Principles of Finance 6e Chapter 9

Numerical solution:

r

1)r1(

PMTFVA

n

n

−+

=

Chapter 9 Principles of Finance 6e

Besley/Brigham

Future Value of the Annuity

Numerical solution:

)r1(

r

1)r1(

PMT)DUE(FVA

n

n

+

−+

=

Principles of Finance 6e Chapter 9

Besley/Brigham

9-37

0 1 2 3 4

90.91 100 300 300 –50

225.39

Numerical solution:

)r1(

1

CF

)r1(

1

CF

)r1(

1

CFPV

n

n

2

2

1

1

+

++

+

+

+

=

g. 0 1 2 3

Numerical solution:

%0.8080.00.1

00.100$

97.125$

r

)r1(100$97.125$

)r1(PVFV

3

1

3

n

==−

=

+=

+=

h. (1) Investments that pay interest more frequently than once per year, for example—

10%

r = ?

(2) The quoted, or simple, rate is merely the quoted percentage rate of return that is used to

compute the periodic rate of return—it is the same as the APR; the periodic rate is the rate

(3) The effective annual rate for 10 percent semiannual compounding, is 10.25 percent:

1.0 –

m

r

+ 1 = r

SIMPLE

m

EAR

360

(4) With semiannual compounding, the $100 is compounded over six semiannual periods at a

5.0 percent periodic rate:

1 2 3 Years

0 1 2 3 4 5 6 Six–month periods

–100 FV=?

Numerical Solution:

m

r

1PVFV

nm

SIMPLE

n

+=

Another approach here would be to use the effective annual rate and compound over

annual periods:

5%

Principles of Finance 6e Chapter 9

Besley/Brigham

9-39

i. If annual compounding is used, then the simple rate will be equal to the effective annual rate. If

more frequent compounding is used, the effective annual rate will be greater than the simple

rate. That is, rSIMPLE = rPER = rEAR when interest is compounded annually, whereas rSIMPLE < rEAR

when interest is compounded more than once per year.

0 1 2 3

100 100 100.00

or (2) treat the cash flows as an ordinary annuity, but use the effective annual rate:

10.25%. = 1 –

2

0.10

+ 1 = 1 –

m

r

+ 1 = r

2

SIMPLE

m

EAR

Now we have this three-period annuity:

5%

Chapter 9 Principles of Finance 6e

Besley/Brigham

9-40

0 1 2 3

100 100 100 100.00 = 100(1.1025)0

Numerical solution:

r

1)r1(

PMTFVA

n

n

−+

=

(2) 0 1 2 3

90.70 100 100 100

Numerical solution:

r

1

PMTPVA

n

)r1(

1

n

−

=+

5%

5%

(3) The payment stream is an annuity in the sense of constant amounts at regular intervals,

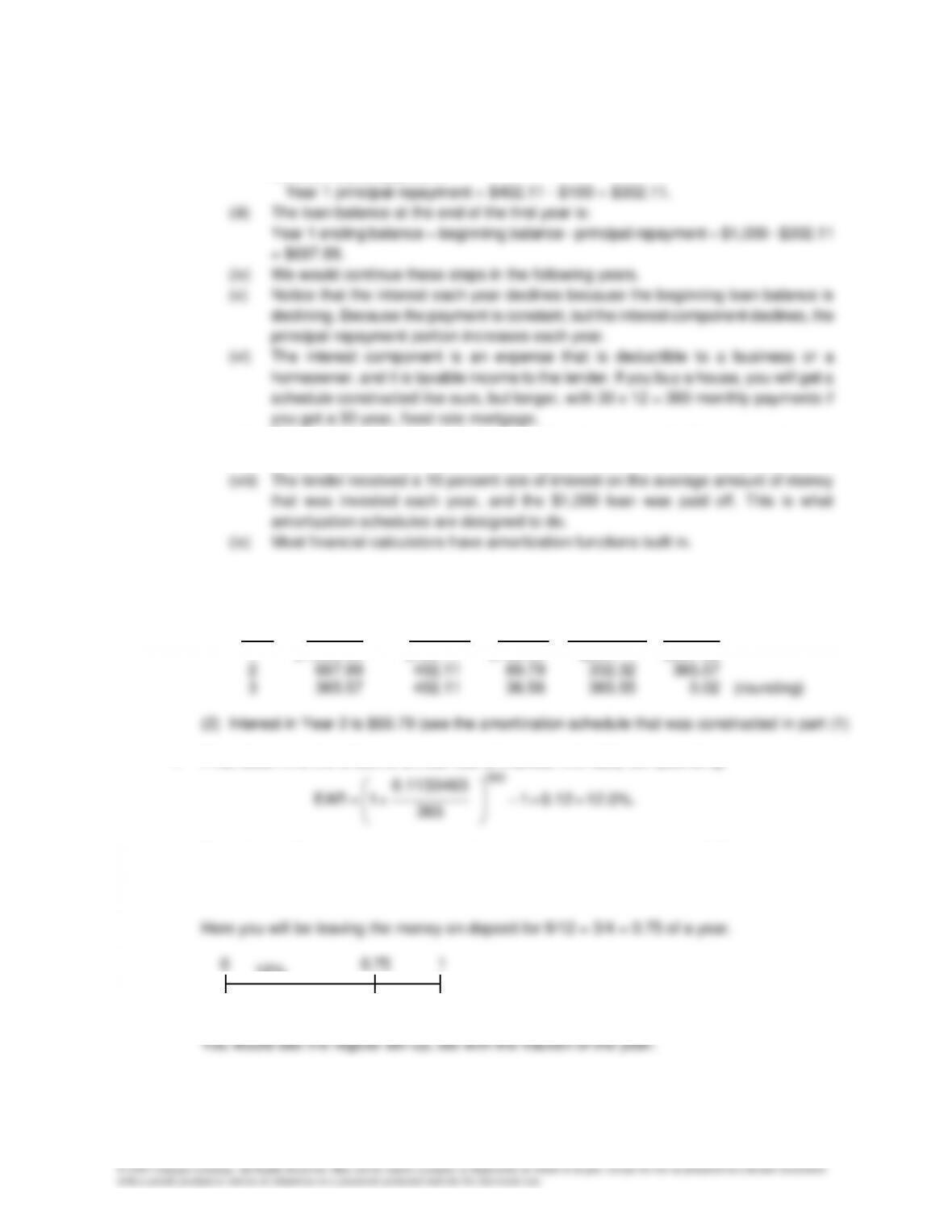

k. (1) To begin, note that the face amount of the loan, $1,000, is the present value of a three-year

annuity at a 10 percent rate:

0 1 2 3

–1,000 PMT PMT PMT

Numerical solution:

r

1

PMTPVA

n

)r1(

1

n

−

=+

10%

Chapter 9 Principles of Finance 6e

Besley/Brigham

9-42

(ii) The repayment of principal is the difference between the $402.11 annual payment

and the interest payment:

(vii) The payment might have to be increased by a few cents in the final year to take care

of rounding errors and make the final payment produce a zero ending balance.

The amortization schedule would be:

Beginning Interest Principal Ending

Year Balance Payment @ 10% Repayment Balance

1 $1,000.00 $402.11 $100.00 $302.11 $697.89

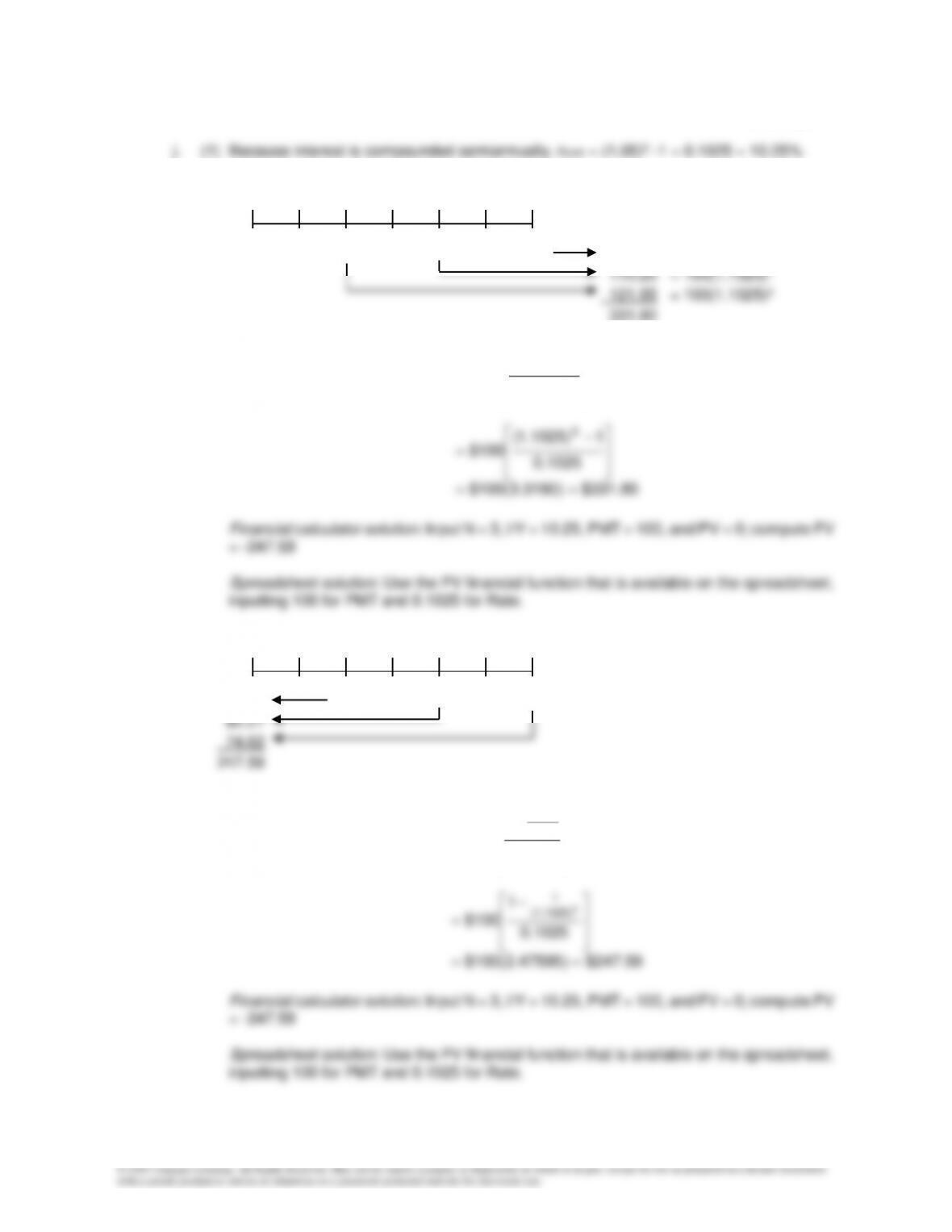

l. First, determine the effective annual rate of interest, with daily compounding:

12.0%. = 0.12 = 1

365

0.1133463

+ 1 = EAR

365

−

Thus, if you left your money on deposit for an entire year, you would earn $12 of interest, and

you would end up with $112. The question, however, is: How much will be in your account on

October 1, 2005?

–100 FV=? 112

12%

Principles of Finance 6e Chapter 9

Besley/Brigham

9-43

Numerical solution:

0 1 1.75 2 Years

–100 112 FV=? 125.44

Numerical solution:

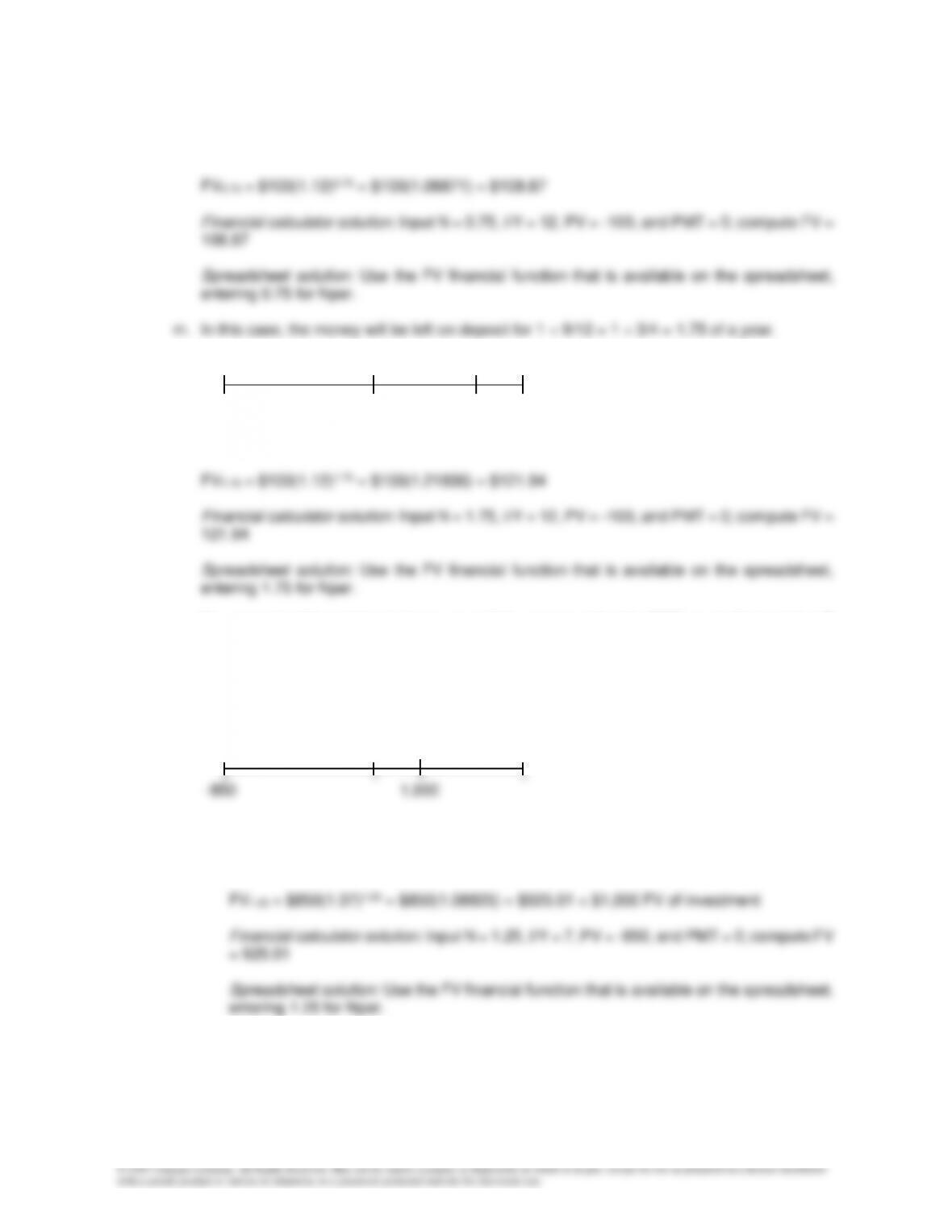

n. You can solve this problem in three ways: (1) by compounding the $850 now in the bank for 15

months and comparing that FV with the $1,000 the note will pay; (2) by finding the PV of the

note and then comparing it with the $850 cost; and (3) by finding the effective annual rate of

return on the note and comparing that rate with the 7 percent you are now earning, which is

your opportunity cost of capital. All three procedures lead to the same conclusion. Here is the

cash flow time line:

0 1 1.25 2 Years

(1) Future Value

Numerical solution:

(2) Present Value

12%

7%

Chapter 9 Principles of Finance 6e

Besley/Brigham

9-44

Numerical solution:

(3) Effective Annual Rate of the Investment

o. Here is the cash flow time line:

¼ ½ ¾ 1 1¼ Years

0 1 2 3 4 5 Quarters

(1) Future Value

Numerical solution:

1)0170585.1(

5

−

(2) Present Value

1.706%

Principles of Finance 6e Chapter 9

Besley/Brigham

9-45

Numerical solution:

25.903)75397.4(190$

0170585.0

1

190$PVA )0170585.1(

1

==

−

=

Financial calculator solution: Input N = 5, I/Y = 1.70585, PMT = 190, and FV = 0; compute

PV = -903.25

Spreadsheet solution: Use the PV financial function that is available on the spreadsheet.

(3) Effective Annual Rate of the Investment

−

=+

r

1

190$850$ )r1(

1

9-45 Computer-Related Problem

a. INPUT DATA: KEY OUTPUT:

Loan amount 30,000 Payment 3,523.79

Interest rate 10.00%

Number of years 20

MODEL-GENERATED DATA:

Amortization schedule:

Principal Remaining PV of

Year Payment Interest Repayment Balance Payments

1 3,523.79 3,000.00 523.79 29,476.21 3,203.44

2 3,523.79 2,947.62 576.17 28,900.04 2,912.22

3 3,523.79 2,890.00 633.78 28,266.26 2,647.47

Chapter 9 Principles of Finance 6e

Besley/Brigham

9-46

14 3,523.79 1,715.53 1,808.26 15,347.02 927.92

b. INPUT DATA: KEY OUTPUT:

Loan amount 60,000 Payment 7,047.58

Interest rate 10.00%

Number of years 20

MODEL-GENERATED DATA:

Amortization schedule:

Principal Remaining PV of

Year Payment Interest Repayment Balance Payments

1 7,047.58 6,000.00 1,047.58 58,952.42 6,406.89

2 7,047.58 5,895.24 1,152.34 57,800.09 5,824.44

11 7,047.58 4,330.43 2,717.15 40,587.17 2,470.13

12 7,047.58 4,058.72 2,988.86 37,598.31 2,245.58

13 7,047.58 3,759.83 3,287.75 34,310.56 2,041.43

14 7,047.58 3,431.06 3,616.52 30,694.04 1,855.85

15 7,047.58 3,069.40 3,978.17 26,715.86 1,687.13

c. INPUT DATA: KEY OUTPUT:

Loan amount 60,000 Payment 13,321.29

Interest rate 20.00%

Number of years 20

MODEL-GENERATED DATA:

Principles of Finance 6e Chapter 9

Besley/Brigham

9-47

Amortization schedule:

Principal Remaining PV of

Year Payment Interest Repayment Balance Payments

1 12,321.39 12,000.00 321.39 59,678.61 10,267.83

2 12,321.39 11,935.72 385.67 59,292.94 8,556.52

11 12,321.39 10,331.42 1,989.97 49,667.12 1,658.31

12 12,321.39 9,933.42 2,387.97 47,279.15 1,381.93

13 12,321.39 9,455.83 2,865.56 44,413.59 1,151.61

14 12,321.39 8,882.72 3,438.67 40,974.91 959.67

15 12,321.39 8,194.98 4,126.41 36,848.50 799.73

ETHICAL DILEMMA

It’s All Chinese to Me!

Ethical dilemma:

Terry Zupita must decide whether she should invest in Universal Autos, which is an American firm that is

partnering with the Chinese government to manufacture U.S. automobiles in China. If she makes the

investment, it appears that Ms. Zupita’s money will grow substantially during the next few years. However,

friends and relatives have told her that UA might use child labor in its Chinese plants, and that employees

often are abused in such plants. Should Terry purchase UA? If she does, she could be supporting

exploitation of children and mistreatment of employees.

Discussion questions:

• Is there an ethical problem? If so, what is it?

Chapter 9 Principles of Finance 6e

Besley/Brigham

© 2015 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed

with a certain product or service or otherwise on a password-protected website for classroom use.

9-48

comments she has heard about the treatment of Chinese employees in the UA plant in Shanghai.

• What are the implications if Terry invests in UA?

If the information about child labor and employee abuse are correct and Terry invests in UA, she would

• Should Terry invest in UA?

You might get some interesting responses to this question. Some students might say that it would be

immoral to invest in UA, given the rumors about its manufacturing plant in China. Others might say that

References:

The following articles might be assigned for background material:

Yochi J. Dreazen, “U.S. Investigates Firm Building Embassy in Iraq,” The Wall Street Journal, June 7, 2007,

A1+.

Betsy Atkins, “Is Corporate Social Responsibility Responsible?,” November 28, 2006, Forbes.com.

Ruth David, “Indian Law Does Little for Littlest Laborers,” October 10, 2006, Forbes.com.

Yochi J. Dreazen, “Probe Targets Ex–Navy Official for Link to Disgraced Contractor,” The Wall Street

Journal, May 5, 2006, A1+.

Deborah Orr, “Slave Chocolate?,” April 24, 2006, Forbes.com.