46. a. The computer output with the missing values filled in is as follows:

Regression Statistics

Multiple R

0.9607

R Square

0.923

Adjusted R Square

0.9102

Standard Error

3.35

Observations

15

ANOVA

df

SS

MS

F

Significance F

Regression

2

1612

806

71.82

2.10068E-07

Residual

12

134.67

11.2225

Total

14

1746.67

Coefficients

Standard Error

t Stat

P-value

Intercept

8.103

2.667

3.0382

0.0103

X1

7.602

2.105

3.6114

0.0036

X2

3.111

0.613

5.0750

0.0003

ˆ

y

= 8.103 + 7.602 X1 + 3.111 X2

b. The p-value (2 degrees of freedom numerator and 12 denominator) corresponding to F = 71.82 is

.0000

Because the p-value ≤ α = .05, there is a significant relationship.

47. a. The regression equation is

Regression Statistics

Multiple R

0.9681

R Square

0.9373

Adjusted R Square

0.9194

Standard Error

0.1298

Observations

10

ANOVA

df

SS

MS

F

Significance F

Regression

2

1.7621

0.8810

52.3053

6.17838E-05

Residual

7

0.1179

0.0168

Total

9

1.88

Coefficients

Standard Error

t Stat

P-value

Intercept

-1.4053

0.4848

-2.8987

0.0230

X1

0.0235

0.0087

2.7078

0.0303

X2

0.0049

0.0011

4.5125

0.0028

b. F = 52.3053

p-value (2 degrees of freedom numerator and 7 degrees of freedom denominator) = .0000

Because the p-value ≤ α = .05, there is a significant relationship.

2SSR .937

For

: the p-value corresponding to t = 4.5125 is .0028

Because the p-value is ≤ α = .05, reject H0:

= 0

48. a. The regression equation is

Regression Statistics

Multiple R

0.9493

R Square

0.9012

Adjusted R Square

0.8616

Standard Error

3.773

Observations

8

ANOVA

df

SS

MS

F

Significance F

Regression

2

648.83

324.415

22.7916

0.0031

Residual

5

71.17

14.234

Total

7

720

Coefficients

Standard Error

t Stat

P-value

Intercept

14.4

8.191

1.7580

0.1391

X1

-8.69

1.555

-5.5884

0.0025

X2

13.517

2.085

6.4830

0.0013

ˆ

y

= 14.4 – 8.69 X1 + 13.517 X2

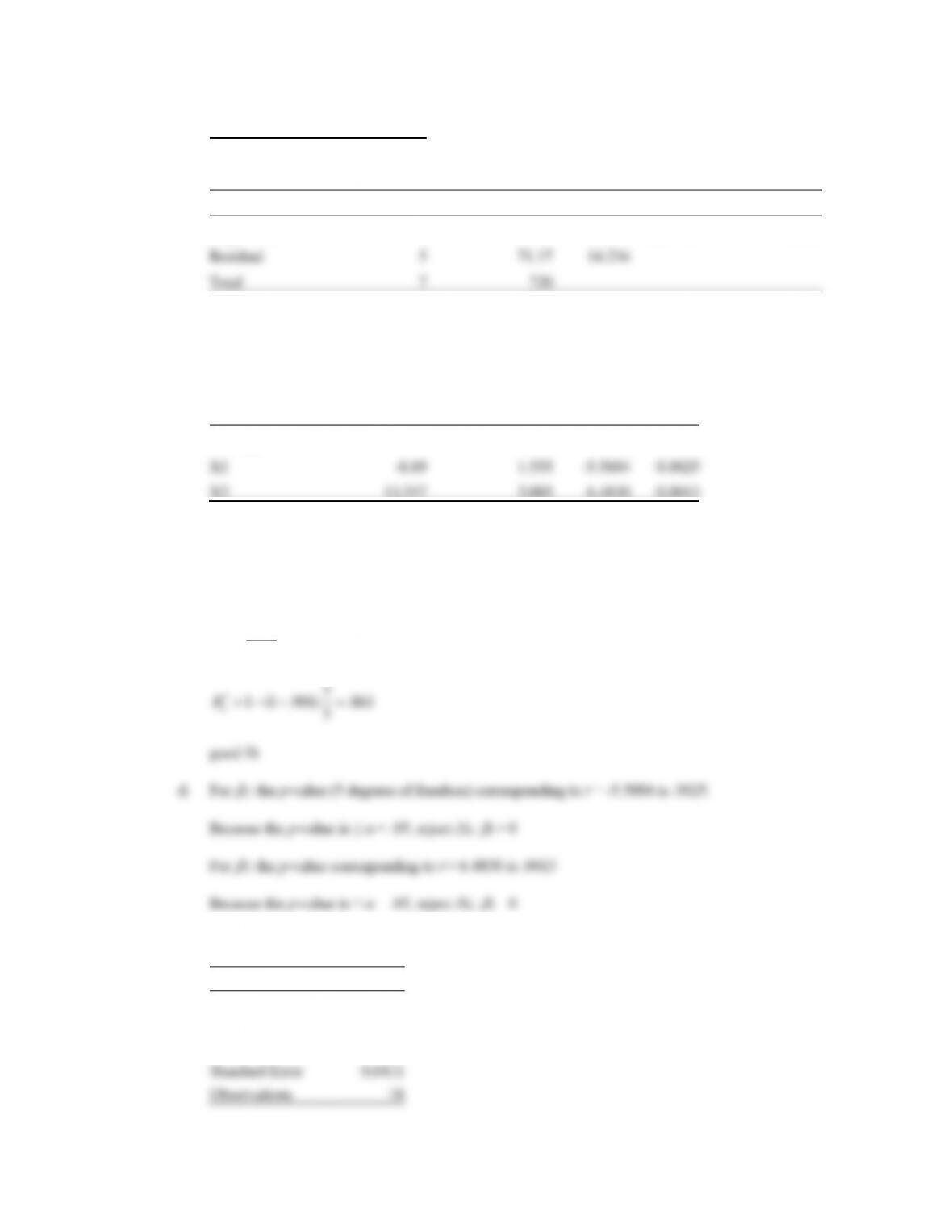

b. The p-value (5 degrees of freedom) corresponding to F = 22.7916 is .0031

Because the p-value is ≤ α = .05, there is a significant relationship.

c.

2SSR .901

SST

R==

27

49. a. A portion of the Excel output follows:

Regression Statistics

Multiple R

0.9182

R Square

0.8430

Adjusted R Square

0.8332

Standard Error

0.8411

Observations

18

ANOVA

df

SS

MS

F

Significance F

Regression

1

60.7866

60.7866

85.9295

7.80448E-08

Residual

16

11.3184

0.7074

Total

17

72.105

Coefficients

Standard Error

t Stat

P-value

Lower 95%

Upper 95%

Intercept

-7.5218

1.4668

-5.1282

0.0001

-10.6312

-4.4124

Steering

1.8151

0.1958

9.2698

7.804E-08

1.4000

2.2302

ˆ

y

Because the p-value = .000 < α = .05, there is a significant relationship.

b. The estimated regression equation provided a good fit; 84.3 % of the variability in the Buy Again

rating was explained by the linear effect of the Steering rating.

c. A portion of the Excel output follows:

Regression Statistics

Multiple R

0.9653

R Square

0.9318

Adjusted R Square

0.9227

Standard Error

0.5727

Observations

18

ANOVA

df

SS

MS

F

Significance F

Regression

2

67.1848

33.5924

102.4121

1.79936E-09

Residual

15

4.9202

0.3280

Total

17

72.105

Coefficients

Standard Error

t Stat

P-value

Lower 95%

Upper 95%

Intercept

-5.3877

1.1095

-4.8558

0.0002

-7.7526

-3.0228

Steering

0.6899

0.2875

2.3992

0.0299

0.0770

1.3028

Tread Wear

0.9113

0.2063

4.4166

0.0005

0.4715

1.3511

The estimated regression equation is

ˆ

y

= – 5.3877 + 0.6899 Steering + 0.9113 Treadwear

d. For the Treadwear independent variable, the p-value = .0005 < α = .05; thus, the addition of

Treadwear is significant.

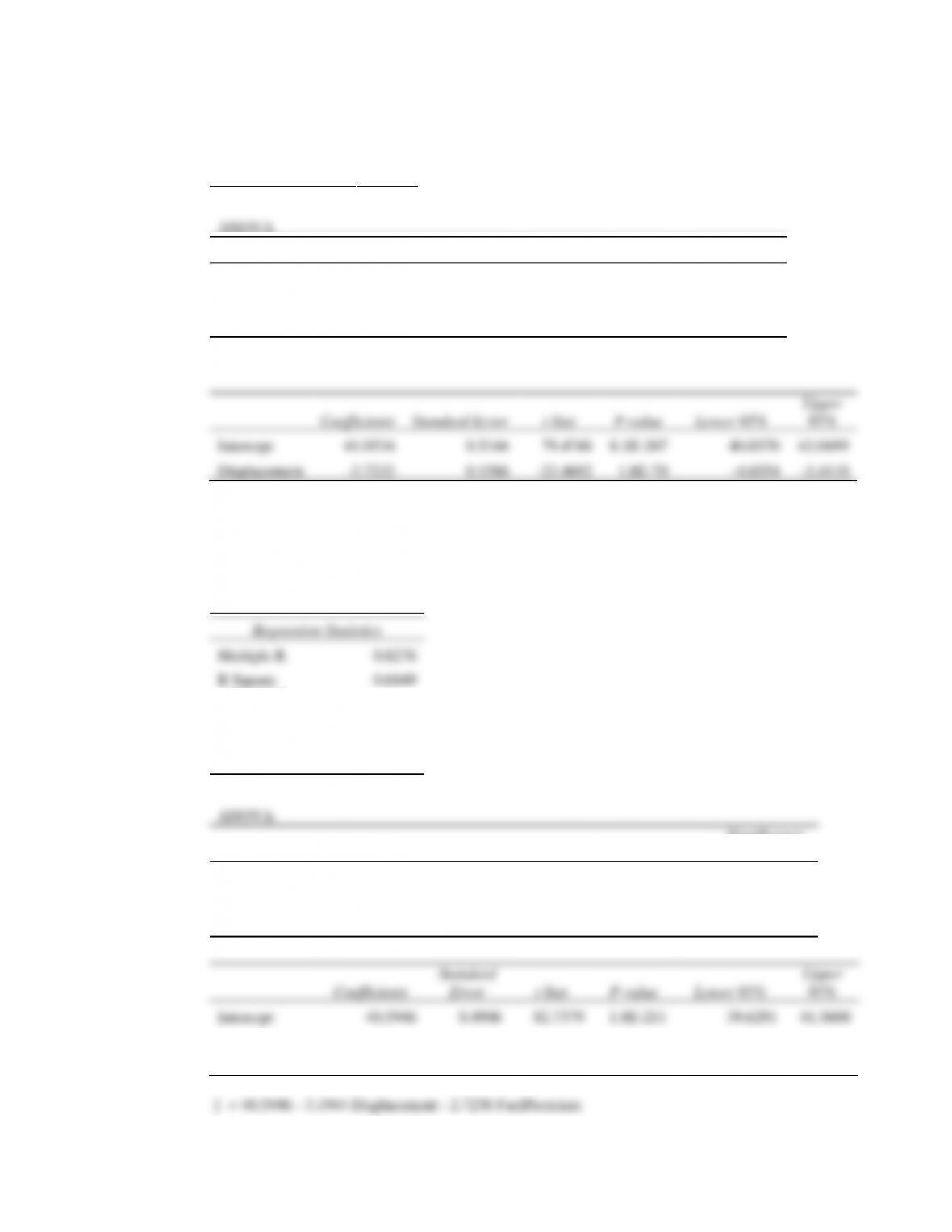

50. a. A portion of the Regression tool output follows.

Regression Statistics

Multiple R

0.8013

R Square

0.6421

Adjusted R Square

0.6409

Standard Error

3.4123

Observations

309

ANOVA

df

SS

MS

F

Significance F

Regression

1

6413.2883

6413.2883

550.8029

1.79552E-70

Residual

307

3574.5628

11.6435

Total

308

9987.8511

Coefficients

Standard Error

t Stat

P-value

Lower 95%

Upper

95%

Intercept

41.0534

0.5166

79.4748

8.1E-207

40.0370

42.0699

Displacement

-3.7232

0.1586

-23.4692

1.8E-70

-4.0354

-3.4110

ˆ

y

= 41.0534 ˗ 3.7232 Displacement

Because the p–value corresponding to F = 550.8029 is .0000 <

= .05, there is a significant

relationship.

b. A portion of the Excel Regression tool output follows.

Regression Statistics

Multiple R

0.8276

R Square

0.6849

Adjusted R

Square

0.6829

Standard Error

3.2068

Observations

309

ANOVA

df

SS

MS

F

Significance

F

Regression

2

6841.0876

3420.5438

332.6232

1.79466E-77

Residual

306

3146.7635

10.2835

Total

308

9987.8511

Coefficients

Standard

Error

t Stat

P-value

Lower 95%

Upper

95%

Intercept

40.5946

0.4906

82.7379

1.8E-211

39.6291

41.5600

Displacement

-3.1944

0.1701

-18.7745

7.43E-53

-3.5292

-2.8596

FuelPremium

-2.7230

0.4222

-6.4498

4.37E-10

-3.5537

-1.8922

ˆ

y

c. For FuelPremium, the p-value corresponding to t = -6.4498 is .000 < = .05; significant. The

addition of the dummy variables is significant.

d. A portion of the Excel Regression tool output follows.

ANOVA

df

SS

MS

F

Significance F

Regression

2

2096.8489

1048.4245

33.4584

2.03818E-09

Residual

42

1316.0771

31.3352

Total

44

3412.9260

Coefficients

Standard Error

t Stat

P-value

Lower 95%

Upper 95%

Intercept

4.9090

1.7702

2.7732

0.0082

1.3366

8.4814

FundDE

10.4658

2.0722

5.0505

9.033E-06

6.2839

14.6477

FundIE

21.6823

2.6553

8.1658

3.288E-10

16.3237

27.0408

The estimated regression equation is

ˆ

y

= 4.9090+ 10.4658 FundDE + 21.6823 FundIE

Since the p-value corresponding to F = 33.4584 is .0000 < α = .05, there is a significant relationship.

c. A portion of the Excel output follows:

Regression Statistics

Multiple R

0.8135

R Square

0.6617

Adjusted R Square

0.6279

Standard Error

5.3726

Observations

45

ANOVA

df

SS

MS

F

Significance F

Regression

4

2258.3432

564.5858

19.5598

5.48647E-09

Residual

40

1154.5827

28.8646

Total

44

3412.9260

Coefficients

Standard Error

t Stat

P-value

Lower 95%

Upper 95%

Intercept

1.1899

2.3781

0.5004

0.6196

-3.6164

5.9961

FundDE

6.8969

2.7651

2.4942

0.0169

1.3083

12.4854

FundIE

17.6800

3.3161

5.3315

4.096E-06

10.9778

24.3821

Net Asset Value ($)

0.0265

0.0670

0.3950

0.6950

-0.1089

0.1619

Expense Ratio (%)

6.4564

2.7593

2.3399

0.0244

0.8798

12.0331

ˆ

y

Since the p-value corresponding to F = 19.5558 is .0000 < α = .05, there is a significant relationship.

For Net Asset Value ($), the p-value corresponding to t = .3950 is .6950 > = .05, Net Asset Value

($) is not significant and can be deleted from the model.

d. Morningstar Rank is a categorical variable. The data set only contains funds with four ranks (2-Star

Regression Statistics

Multiple R

0.8501

R Square

0.7227

Adjusted R Square

0.6789

Standard Error

4.9904

Observations

45

ANOVA

df

SS

MS

F

Significance F

Regression

6

2466.5721

411.0954

16.5072

2.96759E-09

Residual

38

946.3539

24.9040

Total

44

3412.9260

Coefficients

Standard Error

t Stat

P-value

Lower 95%

Upper 95%

Intercept

-4.6074

3.2909

-1.4000

0.1696

-11.2694

2.0547

FundDE

8.1713

2.2754

3.5912

0.0009

3.5650

12.7776

FundIE

19.5194

2.7795

7.0227

2.292E-08

13.8926

25.1461

Expense Ratio (%)

5.5197

2.5862

2.1343

0.0393

0.2843

10.7552

3StarRank

5.9237

2.8250

2.0969

0.0427

0.2048

11.6426

4StarRank

8.2367

2.8474

2.8927

0.0063

2.4725

14.0009

5StarRank

6.6241

3.1425

2.1079

0.0417

0.2624

12.9858

The estimated regression equation is

ˆ

y

= -4.6074 + 8.1713 FundDE + 19.5194 FundIE +5.5197 Expense Ratio (%) + 5.9237 3StarRank

+ 8.2367 4StarRank + 6.6241 5StarRank

At the .05 level of significance, all the independent variables are significant.

Total

29

7069.407

Coefficients

Standard Error

t Stat

P-value

Intercept

-407.9703

68.9533

-5.9166

4.18419E-06

FG%

4.9612

1.3676

3.6276

0.0013

3P%

2.3749

0.8074

2.9413

0.0071

FT%

0.0049

0.5182

0.0095

0.9925

RBOff

3.4612

1.3462

2.5711

0.0168

RBDef

3.6853

1.2965

2.8425

0.0090

ˆ

y

= ˗407.9703 + 4.9612 FG% + 2.3749 3P% + 0.0049 FT% + 3.4612 RBOff +

3.6853 RBDef

d. For the estimated regression equation developed in part (c), the percentage of free throws made

removing this independent variable, the Excel output is shown below:

Regression Statistics

Multiple R

0.8764

R Square

0.7680

Adjusted R

Square

0.7309

Standard Error

8.0993

Observations

30

ANOVA

df

SS

MS

F

Significance F

Regression

4

5429.4489

1357.3622

20.6920

1.24005E-07

Residual

25

1639.9581

65.5983

Total

29

7069.407

Coefficients

Standard Error

t Stat

P-value

Intercept

-407.5790

54.2152

-7.5178

7.1603E-08

FG%

4.9621

1.3366

3.7125

0.0010

3P%

2.3736

0.7808

3.0401

0.0055

RBOff

3.4579

1.2765

2.7089

0.0120

RBDef

3.6859

1.2689

2.9048

0.0076

ˆ

y

= –407.5790 + 4.9621 FG% + 2.3736 3P%+ 3.4579 RBOff + 3.6859 RBDef

e.

ˆ

y

= –407.5790 + 4.9621 FG% + 2.3736(35) + 3.4579(12) + 3.6859(30) = 50.86%