Chapter 5/Consumer Choice: Individual and Market Demand

CHAPTER 5

CONSUMER CHOICE: INDIVIDUAL AND

MARKET DEMAND

Chapter 5 goes behind the market demand curve of Chapter 4 to show how it is based on the

preferences of individual consumers. The text develops the theory of marginal utility for a single

good; the appendix considers indifference curves in the case of two goods.

CHAPTER OUTLINE

SCARCITY AND DEMAND

Because income is limited, the decisions by a consumer to purchase different commodities

must be interdependent.

UTILITY: A TOOL TO ANALYZE PURCHASE DECISIONS

The theory of consumer choice states that each consumer spends his or her income in a way that

yields the greatest satisfaction (utility). Ultimately, the purpose of utility analysis is analyzing

how people behave, not what they think.

Total versus Marginal Utility

Total utility is the benefit to a consumer from all the units of a good purchased.

The “Law” of Diminishing Marginal Utility

The more of a good a consumer has, the less marginal utility an additional unit contributes to

overall satisfaction.

Using Marginal Utility: The Optimal Purchase Rule

When possible, a consumer should buy the quantity of each good at which price and marginal

utility are exactly equal.

From Diminishing Marginal Utility to Downward-Sloping Demand Curves

Because people’s marginal utility declines with the number of goods bought, demand curves

are negatively sloped.

Chapter 5/Consumer Choice: Individual and Market Demand

BEHAVIORAL ECONOMICS: ARE ECONOMIC DECISIONS REALLY

MADE “RATIONALLY”?

Economists and psychologists have questioned the assumption that economic decisions are

made rationally. Such research has led to a school of thought called behavioral economics.

CONSUMER CHOICE AS A TRADE-OFF: OPPORTUNITY COST

The decision to purchase something is simultaneously a decision to forgo something else.

Consumer’s Surplus: The Net Gain from a Purchase

Because purchases are voluntary, it follows that the purchaser must come out ahead.

RESOLVING THE DIAMOND-WATER PUZZLE

A commodity that is scarce, like diamonds, will have a high marginal utility and a high price,

when compared to a commodity that is plentiful, like water.

The plentiful commodity, however, often provides greater total utility.

Income and Quantity Demanded

FROM INDIVIDUAL DEMAND CURVES TO MARKET DEMAND

CURVES

The market demand curve is the horizontal sum of the individual demand curves.

The “Law” of Demand

Demand curves normally have a negative slope.

Chapter 5/Consumer Choice: Individual and Market Demand

Exceptions to the Law of Demand

Exceptions can occur:

1. some inferior goods

APPENDIX: ANALYZING CONSUMER CHOICE GRAPHICALLY:

INDIFFERENCE CURVE ANALYSIS

Geometry of the Available Choices: The Budget Line

The budget line is a graphical representation of all possible combinations of a household’s

purchases of two goods, given their prices and a fixed amount of money to spend.

Properties of the Budget Line

The budget line represents the maximum amounts of the commodities the consumer can

afford.

Changes in the Budget Line

What the Consumer Prefers: Properties of the Indifference Curve

An indifference curve is a line connecting all combinations of the commodities that are

equally desirable.

Properties of the indifference curve:

1. a higher indifference curve is preferred

2. indifference curves never intersect

The Slopes of Indifference Curves and Budget Lines

The slope of the indifference curve is the marginal rate of substitution of the two

commodities.

Chapter 5/Consumer Choice: Individual and Market Demand

Tangency Conditions

A consumer-maximizing utility will choose the point on the budget line tangent to an

Consequences of Income Changes: Inferior Goods

In the case of inferior goods, indifference curves are located such that an increase in income

leads to an increase in purchases of the normal good, but a reduction in purchases of the

inferior good.

Consequences of Price Changes: Deriving the Demand Curve

A fall in price changes the slope of the budget line and leads (usually) to an increase in

MARGIN DEFINITIONS

Total Monetary Utility: the maximum amount of money that a consumer is willing to pay for a

quantity of a good.

Marginal Utility: the maximum amount of money that a consumer is willing to pay for one

more unit of a good.

“Law” of Diminishing Marginal Utility: additional units of a commodity are worth less and

less to a consumer in money terms.

Marginal Analysis: a method for calculating optimal choices – the choices that best promote the

decision maker’s objective. It works by testing whether, and by how much, a small change in a

Chapter 5/Consumer Choice: Individual and Market Demand

Slope of an Indifference Curve: the maximum amount of one commodity a consumer is willing

to give up in exchange for one more unit of another commodity; also referred to as the marginal

rate of substitution.

MAJOR IDEAS

1. As consumers buy a good, the extra benefit they derive from each additional unit

declines.

2. For rational consumers, the marginal utility curve describes the demand curve.

3. When possible, a consumer should buy the quantity of each good at which price and

ON TEACHING THE CHAPTER

This material is fundamental, but instructors often have difficulty making it come alive for the

students. One strategy is to ask the students to predict their own responses in different market

situations (for example, a changing price of hamburgers), and then show how an economist

models that behavior.

One typical response from students is that this modeling is all silly, because they never knew a

consumer who consciously equated marginal utility and price. This can be a good place to take a

step back, and ask what economic models are and are not useful for. Of course people in a

supermarket aisle do not calculate marginal utility curves and equate them to price. Neither does

a driver on a two-lane road solve a differential equation before deciding whether she can pass the

car ahead and not crash into the approaching truck. But a traffic engineer might well find a

differential equation helpful in predicting how frequently passing attempts will be made at

Chapter 5/Consumer Choice: Individual and Market Demand

thing. One approach to take is this: Every consumer has a marginal utility curve for different

goods, a curve that is given by his or her tastes. Every consumer has a demand curve for different

goods, a curve that reflects his or her behavior as prices change. What makes the marginal utility

and the demand curves identical is the assumption that the consumer’s behavior is optimal, or

rational. Economists have different attitudes toward this point. One can take the position that

consumer behavior is by definition optimal, because consumers control it. Therefore the demand

PROBLEMS

1. The table shows the maximum amount of money you would be willing to pay for

increasing numbers of chicken pieces at Fastfood.

Chicken Pieces Maximum Payment

1 $2.00

2 3.80

3 5.40

4 6.80

5 8.00

6 9.00

7 9.80

8 10.40

9 10.80

10 11.00

11 11.00

a) Find the marginal utility for each chicken piece. What is the meaning of the marginal

utility of the 11th piece?

b) If the price of chicken pieces is $1.25 each, how many will you buy?

c) If the price falls to $0.50, how many will you buy? Explain carefully why you will

not buy one more.

Chapter 5/Consumer Choice: Individual and Market Demand

d) Suppose now that Fastfood stops selling chicken pieces individually, and only sells

them in 5-Packs. The price of a 5-Pack is $2.50. How many chicken pieces will you

consume? Reconcile your answers to c) and d).

e) What is the consumer surplus, or net benefit, that you get from purchasing chicken

pieces at $0.50 as in c)?

Solution:

a)

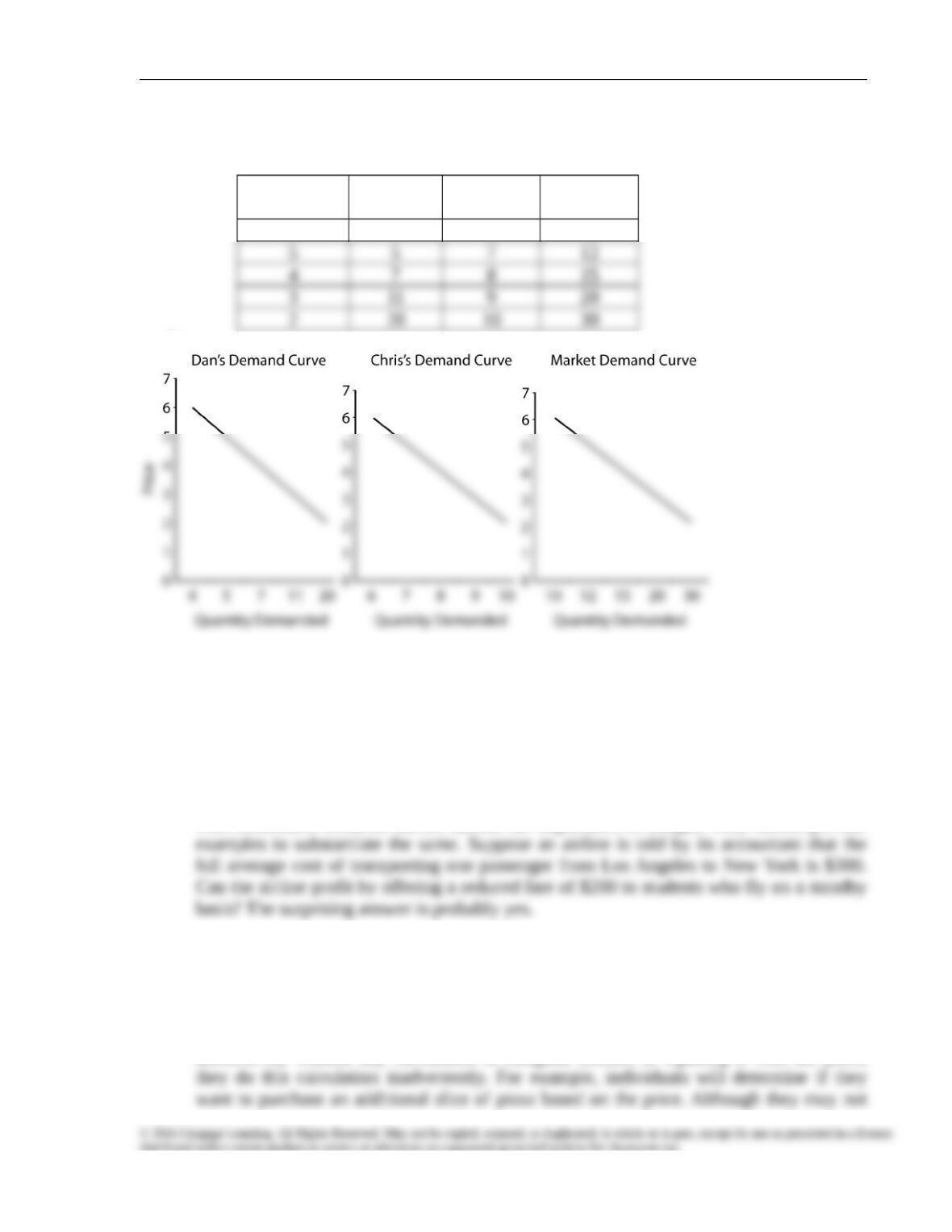

2. The price of whole chickens varied between $2 and $6; Dan and Chris will purchase the

following numbers this year:

Dan’s Chris’

Price Quantity Quantity

$6 4 6

557

478

3 11 9

2 20 10

a) If Dan and Chris are the only two buyers, calculate the market demand curve.

b) On graph paper, draw the demand curves for Dan, for Chris, and for the market.

Chicken

Pieces

Maximum

Payment

Marginal

Utility

1 $2.00 $2.00

2 3.80 1.80

3 5.40 1.60

Chapter 5/Consumer Choice: Individual and Market Demand

Solution:

a)

Price(in $)

Dan’s

Quantity

Chris’

Quantity

Market

Demand

6 4 6 10

b)

DISCUSSION QUESTIONS

1. “Economists are wrong to pay so much attention to the margin, to the last unit of a good

that is bought. The last unit is the least important. They should focus their attention on the

more important earlier units.” Discuss.

Suggested Answer: This statement might look correct to someone who is not familiar

with economics. Students should discuss the importance of margin. They should provide

2. “Perhaps economists consciously equate marginal utility with price as they are shopping

for groceries, but I am sure no one else does, and I suspect even they slip up. It is

ridiculous to describe consumer behavior in terms of a theory that consumers have never

even heard of.” Discuss.

Suggested Answer: Even though buyers may seem to make decisions much more

instinctively without any calculation of marginal utilities or equating it with the price,

Chapter 5/Consumer Choice: Individual and Market Demand

3. “The text explains that consumers who follow the optimal purchase rule will behave such

that their demand curve for a good is the same as their marginal utility curve. This is an

interesting but not very relevant piece of information. Consumers do not follow an

optimal purchase rule. They buy on impulse, and they often buy things that do them no

good. It is a serious mistake to develop models based on the assumption that human

behavior is rational.” Discuss.

Suggested Answer: Students should attempt to identify models based on the assumption

that human behavior is rational. Note that price is an objective, observable figure

determined by the market, whereas marginal utility is subjective and reflects consumer

4. “Price has nothing to do with utility or value. Tickets to the worst Broadway play cost

$50, while tickets to Oscar-winning movies cost no more than $10. I rest my case.”

Discuss.

Suggested Answer: This question is aimed at revealing the importance of marginal

analysis in economics. The price of a commodity depends on what that good is worth to