The Movie Exhibition Industry: 2015

Movie Exhibition Industry – 1

INTRODUCTION

This case is an in-depth study of the motion picture exhibition industry which

exposes the tenuous and uncertain outlook for movie theater owners. Changing value

chain dynamics and operating variables that affect the profitability of exhibitors are

discussed, with comparisons provided for the four major exhibitor circuits in the U.S. The

impact of evolving digital technology, trends which influence consumer decisions (most

notably, consumer viewing practices in the age of portable devices), and constraints

within the studio-dominated business model are also reviewed in detail. The case then

closes with a discussion of some of the initiatives taken by exhibitors to confront existing

environmental challenges.

The objective of this case is to thoroughly examine industry conditions and the

performance of key industry participants in order to identify strategic measures which

might improve the viability of major exhibitor operations. By profiling the external

environment, the industry’s competitive forces, competitor circumstances and approaches,

and the standard business revenue/cost structure, meaningful strategic alternatives can be

proposed to aid movie theater owners in their struggle to remain profitable and to

increase their likelihood for success.

• Review trends in the general environment that affect the movie exhibition

business, and establish whether their effects are helpful or harmful to theater

owners.

• Assess the five competitive forces at work in the industry environment. Identify

the forces that threaten the profitability of prevailing movie circuits, and prescribe

the level of competition that can be anticipated amongst industry rivals.

• Perform comparative situation and strategy analyses for the four companies with

dominant market share. What are the advantages and disadvantages for each of

the industry’s top competitors?

• Evaluate the revenue sources and major costs for movie exhibitors. Discuss how

the income structure of their business impacts their financial results.

• Summarize your findings and the current situation for exhibitor circuits. Based on

your analysis, what strategic actions do you propose for theater operators to

increase the appeal of the theater setting to attract the audiences needed for

improved performance under existing industry conditions?

ANALYSIS

• Review trends in the general environment that affect the movie exhibition business,

and establish whether their effects are helpful or harmful to theater owners.

The forces existing in the general environment are beyond the control of

companies competing in the film industry. Nevertheless, these external conditions can

create opportunities and/or threats that will impact the performance and success of movie

The Movie Exhibition Industry: 2015

Movie Exhibition Industry – 2

exhibition firms. Key trends in each of the general environmental segments that have the

greatest potential impact on theater owners are outlined and discussed below.

» Americans spend a very large amount of time on entertainment, and movie viewing is

a prevalent form of entertainment in the U.S. In particular, teens and young adults

frequently seek entertainment options outside of the home for dating purposes. While

these sociocultural conditions should be viewed with optimism, movies are more

widely available to the public than ever. Consequently, with a profusion of substitute

viewing options emerging, the long-term trend in per-capita admissions is negative.

» Studios focus on 12-24 year olds who are consistently the largest demographic group

of movie goers. At just 18% of the U.S. population, this group purchases 30% of all

tickets. (More narrowly, 10% of the population is “frequent” movie goers who attend

more than one movie per month and are responsible for half of all ticket sales.)

The Movie Exhibition Industry: 2015

Movie Exhibition Industry – 3

Demographic

Group

Population

Change

2014-2035

(in millions)

Population

Change

2014-2035

(in percent)

Per Screen

Change

2014-2035

(in millions)

Per Screen

Change 2014-

2035 (in

percent)

2 to 11 yrs

6.8

16%

170

10%

12 to 17 yrs

5.3

21%

132

15%

18 to 24 yrs

4.6

15%

114

13%

25 to 39 yrs

8.9

14%

223

15%

40 to 49 yrs

6.8

16%

170

11%

50 to 59 yrs

-0.1

0%

-2

0%

60 yrs+

33.6

53%

839

36%

Total (mil.)

65.8

19%

1,646

14%

In addition, technological advancements and dramatically reduced prices in retail

electronic equipment have increased the availability, affordability, quality, and

number of “in-home theaters”. Even without home screening rooms, 77% of U.S.

households now have at least one HD television (which deliver very high quality

visual images); and the average TV set in 2014 was 39 inches (up 7 inches in just four

years). Coupled with trends in the use of portable devices and the threat of “Ultra”

HD or 4K televisions hitting the market, these developments are having a

transformational effect on movie (and media) viewing choices and are reducing the

novelty of the exhibition theater setting. These conditions are threats that are likely to

continue to have a significant negative impact on the profit potential of film

exhibitors.

The Movie Exhibition Industry: 2015

Movie Exhibition Industry – 4

• Assess the five competitive forces at work in the industry environment. Identify the

forces that threaten the profitability of prevailing movie circuits, and prescribe the

level of competition that can be anticipated amongst industry rivals.

Threat of New Entrants – Low

Supplier Power – Very High

The strength of studio bargaining power is the leading cause of the industry’s low

profitability. Exhibitors, and their financial well-being, are heavily dependent on studio

policy decisions. Currently, over 81% of box office receipts are generated from the top 6

motion picture studios. These content providers completely control the release channel(s)

The Movie Exhibition Industry: 2015

Movie Exhibition Industry – 5

Buyer Power – Moderate

The industry’s core customer audience is 12- to 24-year-olds, who purchased 30%

of all movie tickets sold in 2014. The preferences and tastes of this age group can be

Product Substitutes – High

The availability of alternatives to movie theaters is another powerful force

working against theater owner profitability. While the industry is seeing the allure of its

value proposition and the theatrical experience diminish, product substitutes are rapidly

Intensity of Rivalry – Moderate

Since the 1980s, declining ticket sales, rising operating costs, and the advent of

The Movie Exhibition Industry: 2015

Now, four major theater companies, with just 24.3% of all cinemas, operate 45.5% of the

industry’s existing screens. The typical exhibitor location has 7-12 screens, which

improves labor and facility efficiencies and increases operator bargaining power.

Excess screen capacity in the U.S. affects the level of industry competition. High

costs associated with the development of megaplexes and with the conversion to digital

home, conveniences (such as parking), and proximity to restaurants (all variables which

cannot be readily changed without large capital allocations).

• Perform comparative situation and strategy analyses for the four companies with

dominant market share. What are the advantages and disadvantages for each of the

industry’s top competitors?

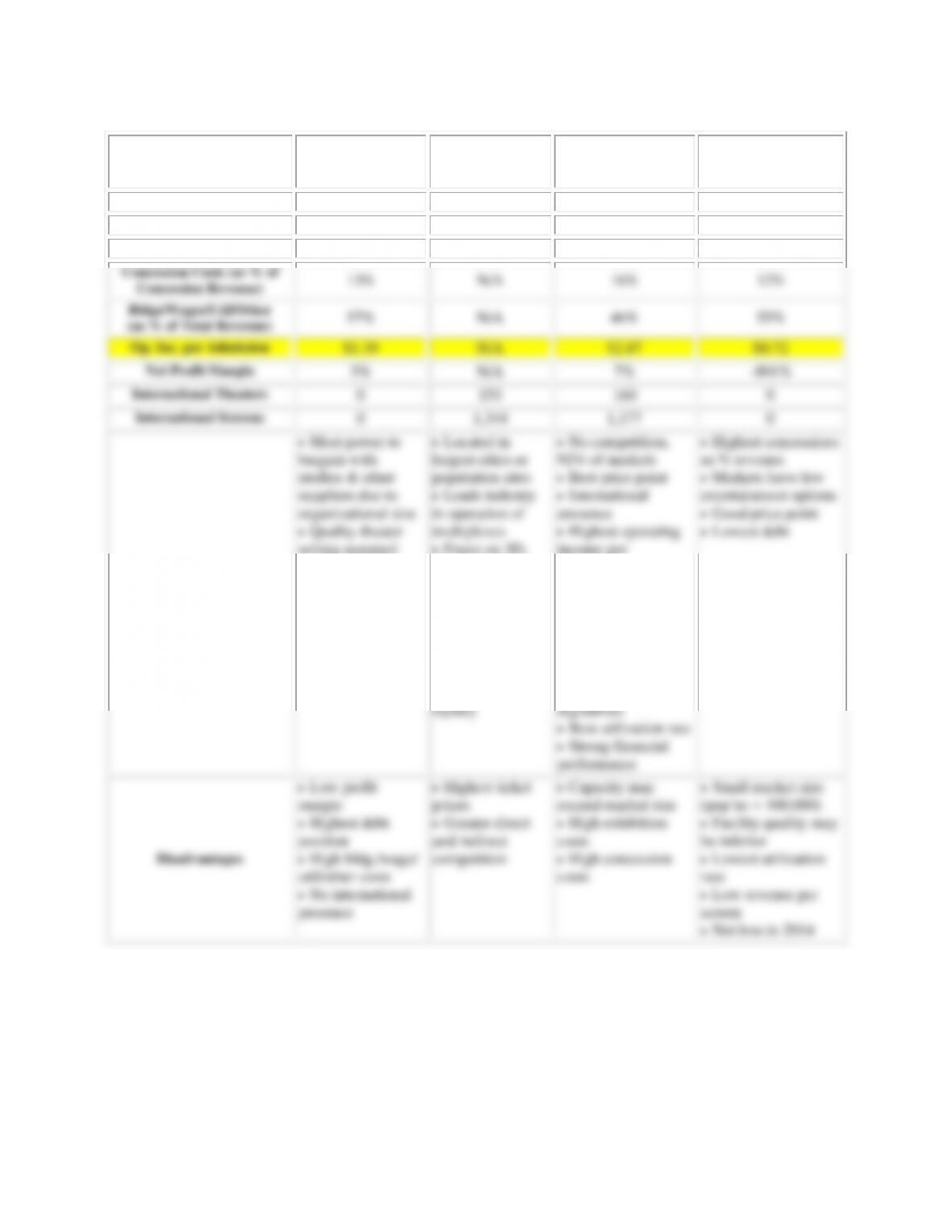

An overview of the top four competitors’ business situations and approaches

provides valuable insight for industry participants seeking to improve performance. The

following table presents a comparison of the market focus, facilities, pricing, costs,

The Movie Exhibition Industry: 2015

continued

Regal

(w/ United Artists

and Edwards)

AMC

(w/ Lowes and

Wanda)

Cinemark

(w/ Century)

Carmike

Admissions (as % of Rev)

67%

N/A

63%

62%

Concessions (as % of Rev)

28%

N/A

32%

33%

Exh Costs (as % Adm Rev)

52%

53%

56%

55%

Concession Costs (as % of

Concession Revenue)

13%

N/A

16%

12%

Bldgs/Wages/Util/Other

(as % of Total Revenue)

57%

N/A

46%

55%

Op. Inc. per Admission

$1.39

N/A

$2.87

$0.72

Net Profit Margin

3%

N/A

7%

–891%

International Theaters

0

153

160

0

International Screens

0

1,344

1,177

0

Advantages

• Most power to

bargain with

studios & other

suppliers due to

organizational size

• Quality theater

setting assumed

• Highest revenue

per screen and

admissions as %

revenue

• Largest domestic

exhibitor

• Lowest exhibition

costs as % revenue

• Located in

largest cities or

population sites

• Leads industry

in operation of

multiplexes

• Focus on 3D,

IMAX, and other

premium viewing

experiences

• International

(Asian) scope

through Wanda

acquisition

• Expanding

rapidly

• No competition,

92% of markets

• Best price point

• International

presence

• Highest operating

income per

admissions

• Greatest total

assets

• Highest NP margin

and operating

income per

admissions

• Completely

digitalized

• Best utilization rate

• Strong financial

performance

• Highest concessions

as % revenue

• Markets have few

entertainment options

• Good price point

• Lowest debt

Disadvantages

• Low profit

margin

• Highest debt

position

• High bldg./wage/

util/other costs

• No international

• Highest ticket

prices

• Greater direct

and indirect

competition

• Capacity may

exceed market size

• High exhibition

costs

• High concession

costs

• Small market size

(pop’ns < 100,000)

• Facility quality may

be inferior

• Lowest utilization

rate

• Low revenue per

A close look at the theater business model reveals that cinema managers have

limited ability to impact revenues with existing tangible and intangible resources. In

addition, restricted power or flexibility to control product, facility, and labor costs leaves

The Movie Exhibition Industry: 2015

Movie Exhibition Industry – 8

operating margins near just 12% across the industry. These constraints severely limit

financial control and profit potential for theater owners.

The table below dissects the revenue structure and helps to identify earnings

barriers faced by movie theater managers.

Movie theater profitability is severely hampered by this income structure, and

when trends in both the general and industry environments are also considered, long-term

viability is untenable. Because of the power imbalance with studios, increasing box office

receipts provides virtually no additional income for theater owners, even though they

represent the greatest source of revenue. In addition, consumer tolerance for higher ticket

prices (which have risen 27% since 2005) is low despite that fact that they have risen less

than the inflation rate. Even 3D movies, which temporarily yielded revenue growth, have

seen fewer ticket sales each year since 2010. And although concession sales are the

Revenue

Source

Percentage

of Total

Revenues

Margin

Over Direct

Costs

Comments

Ticket Sales

63%

0%

Loss leadership on movies. Ticket revenues

essentially cover commitment to studios and

costs of operations, facilities, and debt.

Concession

Sales

30%

85%

Largest source of exhibitor income. Highly

influenced by attendance, but also pricing

and supply costs. Prices at maximum. Caps

on volume per patron.

Advertising

Sales

5%

100%

Highly profitable. Has increased 100% in the

past decade. Attractive source of income, but

low audience tolerance.

The Movie Exhibition Industry: 2015

Movie Exhibition Industry – 9

EXHIBITOR EXPENSES

Per Screen

% of

Total

Expenses

% Box

Office

Revenues

Fixed

Facility

$65,942

17%

25.6%

Labor

$39,565

10%

15.3%

Utilities

$48,358

12%

18.7%

Other SG&A

$79,131

20%

30.7%

Total Fixed Costs

$232,997

60%

90.3%

Variable

Film Rental

$139,278

36%

54.0%

Concession Supplies

$17,898

5%

6.9%

Total Variable Costs

$157,177

40%

60.9%

Total Expenses

$390,174

100%

151.3%

BOX OFFICE REVENUE

$257,923

66%

100.0%

STRATEGY

• Summarize your findings and the current situation for exhibitor circuits. Based on

your analysis, what strategic actions do you propose for theater operators to

increase the appeal of the theater setting to attract the audiences needed for

improved performance under existing industry conditions?

The situation overview pinpoints the many factors which are diminishing movie

theater profitability. Today, cinemas are operating from a position of weakness. They are

competing against substitute products, constrained by supplier power, managing an

unprofitable business model, and facing long-term declines in admissions per capita.

Conditions in the general environment are mostly harmful to domestic exhibitors. Global

forces are changing the dynamics of the industry, and technological investment demands

are high with elusive pay-offs. But some bright spots exist – particularly with demand for

quality entertainment, demographic trends if studios look beyond today’s core audience,

and opportunities to grow internationally. To find success, industry leaders must

minimize pressures which are squeezing earnings from all directions and develop

conditions which create superior value for which customers are willing to pay.

The Movie Exhibition Industry: 2015

Movie Exhibition Industry – 10

Because participants in the industry cannot rely on standard business-level

strategies and because of their inability to increase margins by controlling revenue or cost

variables, leaders will find it necessary to discover new and creative strategic measures to

improve or sustain the profitability of ongoing operations.

The completed analysis suggests that to enhance performance and improve the

likelihood of future success, theater operators need to take measures to reduce the

bargaining power of studios and to stimulate demand for established cinema complexes.

It is a question of enhancing profits, increasing venue appeal, and taking steps to reduce

uncertainty. Exhibitors must think in terms of efforts that will offset the high costs of

existing facilities. The following recommendations offer feasible strategies for meeting

these objectives. Suggestions range from smaller scale actions to larger scale cooperative

strategies and facility re-design. Due to the failing business model, retaining patrons and

growing profits may require such dramatic actions by exhibitors.

The Movie Exhibition Industry: 2015

Movie Exhibition Industry – 11

o Engage studios in mutually-beneficial partnership arrangements. While delivery

channels are emerging and evolving, studios are taking steps to recover lost DVD

sales and to react to the success and power of VOD providers. Even though they

o Cater to semi-frequent and frequent movie goers. To deliver the “experience”

being sought by their core audience and to increase attendance of tentative patrons,

theaters need to overcome the declining value proposition and initiate customer

outreach efforts. This involves focusing on quality measures and deepening the

richness and affiliation of customer relationships.

The case material emphasizes that cost, home viewing options, theater

interruptions or distractions, inconvenience, and screen advertising all impact the

quality of the theater experience. Perceived quality can be enhanced through

o Seek alternative facility uses and content. The conversion of most theaters to

digital projection creates great potential to find and offer alternative content.

Alternative content can attract new audiences in novel ways, especially during

off-peak time periods. The greatest advantage of this strategy is that it reduces

theaters’ over-dependence on powerful studios – removing income restraints and

protecting against failure to receive viable hit films. At the time of the case,

exhibitors have begun to collectively seek alternative content through

intermediary distributor services. The benefits of this option are emerging.

The Movie Exhibition Industry: 2015

Movie Exhibition Industry – 12

educational showings, school activities, or other celebratory events (such as

reunions, couples’ wedding showers, or octogenarian guests of honor). With

widespread personal video recording taking place, screening customized content

for such events can be done with very little cost or effort. In fact, the exhibitor

might be able to produce and deliver the content for a surcharge or fee. Theaters

could restage classics or offer series marathons, turning them into social events,

particularly during slow sales periods. Perhaps new forms of health treatment or

therapeutic experiences could be designed with new immersive technologies for

senior or specialty audiences (such as the use of massage seating, sound therapy,

etc.)

o Expand entertainment value of offering. This option involves diversifying into

other forms of entertainment and services or changing the format of the venue

entirely. Partnering with commercial development, restaurant, or other

entertainment groups is a potential way of expanding the service “menu” at

theater facilities. This might involve ideas such as bringing in unique snacking

options (such as ethnic foods or pop-up restaurants/kiosks of the ”mobile food

The Movie Exhibition Industry: 2015

Movie Exhibition Industry – 13

One of the most promising new entertainment offerings is the use of interactive

digital experiences (made possible by new digital technologies, immersive

technologies, and social media capabilities) for purposes other than interactive

advertising. The core theater audience is a media-driven, gaming generation. (In

fact, the original “gamers” are now middle aged men.) Cooperative strategies with

gaming companies could generate especially appealing prospects. Not only could

they offer exciting new experiences for targeted electronic gamers to increase

demand; but if successful, they would create competition for studios to book

theater space (decreasing supplier power). In addition, integrating the social

With this suggestion, viewing selections and flexibility can be increased –

particularly with the growing availability of original digital content. Alliances

with companies like Netflix, Comcast, Hulu, or other major content providers

(even television and cable networks for marathon events of popular series, such as

‘Breaking Bad’ and ‘The Walking Dead’) would secure viewing material and,

again, reduce dependence on studios. Tapping into the recent phenomenon of TV

“binging”, theaters could offer marathon weekends of popular content for

enthusiasts to view full seasons or series with a like-minded crowd.

The Movie Exhibition Industry: 2015

Movie Exhibition Industry – 14