Chapter 10/The Firm and the Industry under Perfect Competition

CHAPTER 10

THE FIRM AND THE INDUSTRY UNDER

PERFECT COMPETITION

Chapter 10 develops the model of the perfectly competitive firm and the perfectly competitive

industry. It stresses the zero profit condition for long-run equilibrium.

CHAPTER OUTLINE

PERFECT COMPETITION DEFINED

Perfect competition exists when:

1. There are numerous small firms and customers.

2. The product of all the firms is homogeneous.

THE PERFECTLY COMPETITIVE FIRM

Under perfect competition the firm is a price taker. The firm has no choice but to accept the

price that has been determined by the market.

The Firm’s Demand Curve under Perfect Competition

A perfectly competitive firm faces a horizontal demand curve. It can sell as much as it wants

at the market price.

Short-Run Equilibrium for the Perfectly Competitive Firm

Because the demand curve is horizontal (i.e., the firm is a price taker), the firm’s demand

Short-Run Profit: Graphic Representation

A graph can be drawn to show the profit-maximizing output, together with the actual profit

level.

The Case of Short-Term Losses

The profit-maximizing output may lead to a loss, but if so it is the minimum possible loss.

Chapter 10/The Firm and the Industry under Perfect Competition

Shutdown and Break-Even Analysis

Rule 1: The firm will make a loss if total revenue (TR) is less than total cost (TC). In that

case, it should plan to shut down, either in the short run or the long run.

The Perfectly Competitive Firm’s Short-Run Supply Curve

The short-run supply curve is the portion of the marginal cost curve that lies above the

FARMING ECONOMICSL UNPREDICTABLE WEATHER DRIVES

DOWN CORN PRICES

Because farmers operate within a perfectly competitive market then they are price takers.

THE PERFECTLY COMPETITIVE INDUSTRY

The Perfectly Competitive Industry’s Short-Run Supply Curve

Summing the short-run supply curves of all the firms in the industry horizontally derives the

short-run supply curve of the competitive industry.

Industry Equilibrium in the Short Run

A competitive industry has a stable equilibrium at the output where supply equals demand.

Industry and Firm Equilibrium in the Long Run

In the long run, firms enter or exit the industry in response to profits or losses.

Zero Economic Profit: The Opportunity Cost of Capital

Economic costs include opportunity costs, so zero economic profit means that firms are

The Long-Run Industry Supply Curve

The long-run supply curve of the perfectly competitive industry is also the industry’s

long-run average cost curve.

Chapter 10/The Firm and the Industry under Perfect Competition

PERFECT COMPETITION AND ECONOMIC EFFICIENCY

In the long run, perfectly competitive firms are driven to produce at the minimum point of

their average cost curves.

In this case, output is produced at the lowest possible cost to society.

WHICH MORE EFFECTIVELY CUTS POLLUTION: THE CARROT OR

THE STICK?

The analysis of perfect competition can be used to show that if firms are offered a subsidy to

MARGIN DEFINITIONS

Perfect Competition: occurs in an industry when that industry is made up of many small firms

producing homogeneous products, when there is no impediment to entry or exit of firms, and

when full information is available.

Price Taker: a firm that has no choice but to accept the price that has been determined in the

market.

Variable Cost: a cost whose total amount changes when the quantity of output of the supplier

changes.

MAJOR IDEAS

1. The demand curve of the perfectly competitive firm is horizontal because so many other

firms are selling identical products and the firm’s output is so small a share of the

industry’s production that it cannot affect price (i.e., the firm is a price-taker). With a

horizontal demand curve, price, average revenue, and marginal revenue are all equal.

2. The short-run equilibrium of the perfectly competitive firm is at the level of output that

ON TEACHING THE CHAPTER

There is a lot of material in Chapter 10 and it is important material, not so much because of its

correspondence to reality, but for other reasons. It is an application of the principles of Chapter 8,

and helps to reinforce those principles. Furthermore, the case of pure competition constitutes a

Chapter 10/The Firm and the Industry under Perfect Competition

standard by which other market structures can be judged. The presentation flows so logically that

students should be able to understand the basics fairly easily.

A most interesting point to ponder in class is the zero profit condition for long-run

equilibrium of the industry. It is a different kind of equilibrium condition than the text has dealt

PROBLEMS

1. The price of strawberries is $10 a bucket. Three competitive strawberry farmers, Jones,

Garcia, and Moon, face different cost conditions:

Total Cost (thousands of dollars)

Thousands

of Buckets Jones Garcia Moon

10 100 275 50

20 200 335 125

30 300 400 225

40 400 470 350

50 500 545 500

60 600 625 675

70 700 710 875

80 800 800 1100

a) For each farmer, calculate the marginal cost at each output level.

b) Describe in words the difference between the cost schedules of the three farmers.

c) What are the profit-maximizing output levels of the three farmers, and what are their

profits at those outputs?

d) Explain the differences and/or similarities in the outputs and profits of the three

farmers.

Chapter 10/The Firm and the Industry under Perfect Competition

Solution:

a)

Marginal Cost

Thousand

s

of buckets

Thousands of dollars

Jones Garcia Moon

10 10 5.5 5

20 10 6 7.5

b) Total cost and marginal cost are different for the three farmers. For Jones, marginal

cost is fixed at various levels of output. As output increases, marginal cost decreases

2. Farmer Dorr figures that her fixed costs are $2,000, and the relevant portion of her total

cost curve is:

Thousands of Total Cost

Bushels (in thousands of dollars)

10 10.70

11 11.45

12 12.25

13 13.10

14 14.00

15 15.00

16 16.10

17 17.32

18 18.75

19 20.30

a) Calculate Farmer Dorr’s schedules of average cost, marginal cost, total variable cost,

and average variable cost.

b) If Farmer Dorr is a perfect competitor, what level of output should she produce, and

what will her profits be, if the market price is:

(i) $1.50 (iii) $0.92

(ii) $1.00 (iv) $0.82

Chapter 10/The Firm and the Industry under Perfect Competition

Solution:

a)

Outpu

t

Total

cost AC MC TVC AVC

10 10.7 1.07 — 8.7 0.87

11 11.45 1.04 0.75 9.45 0.86

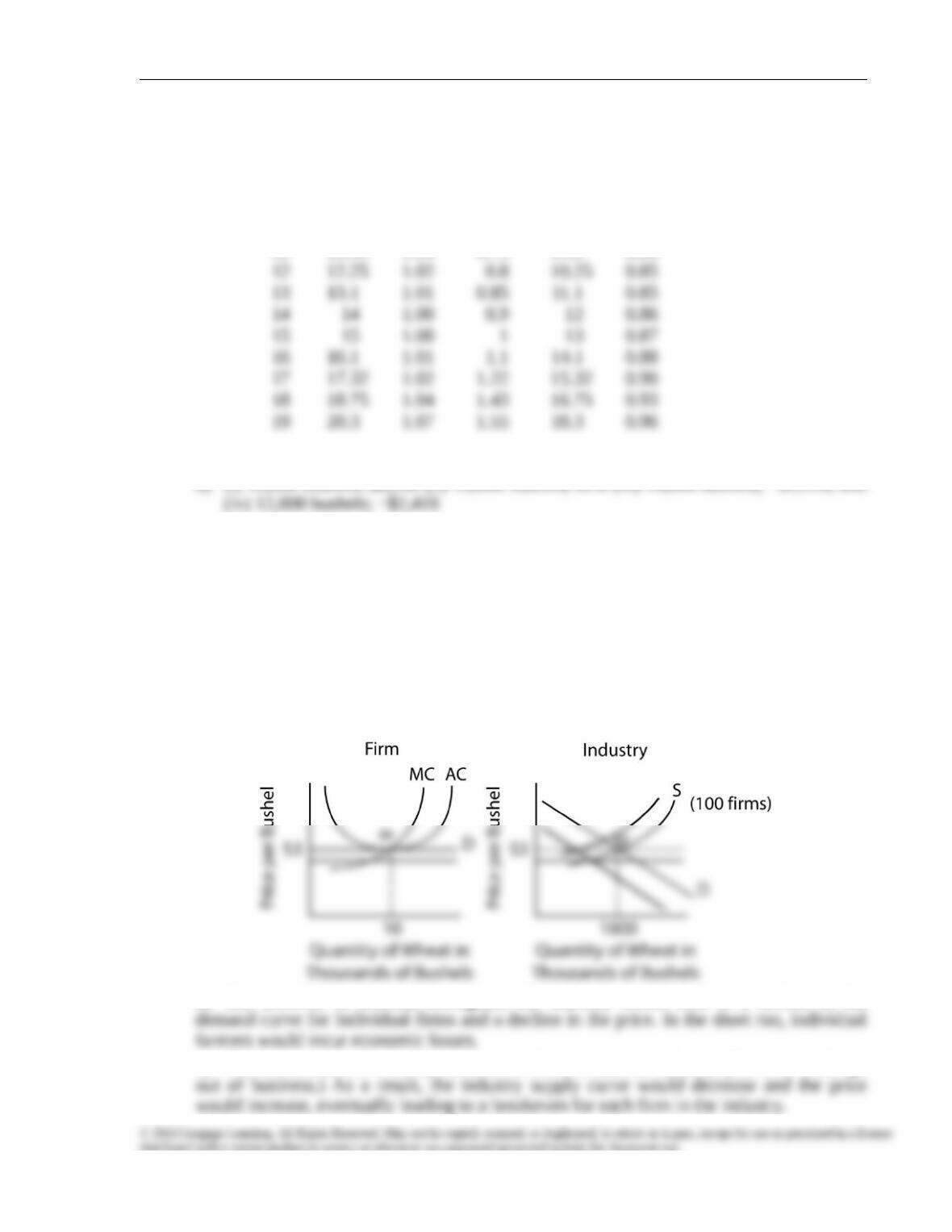

3. a) Draw the relevant diagrams for a typical farm, and for the market as a whole, when

the market for wheat is in long-run equilibrium.

b) Changes in tastes reduce the demand for wheat substantially. What happens to price

and output in the market for wheat? What happens to the price, output, and profits of

the individual wheat farmer in the short run? Illustrate with diagrams.

c) How does the market move to a new long-run equilibrium? Using diagrams, show the

new price and quantity of wheat in the market. Show also the new price, output, and

profits of the individual farmer.

Solution

a)

b) The decrease in demand throughout the industry would lead to a decline in the

c) The losses would eventually cause some firms to exit the industry. (Farmers would go

Chapter 10/The Firm and the Industry under Perfect Competition

4. Xander Harris is considering whether to buy a corn and soybean farm in Iowa. The farm

will cost $800,000, and Xander will be able to pay this from profits his recently deceased

mother made on the stock market and willed to him. He estimates that if he does not run

the farm, and keeps his current job as an economic forecaster, he will be able to earn

$40,000 a year. The prevailing interest rate is 9 percent. Xander’s only motive is to

maximize his income.

a) From the accounting perspective only, should he buy the farm and become a farmer if

his accountant tells him the annual profit from the farm is likely to be:

i) $160,000?

ii) $100,000?

iii) $50,000?

b) Because he is currently an economist, Xander decides to re-calculate the profit figures

according to the logic used by economists rather than accountants. What profit figures

does he come up with? Do these new figures cause him to change his mind about

becoming a farmer?

Solution:

a) Yes in all three cases (from an accounting viewpoint)

DISCUSSION QUESTIONS

1. Under what circumstances will drought help or hurt a farmer?

Suggested Answer: Students should discuss the effects of drought on an economy,

especially on farming, and possible government actions such as price ceilings and

2. When demand rises in a perfectly competitive market, do you think the long-run

equilibrium price will rise, fall, or stay constant? What will determine this?

Suggested Answer: In a perfectly competitive market, its long-run equilibrium price will

3. What examples of perfectly competitive markets can you think of in the economy?

Suggested Answer: Students should come up with their own examples that approximate

4. The text states that four conditions are necessary for the existence of a perfectly

competitive market. Discuss each one.

a) Numerous participants: Roughly how many sellers do you think are needed to make a

market perfectly competitive?

Chapter 10/The Firm and the Industry under Perfect Competition

b) Homogeneity of product: How would perfect competition be altered if buyers could

distinguish between the products of different producers?

c) Freedom of entry and exit: How might this condition be violated? What sorts of

barriers to entry or exit might exist?

d) Perfect information: What exactly needs to be known, and by whom, in order to make

competition perfect?

Suggested Answer:

a) The number of participants should be enough to ensure that no participant has control