column 7 in the final

row.

8. The formula for calculating a price–quality coefficient r is as follows:

rs=1 – 6∑ d2

( n3 – n)

In the formula, rs is the coefficient of correlation, 6 is a constant, and n is the number of items ranked.

9. What does the result of your calculation tell you about the correlation between the price and the quality of

the canned vegetable or fruit you selected? Now that you know this, will it change your buying habits?

Purpose: To have students investigate the relationship between price and quality and perceptions of quality.

Setting It Up: This exercise requires high-school algebra to calculate the price–quality coefficient. You can assign this

as an individual or group project.

This exercise was inspired by the following Great Idea in Teaching Marketing:

Vaughn C. Judd

12 Chapter 19 ♦ Pricing Concepts

Auburn University Montgomery

ANALYZING THE PRICE–QUALITY RELATIONSHIP

The relationship between product price and quality is more relevant to students when they analyze it using third-party

data. Food product ratings in Cook’s Illustrated magazine provide the data for the analyses. Consumer Reports, however,

can be used as a data source if Cook’s Illustrated is not readily available. The Spearman rank correlation coefficient, an

easy statistic to calculate in class with a hand-held calculator, is used to measure the relationship.

An Example of the Process

Step 1: Students are grouped in teams of two or three. Each team is given a reprint of a different food review from

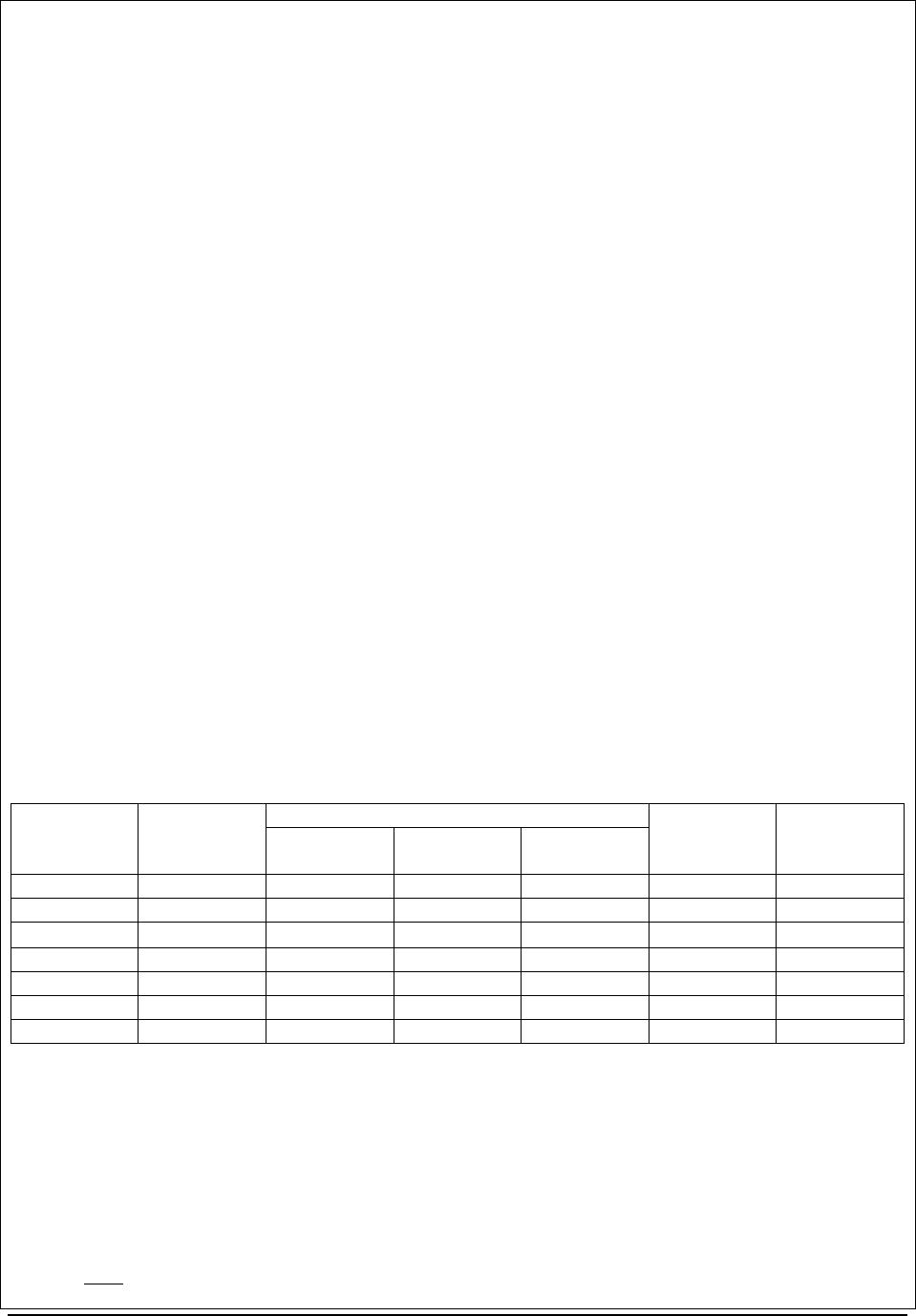

Cook’s Illustrated magazine and a worksheet that is equivalent in form to Table 1, but with only the column headings.

Step 2: The example, Table 1, is based on ratings of six brands of canned red kidney beans. Students list the brands in

column 1 and the rank order of quality in column 2—the best quality being ranked number one. Although there are no

ties in quality ranks in this example, brands are sometimes tied.

Step 3: Students then list the price and volume of each brand in column 3. Since the cans contain different volumes, the

prices from column 3 are converted to per ounce equivalents in column 4. The prices shown in column 4 are ranked from

highest to lowest (1 = highest) in column 5. Note that there are two brands with identical prices—at $.030/ounce. Using

the midrank method for handling ties, these brands are each ranked 5.5.

Step 4: Students next calculate the coefficient of correlation between the quality and price rankings. First, they complete

the d (difference) column by subtracting the x rank from the y rank for each brand, then the d2 column by squaring the

values in the d column and summing them up. Finally, the coefficient of correlation is calculated.

Step 5: Each group is asked to draw conclusions regarding the relationship between price and quality for the brands

analyzed, and to report the conclusions to the class. The conclusions, based on the coefficients, are noted on the

chalkboard. Also they are asked how successful a consumer would be in obtaining quality by picking the highest– or

lowest-priced brands. With regard to canned red kidney beans, there is a strong association between quality and price.

Unfortunately for consumers, the relationship is in the wrong direction as expressed by the –.90 coefficient. Also, out of

the six brands evaluated, the highest-priced brand ranked last in quality.

Table 1 Canned Red Kidney Beans

(1)

Brand

(2)

Quality Rank

Price

(6)

d

(y–x)

(7)

d2

(3)

Price/Wt.

(4)

*Price per U

(5)

Price Rank

Green Giant

1

$.59/15.5 oz.

$.038

5.5

–4.5

20.25

Goya

2

$.59/15.5oz.

$.038

5.5

–3.5

12.25

S&W

3

$1.09/15 oz.

$.073

3

0

0

Progresso

4

$.89/19 oz.

$.047

4

0

0

Wesbrae

5

$1.59/15 oz.

$.106

2

3.0

9.00

Eden

6

$1.99/15oz.

$.133

1

5.0

25.0

TOTAL

66.5

Source: Cook’s Illustrated (September/October 1997)

*Converted to a per/ounce basis

The formula for calculating Spearman’s rho is:

rs = 1 – 6d2

(n3 – n)

Chapter 19 ♦ Pricing Concepts 13

Where: rs= Spearman rank order correlation, d, = difference in rank in the paired rankings, n = number of items ranked,

and 6 = a constant in the formula.

Calculation:

rs = 1 – 6(66.5)/(63 – 6)

rs = l – (1.90)

rs = –.90

Conclusion

Discovering on one’s own is an important element of learning. This exercise provides that opportunity. Students sharing

their discoveries with their fellow classmates further complement the learning process. Finally, from the shared findings

there is an opportunity to generalize about the price–quality relationship. Obviously the results will vary depending on

the product categories assigned. With regard to food products, however, experience has shown that there tends to be low

levels of correlation between price and quality.

ETHICS EXERCISE

Advanced Bio Medics (ABM) has invented a new stem–cell–based drug that will arrest even advanced forms of lung

cancer. Development costs were actually quite low because the drug was an accidental discovery by scientists working

on a different project. To stop the disease requires a regimen of one pill per week for 20 weeks. There is no substitute

offered by competitors. ABM is thinking that it could maximize its profits by charging $10,000 per pill. Of course, many

people will die because they can’t afford the medicine at this price.

1. Should ABM maximize its profits?

Profit maximization entails setting prices so that total revenue is as large as possible relative to total costs. It is not

2. Does the AMA Statement of Ethics address this issue? Go to http://www.marketingpower.com and review the

Statement. Then write a brief paragraph on what the AMA Statement of Ethics contains that relates to

ABM’s dilemma.

The AMA Statement of Ethics does not specifically address profit maximization in its pricing section. The

VIDEO ASSIGNMENT: Ski Butternut

Ski Butternut is a ski mountain in the Berkshires dedicated to offering a great family ski value. In this video, Matt

Sawyer discusses the various ways that Ski Butternut uses pricing to drive new business and local business to the

mountain. He also discusses how correct pricing can help the next year’s business model through season pass sales.

1. First time skiiers demonstrate elastic demand.

a. True

14 Chapter 19 ♦ Pricing Concepts

b. False

2. When Ski Butternut reduced the first time skier package from $135 to $75, first time skiiers

a. experienced unitary elasticity for ski lessons.

b. saw a profit maximization scheme based on discounting the first visit and charging a lot more once the skier

is hooked.

c. saw a perceived reasonable value for an activity they haven’t tried yet.

d. bartered for lower priced rentals.

3. Knowing that weather can affect the profits for a ski area, but also that offering low prices drives more locals to Ski

Butternut, Matt Sawyer is saying that Ski Butternut is aiming for profit maximization.

a. True

b. False

4. Moving from $199 season pass to $275 season pass was part of a trial and error of pricing promotions for Ski

Butternut. They have stayed at the $275 price point

a. because it maximizes profits.

b. because it meets costs without exceeding the competition’s prices.

c. because it makes the cost an inconsequential part of an individual’s budget.

d. because the decline stage can cause some prices to increase.

5. According to the video, college students respond really well when Ski Butternut takes $20 off the price of a lift

ticket. College students

a. are sensitive to price changes—they have inelastic demand.

b. are sensitive to price changes—they have elastic demand.

c. are sensitive to price changes—they have unitary elasticity.

d. are insensitive to price changes—they have elastic demand.

6. Pricing lift tickets at $25 Monday-Friday to drive customers to Ski Butternut is an aggressive pricing structure

designed to increase market share by taking mid-week skiers away from other mountains.

a. True

b. False

7. Matt Sawyer says that Ski Butternut increases its holiday prices by five dollars because otherwise the “quality of

the experience will deteriorate.” This suggests that on holidays:

a. supply exceeds demand

b. the equilibrium price has been reached

c. demand exceeds supply

Chapter 19 ♦ Pricing Concepts 15

d. there is unitary elasticity

CASE ASSIG NMEN T: Pric e Ma t c hing

In an effort to stem their losses and gain an advantage over their Internet competitors, Target and Best Buy recently

announced a price-matching policy. During the holiday shopping season of 2012, both retailers promised that they would

match the prices offered by a number of popular online retailers such as Amazon and Walmart.com. According to Target

CEO Gregg Steinhafel, the price match move was intended to show consumers that Target should be their preferred

shopping destination. “We’re already rock solid in price. But if periodically some competitor has a lower price, this gives

our guests the ability to know ‘I can do all of my one–stop shopping in Target.’”

On the surface of things, the price-match policies seem to favor consumers, since they can physically check out a

product and get the lowest price. However, a number of exceptions to both policies made them difficult and frustrating to

use. For example, shoppers have to ask for the price cuts and show proof of the lower price to an in-store employee.

“Can you imagine,” asked CEO of CFI Group Sheri Petras, “being on the checkout line at Target with 21 items and

you’re scanning products on your phone to find out the gum is 12 cents less at Amazon? Can you imagine standing

behind that person in line?”

Many retail experts believe that, far from increasing physical store sales, such price-matching policies may actually

do the opposite. They suggest that it is simply too difficult to match Internet prices since they fluctuate so much.

Moreover, they argue that even with a price-match, there simply is not enough motivation for customers to drive to the

store, wait in line, and hope that an employee doesn’t make them the exception to the rule.

Ann Zimmerman, “We Promise to Match Prices*,” Wall Street Journal, October 18, 2012, B1, B4; Ann

Zimmerman and Elizabeth Holmes, “Target Vows Price Match,” Wall Street Journal, October 17, 2012, B6; Tom

Gara, “Best Buy’s Online Price Matching: There Is a Catch,” Wall Street Journal, October 12, 2012,

http://blogs.wsj.com/corporate-intelligence/2012/10/12/best-buys-online-price-matching-there-is-a-catch (Accessed

March 26, 2013).

TRUE/FALSE

1. If, instead of case-by–case price matching, Target used Amazon’s pricing structure to set its own prices across the board,

it would be using status quo pricing.